Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI US: Lawmakers Debate Fed's Lender of Last Resort Role

- MNI FED: Fed's Waller Sees Dollar Staying Dominant World Currency

- MNI SOURCES: ECB Cut Expectations Range From 50-100BP In 2024

- MNI SOURCES: New ECB Framework To Maintain Continuity

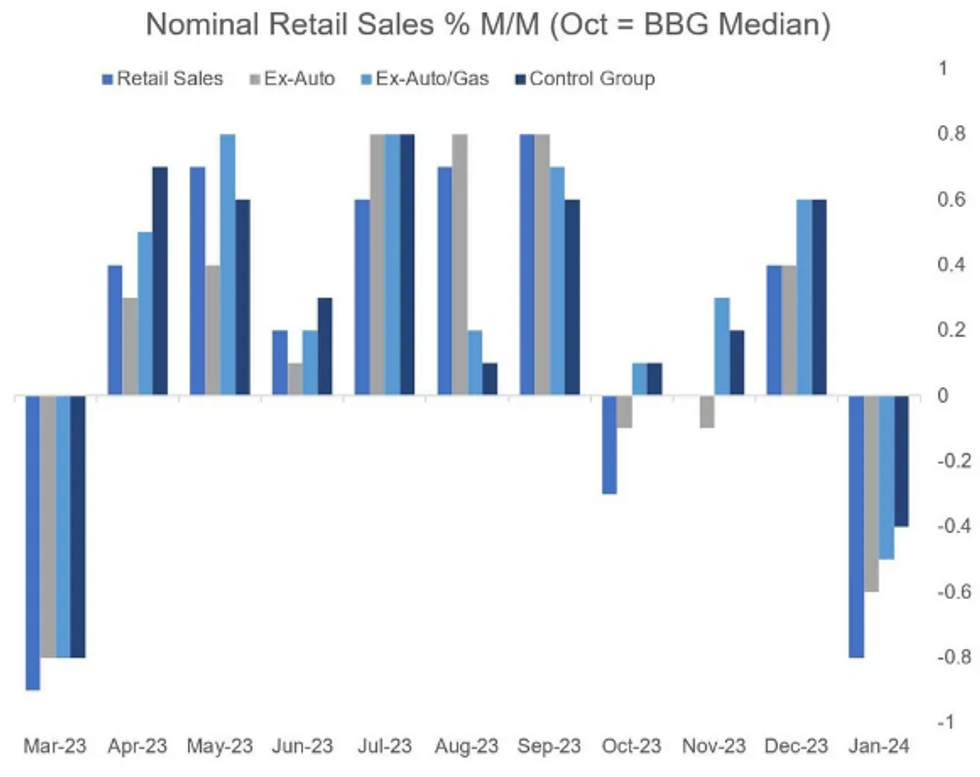

- MNI US DATA: Poorest Retail Sales Report In 10 Months, Weather A Potential Factor

US TSYS Hold Modest Bid After Weakest Retail Sales Since March 2023

- Still bid, Treasury futures are drifting near the lower end of a narrow session range Thursday (TYH4 +4.5 at 110-05 vs. 110-00.5 low, yield -.0117 at 4.2437). No significant technical breakout despite an initial gap bid after this morning's deluge of economic data.

- Cash Tsys mirrored similar bull flattening moves in EGBs while off highs following wait and see tones from ECB Lagarde wanting to avoid any "hasty" decisions to cut rates with more evidence of inflation decline needed.

- Treasury futures gap higher, retrace half the move after lower than expected Retail Sales MoM (-0.8% vs. -0.2% st, 0.6% prior). The core categories also started the year on a negative note, inc contrast to relative strength at the end of 2023: ex-autos -0.6% (+0.2% survey, +0.4% prior), ex-auto/gas -0.5% (+0.2% survey, +0.6% prior), and for the key Control Group which is a GDP input, -0.4% (+0.2%, +0.8% prior). Overall the contractions pointed to the weakest report since March 2023.

- Initial Jobless Claims less than expected, however: 212k vs. 220 est, while Continuing Claims rise 1.895M vs. 1.880M est.

- TYH4 breached Initial technical resistance at 110-16 (low Feb 9) briefly before settling in around 110-06 +/- 1-2 tics. little react to the rest of the data: Industrial Production/Capacity Utilization, Business Inventories and NAHB Housing Market Index. Total Net TIC Flows wraps things up at 1600ET.

- Look ahead: Friday data calendar includes PPI, House Starts/Build Permits, UoM Inflation

NEWS

US BRIEF (MNI): Lawmakers Debate Fed's Lender of Last Resort Role

Lawmakers in the House of Representatives Thursday debated how to solve issues with the Fed's discount window and whether to adjust emergency lending practices, with some bipartisan criticism of Federal Home Loan Banks' emergency lending to banks.

FED (MNI): Fed's Waller Sees Dollar Staying Dominant World Currency

Federal Reserve Governor Christopher Waller on Thursday said he doesn't see the U.S. dollar being dethroned anytime soon despite frequent questions about a decline, because it continues to dominate as a store of value, a medium of exchange and as a unit of account.

MNI SOURCES (MNI): ECB Cut Expectations Range From 50-100BP In 2024

Expectations on the European Central Bank’s Governing Council for rate cuts this year currently range between 50 and 100 basis points in 25bp steps, with more dovish members looking for an earlier start but the largest bloc coalescing around a June commencement for easing and then lowering the deposit rate twice more, Eurosystem sources told MNI.

SOURCES (MNI): New ECB Framework To Maintain Continuity

Options for the European Central Bank’s new Operational Framework Review are likely to be presented to the Governing Council by as soon as the Feb 22 non-monetary policy meeting, and while sources close to technical discussions told MNI that there appears to be broad agreement on maintaining a modified version of the existing framework, they stressed no final decision has been made.

SECURITY (MNI): Blinken: Israel-Hamas Hostage Deal Is Still Possible

Wires carrying comments from US Secretary of State Antony Blinken on a range of issues. Blinken says he, "believes an Israel-Hamas hostage deal is possible," but there are some "very hard" issues to be resolved.

UKRAINE (MNI): Zelenskyy To Sign Security Deal w/France Ahead Of MSC Appearance:

President Volodymyr Zelenskyy will travel to the French capital Paris on 16 Feb to sign a bilateral security deal with his counterpart Emmanuel Macron.

MIDEAST (MNI): US Intercepts Iran Weapons Set For Houthis As Frequency Of Attacks Fall

US Central Command (CENTCOM) has posted on X a message confirming that a US Coastguard ship intercepted a vessel in the Arabian Sea that it claims was carrying "advanced conventional weapons and other lethal aid originating in Iran and bound to Houthi-controlled areas of Yemen".

OVERNIGHT DATA

US DATA (MNI): Poorest Retail Sales Report In 10 Months, Weather A Potential Factor. US retail sales came in weaker than expected in January's advance estimates, with the headline figure printing -0.8% M/M (vs -0.2% survey, 0.4% prior revised down from 0.6%).

- The core categories also started the year on a negative note, inc contrast to relative strength at the end of 2023: ex-autos -0.6% (+0.2% survey, +0.4% prior), ex-auto/gas -0.5% (+0.2% survey, +0.6% prior), and for the key Control Group which is a GDP input, -0.4% (+0.2%, +0.8% prior). Overall the contractions pointed to the weakest report since March 2023

US JOBLESS CLAIMS -8K TO 212K IN FEB 10 WK

US PREV JOBLESS CLAIMS REVISED TO 220K IN FEB 03 WK

US CONTINUING CLAIMS +0.030M to 1.895M IN FEB 03 WK

US JAN IMPORT PRICES +0.8%

US JAN EXPORT PRICES +0.8%; NON-AG +0.9%; AGRICULTURE -1.0%

US NY FED EMPIRE STATE MFG INDEX -2.4 FEB

US NY FED EMPIRE MFG NEW ORDERS -6.3 FEB

US NY FED EMPIRE MFG EMPLOYMENT INDEX -0.2 FEB

US NY FED EMPIRE MFG PRICES PAID INDEX 33.0 FEB

US FEB PHILADELPHIA FED MFG INDEX 5.2

US JAN INDUSTRIAL PROD -0.1%; CAP UTIL 78.5%

US DEC IP REV TO +0.0%; CAP UTIL REV 78.7%

US JAN MFG OUTPUT -0.5%

US DEC BUSINESS INVENTORIES +0.4%; SALES +0.4%

US DEC RETAIL INVENTORIES +0.6%

US NAHB HOUSING MARKET INDEX 48 IN FEB

US NAHB FEB SINGLE FAMILY SALES INDEX 52; NEXT 6-MO 60

CANADA DATA: Dec Manufacturing Declines, Q4 -1.6%

Dec sales -0.7% vs advanced estimate for -0.6%, prior +1.2%. Decrease led by motor vehicles and chemical products.

CANADA DATA: Jan Housing Starts -10% Despite Increased Demand

Seasonally adjusted starts -10% to 223,589 units after +18% MOM in Dec. Even with decline the total is the second highest for the month on Jan in records back to 1990

CANADIAN DEC MANUFACTURING SALES -0.7% MOM

CANADA DEC FACTORY INVENTORIES -0.6%; INVENTORY-SALES RATIO 1.73

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA up 313.03 points (0.81%) at 38740.92

- S&P E-Mini Future up 25.25 points (0.5%) at 5043.75

- Nasdaq up 34.3 points (0.2%) at 15895.58

- US 10-Yr yield is down 1.6 bps at 4.2398%

- US Mar 10-Yr futures are up 4.5/32 at 110-5

- EURUSD up 0.0042 (0.39%) at 1.0769

- USDJPY down 0.6 (-0.4%) at 149.98

- WTI Crude Oil (front-month) up $1.57 (2.05%) at $78.16

- Gold is up $11.91 (0.6%) at $2004.14

- European bourses closing levels:

- EuroStoxx 50 up 33.95 points (0.72%) at 4743.17

- FTSE 100 up 29.13 points (0.38%) at 7597.53

- German DAX up 101.21 points (0.6%) at 17046.69

- French CAC 40 up 66.07 points (0.86%) at 7743.42

US TREASURY FUTURES CLOSE

- 3M10Y +0.084, -115.045 (L: -120.585 / H: -113.088)

- 2Y10Y -0.542, -32.996 (L: -35.173 / H: -30.959)

- 2Y30Y -0.139, -14.668 (L: -17.993 / H: -11.665)

- 5Y30Y +1.137, 20.477 (L: 17.26 / H: 22.137)

- Current futures levels:

- Mar 2-Yr futures up 1/32 at 102-3.25 (L: 102-01.875 / H: 102-06.87)

- Mar 5-Yr futures up 3.25/32 at 106-26.5 (L: 106-23 / H: 107-02.5)

- Mar 10-Yr futures up 5/32 at 110-5.5 (L: 110-00.5 / H: 110-17.5)

- Mar 30-Yr futures up 10/32 at 118-27 (L: 118-18 / H: 119-20)

- Mar Ultra futures up 17/32 at 124-29 (L: 124-17 / H: 125-28)

US 10Y FUTURE TECHS: (H4) Corrective Bounce

- RES 4: 112-00 Round number resistance

- RES 3: 111-21+ High Feb 5

- RES 2: 111-02+ 20-day EMA

- RES 1: 110-17.5 High Feb 15

- PRICE: 110-05 @ 1500 ET Feb 15

- SUP 1: 109-17/16+ 50.0% of Oct 19 - Dec 27 climb / Low Feb 14

- SUP 2: 109-05+ Low Nov 28

- SUP 3: 108-19+ 61.8% of the Oct 19 - Dec 27 bull phase

- SUP 4: 108-14 Low Nov 15

A bear threat in Treasuries remains present and short-term gains are considered corrective. The break lower this week has confirmed a resumption of the downleg that started Dec 27. The 110-00 handle has been cleared and sights are on 109-17, a Fibonacci retracement. It has been tested, a clear break would open 109-05+, the Nov 28 low. Initial firm resistance is at 111-02+, the 20-day EMA.

SOFR FUTURES CLOSE

- Mar 24 -0.005 at 94.725

- Jun 24 steady00 at 95.005

- Sep 24 -0.005 at 95.335

- Dec 24 -0.005 at 95.665

- Red Pack (Mar 25-Dec 25) +0.005 to +0.025

- Green Pack (Mar 26-Dec 26) +0.030 to +0.035

- Blue Pack (Mar 27-Dec 27) +0.030 to +0.035

- Gold Pack (Mar 28-Dec 28) +0.030 to +0.035

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00156 to 5.31979 (-0.00093/wk)

- 3M -0.00659 to 5.31909 (+0.01004/wk)

- 6M -0.01340 to 5.24355 (+0.05489/wk)

- 12M -0.01429 to 5.00468 (+0.12443/wk)

- Secured Overnight Financing Rate (SOFR): 5.30% (-0.01), volume: $1.596T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $671B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $656B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $107B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $270B

US FED REVERSE REPO OPERATIONS

NY Federal Reserve/MNI

- RRP usage falls below $500B for the first time since early June 2021 today: $493.065B vs. $575.332B Wednesday.

- Meanwhile, the latest number of counterparties is at 82 from 91 Wednesday (compares to 65 on January 16, the lowest since July 7, 2021).

PIPELINE $2.55B Intel 3Pt Launched

$8B to Price Thursday, $44.85B/wk

- Date $MM Issuer (Priced *, Launch #)

- 2/15 $2.55B #Intel $500M 7Y +82, $900M 10Y +95, $1.15B 30Y +120

- 2/15 $1.7B #BAT Capital Corp 7Y +158, 10Y +183

- 2/15 $1.25B *World Bank 3Y SOFR+28

- 2/15 $750M *Waste Connections 10Y +92

- 2/15 $750M *Eastman Chemical 10Y +142

- 2/15 $500M #Kyndryl WNG 10Y +212.5

- 2/15 $500M #Mondelez 5Y +65

EGBs-GILTS CASH CLOSE: Marginally Weaker As Data Is Second-Guessed

Bunds and Gilts faded after a constructive start Thursday, with negative data surprises being second-guessed.

- Core FI got off on the front foot as Q4 UK GDP came in weak and confirmed a technical recession in 2H 2023, but the move fades as the report wasn't seen to be shifting the needle significantly for BoE policy.

- Likewise, Bunds and Gilts got a boost in early afternoon trade amid mixed-to-soft US data highlighted by poor January retail sales but eventually reversed lower as the miss was seen to be at least partially influenced by poor weather, and US jobless claims/regional manufacturing surveys were more favourable.

- While there was plenty of central banker commentary, from ECB's Lagarde and BoE's Greene (sounding as though she won't soon vote for a cut) among others, there was little evident immediate reaction in rates markets.

- Even so, rate cut expectations drifted lower overall on the day, with 77bp in BoE cuts now seen in 2024 (vs 79bp Weds); ECB cut pricing was likewise pared by 2bp, last 112bp.

- Bunds underperformed Gilts, with the German curve leaning bear flatter; the UK curve marginally bear steepened. Periphery spreads were a little tighter

- UK retail sales will be the highlight early Friday, concluding a busy week for UK data; we also hear from ECB's Schnabel (and BoE's Pill after the close).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.5bps at 2.755%, 5-Yr is up 3bps at 2.332%, 10-Yr is up 2.2bps at 2.359%, and 30-Yr is up 2.2bps at 2.531%.

- UK: The 2-Yr yield is up 0.5bps at 4.58%, 5-Yr is up 0.6bps at 4.063%, 10-Yr is up 1bps at 4.054%, and 30-Yr is up 2.5bps at 4.604%.

- Italian BTP spread down 2bps at 149.6bps / Spanish down 1.4bps at 91.6bps

FOREX USD Index Extends Retracement Lower Amid Equities Recovery

- Following Tuesday’s strong advance for the greenback on the back of hotter-than-expected inflation data, the past two sessions have seen the dollar steadily reverse lower. The USD index is down a further 0.40% on Thursday and has been assisted lower by the impressive recovery for major equity indices and e-mini S&Ps within close proximity of the all-time highs for the index.

- Associated gains for G10 currencies were broad based, with the likes of AUD, NZD and CAD all moderately outperforming and the Swiss Franc the major beneficiary to the more optimistic risk sentiment across global markets.

- USDCHF has declined 0.7% on the session but in the broader context remains around 5.5% above the December low, with the softer-than-expected local CPI data stoking the most recent CHF weakness this week.

- Overall, intra-day volatility was spurred on by a weaker set of January retail sales data in the US, however, firmer Philly Fed and Empire Manufacturing data quickly offset the greenback dip. USDJPY reached as low as 149.57 on the data from the earlier 150.58 highs, but has since settled around mid-range and close to the psychological 150.00 mark.

- EURUSD rose in line with the moves for the greenback, breaching its initial resistance point of 1.0750 (50% retracement for this week's downleg) and has continued to narrow the gap to the 50-dma which resides at 1.0796.

- UK retail sales data headlines the European docket on Friday before focus turns to US PPI figures and building permits. Preliminary UMich consumer sentiment and inflation expectations will round off the week.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 16/02/2024 | 1300/0800 |  | US | Richmond Fed's Tom Barkin | |

| 16/02/2024 | 1330/0830 | * |  | CA | International Canadian Transaction in Securities |

| 16/02/2024 | 1330/0830 | ** | | CA | Wholesale Trade |

| 16/02/2024 | 1330/0830 | *** | | US | PPI |

| 16/02/2024 | 1330/0830 | *** | | US | Housing Starts |

| 16/02/2024 | 1410/0910 | | US | Fed Vice Chair Michael Barr | |

| 16/02/2024 | 1500/1000 | ** | | US | U. Mich. Survey of Consumers |

| 16/02/2024 | 1710/1210 | | US | San Francisco Fed's Mary Daly | |

| 16/02/2024 | 1800/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 16/02/2024 | 1940/1940 |  | UK | BOE's Pill panellist at 40th NABE Conference |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.