Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

US TSYS: Risk Appetite Gains Momentum

Tsy well bid across the board holding narrow range since midmorning after 30YY fell to 4.2216% lows, FI mkts continues to reassess rate hike expectations for year end after SF Fed Daly voiced concern over tightening monetary policy too much last Friday.

- Yields curves bull flattening (2s10s -12.933 at -39.575) despite the strong support in short end as hike expectations for Dec move closer to 50bp than last week's 75bp pricing.

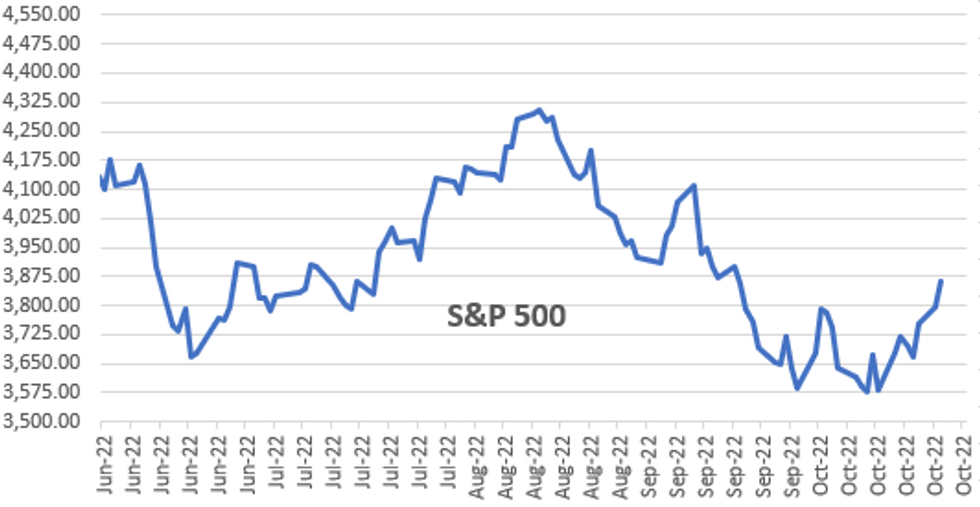

- Risk appetite gains momentum as stocks trade higher for third consecutive session: SPX emini +59.0 at 3868.25 (Sep 21 levels) not far from 3923.88: 50.0% retracement of the Aug 16 - Oct 13 downleg

- Softer than expected data contributing to today's moves while Tsy held gains, little react after $42B 2Y note auction (91282CFQ9) tailed: 4.460% high yield vs. 4.447% WI; 2.59x bid-to-cover vs. 2.51x prior.

- The 2-Yr yield is down 3.2bps at 4.4728%, 5-Yr is down 11.2bps at 4.2503%, 10-Yr is down 15.7bps at 4.0854%, and 30-Yr is down 14.6bps at 4.2324%.

EUROPE

ECB: The European Central Bank will likely hike its key deposit rate by 75bps on Thursday, confirming market expectations, and possibly announcing changes in the terms of its cheap loans to banks.

- Although the hike in the deposit rate to 1.5% and any indication on the forward path will be the main focus of attention, how policymakers look to deal with the growing problem for the national central banks of interest payments on reserve holdings will also be of concern.

- Although headline inflation saw some mixed messages in September, slowing in France and Spain, but accelerating in Germany, core inflation picked up again, and policymakers will likely reiterate their belief that a (possibly mild) euro area recession -- of which there is growing evidence and over which there is increasing concern --cannot by itself bring inflation back to the 2% target over the medium term.

OVERNIGHT DATA

- US OCT PHILADELPHIA FED NONMFG INDEX -14.9

- US AUG FHFA HPI SA -0.7% V -0.6% JUL; +11.9% Y/Y

- S&P CoreLogic Case-Shiller 20-City Index Up 13.1% Y/Y; Est 14.0%

- US OCT. CONSUMER CONFIDENCE AT 102.5; EST. 105.9

- US Oct. Richmond Fed Factory Index at -10 -bbg (-5 expected, 0 prior)

- The Richmond Fed mfg index missed in Oct, falling from 0 to -10 (cons -5), following equally sized misses for Empire (-9.1 vs -4.3 exp) and Philly (-8.7 vs -5.0 exp).

- The average -9.3 for the three is close to the Aug low of -11, as the Regional Fed surveys continue to signal risk to more significantly sub-50 ISM readings after yesterday’s 2pt decline in the preliminary mfg PMI to 49.9.

- Supply chains: “There was little indication of supply chain relief since August, as the indexes for vendor lead time and backlog of orders remained steady, although both have improved dramatically since earlier this year”

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 348.07 points (1.11%) at 31849.03

- S&P E-Mini Future up 61.25 points (1.61%) at 3870.5

- Nasdaq up 247.1 points (2.3%) at 11200.1

- US 10-Yr yield is down 15.5 bps at 4.0875%

- US Dec 10Y are up 29/32 at 110-20.5

- EURUSD up 0.0092 (0.93%) at 0.9966

- USDJPY down 1.01 (-0.68%) at 147.9

- WTI Crude Oil (front-month) up $0.45 (0.53%) at $85.02

- Gold is up $3.26 (0.2%) at $1653.04

- EuroStoxx 50 up 57.79 points (1.64%) at 3585.58

- FTSE 100 down 0.51 points (-0.01%) at 7013.48

- German DAX up 121.51 points (0.94%) at 13052.96

- French CAC 40 up 119.19 points (1.94%) at 6250.55

US TSY FUTURES CLOSE

- 3M10Y -20.098, 2.419 (L: -2.407 / H: 13.738)

- 2Y10Y -12.51, -39.164 (L: -39.17 / H: -27.056)

- 2Y30Y -11.303, -24.353 (L: -24.462 / H: -11.409)

- 5Y30Y -3.076, -1.859 (L: -2.076 / H: 5.306)

- Current futures levels:

- Dec 2Y up 2.875/32 at 102-9.375 (L: 102-05.375 / H: 102-13.5)

- Dec 5Y up 14.25/32 at 106-19.5 (L: 106-03 / H: 106-28)

- Dec 10Y up 29/32 at 110-20.5 (L: 109-20 / H: 110-31.5)

- Dec 30Y up 2-2/32 at 120-12 (L: 118-05 / H: 120-22)

- Dec Ultra 30Y up 2-28/32 at 127-12 (L: 124-02 / H: 127-21)

US 10YR FUTURE TECH: (Z2) Corrective Bounce

- RES 4: 113-18 50-day EMA

- RES 3: 112-22+ High Oct 6

- RES 2: 111-28+ High Oct 13 and key near-term resistance

- RES 1: 111-11 20-day EMA

- PRICE: 110-26+ @ 15:35 BST Oct 25

- SUP 1: 108-26+ Low Oct 21 and the bear trigger

- SUP 2: 108-06+ Low Oct 2007 (cont)

- SUP 3: 107.05 3.0% 10-dma envelope

- SUP 4: 106-20+ Low Aug 2007 (cont)

Treasuries have recovered further off the Friday low. The primary trend is unchanged despite this bounce and remains lower. The extension lower last week confirmed a break of support at 110.02, Oct 13 low and the psychological 110.00 handle. This resumes the primary downtrend and marks an extension of the price sequence of lower lows and lower highs. The focus is on 108-20, a Fibonacci projection. Initial firm resistance has been defined at 111-28+, the Oct 13 high.

US EURODOLLAR FUTURES CLOSE

- Dec 22 +0.015 at 94.90

- Mar 23 +0.005 at 94.805

- Jun 23 +0.005 at 94.860

- Sep 23 +0.020 at 95.020

- Red Pack (Dec 23-Sep 24) +0.035 to +0.065

- Green Pack (Dec 24-Sep 25) +0.070 to +0.110

- Blue Pack (Dec 25-Sep 26) +0.120 to +0.145

- Gold Pack (Dec 26-Sep 27) +0.150 to +0.150

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00300 to 3.06271% (-0.001415/wk)

- 1M +0.02000 to 3.59643% (+0.01086/wk)

- 3M +0.03114 to 4.35800% (-0.00043/wk) * / **

- 6M +0.03857 to 4.91557% (+0.04057/wk)

- 12M +0.03371 to 5.39971% (-0.07586/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.35843% on 10/21/22

- Daily Effective Fed Funds Rate: 3.08% volume: $99B

- Daily Overnight Bank Funding Rate: 3.07% volume: $276B

- Secured Overnight Financing Rate (SOFR): 3.01%, $962B

- Broad General Collateral Rate (BGCR): 3.00%, $388B

- Tri-Party General Collateral Rate (TGCR): 3.00%, $376B

- (rate, volume levels reflect prior session)

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,195.616B w/ 102 counterparties vs. $2,242.044B in the prior session. Prior record high stands at $2,425.910B on Friday, September 30.

PIPELINE: $9B United Health 7Pt Jumbo Launched

- Date $MM Issuer (Priced *, Launch #)

- 10/25 $9B #United Health $500M 2Y +55, $750M 3Y +70, $1B +5Y +100, $1.25B +7Y +115, $2 +10Y +130, $2B +30Y +165, $1.5B +40Y +185

- 10/25 $4B *CADES 3Y Social SOFR+46

- 10/25 $2.5B #PNC Financial $1B 3NC2 +120, $1.5B 11NC10 +195

- 10/25 $1B *OKB WNG 3Y SOFR+37

- 10/25 $Benchmark Farmer Insurance investor calls

EGBs-GILTS CASH CLOSE: Broad Rally As Terminal Hike Pricing Pared Further

German yields dropped sharply Tuesday in a strong bull flattening move, while periphery EGBs maintained their solid performance ahead of the ECB meeting Thursday.

- Amid continued downward repricing of Federal Reserve hike expectations and further weak US housing data, global yields fell sharply alongside a weaker USD. Long-end Bunds outperformed, while UK 10Y yields were down by double-digits.

- BoE terminal rate pricing dropped by 6bp, closing below 5% for the first time since Sept 22, with Gilt markets calming further as ex-Chancellor Sunak officially became PM.

- ECB terminal hike pricing fell by around 10bp, though expectations for this week's decision were steady (92% chance ofa 75bp hike). MNI reported the ECB is set to make changes to the terms of TLTRO loans this Thursday.

- BTPs outperformed amid a broader risk-on rally.

CLOSING YIELDS / 10-YR PERIPHERY EGB SPREADS TO GERMANY:

- Germany: The 2-Yr yield is down 4bps at 1.969%, 5-Yr is down 11.9bps at 2.03%, 10-Yr is down 16.4bps at 2.166%, and 30-Yr is down 19.8bps at 2.139%.

- UK: The 2-Yr yield is down 1.4bps at 3.414%, 5-Yr is down 7.2bps at 3.75%, 10-Yr is down 11.2bps at 3.634%, and 30-Yr is down 8.8bps at 3.668%.

- Italian BTP spread down 5.7bps at 220.2bps / Greek down 0.7bps at 251.5bps

FOREX: Greenback Slumps Following Housing Data, GBP Surges

- Data on Tuesday indicated the sharpest slowdown in US house price growth on record and the US Dollar really felt the pinch in the aftermath. The greenback weakness began to build momentum approaching the US cash equity open, with the BBG USD Index consistently under pressure through to the NY cut at 1000 ET, where the losses then consolidated for the rest of the session.

- The move has heavily favoured GBP/USD (+1.80%), with the pair sharply extending through yesterday's highs of 1.1409 and reaching a peak of 1.1499 in a potentially delayed response to the new appointment of Prime Minister Sunak and the expectation of more benign policy for markets.

- Cable has briefly pierced 1.1495, the Oct 5 high and the technical bull trigger. Above here, markets will turn their focus to 1.1590, the Sep 14 high.

- Similarly, USD/CNH staged a decent relief rally, with the pair edging off the record highs of 7.3749 printed overnight - coinciding with EUR/USD back above $0.99.

- EURUSD is extending the latest recovery, from 0.9705, the Oct 21 low and today’s price action is potentially significant. The pair is trading above an important resistance level at 0.9874 - the top of the bear channel drawn from the Feb 10 high.

- A clear break of this level would highlight a channel breakout and a stronger bullish reversal. The short-term focus now turns to 0.9999, the Oct 4 high and a reversal trigger.

- Similar strength was seen for the likes of AUD and NZD, although this mainly marked a reversal of Monday’s sharp losses associated with Chinese concerns.

- Australian CPI is due overnight before tomorrow’s main event which is the Bank of Canada rate decision. Some emphasis may also be placed on US new home sales data after the poor figures released today.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/10/2022 | 0030/1130 | *** |  | AU | CPI inflation |

| 26/10/2022 | 0600/1400 | ** |  | CN | MNI China Liquidity Suvey |

| 26/10/2022 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 26/10/2022 | 0800/1000 | ** |  | EU | M3 |

| 26/10/2022 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 26/10/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 26/10/2022 | 1230/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 26/10/2022 | 1400/1000 | *** |  | CA | Bank of Canada Policy Decision |

| 26/10/2022 | 1400/1000 | | CA | BOC Monetary Policy Report | |

| 26/10/2022 | 1400/1000 | *** | | US | New Home Sales |

| 26/10/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 26/10/2022 | 1500/1100 | | CA | BOC Governor Press Conference | |

| 26/10/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 26/10/2022 | 1700/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.