Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI: Tighter Fin. Conditions Could Affect Policy Path -Minutes

- MNI US DATA: Existing Home Sales Continue Slide In October

US

FED: Federal Reserve officials believed tighter financial conditions could lessen the need for additional monetary tightening as they decided to hold interest rates steady for the second straight meeting earlier this month, according to minutes of the central bank's November meeting.

- “Financial conditions had tightened significantly in recent months,” the minutes said. “Persistent changes in financial conditions could have implications for the path of monetary policy and it would therefore be important to continue to monitor market developments closely.”

- A spike in ten-year Treasury note yields to around 5% in recent months has been a major focus of policymakers, many of whom have said tighter financial conditions could reduce the need for additional Fed tightening. Still, long-term rates have retraced a substantial part of that rise, and ten-year note is currently yielding around 4.4%.

- Top policymakers have not closed the door to additional hikes in recent public remarks, but many have indicated the bar is high for further tightening. That's because recent inflation readings have been benign, labor market activity is moderating, and many officials are convinced policy lags have yet to fully kick in. For more see MNI Policy Main Wire at 1406ET.

US TSYS Muted React To Nov FOMC Minutes, Watching Financial Conditions Closely

- Treasury futures are firmer for the most part, 30Y Bond still mildly weaker vs. the balance of the strip. Still inside a narrow session range, markets showed little reaction to the November FOMC minutes.

- Fed officials believed tighter financial conditions could lessen the need for additional monetary tightening as they decided to hold interest rates steady for the second straight meeting earlier this month. “Financial conditions had tightened significantly in recent months,” the minutes said. “Persistent changes in financial conditions could have implications for the path of monetary policy and it would therefore be important to continue to monitor market developments closely.”

- Tsy futures had extended highs after this morning's lower than expected Existing Home Sales data (3.79M vs. 3.9M est, 3.95M prior/rev), MoM (-4.1% vs. -1.5M est, -2.2% prior/rev).

- Dec'23 10Y futures had tapped 109-03.5 high (+8.5), pared gains after the 10Y TIPS auction drew 2.180% yield vs. 2.94% prior. TYZ3 trades 108-30.5 last, still well above initial technical support below at 108-04 (50-day EMA). Initial technical resistance at 109-08+ (High Nov 17).

- Heavy volumes (TYZ3 >2.7M) is due to a surge in quarterly futures rolling ahead First Notice on Nov 30.

- Reminder: shortened Thanksgiving holiday week: full session Wednesday sees weekly claims, durables/cap-goods and UofM conditions/inflation expectations., Thursday close, Friday early close.

OVERNIGHT DATA

US DATA: Existing home sales were lower than expected in October at 3.79m (cons 3.90m), with a clean read on the month after only marginal revisions.

- The latest profile sees sales falling -4.1% M/M (cons -1.5) after -2.2% (initial -2.0), for the largest single seasonally adjusted monthly decline since Nov’22.

- Whilst lower than expected, the relative level of existing home sales is in keeping with the prior decline in pending sales, now almost 30% below the 2019 average.

- Months of supply showed further signs of the housing market moving back closer to pre-pandemic balances, up from 3.4 to 3.6 on the month for the highest October since 2019 and vs the 4.1 averaged in 2017-19 Octobers.

- US NOV PHILADELPHIA FED NONMFG INDEX -11

- CHICAGO FED NATIONAL ACTIVITY INDEX AT -0.49 VS -0.02 PRIOR

- US REDBOOK: NOV STORE SALES +3.2% V YR AGO MO

- US REDBOOK: STORE SALES +3.4% WK ENDED NOV 18 V YR AGO WK

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA down 82.81 points (-0.24%) at 35067.58

- S&P E-Mini Future down 11.5 points (-0.25%) at 4550.5

- Nasdaq down 79 points (-0.6%) at 14204.86

- US 10-Yr yield is down 1 bps at 4.4101%

- US Dec 10-Yr futures are up 3/32 at 108-30

- EURUSD down 0.0025 (-0.23%) at 1.0915

- USDJPY down 0.09 (-0.06%) at 148.3

- Gold is up $21.39 (1.08%) at $1999.49

- European bourses closing levels:

- EuroStoxx 50 down 10.51 points (-0.24%) at 4331.9

- FTSE 100 down 14.37 points (-0.19%) at 7481.99

- German DAX down 0.8 points (-0.01%) at 15900.53

- French CAC 40 down 17.48 points (-0.24%) at 7229.45

US TREASURY FUTURES CLOSE

- 3M10Y +1.261, -98.327 (L: -105.733 / H: -95.992)

- 2Y10Y +2.436, -47.091 (L: -52.384 / H: -45.516)

- 2Y30Y +3.309, -31.109 (L: -38.374 / H: -28.671)

- 5Y30Y +2.402, 15.439 (L: 9.998 / H: 17.209)

- Current futures levels:

- Dec 2-Yr futures up 1.5/32 at 101-17 (L: 101-14.875 / H: 101-18.5)

- Dec 5-Yr futures up 2.75/32 at 105-30.25 (L: 105-25.25 / H: 106-02)

- Dec 10-Yr futures up 3.5/32 at 108-30.5 (L: 108-23.5 / H: 109-03.5)

- Dec 30-Yr futures down 3/32 at 115-23 (L: 115-08 / H: 116-14)

- Dec Ultra futures down 2/32 at 120-18 (L: 119-29 / H: 121-18)

US 10Y FUTURE TECHS: (Z3) Trend Needle Points North

- RES 4: 110-07+ High Sep 14

- RES 3: 110-00 Round number resistance

- RES 2: 109-20 High Sep 19

- RES 1: 109-08+ High Nov 17

- PRICE: 108-30.5 @ 1500ET Nov 21

- SUP 1: 108-04 50-day EMA

- SUP 2: 107-27+ 20-day EMA

- SUP 3: 107-00 Low Nov 13

- SUP 4: 106-02+ 2.0% 10-dma envelope

Treasuries are unchanged. Short-term bullish conditions remain intact and the contract is trading closer to its recent highs. Price has recently traded above resistance at 108-25, the Nov 3 high. A clear break of this hurdle would signal scope for an extension towards 109-20, the Sep 19 high. Key short-term support has been defined at 107-00, the Nov 13 low. A reversal and a break of this support, would instead highlight a bearish threat.

SOFR FUTURES CLOSE

- Current White pack (Dec 23-Sep 24):

- Dec 23 -0.003 at 94.615

- Mar 24 +0.005 at 94.755

- Jun 24 +0.010 at 94.995

- Sep 24 +0.020 at 95.290

- Red Pack (Dec 24-Sep 25) +0.030 to +0.050

- Green Pack (Dec 25-Sep 26) +0.025 to +0.045

- Blue Pack (Dec 26-Sep 27) +0.010 to +0.020

- Gold Pack (Dec 27-Sep 28) steady to +0.005

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00596 to 5.34079 (+0.00826/wk)

- 3M +0.00651 to 5.37802 (+0.01109/wk)

- 6M +0.00734 to 5.38015 (+0.01668/wk)

- 12M +0.01516 to 5.24150 (+0.04077/wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $101B

- Daily Overnight Bank Funding Rate: 5.32% volume: $257B

- Secured Overnight Financing Rate (SOFR): 5.31%, $1.621T

- Broad General Collateral Rate (BGCR): 5.30%, $588B

- Tri-Party General Collateral Rate (TGCR): 5.30%, $574B

- (rate, volume levels reflect prior session)

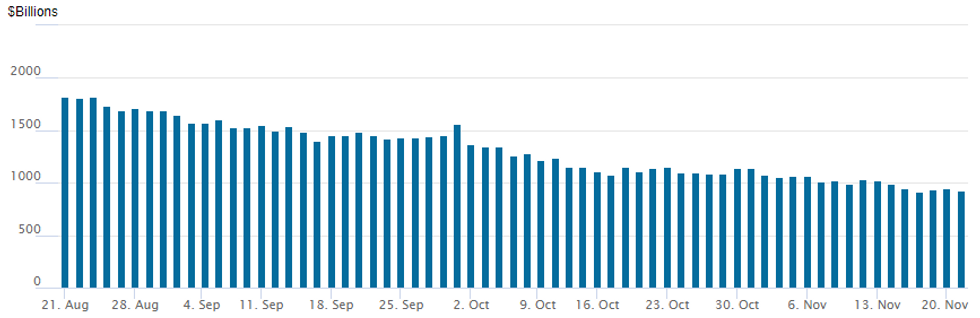

FED REVERSE REPO OPERATION

NY Federal Reserve/MNI

The NY Fed Reverse Repo operation usage slipped to $931.155B w/95 counterparties today vs. $953,088B Monday. Usage fell below $1T for the first time since August 2021 last on November 9 ($993.314B) declining to $912.010B on November 16 - the lowest level since early August 2021.

PIPELINE $2B AfDB +2Y SOFR, $500M Kommuninvest 5Y Priced

Should wrap up the pre-holiday high-grade corporate issuance:

- Date $MM Issuer (Priced *, Launch #)

- 11/21 $2B *AfDB 2027 SOFR+36

- 11/21 $500M *Kommuninvest WNG 5Y +47

EGBs-GILTS CASH CLOSE: Gilts Underperform Ahead Of UK Autumn Statement

Bunds outperformed Gilts and reversed most of Monday's losses in a constructive session Tuesday, with the German curve bull flattening and the UK's twist flattening.

- ECB and BoE speakers largely reiterated the higher-for-longer narrative, though some of BoE Gov Bailey's commentary today re market pricing were explicit than in the past, in line with those that we have seen recently from hawks Mann and Greene.

- BTPs underperformed with spreads widening marginally on the day. The European Commission warned that the draft 2024 budgets of multiple countries were either not fully in line or risk not being in line with EU guidance, including Germany, Italy, and France.

- Gilts started strong but traded with little direction, with futures trade beginning to reflect the quarterly roll period (MNI Europe Pi sees the contract as marginally short going into the roll).

- The UK autumn statement looms large Wednesday - MNI's preview was out today, including potential impact on Gilt issuance.

- The European data slate remains relatively thin Wednesday, with Eurozone consumer confidence the highlight. We also hear from ECB's Nagel and Centeno. Additionally, the Netherlands holds elections - MNI's preview is here.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3.3bps at 2.994%, 5-Yr is down 5bps at 2.521%, 10-Yr is down 4.5bps at 2.566%, and 30-Yr is down 3.3bps at 2.77%.

- UK: The 2-Yr yield is up 1.4bps at 4.545%, 5-Yr is up 2.6bps at 4.138%, 10-Yr is down 2bps at 4.105%, and 30-Yr is down 1.5bps at 4.537%.

- Italian BTP spread up 1.7bps at 175.1bps / Greek down 1.5bps at 120.2bps

FOREX USD Index Recovers Into Positive Territory As Thanksgiving Approaches

- The greenback has traded on a firmer note across US hours, with the USD index erasing its earlier declines and extending into positive territory ahead of the FOMC minutes. While no surprises within the minutes, similarly positive price action for the greenback prevailed in the direct aftermath. This was mainly reflective of the grinding downward pressure on major equity indices throughout the session amid potential profit taking dynamics in play, especially as we approach the Thanksgiving Holiday in the US.

- The most notable uptick has been for USDJPY, which makes sense given its more volatile nature in recent sessions and its impressive extension lower below 150.00 from last week. After reaching a low of 147.15, the pair now trades around 148.35 as we approach the APAC crossover, having traded as high as 148.60 after the minutes release.

- Overall, support at 149.16 (50-day EMA), has been cleared. This strengthens a short-term bearish theme and signals scope for a deeper correction, towards 146.00, a trendline support drawn from the Mar 24 low.

- EURUSD has echoed this sentiment, however the moves have been much more measured with 1.0900 limiting the downside and the pair consolidating around 1.0915 at typing.

- RBA Governor Bullock is due to speak overnight about the economic outlook and monetary policy at the Australian Business Economists Annual Dinner. AUDUSD has kept a fairly narrow range on Tuesday and trades close to unchanged at 0.6555. Importantly, the latest rally has resulted in a clear break of former resistance at 0.6522, the Aug 30 and Sep 1 high. The breach is an important short-term bullish development and signals scope for a continuation higher near-term towards 0.6616 next, the Oct 8 high.

- Elsewhere on Wednesday, markets will await the UK’s Autumn Forecast Statement, and in the US, initial jobless claims, durable goods and revised UMich sentiment data are all scheduled.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 22/11/2023 | 1100/1100 | ** |  | UK | CBI Industrial Trends |

| 22/11/2023 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 22/11/2023 | 1230/1230 | | UK | UK Autumn Statement | |

| 22/11/2023 | 1330/0830 | ** | | US | Durable Goods New Orders |

| 22/11/2023 | 1330/0830 | *** | | US | Jobless Claims |

| 22/11/2023 | 1410/1510 |  | EU | ECB's Elderson keynote speech on stability in the Green Transition | |

| 22/11/2023 | 1500/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 22/11/2023 | 1500/1000 | ** | | US | U. Mich. Survey of Consumers |

| 22/11/2023 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 22/11/2023 | 1530/1530 | | UK | DMO publish agenda for quarterly meetings | |

| 22/11/2023 | 1630/1130 |  | CA | BOC Governor Tiff Macklem speech/press conference | |

| 22/11/2023 | 1700/1200 | ** | | US | Natural Gas Stocks |

| 23/11/2023 | 2200/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.