Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- A majority of 22 sell-side analysts in a Bloomberg survey expect Bank Indonesia to keep the 7-Day Reverse Repo Rate unchanged this week, while the remaining 14 economists call for a 25bp hike. We cautiously side with the stand-pat camp but cannot rule out a rate rise.

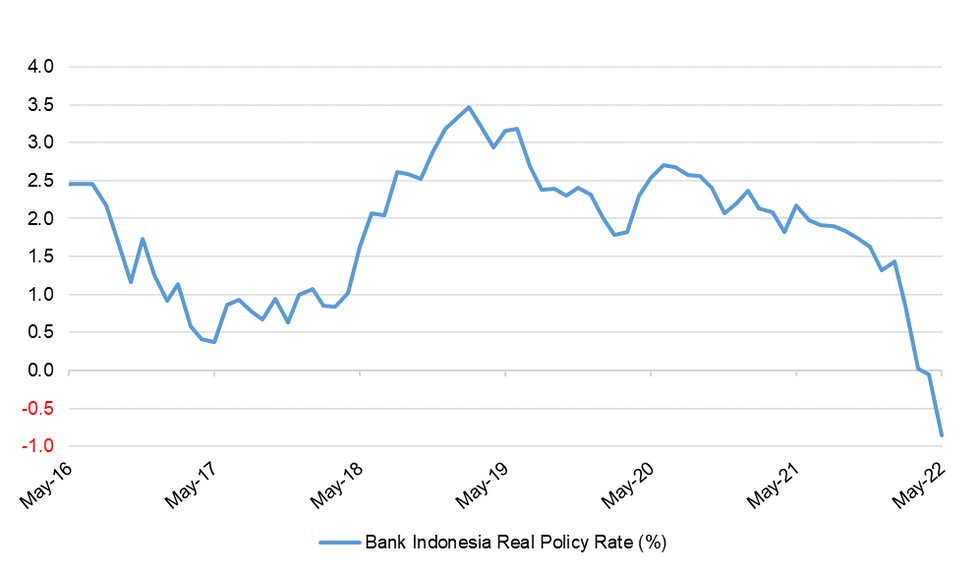

- Pressure keeps mounting on Bank Indonesia to fire the starting pistol on its rate-hike cycle. Rupiah stability indicators are sending warning signals, while narrowing yield differentials reduce the attractiveness of local assets. Furthermore, accelerating inflation is pushing the real policy rate deeper into negative territory.

- Nonetheless, Bank Indonesia has been vocal about focusing on core inflation as the key indicator of price pressures. The main metric of underlying inflation remains below the mid-point of the target range, with the Bank still "comfortable" with current levels of inflation.

- The global commodity boom has allowed Indonesia to fund subsidies and keep inflation in check. It has also underpinned Indonesia's trade surplus, lending support to the rupiah. Resultant price stability has put Bank Indonesia in a comfortable position to hold off on raising the key policy rate longer than most of its peers.

- We are looking at a live meeting, with Bank Indonesia on the cusp of interest-rate action. If its opts to stand pat, which is our base-case scenario, focus will turn to the imminent budget speech from President Widodo, in which he may provide some clarity on the outlook for fiscal efforts to cushion inflation.

Fig. 1: Bank Indonesia Real Policy Rate (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Click here to access the full preview: MNI BI Preview July 2022.pdf

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok