HIGHLIGHTS

- Treasuries look to finish firmer Friday, trading sideways since extending session highs by midmorning.

- Despite initial price volatility, Tsys held gains amid general consensus that inflation has cooled slightly as PCE Price Index slipped to 2.5% from 2.6% prior YoY.

- Drawing some profit taking sales in late trade, stocks look to finish higher, the Dow outperforming S&P Eminis and Nasdaq as Industrials climbed to one week highs.

US Tsys Near Session Highs After Inflation Measure Cools Slightly

- Treasuries look to finish broadly higher Friday - trading sideways since climbing to session highs by midmorning amid a general consensus that inflation has cooled slightly as PCE Price Index slipped to 2.5% from 2.6% prior YoY.

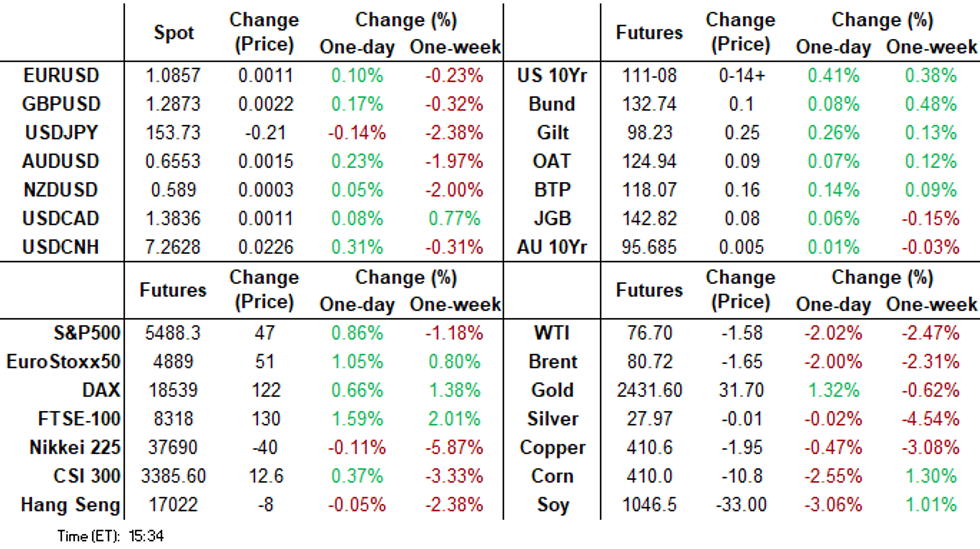

- Tsy Sep'24 10Y futures currently trade 111-08 last (+14.5) vs. 111-08.5, below initial technical resistance of 111-13+/17+ (High Jul 16 / 1.382 of Apr 25-May 16-29 swing).

- Early data-driven volatility saw Treasury futures alternately gap higher, lower and back higher, in turn extending overnight low/high end of the range after latest Personal Income comes out lower than expected, Personal Spending in-line while the prior was up-revised.

- Core PCE inflation ended up being very much as analysts expected in June, at 0.18% M/M (detailed post-CPI and PPI estimates had averaged around 0.17%). Instead, yesterday’s upside surprise for Q2 was primarily concentrated in May.

- Little overall reaction to the University of Michigan data: 1Y inflation: confirmed at 2.9% (cons and prelim 2.9) in July after 3.0% in June; 5-10Y inflation: surprisingly revised up to unchanged at 3.0% (cons and prelim 2.9) in July.

- Support and mildly steeper curves (2s10s +0.629 at -18.573), projected rate cut pricing into year end look steady to mildly higher vs. pre-data levels (*): July'24 at -4.5% w/ cumulative at -1.1bp at 5.318%, Sep'24 cumulative -28.4bp (-27.8bp), Nov'24 cumulative -45.1bp (-44.6bp), Dec'24 -67.9bp (-67.2bp).

- Focus on the week ahead ahead: Monday kicks off with Dallas Fed Mfg Activity at 1030 followed by the US Tsy Borrowing estimates at 1500ET. The TSY quarterly refunding annc is on Wed at 0830ET, along with ADP, PMI and the next FOMC policy annc. Next Friday sees the July nonfarm payrolls data.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00214 to 5.34712 (+0.00069/wk)

- 3M -0.01565 to 5.26356 (-0.01943/wk)

- 6M -0.03153 to 5.10750 (-0.02718/wk)

- 12M -0.04955 to 4.76862 (-0.03164/wk)

- Secured Overnight Financing Rate (SOFR): 5.35% (+0.01), volume: $2.129T

- Broad General Collateral Rate (BGCR): 5.34% (+0.01), volume: $813B

- Tri-Party General Collateral Rate (TGCR): 5.34% (+0.01), volume: $791B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $88B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $226B

FED Reverse Repo Operation

NY Federal Reserve/MNI

RRP usage inches up to $381.257B from $377.433B on Thursday. Number of counterparties at 70 from 69 prior. Today's usage compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

SOFR/TEASURY OPTION SUMMARY

SOFR and Treasury options continued to favor upside call buying, carry-over from the prior session on lighter volumes compared to Thursday's flow. Note: TYU4 112 call open interest up over 100k to 179,634 after yesterday's scale buying supported skew and implied vol. Underlying futures are trading firmer, while projected rate cut pricing into year end look steady to mildly higher vs. pre-data levels (*): July'24 at -4.5% w/ cumulative at -1.1bp at 5.318%, Sep'24 cumulative -28.4bp (-27.8bp), Nov'24 cumulative -45.1bp (-44.6bp), Dec'24 -67.9bp (-67.2bp).- SOFR Options:

- -1,500 2QU/3QV 96.50 straddle spds, 6.0

- +5,000 SFRU4 94.93/95.00/95.06/95.12 call condors 1 ref 94.96

- -4,000 SFRX4 SRZ4 95.06/95.18/95.31 call fly strip 5.75 ref 95.375

- +2,000 SFRZ4 95.37/95.50 call spd w/ 95.62/95.87 call spd strip 7.75

- +5,000 SFRQ4 94.81/94.87/94.93pf 1.5 ref 94.955

- +4,000 SFRZ4 96.00/96.25 call spds 1.375 ref 95.355

- -5,000 SFRQ4 94.87 calls, 10.0 vs. 94.96/0.75%

- +6,000 SFRZ4 95.18/95.37/95.50 put trees 0.75 ref 95.37

- 1,500 SFRZ4 94.62/94.75 2x1 put spds

- Block/screen, +6,000 SFRV4 95.12/95.25/95.31/95.43 call condors, 3.5 ref 95.345 to -.355

- over 6,900 SFRZ4 95.37 calls ref 95.355

- 2,000 SFRZ4 95.62/95.87 call spds ref 95.355

- +4,000 SFRZ4 95.37/95.50 call spds, 4.25 ref 95.355

- Treasury Options: Reminder, August options expire today

- +14,000 TYU4 115 calls, 3 vs. 111-09.5/0.04%

- -8,000 TYU4 110/112 strangles, 44 vs. 111004.5

- 4,000 USU4 115/116 put spds, 8 ref 119-09

- -6,500 wk1 TY 111 puts, 15 vs. 111-14.5/0.44%

- 2,500 TYU4 111.5/113 1x2 call spds, 13 ref 111-07

- +30,000 Wednesday wk5 TY 111.25 puts, 21

- 35,000 Wednesday wk5 111 straddle (expires next Wed) vs. wk1 TY 110.5/111.5 strangle (expires next Fri)

- 5,000 USU4 115/116 put spds, 10

- -5,000 TYU4 112 calls, 24

- -4,500 TYU4 109.5 puts, 16 ref 110-17

- 2,000 TYQ4 111/111.25 call spds ref 110-28.5

- 3,000 TYV4 113.5 calls, 23 last

- Blocks, total 10,000 TYQ4 110.75 straddles, 18.5 avg

- +2,000 TYU4 111.5/112.5/113.5 call trees, 9 ref 110-26.5

- 1,600 TYU4 112.5/113.5/114.5/115.5 call condors ref 110-27.5

- over -10,000 TYU4 111/112 call spds, 22 ref 110-28.5

FOREX: JPY Firmer, But Pace of Run Higher Slows

- The aggressive short-covering rally in the JPY slowed on Friday, with the currency initially trading weaker against all others in G10 - but the effect was short-lived. The currency gradually picked up pace through the US crossover and is on course for another positive session against the USD, although yesterday's cycle extremes are seen in tact for now.

- US PCE data came and with little long-lasting market consequence. PCE price indices were generally inline with expectations, although modest weakness was noted in the personal income category. A softer oil market worked against commodity and oil-tied currencies into the Friday close, as the 2.5% dip for WTI and Brent crude futures undermined the CAD and NOK ahead of the close.

- CHF traded toward the lower-end of the G10 table. The currency had benefited for much of the week from the short squeeze across funding currencies - resulting in USD/CHF's break below 0.88 on Thursday. CHF failed to gain the same tailwind Friday, allowing markets to partially fade the recent rally and tilt CHF weaker.

- Focus in the coming weeks shifts to central banks, with the Bank of Japan, Federal Reserve and Bank of England all set to decide in policy in three very live and critical policy decisions. Both the BoJ and BoE decisions see split consensus over whether the Bank hikes or cuts respectively, while the Fed are expected to signal for their first rate cut as soon as September.

OPTIONS: Expiries for Jul29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0800(E620mln), $1.0825-35(E699mln), $1.0900(E832mln)

- USD/JPY: Y153.25-30($1.0bln), Y154.00($1.3bln), Y155.85($586mln), Y156.50($2.4bln)

- AUD/USD: $0.6680(A$1.0bln)

- USD/CNY: Cny7.3000($815mln)

Late Equities Roundup: Paring Gains, Dow Still Up on Week

- Still strong in late trade, stocks drew some profit taking/position squaring ahead of the weekend. The Dow outpaced the S&P Eminis and Nasdaq indexes as the former climbed back to July 18 levels.

- Currently, the DJIA is up 649.11 points (1.63%) at 40584.79, S&P E-Minis up 52.5 points (0.96%) at 5494.5, Nasdaq up 149.1 points (0.9%) at 17331.79.

- Industrial and Financial sectors continued to outperform in late trade, manufacturing and construction names supporting the former: better than expected earnings and up-revised profit forecasts helps 3M surge 21.73%, GE Vernova +7.58%, Stanley Black & Decker +6.42. Insurance and financial companies buoyed the Financial sector: AON +7.48%, Hartford +6.21%, Cincinnati Financial Group +3.31%.

- On the flipside, Energy and Consumer Staples sectors continued to lag the broad based rally, weaker crude (WTI -1.50 at 76.73) weighing on oil and gas shares: Phillips 66 -0.33%, Occidental Petroleum and APA both -0.13%, EQT Corp -0.05%. Meanwhile, retailers weighed on the Consumer Staples sector: Walmart -0.36%, Costco and Dollar General both -0.18%.

- Earnings announcement are largely done for the week. Monday kicks off with Arbor Realty, Revvity Inc, McDonalds Corp and ON Semiconductors early on; SBA Communications, Welltower, Chesapeake Energy, Lattice Semiconductor and Sybmotic after Monday's close.

E-MINI S&P TECHS: (U4) Bearish Cycle

- RES 4: 5741.34 3.382 proj of the Apr 19 - 29 - May 2 price swing

- RES 3: 5721.25 High Jul 16 and the bull trigger

- RES 2: 5629.75 High Jul 23

- RES 1: 5570.08 50-day EMA

- PRICE: 5479.25 @ 14:22 BST Jul 26

- SUP 1: 5432.50 Low Jul 25

- SUP 2: 5429.62 3.0% 10-dma envelope

- SUP 3: 5370.62 50.0% retracement of the Apr 19 - Jul 16 bull leg

- SUP 4: 5267.75 Low May 31 and key support

S&P E-Minis have traded lower this week and the move down has resulted in a break of both the 20- and 50-day EMAs. This reinforces a short-term bearish cycle and signals scope for an extension near-term. Note that the move down is considered corrective. Potential is seen for a move towards 5429.62, the lower band of a MA envelope, ahead of 5370.62 a Fibonacci retracement. Key short-term resistance is 5629.75, the Jul 23 high.

COMMODITIES Crude Loses Ground, Copper Bear Cycle Remains In Play

- WTI has recouped some losses but has fallen both on the day and week-on-week. Downside drivers have been Chinese demand weakness and Gaza ceasefire talks.

- WTI Sep 24 is down 1.3% at $77.3/bbl.

- WTI futures have traded through both the 20- and 50-day EMAs, reinforcing a short-term bearish threat. A resumption of the bear leg would open $72.23, the Jun 4 low and the next key support.

- Spot gold has risen by 0.9% on Friday to $2,385/oz, leaving the yellow metal 0.7% lower on the week.

- From a technical perspective, the recent pullback is considered corrective. However, a clear break of the 50-day EMA at $2,360.9 would signal scope for a deeper retracement, opening $2,277.4, the May 3 low.

- For bulls, a reversal higher would refocus attention on $2,483.7, the Jul 17 high.

- Meanwhile, copper has edged down by 0.4% to $411/lb, leaving it 3% lower over the week and 20% down from a record high in May.

- A bear cycle in copper futures remains intact and this week’s downleg reinforces current conditions.

- A clear break of $405.57, 76.4% of the Feb 9 - May 20 bull cycle, would set the scene for weakness towards $372.35, the Feb 9 low.

- Initial firm resistance is $443.97 the 50-day EMA.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/07/2024 | 0600/0800 | *** |  | SE | GDP |

| 29/07/2024 | 0600/0800 | ** | | SE | Retail Sales |

| 29/07/2024 | 0830/0930 | ** |  | UK | BOE M4 |

| 29/07/2024 | 0830/0930 | ** | | UK | BOE Lending to Individuals |

| 29/07/2024 | 1000/1100 | ** | | UK | CBI Distributive Trades |

| 29/07/2024 | 1430/1030 | ** |  | US | Dallas Fed manufacturing survey |

| 29/07/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 29/07/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

1570 words