Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

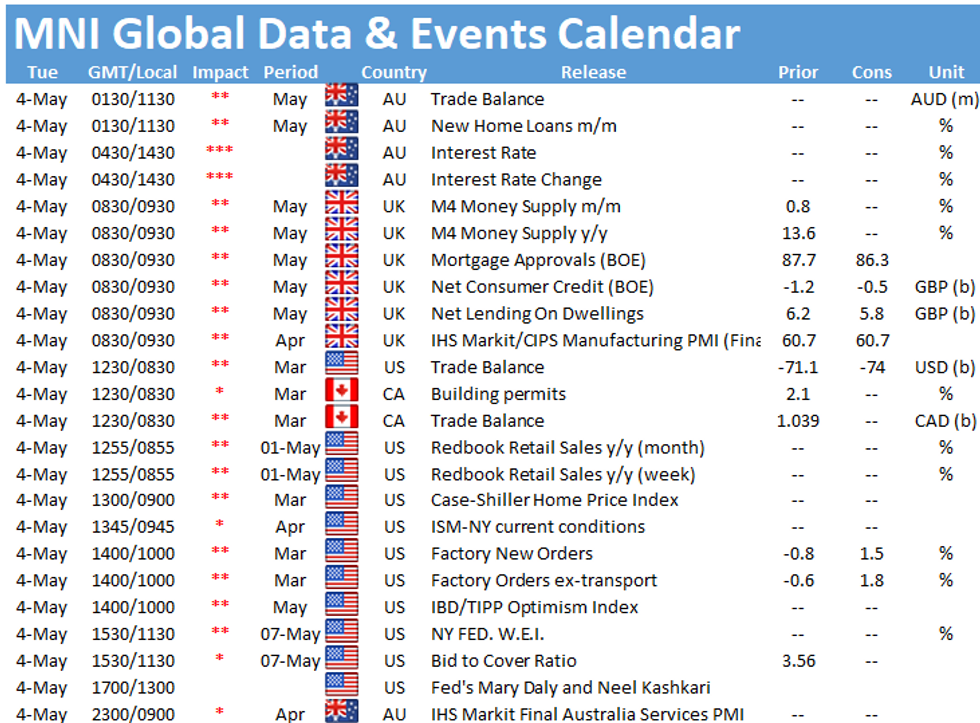

- MNI INTERVIEW: Factory Prices May Rise Fastest Since 1950s-ISM

- MNI POLICY: Williams Says Fed's Dual Goals Are Still Far Away

- MNI BRIEF: Treasury Raises Q2 Borrowing Estimate by USD368B

- MNI BRIEF: Atlanta Fed Model Revises US Q2 GDP Outlook Higher

- WHITE HOUSE BACKS PFIZER'S MOVE TO BEGIN U.S. VACCINE EXPORTS, Bbg

US

US: U.S. manufacturing price gains may surge to the fastest pace since the 1950s in the next few months on widespread shortages of parts, materials, and workers, Institute for Supply Management chair Tim Fiore told MNI Monday.

- Previous ISM estimates that foresaw price growth of 2.5% over the first half of 2021 are likely to double to 5%, according to revised preliminary estimates the group hasn't published yet, Fiore said in a phone interview. Estimates for the second half of the year are also being increased, and even with some moderation late this year, the 2021 price gain will likely be around 3%, he said.

- "Officials are saying that this is transitory and as demand gets back to normal prices will fall back down," he said. "It could very well be, but in the meantime there's no indication that they will. There's no end in sight that anyone can really see here." For more see MNI Policy main wire at 1328ET.

FED: The Atlanta Fed has revised it's Q2 GDP forecast higher to an annualized 13.2% from the 10.4% forecast last week, according to the regional Fed bank's latest weekly real-time GDPNow model.

- That was mostly driven by positive construction and manufacturing data released Monday by the Institute for Supply Management and the Census Bureau. The ISM's monthly manufacturing index fell to 60.7 in April from 64.7 in March but still signaled expansion, and construction spending was up 0.2%, a slower-than-expected gain but still an improvement over February's 0.6% decline.

- Treasury is assuming a cash balance of approximately USD450 billion at the expiration of the debt limit suspension on July 31, more than the roughly USD130 billion that market analysts have expected.

- Officials also raised their end-of-June cash balance goal to USD800 billion, from USD500 billion previously, citing the Biden administration fiscal support in the face of the coronavirus. The Treasury's cash balance on Friday was just over USD900 billion.

- For the third quarter, the Treasury plans to issue USD821 billion in net marketable debt, assuming an end-June cash balance of USD700 billion. The Treasury's quarterly refunding will be released at 8:30 a.m. May 5.

OVERNIGHT DATA

- US MAR CONSTRUCT SPENDING +0.2%

- US MAR PRIVATE CONSTRUCT SPENDING +0.7%

- US MAR PUBLIC CONSTRUCT SPENDING -1.5%

- US ISM Apr Manufacturing PMI Falls To 60.7 vs Mar 64.7

- US ISM NEW ORDERS INDEX 64.3 APR VS 68.0 MAR

- US ISM EMPLOYMENT INDEX 55.1 APR VS 59.6 MAR

- US ISM PRODUCTION INDEX 62.5 APR VS 68.1 MAR

- US ISM SUPPLIER DELIVERY INDEX 75.0 APR VS 76.6 MAR

- US ISM INVENTORIES INDEX 46.5 MAR VS 50.8 MAR

- Apr's reading marks a 3-month low, nevertheless, the index remains comfortably above the 50-mark since Jun 2020. This month's decrease was broad-based with every major category posting a decline, led by a 5.6pt drop of Production to the lowest level since Jan.

- Employment fell 4.5pt to 55.1 and Inventories shifted back below the 50-mark to 46.5, while New Orders declined 3.7pt to a 3-month low of 64.3. Supplier Deliveries eased by 1.6pt to 75.0, remaining elevated by historical standards.

- Among the other categories, Imports saw the largest decline of 4.5pt to 52.2, followed by Customer's inventory, down 1.5pt to 28.4 and hitting a new record low.

- Prices increased 4pt to 89.6, surging to the highest level since Jul 2008 where the index registered at 90.4. Order Backlogs ticked up 0.7pt to 68.2, the highest reading since the series, while Exports edged up 0.4pt to 54.9.

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 284.73 points (0.84%) at 34161.64

- S&P E-Mini Future up 18.25 points (0.44%) at 4193.25

- Nasdaq down 42.4 points (-0.3%) at 13920.26

- US 10-Yr yield is down 1.6 bps at 1.61%

- US Jun 10Y are up 8.5/32 at 132-9.5

- EURUSD up 0.0043 (0.36%) at 1.2064

- USDJPY down 0.21 (-0.19%) at 109.1

- WTI Crude Oil (front-month) up $0.89 (1.4%) at $64.47

- Gold is up $22.38 (1.27%) at $1791.67

European bourses closing levels:

- EuroStoxx 50 up 25.51 points (0.64%) at 4000.25

- German DAX up 100.56 points (0.66%) at 15236.47

- French CAC 40 up 38.42 points (0.61%) at 6307.9

US TSY SUMMARY: ISM Miss Weighs on Tsy Ylds

Robust volumes traded despite Asia and London out for extended holiday (Japan and China through Wednesday still). Rates and equities climbed higher while USD dipped as focus turns to US data, rounding out the week with headline employment report, April job gain mean estimate +978k.- Early two-way trade on inside range, Tsys followed Bund lead into the NY open, overnight rate sellers on the back of upbeat PMI and re-open plans in Europe.

- Tsys bounced on the open with for no obvious reason save perhaps unwinds of month-end positioning.

- Strong data through April hit a snag midmorning: Tsys surged post ISM: 60.7 vs. 65.0 est and 64.7 in March. over 175k TYM1 trades in appr 5 minutes post data. 10YY fell to 1.5763% low, 1.6118% after the bell as futures pared gains; 30YY fell to 2.2515% low, 2.2929% last.

- No new ground broken by several Fed speakers including Fed Chair Powell late session.

- The 2-Yr yield is up 0.2bps at 0.1604%, 5-Yr is down 1.4bps at 0.8317%, 10-Yr is down 1.6bps at 1.61%, and 30-Yr is down 0.5bps at 2.2913%.

US TSY FUTURES CLOSE:

- 3M10Y -1.687, 159.379 (L: 156.62 / H: 164.51)

- 2Y10Y -1.749, 144.407 (L: 141.592 / H: 148.854)

- 2Y30Y -0.113, 212.588 (L: 209.113 / H: 216.063)

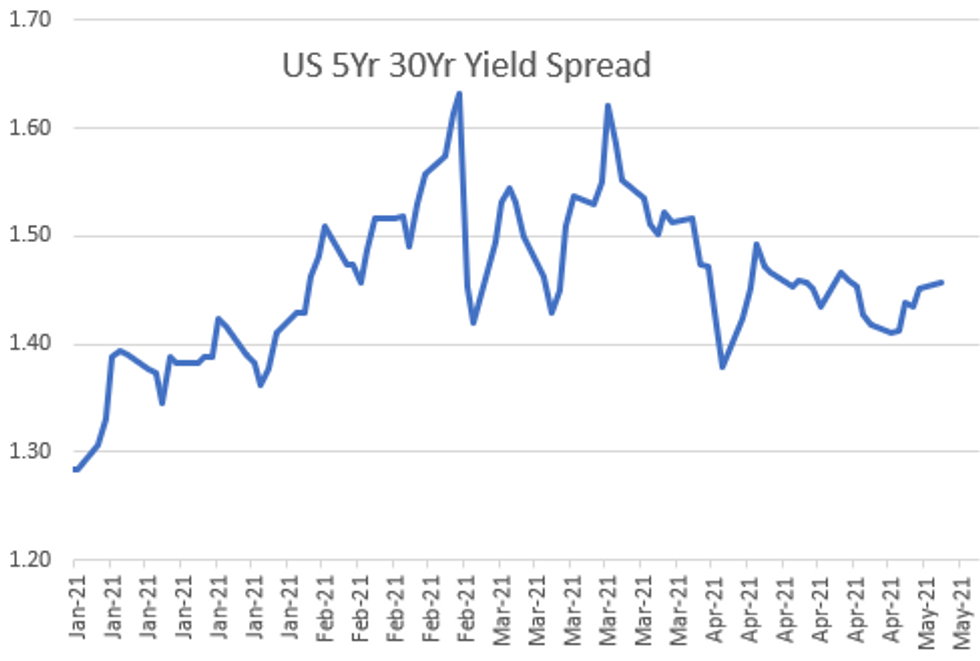

- 5Y30Y +1.457, 145.818 (L: 142.808 / H: 146.8)

- Current futures levels:

- Jun 2Y up 0.125/32 at 110-12.25 (L: 110-11.875 / H: 110-12.5)

- Jun 5Y up 4.25/32 at 124-2.25 (L: 123-27.25 / H: 124-04.75)

- Jun 10Y up 9/32 at 132-10 (L: 131-26.5 / H: 132-16)

- Jun 30Y up 11/32 at 157-19 (L: 156-21 / H: 158-10)

- Jun Ultra 30Y up 16/32 at 186-13 (L: 184-25 / H: 187-24)

US EURODOLLAR FUTURES CLOSE

- Jun 21 -0.005 at 99.810

- Sep 21 steady at 99.80

- Dec 21 steady at 99.745

- Mar 22 -0.005 at 99.775

- Red Pack (Jun 22-Mar 23) steadysteady0 to +0.020

- Green Pack (Jun 23-Mar 24) +0.025 to +0.035

- Blue Pack (Jun 24-Mar 25) +0.035 to +0.045

- Gold Pack (Jun 25-Mar 26) +0.035 to +0.040

Short Term Rates

US DOLLAR LIBOR: No new settles Monday due to UK bank holiday, resume Tuesday. Friday sets':

- O/N -0.00150 at 0.07125% (-0.00212/wk)

- 1 Month -0.00288 to 0.10725% (-0.00375/wk)

- 3 Month +0.00075 to 0.17638% (-0.00500/wk) ** (Record Low 0.17288% on 4/22/21)

- 6 Month -0.00150 to 0.20488% (+0.00075/wk)

- 1 Year -0.00025 to 0.28113% (+0.00025/wk)

- Daily Effective Fed Funds Rate: 0.05% volume: $70B

- Daily Overnight Bank Funding Rate: 0.03%, volume: $235B

- Secured Overnight Financing Rate (SOFR): 0.01%, $924B

- Broad General Collateral Rate (BGCR): 0.01%, $377B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $351B

- (rate, volume levels reflect prior session)

- Tsy 2.25Y-4.5Y, $8.801B accepted vs. $27.933B submission

- Next scheduled purchases:

- Tue 5/04 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Wed 5/05 1100-1120ET: Tsy 4.5Y-7Y, appr $6.025B

- Thu 5/06 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

PIPELINE: Bigger and Bigger

Equinix outpaces EBay that outpaced General Dynamics. All said and done, $9.425B to price Monday- Date $MM Issuer (Priced *, Launch #)

- 05/03 $2.6B #Equinix $700M 5Y +65, $400M 7Y +80, $1B 10Y +95, $500M 30Y +115. Last year, Equinix issued 2.6B on Jun 8: $500M 5Y +85, $500M 7Y +115, $1.1B 10Y +130, $00M 30Y +145

- 05/03 $2.5B #EBay $750M 5Y +60, $750M 10Y +100, $1B 30Y +135. Last year, EBay issued total $1.75B: $500M each 5Y +120, 10Y +170, $300M 5Y Tap +70, $450M 10Y tap +145

- 05/03 $1.5B #General Dynamics $500M 5Y +35, $500M 10Y +65, $500M 20Y +70. Last year General Dynamics issued $4B on March 23: $750M 5Y +295, $750M 7Y +300, $1B 10Y +300, $750M 20Y +295, $750M 30Y +295

- 05/03 $1.1B #Norfolk Southern $500M 10Y +70, $600M 100Y +180. NS issued $800M 30Y +178 on April 3, 2020.

- 05/03 $1B #Southern Co 30NC5 3.75%

- 05/03 $725M #NGPL PipeCo 10Y +165

FOREX: USD Slips as ISM Confirms Deceleration

- Monday was a generally quiet session for news, but markets still found excuses to nudge currencies, with a poorer-than-expected ISM Manufacturing release leading to a solidly USD negative environment. The employment component was of particular interest, with the rate of growth slowing to 55.1 from the 59.6 previous - which may cause some uncertainty in Friday's NFP release.

- At the other end of the table, one of last week's poorest performers, GBP, was the strongest currency in G10 Monday. Confirmation over the weekend that the UK will look to remove all Coronavirus restrictions in June may have helped solidify the outlook, but the UK Bank Holiday kept most traders away, clouding the signal somewhat.

- Focus Tuesday turns to trade balance data from Australia, the US and Canada as well as the March factory orders numbers. The Reserve Bank of Australia rate decision also crosses. The RBA are seen keeping the main policy tools unchanged this month. Speeches are scheduled from ECB's Villeroy and Fed's Daly & Kaplan.

EGB/Gilt - Recovering Early Losses

Having sold off through to mid-morning, EGBs traded firmer through the remainder of the session with curves broadly bull flattening.

- The bund curve is 2bp flatter.

- OAT yields are 1-2bp lower with the long-end of the curve similarly outperfomring.

- BTPs have marginally outperformed core EGBs with cash yields 2-3bp lower on the day.

- Final Eurozone Manufacturing PMI data confirm that the economic recovery was underway in April.

- Market focus will be on the BoE MPC meeting on Thursday. Although no change in the main monetary policy instruments is expected, there is some speculation on the possibility that the asset purchase pace could be tapered.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.