Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- MNI: Fed's Jefferson says raising 2% inflation goal could hurt Fed, Bbg

- MNI: UKRAINE: US' Yellen In Kyiv-'Severe Consequences' For China If It Arms Russia

- UK, EU REACH DEAL TO END BREXIT DISPUTE OVER NORTHERN IRELAND, Bbg

- ECB VUJCIC: AS LONG AS CORE INFLATION PERSISTS, WE MUST PERSEVERE, Bbg

- MORGAN STANLEY EXPECTS U.S. FED TO DELIVER FIRST INTEREST RATE CUT IN MARCH 2024 VS PREVIOUS FORECAST OF DECEMBER 2023 - Reuters

US TSYS: Tsy 2s Off Contract Lows

Tsy futures continue to bob around session highs after the bell, holding narrow range since rates bounced post Durables/Cap-Goods. Heavy spate of corporate debt issuance (over $19B over 17 names) provided two way hedging across the curve.

FI markets gained

- Rates gained earlier after larger drop in Jan durables new orders (-4.5% vs. -4.0%; Dec revised +5.1%) then scaled back from session highs following Pending Home Sales read for Jan at 82.5 up from 76.3 in Dec, +8.1 MoM well over 1.0% estimate. Futures reluctant to recede very far from session highs, however, 30YY 3.9097% (-.0194). Some technical buying in the mix as rates move off contract lows (TUH3 101-17.75 vs. 101-22.38 last).

- STIR: Fed funds implied hike for Mar'23 at 29.8bp, May'23 cumulative 55.8bp (-1.4) to 5.138%, Jun'23 73.2bp (-1.9) to 5.312%, terminal at 5.395-5.400 in Aug'23-Oct'23 (5.41-5.415% prior).

- Tuesday focus: Adv Goods, Wholesale Inv and MNI Chicago PMI.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00528 to 4.55643% (+0.00485 total last wk)

- 1M +0.02714 to 4.66200% (+0.04357 total last wk)

- 3M +0.00900 to 4.96243% (+0.03814 total last wk)*/**

- 6M +0.03600 to 5.27114% (-0.00786 total last wk)

- 12M +0.05272 to 5.69143% (-0.00415 total last wk)

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 4.96243% on 2/27/23

- Daily Effective Fed Funds Rate: 4.58% volume: $109B

- Daily Overnight Bank Funding Rate: 4.57% volume: $298B

- Secured Overnight Financing Rate (SOFR): 4.55%, $1.122T

- Broad General Collateral Rate (BGCR): 4.51%, $456B

- Tri-Party General Collateral Rate (TGCR): 4.51%, $442B

- (rate, volume levels reflect prior session)

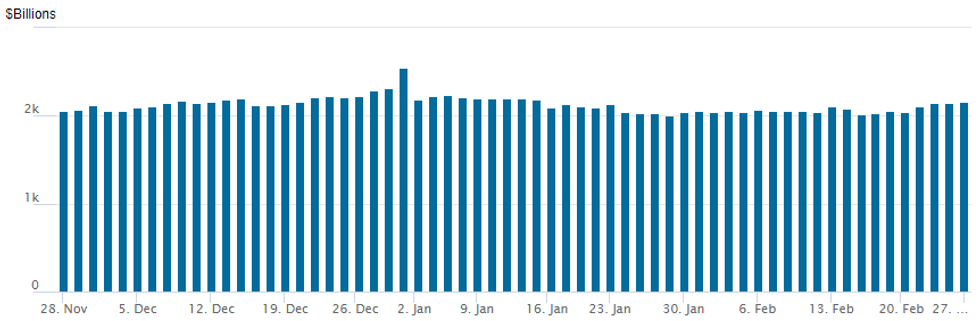

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage slips to $2,162.435B w/ 110 counterparties vs. prior session's $2,142.141B. Compares to Friday, Dec 30 record/year-end high of $2,553.716B (prior record high was $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Carry-over low delta put buying on net, discounting the modest bounce in underlying futures, looking to hedge dwindling rate cut pricing at least through 2023.- SOFR Options:

- Block, 7,500 SFRZ3 94.25/95.25 strangles, 31.5 ref 94.75

- Block, 5,000 OQJ3 95.25/95.37 put spds, 0.5 ref 95.475

- Block/pit, +9,000 2QH3/2QJ3 96.25 put, 6.5 apr over

- Block/pit, +20,000 SFRK3 94.37/94.50 put spds, 2.5 ref 94.645

- Block, 3,000 SFRZ3 94.75/95.12/95.50 4x9x5 put flys

- Block, 3,750 SFRU3 94.75/94.87/95.00 put flys on 4x9x5 ratio

- 12,000 OQJ3 95.37/95.62 put strip vs. 6,000 95.75/96.00 put strip

- Block, 15,000 OQM3 94.50/94.87/95.50 broken put flys, 17.5

- Block, 6,000 2QH3 96.50 puts, 25.5 ref 96.28

- over 3,900 SFRU3 95.00 calls, 8.5 ref 94.575

- 5,000 SFRU3 94.50/94.75/94.87/95.00 broken put condors ref 94.605

- Block, 10,000 OQM3 94.75/95.00/95.25 put flys, 3.0 vs. 95.43/0.10%

- Block, 10,000 OQU3 93.50/94.00/94.50 put flys, 2.5 vs. 95.775/0.05%

- Treasury Options:

- +15,000 TYJ3/wk1 TY 112.5 call spds, 24 vs. 111-10

- -8,000 FVJ3 105.75/108.25 put over risk reversals, 8.5 vs. 106-24

- over 3,800 FVJ 106 puts, 20.5

- 7,700 TYJ3 111.5/112.75 call spds vs. 110.25 puts, 1

FOREX: USD Downtick Puts Cumulative Volumes Ahead of Average For This Time of Day

- Dollar downdraft extends in recent trade, with both EUR/USD and GBP/USD hitting the session's best levels ahead of the London close. Comments from Fed's Jefferson do little to reverse the daily trend.

- Volumes picking up slightly on the latest move higher in USD pairs - EUR/USD futures saw just shy of 3,000 contracts change highs at the session high - that's a cash equivalent of approx $385mln.

- Latest bump higher in volumes puts today's activity ahead of average for this time of day. Cumulative volumes are now just over 10% ahead of average for this time of day.

Expiries for Feb28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0500(E1.3bln), $1.0520-30(E656mln), $1.0625-35(E559mln)

- USD/JPY: Y134.50-60($600mln), Y136.00($592mln), Y137.50($850mln)

- GBP/USD: $1.1850(Gbp854mln)

- AUD/USD: $0.7000-05(A$1.1bln)

- USD/CAD: C$1.3250($830mln), C$1.3415-25($650mln)

Late Equity Roundup: Consumer Discretionary, Industrials Outperform

Stocks firmer by the bell, back near opening levels, Consumer Discretionary and Industrials sectors still outperforming. SPX eminis currently trading +13 (0.33%) at 3989; DJIA +78.17 (0.24%) at 32896.3; Nasdaq +73.1 (0.6%) at 11468.76.

- SPX leading/lagging sectors: Consumer Discretionary (+1.20%) buoyed by automakers and component mfgs (TSLA +5.65%, F +2.02%, GM +0.43%; APTV +1.57%, BWA +0.86%). Industrials (+1.29) lead by road and rail shares (UNP +9.41, ODFL +1.1%).

- Laggers: Utilities (-0.55%), Real Estate (-0.17%) and Consumer Staples (-0.14%) underperformed in the second half, independent power and renewable energy shares weighing on the former (AES Corp -2.3%).

- Dow Industrials Leaders/Laggers: Caterpillar (CAT) +3.93 at 240.10, Boeing (BA) +2.52 to 200.67 after heavy sell-off last Fri, Goldman Sachs (GS) +2.43 at 366.28. Laggers: Walmart (WMT) -1.08 at 141.39, DOW -0.95 at 56.84, American Express (AXP) -0.61at 173.64.

- Earnings cycle starts to wind down next week, Occidental Petroleum after Mon's close (OXY 1.79 est), Advanced Auto Parts (AAP $2.42) and AutoZone (AZO $21.74) early Tuesday.

COMMODITIES

- WTI Crude Oil (front-month) down $0.67 (-0.88%) at $75.61

- Gold is up $5.75 (0.32%) at $1816.75

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/02/2023 | 0030/1130 | ** |  | AU | Retail Trade |

| 28/02/2023 | 0030/1130 | | AU | Balance of Payments: Current Account | |

| 28/02/2023 | 0700/0800 | ** |  | SE | PPI |

| 28/02/2023 | 0700/0800 | *** | | SE | GDP |

| 28/02/2023 | 0745/0845 | ** |  | FR | Consumer Spending |

| 28/02/2023 | 0745/0845 | *** | | FR | HICP (p) |

| 28/02/2023 | 0745/0845 | ** | | FR | PPI |

| 28/02/2023 | 0745/0845 | *** | | FR | GDP (f) |

| 28/02/2023 | 0800/0900 | *** |  | CH | GDP |

| 28/02/2023 | 0800/0900 | *** |  | ES | HICP (p) |

| 28/02/2023 | 0800/0900 | * | | CH | KOF Economic Barometer |

| 28/02/2023 | 1015/1015 |  | UK | BOE Treasury Select Committee hearing: The crypto-asset industry | |

| 28/02/2023 | 1215/1215 | | UK | BOE Pill Closes BEAR Research Conference | |

| 28/02/2023 | 1230/1230 | | UK | BOE Mann Panellist at EIB Forum | |

| 28/02/2023 | 1330/0830 | *** |  | CA | CA GDP by Industry and GDP Canadian Economic Accounts Combined |

| 28/02/2023 | 1330/0830 | * | | CA | Capital and repair expenditure survey |

| 28/02/2023 | 1330/0830 | ** |  | US | Advance Trade, Advance Business Inventories |

| 28/02/2023 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 28/02/2023 | 1400/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 28/02/2023 | 1400/0900 | ** | | US | FHFA Home Price Index |

| 28/02/2023 | 1400/0900 | ** | | US | FHFA Quarterly Price Index |

| 28/02/2023 | 1445/0945 | ** | | US | MNI Chicago PMI |

| 28/02/2023 | 1500/1000 | *** | | US | Conference Board Consumer Confidence |

| 28/02/2023 | 1500/1000 | ** | | US | Richmond Fed Survey |

| 28/02/2023 | 1530/1030 | ** | | US | Dallas Fed Services Survey |

| 28/02/2023 | 1930/1430 | | US | Chicago Fed's Austan Goolsbee |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.