Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI BRIEF: Fed Regulation Chief Quarles to Resign At Year-End

- MNI: Harker Prepared To Hike Before Taper Ends If Prices Surge

- MNI: Clarida Says Fed On Track To Raise Rates By End Of 2022

- MNI: Evans Sees Low Fed Rates For Some Time, Inflation Ebbing

- FED VC CLARIDA SEES INTEREST-RATE LIFTOFF TEST MET BY END-2022, Bbg

- FED BULLARD: THIS IS `ONE OF THE HOTTEST LABOR MARKETS' WE'VE SEEN, Bbg

- FED BULLARD: I'VE GOT TWO RATE HIKES PENCILLED IN FOR 2022, Bbg

US

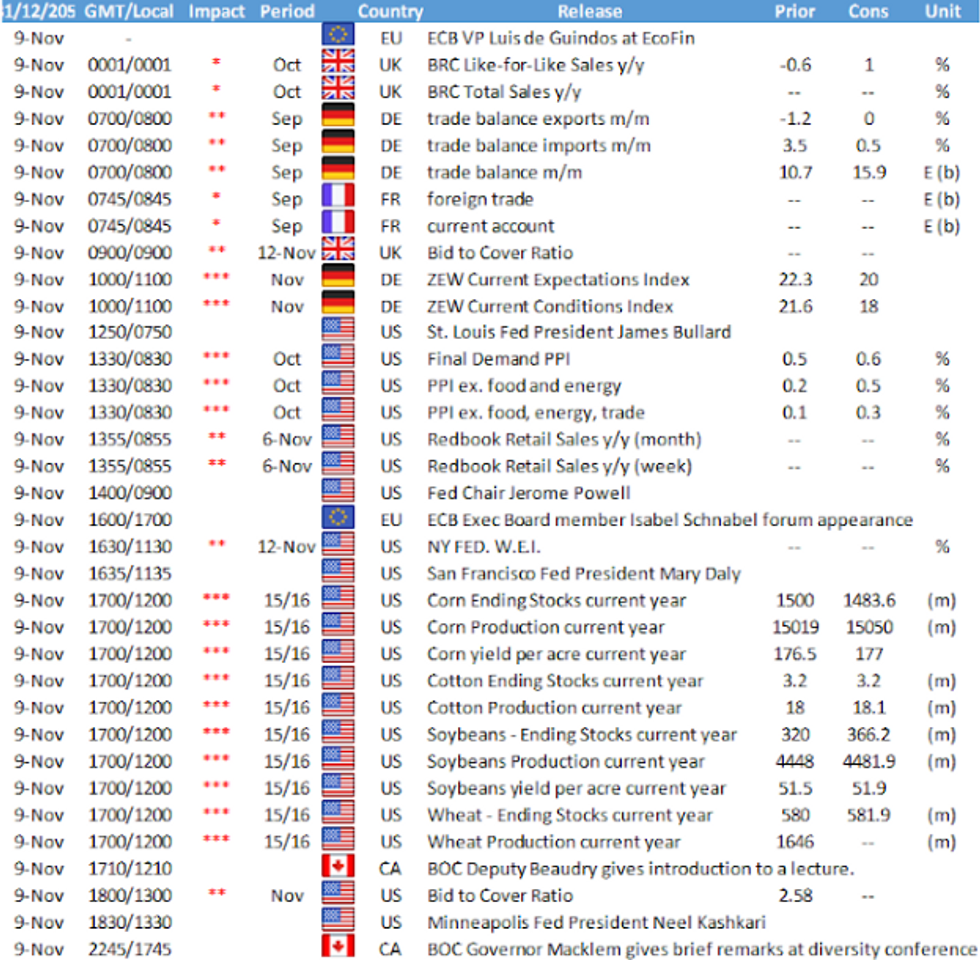

FED: Federal Reserve Vice Chair Richard Clarida said Monday the Fed is on track to raise benchmark interest rates by the end of 2022 if the economy develops as he expects.

- Core PCE inflation is running at 2.8% in the February 2020 to September 2021 period and projected to remain "moderately" above target for the next three years, meeting the Fed's threshold for liftoff, he said. The labor market by the end of 2022 will also have reached maximum employment "if the unemployment rate has declined by then to the SEP median of modal projections of 3.8%," he said in remarks prepared for a Brookings Institution webcast.

- "While we are clearly a ways away from considering raising interest rates, if the outlooks for inflation and unemployment I summarized a moment ago turn out to be the actual outcomes realized over the forecast horizon, then I believe that these three necessary conditions for raising the target range for the federal funds rate will have been met by year-end 2022."

FED: Chicago Fed President Charles Evans said Monday that policy interest rates could remain low for some time and even with some recent upside risks inflation should moderate as workers and firms restore supply networks.

- "There are many uncertainties to the outlook and changing circumstances could lead the FOMC to move up or delay rate increases. But judging from where the economy stands today, it looks like we are in for a low rate environment for some time to come," Evans said in prepared remarks to the OESA automotive suppliers' conference.

- "Much of the current surge in inflation is temporary," he said, and "while good progress has been made, we still have a way to go before we meet the FOMC's inclusive employment mandate." For more see MNI Policy main wire at 1338ET.

FED: Federal Reserve Governor Randal Quarles will resign at the end of the year, after his term as the central bank's first vice chair for supervision ended last month.

- Quarles, who first took office in October 2017, also serves as chair of the Financial Stability Board and his three-year term ends Dec. 2.

- President Joe Biden is gearing up to nominate the next Fed chair and vice chair of supervision, expected before year-end.

FED: Philadelphia Federal Reserve President Patrick Harker indicated Monday that it is possible that interest rates could rise before tapering of bond purchases is finished, but only if inflation fails to subside next year as he expects.

- "I don't expect that the federal funds rate will rise before the tapering is complete, but we are monitoring inflation very closely and are prepared to take action, should circumstances warrant it," he said in the text of a speech to the Economics Club of New York. The Fed last week began a taper that at the current pace could end around mid-2022.

- "Inflation is more widespread across products and services than it was earlier this year," he said. "I am acutely aware that this period of rising prices is painful for many Americans. But I do expect inflation to moderate next year as supply chains come back online and bottlenecks ease." For more see MNI Policy main wire at 1200ET.

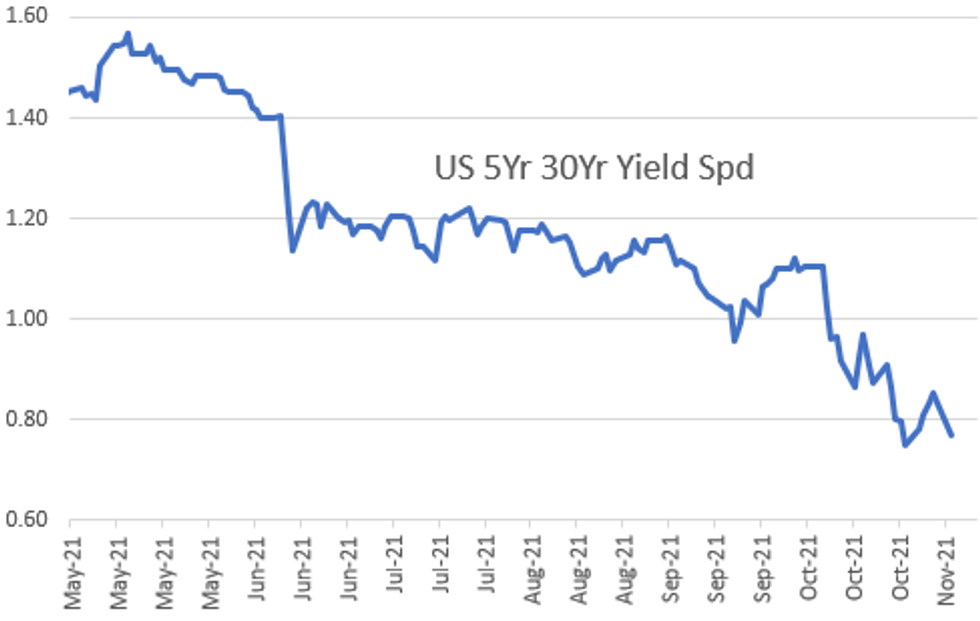

US TSYS: 30Y Inflation-Linked Yld -0.508% Record Low

Tsys revisit second half lows in after hours trade, moderate overall volumes (TYZ1 just over 1.0M futures), yield curves mixed/longer spds flatter (5s30s -6.72 at 76.04), 30Y Inflation-linked yld -0.508% record low.- No data Monday but multiple Fed speakers echoing hawkish tones: Clarida Says Fed On Track To Raise Rates By End Of 2022; Harker Prepared To Hike Before Taper Ends If Prices Surge; BULLARD: THIS IS `ONE OF THE HOTTEST LABOR MARKETS' WE'VE SEEN ... has TWO RATE HIKES PENCILLED IN FOR 2022, Bbg.

- For a little variety: Fed Regulation Chief Quarles announced his resign at year-end. Chairman Powell again Tuesday; data focus on PPI Final Demand MoM (0.5%, 0.6% est); YoY (8.6%, 8.6% est)

- Early long end bid evaporated quickly, futures see-sawed to session lows early second half. Tsy futures held near lows after $56B 3Y note sale (91282CDH1) tailed (0.750% high yield vs. 0.642% WI; 2.33x bid-to-cover vs. 2.44x 5-auction avg) but bounced off lows following Block buy 7.5k FVZ 122-04.

- Sources also report bank portfolio buying 10s-30s after real$ sold 30s earlier, foreign real$ bought 3s earlier. Deal-tied selling earlier starting to unwind as swappable corporate issuance launched, $5.5B Westpac 5Pt lions share of Mon's $12.55B total corporate issuance. Large 12k Eurodollar Green-pack Block buys.

- The 2-Yr yield is up 4.6bps at 0.4466%, 5-Yr is up 6.1bps at 1.1169%, 10-Yr is up 4.2bps at 1.4932%, and 30-Yr is down 0.1bps at 1.8857%.

MARKET SNAPSHOT

Key late session market levels:

- DJIA up 125.69 points (0.35%) at 36450.49

- S&P E-Mini Future up 8.75 points (0.19%) at 4699.5

- Nasdaq up 41.4 points (0.3%) at 16015.92

- US 10-Yr yield is up 4.4 bps at 1.495%

- US Dec 10Y are down 17/32 at 131-9.5

- EURUSD up 0.0022 (0.19%) at 1.1589

- USDJPY down 0.17 (-0.15%) at 113.23

- WTI Crude Oil (front-month) up $0.89 (1.1%) at $82.14

- Gold is up $7.61 (0.42%) at $1826.01

- EuroStoxx 50 down 10.51 points (-0.24%) at 4352.53

- FTSE 100 down 3.56 points (-0.05%) at 7300.4

- German DAX down 7.84 points (-0.05%) at 16046.52

- French CAC 40 up 6.69 points (0.1%) at 7047.48

US TSY FUTURES CLOSE

- 3M10Y +4.791, 145.361 (L: 140.685 / H: 145.631)

- 2Y10Y -0.043, 104.414 (L: 103.912 / H: 106.546)

- 2Y30Y -4.513, 143.516 (L: 143.448 / H: 149.864)

- 5Y30Y -6.394, 76.435 (L: 76.42 / H: 84.155)

- Current futures levels:

- Dec 2Y down 3.375/32 at 109-23.625 (L: 109-23.5 / H: 109-26.5)

- Dec 5Y down 11.25/32 at 122-3.25 (L: 122-02.75 / H: 122-14.5)

- Dec 10Y down 17.5/32 at 131-9 (L: 131-08.5 / H: 131-25.5)

- Dec 30Y down 20/32 at 162-8 (L: 162-04 / H: 162-25)

- Dec Ultra 30Y down 5/32 at 198-6 (L: 197-04 / H: 198-14)

US EURODOLLAR FUTURES CLOSE

- Dec 21 -0.005 at 99.810

- Mar 22 -0.020 at 99.775

- Jun 22 -0.035 at 99.615

- Sep 22 -0.055 at 99.420

- Red Pack (Dec 22-Sep 23) -0.105 to -0.07

- Green Pack (Dec 23-Sep 24) -0.095 to -0.085

- Blue Pack (Dec 24-Sep 25) -0.08 to -0.07

- Gold Pack (Dec 25-Sep 26) -0.065 to -0.06

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00763 at 0.06500% (+0.00050 total last wk)

- 1 Month +0.00250 to 0.09113% (+0.00213 total last wk)

- 3 Month +0.00288 to 0.14563% (+0.01050 total last wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.00188 to 0.21900% (+0.01988 total last wk)

- 1 Year -0.00462 to 0.35288% (-0.00363 total last wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $79B

- Daily Overnight Bank Funding Rate: 0.07% volume: $283B

- Secured Overnight Financing Rate (SOFR): 0.05%, $875B

- Broad General Collateral Rate (BGCR): 0.05%, $354B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $331B

- (rate, volume levels reflect prior session)

- Tsy 22.5Y-30Y, $1.999B accepted vs. $3.768B submission

- Next scheduled purchases

- Tue 11/09 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Wed 11/10 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

- Thu 11/11 Veterans Day holiday, no purchase operation

- Fri 11/12 1500ET: Update NY Fed Operational Purchase Schedule

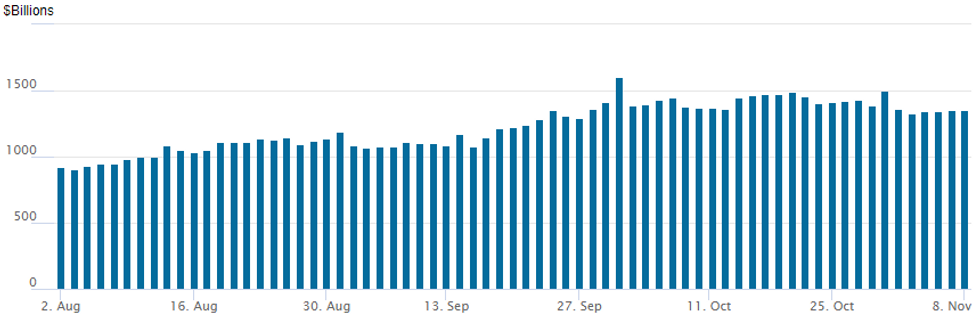

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage creeps higher: $1,354.382B from 75 counterparties vs. $1,354.059B on Friday. Record high remains at $1,604.881B from Thursday, September 30.

PIPELINE: $5.5B Westpac 5pt Jumbo Launched

- Date $MM Issuer (Priced *, Launch #)

- 11/08 $5.5B #Westpac 5pt Jumbo: $1.25B 3Y +30, $750M 3Y FRN/SOFR+30, $1.25B 7Y +58, $1.25B 15NC10 +153, $1B 20Y +123

- 11/08 $2.5B #Ford 10Y Green 3.25%

- 11/08 $1.3B #Bank of NY Mellon perp NC5 3.75%

- 11/08 $1.25B #Cargill Inc $1B 10Y +68, $250M 30Y tap +73

- 11/08 $1B #Sherwin-Williams $500M 10Y +75, $500M 30Y +105

- 11/08 $1B #Equitable Financial Life $500M 3Y +38, $500M 5Y +60

- Rolled to following days:

- 11/08 $500M Kommunalbanken 4.5Y FRN/SOFR+22a, exp Tue launch

- 11/08 $Benchmark SEK (Svensk Exportkredit) 2Y SOFR+16a, exp Tue launch

- 11/08 $1B CDC (Caises des Depots et Consignations) 3Y +23a, exp Tue launch

- 11/08 $4B Dish Network 5Y, 7Y investor call, exp Wed launch

- $Benchmark Investor calls today: Swedbank, State of Israel, Telefonica Chile, United Bank of Africa, Zhengzhou Metro Grp, Wuhan Financial, Avic Int, Uzbekneftgaz.

EGBs-GILTS CASH CLOSE: Short-End Rally Pauses For Breath

UK and German short-end yields ticked higher after a strong rally late last week following the BoE meeting. Long end yields fell, though, with 30Ys outperforming in a flattening curve move.

- Periphery spreads modestly tightened (Italy and Greece 10Y in ~2bp vs Bunds).

- Definitely the least active session in a few days in terms of both volumes and tradeable events, amid a quiet day for data and supply.

- Nothing new from ECB's Lane who reiterated his dovish stance.

- The schedule picks up a bit Tuesday with German ZEW data and German / Dutch bond sales, as well as appearances by BOE's Broadbent and ECB's Lagarde, among others.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.7bps at -0.722%, 5-Yr is up 2.2bps at -0.557%, 10-Yr is up 3.5bps at -0.245%, and 30-Yr is up 4.8bps at 0.115%.

- UK: The 2-Yr yield is up 0.9bps at 0.417%, 5-Yr is up 0.3bps at 0.568%, 10-Yr is up 1bps at 0.855%, and 30-Yr is down 1.3bps at 1.003%.

- Italian BTP spread down 1.9bps at 113.8bps / Greek down 2.3bps at 134.6bps

FOREX: Greenback Edges Lower As Kiwi Outperforms

- The greenback extended on some late Friday weakness, with the dollar index retreating roughly 0.3% to start the week.

- Gains for major currencies were broad based against the US dollar with just CHF and SEK also showing weakness.

- NZDUSD led the G10 charge, rising 0.7% and back above 0.7150. Notable resistance comes in at 0.7219, multiple highs throughout October. GBPUSD also traded with a positive tone after rising back above 1.3500 and ranking second on the G10 Monday leaderboard.

- USDJPY continued to edge lower towards the 113 handle, a level the pair has not closed beneath since October 8, also representing the October 12 low. Despite primary trend conditions remaining bullish, a break of this support zone would signal scope for a deeper pullback and open 112.08, Sep 30 high.

- The Euro also strengthened and worth noting EURCHF extending a bounce from the 1.0534 Friday lows to just shy of the 1.06 handle as New York sat down on Monday. Recent commentary had been focusing on the 1.0505 level that provided crucial support following the onset of the pandemic in early 2020, garnering increased attention among market participants.

- Dollar weakness filtered through to some emerging market FX with notable strength in both the South African Rand and the Chilean Peso, both rising 1%.

- German ZEW sentiment data will be the focus of the European data calendar on Tuesday before US PPI headlines the US docket.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok