Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

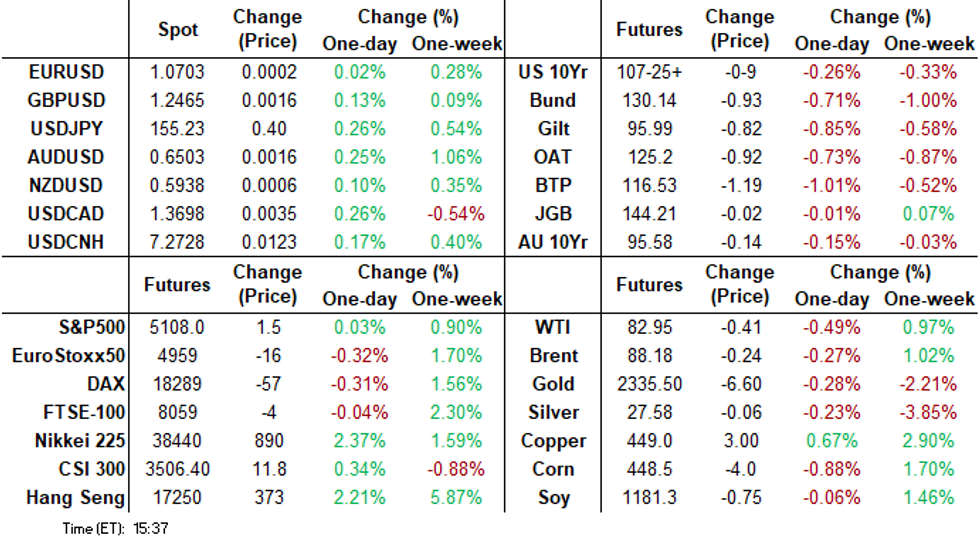

- Treasuries followed EGBs lower, the latter weighed by Bund supply and higher than expected Australia CPI.

- Treasuries traded back near Tuesday's pre-flash PMI lows, curves broadly steeper with Bonds underperforming.

- Focus turns to Thursday's Weekly Jobless Claims, GDP and Core PCE Index.

US TSYS Unwinding Tuesday's PMI Rally, Curves Bear Steepen Near 3M Highs

- Treasuries remain weaker after the bell, off late morning lows amid moderate two-way positioning in the second half. Rates followed EGBs lead on the open with BTP, Bund and Gilt yields supported after Bund supply and higher than expected Australia CPI.

- Treasury futures held near lows following this morning's largely in-line Durables/Cap goods data - brief short cover support on down-revisions to prior: Durable Goods Orders (2.6% vs 2.5% est; prior down-revised to 0.7% from 1.3%), Cap Goods Orders Nondef Ex Air (0.2% vs 0.2% est, prior down revised to 0.4% from 0.7%.).

- Futures remained weaker after the $70B 5Y note auction (91282CKP5) tailed: drawing 4.659% high yield vs. 4.655% WI; 2.39x bid-to-cover vs. 2.41x for the prior auction.

- Jun'24 10Y futures marked a 107-20 low (-14.5) in the first half, traded 107-25 after the bell, 10Y yield climbs to 4.6686% high. 2s10s curve bear steepened to -27.488 - steepest level since February 1.

- In turn, projected rate cut pricing swung back to recent lows: May 2024 -2.6% w/ cumulative -0.6bp at 5.322%; June 2024 at -16.2% vs. -13.6% this morning w/ cumulative rate cut -4.7bp at 5.282%. July'24 cumulative at -12.6bp vs. -11.6bp earlier, Sep'24 cumulative -24bp vs. -22.9bp.

- Thursday Data Calendar: Wkly Claims, GDP, Core PCE Index.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00131 to 5.31816 (+0.00006/wk)

- 3M +0.00090 to 5.32445 (+0.00035/wk)

- 6M -0.00805 to 5.28965 (-0.00885/wk)

- 12M -0.02235 to 5.18826 (+0.00045/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.757T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $689B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $679B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $74B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $253B

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage climbs to $441.215B vs. $435.880B Tuesday. Compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

- Meanwhile, the latest number of counterparties rebounds to 82 vs. 71 prior.

SOFR/TEASURY OPTION SUMMARY

With a few exceptions, SOFR and Treasury option trade centered on downside puts Wednesday as underlying futures unwound Tuesday's post flash PMI support. In turn, projected rate cut pricing swung back to recent lows: May 2024 -2.6% w/ cumulative -0.6bp at 5.322%; June 2024 at -16.2% vs. -13.6% this morning w/ cumulative rate cut -4.7bp at 5.282%. July'24 cumulative at -12.6bp vs. -11.6bp earlier, Sep'24 cumulative -24bp vs. -22.9bp.

- SOFR Options:

- Block, +10,000 SFRZ3 94.62/94.68/94.87 broken put tree, 0.0

- +5,000 SFRM5 93.75/94.25 put spreads 5.5 ref 95.455

- +10,000 0QK4 95.50/95.75 call spds 6.5 ref 95.44

- -12,000 SFRN4 94.62/94.78/94.87/94.93 Iron Condor, 3.25 ref 942895

- -10,000 SFRZ4 94.62/94.68/94.87 put tree 0.25/2-legs over ref 95.08

- -12,000 SFRK4/SFRM4 94.93 put spds, 1.5

- Block, 8,001 SFRV4 94.75 puts, 8.5 vs. 13,335 SFRV4 94.31 puts, 2.0 vs. 1,200 SFRZ4 95.07

- +4,000 SFRK4 94.75/94.87/95.06 broken call flys, 1.25

- +30,000 SFRK4 96.75 calls, 0.25

- 3,950 SFRM4 94.68/94.81/94.93 call trees ref 94.73

- 1,250 SFRM4 94.68/94.75/94.81/94.93 call condors ref 94.73

- 3,300 SFRZ4 94.87/95.37 2x1 put spds ref 95.065

- 1,250 SFRV4 /SFRZ4 94.37/94.62 put spd spd

- 2,500 SFRZ4 94.00/94.12/94.37/94.50 put condors ref 95.075

- 2,500 SFRK4 94.93/95.06 call spds ref 94.73

- Treasury Options: Reminder, May options expire Friday

- +10,000 TYM4 111/112.5/113 call strip, 12 ref 107-23

- 10,000 TYM4 105/106 put spds vs. TYM4 110-111 call spds

- 2,176 FVK4 105/105.25/105.5 call flys vs. FVK4 104.5/104.75/105 put flys

- 6,000 wk2 US 106.25 puts expire May 10

- 4,700 weekly Wednesday 10Y 107.5 puts, 1 expire today

- 2,500 TYK4 107.25/108 2X1 put spds

EGBs-GILTS CASH CLOSE: UK Curve Belly Leads Broader Sell-Off

Core European FI pulled back sharply Wednesday, with Gilts underperforming Bunds and periphery EGB spreads widening.

- Global bond weakness began with the Asia-Pacific overnight session as above-expected Australian inflation data kicked off a round of hawkish central bank repricing.

- The sell-off carried on steadily through the day as supply was digested (Gilt syndication, Bund auction), German IFO data came in firm, and Bund and Gilt futures saw downside technical breaks.

- Implied 2024 ECB rate cuts were pared by 4bp to 72bp; for the BoE, the 48bp implied was 7bp less than seen in the prior session.

- The shift in the BoE outlook translated into belly underperformance on the UK curve, while the German curve bear steepened. With less ECB accommodation implied, periphery EGB spreads widened, exacerbated by risk-off moves elsewhere.

- Thursday's agenda includes French confidence surveys and German GfK consumer confidence, and appearances by ECB's Schnabel and Lagarde.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 4.4bps at 2.971%, 5-Yr is up 7.8bps at 2.588%, 10-Yr is up 8.6bps at 2.588%, and 30-Yr is up 8.2bps at 2.732%.

- UK: The 2-Yr yield is up 9.5bps at 4.446%, 5-Yr is up 9.7bps at 4.221%, 10-Yr is up 9.3bps at 4.334%, and 30-Yr is up 8.2bps at 4.798%.

- Italian BTP spread up 5.3bps at 140bps / Spanish up 2.3bps at 79.6bps

EGB Options: Predominantly Downside Wednesday

Wednesday's Europe rates/bond options flow included:

- DUM4 105.30/105.20ps, bought for 4.5 in 2.6k

- OEM4 119.25/117.50ps 1x2 sold at 57.5 in 1k

- RXN4 130.50/128.00/125.50p fly, bought for 44 in 2k

- ERM4 96.12/96.00ps, bought for 0.75 in ~2.7k

- SFIK4 95.20/95.10/95.05p ladder bought for -2.75 in 2k

- SFIK4/SFIQ4 95.15/95.25/95.35/95.45c condor, bought the August for 2 in 4.5k

- SFIU4 95.40/95.60/95.80c fly, bought for 1.75 in 2k

- SFIZ4 95.90/96.10cs vs 95.10/94.90ps, bought the ps for 4.25 in 1k

FOREX: USDCAD Outperforms Following Data, USDJPY Extends Above 155.00

- Despite the solid moves in core fixed income markets on Wednesday, G10 currencies traded in relatively narrow ranges. Higher yields have moderately benefitted the dollar index (+0.16%), whilst continuing to weigh on the Japanese yen.

- USDJPY sprung to life approaching the US data, breaching the 155.00 handle for the first time since 1990. Stops may have been triggered through this mark, prompting an initial cycle high of 155.17. Despite the level breach, and trend conditions remaining firmly bullish, the pair had an immediate & sharp 35 pip turnaround to print 154.81 before the durable goods data release.

- Since then, USDJPY has extended higher as we approach the APAC crossover. breaching to print a fresh high 155.37. Above here, there is nothing on the technical front until 156.00 and 156.47. The usual caution regarding both verbal and actual intervention will continue to be in focus as we approach Friday's Bank of Japan decision.

- USDCAD (+0.28) received a boost following soft Canadian retail and manufacturing sales, leaving the Canadian dollar as the poorest performing major currency in G10. USDCAD has breached yesterday’s high of 1.3714 and a clear break opens 1.3855 next, the Nov 10 ‘23 high. Note that moving average studies remain in a bull-mode position, highlighting a clear rising trend.

- Higher core yields appeared to have a greater impact on emerging market currencies, with the likes of MXN, PLN and ZAR all underperforming. USDMXN (+0.70%) in particular has risen back above the 17.00 mark and will eye another test of 17.3860, the Jan 17 high, which represents an important reversal trigger.

- All focus turns to the advance reading of first quarter GDP in the US on Thursday, before Friday’s Bank of Japan decision.

Late Equities Roundup

- Stocks holding to modestly lower territory in late trade, DJIA underperforming but well off lows in late trade. Currently, DJIA is down 93.95 points (-0.24%) at 38411.02, S&P E-Minis down 10.75 points (-0.21%) at 5095.25, Nasdaq down 30 points (-0.2%) at 15666.07.

- Heavy earnings announcements on the day included the following ahead of the open: Owens Corning, Thermo Fisher, AT&T, Boston Scientific, Humana, Amphenol, Norfolk Southern and Old Dominion Freight. Announcements expected after the close: Whirlpool, Ford, IBM, United Rentals, Teradyne, Lam Research, Waste Management, Raymond James and Meta.

- Laggers: Industrials and Communication Services continued to underperform in late trade, transportation shares weighed on the former: Old Dominion Freight -10.19% after meeting income targets, Norfolk Southern -3.71%, CSX -2.89%. Meanwhile, interactive media and telecommunications shares weighed on the former: Netflix -3.99%, Warner Bros -1.48%, Meta -1.23%.

- Leading gainers: Consumer Staples and Utilities displaced earlier leaders Consumer Discretionary and Information Technology sectors in the second half. Beverage shares buoyed Consumer Staples: PepsiCo +3.91%, Monster Beverage +1.99%, Coca-Cola +1.40%. Independent power and water providers supported Utilities in late trade: NRG Enerrgy +1.97%, AES Corp +1.40%, American Water Works +1.23%.

E-MINI S&P TECHS: (M4) Approaching Resistance

- RES 4: 5285.00/5333.50 High Apr 10 / 1 and the bull trigger

- RES 3: 5213.25 High Apr 15

- RES 2: 5148.79 20-day EMA

- RES 1: 5136.32 50-day EMA

- PRICE: 5094.00 @ 1505 ET Apr 24

- SUP 1: 4963.50 Low Apr 19

- SUP 2: 4907.57 50.0% retracement of the Oct 27 ‘23 - Apr 1 bull leg

- SUP 3: 4863.75 Low Jan 19

- SUP 4: 4799.50 Low Jan 17

The short-term trend condition in S&P E-Minis remains bearish and the latest recovery appears - for now - to be a correction. Last Friday’s bearish extension reinforced current short-term conditions. The contract has recently cleared the 50-day EMA, signalling scope for a continuation lower. Sights are on 4907.57 next, a Fibonacci retracement. Firm resistance is 5153.25, the 20-day EMA. A clear break of the average would signal a possible reversal.

COMMODITIES Crude Loses Ground, Spot Gold Remains Steady

- WTI has slid further during US hours, as the eroding geopolitical risk premium and concerns about near-term demand growth outweigh a larger than expected US stock draw.

- WTI Jun 24 is down 0.5% at $82.9/bbl.

- WTI futures have recovered from their recent lows and price remains above key short-term support at $80.85, the 50-day EMA. A break of the 50-day average would signal a stronger bearish theme and open $76.07, the Mar 11 low.

- On the upside, key resistance and the bull trigger has been defined at $86.97, the Apr 12 high.

- Meanwhile, Henry Hub is headed for its lowest close since March 26 as milder weather and high storage inventories pile pressure on the front month.

- US Natgas May 24 is down 7.5% at $1.68/mmbtu.

- Spot gold remains broadly unchanged again on Wednesday at $2,321/oz.

- The precious metal has traded below the 20-day EMA and this signals the start of a possible corrective cycle. A continuation lower would signal scope for an extension towards $2,221.5, the 50-day EMA.

- Key resistance and the bull trigger has been defined at $2,431.5, the recent Apr 12 high.

- Copper is up by 0.5% to $445.7/lb.

- A bullish theme in copper futures remains intact, with attention on $460.76, a Fibonacci projection. Key support is seen at $414.19 the 50-day EMA.

THURSDAY DAYA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 25/04/2024 | 0600/0800 | * |  | DE | GFK Consumer Climate |

| 25/04/2024 | 0600/0800 | ** |  | SE | PPI |

| 25/04/2024 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 25/04/2024 | 0700/0900 | ** |  | ES | PPI |

| 25/04/2024 | 0700/0900 | ** | | SE | Economic Tendency Indicator |

| 25/04/2024 | 0700/0900 |  | EU | ECB's Schnabel Speech for 'ChaMP' | |

| 25/04/2024 | 1000/1100 | ** |  | UK | CBI Distributive Trades |

| 25/04/2024 | 1100/0700 | *** |  | TR | Turkey Benchmark Rate |

| 25/04/2024 | 1230/0830 | *** |  | US | Jobless Claims |

| 25/04/2024 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 25/04/2024 | 1230/0830 | *** | | US | GDP |

| 25/04/2024 | 1230/0830 | * |  | CA | Payroll employment |

| 25/04/2024 | 1230/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 25/04/2024 | 1400/1000 | ** | | US | NAR Pending Home Sales |

| 25/04/2024 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 25/04/2024 | 1500/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 25/04/2024 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 25/04/2024 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 25/04/2024 | 1700/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.