Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Russia Central Bank

Executive Summary:

- CBR expected to rase its Key Rate +75bp, with material risks to +100bp

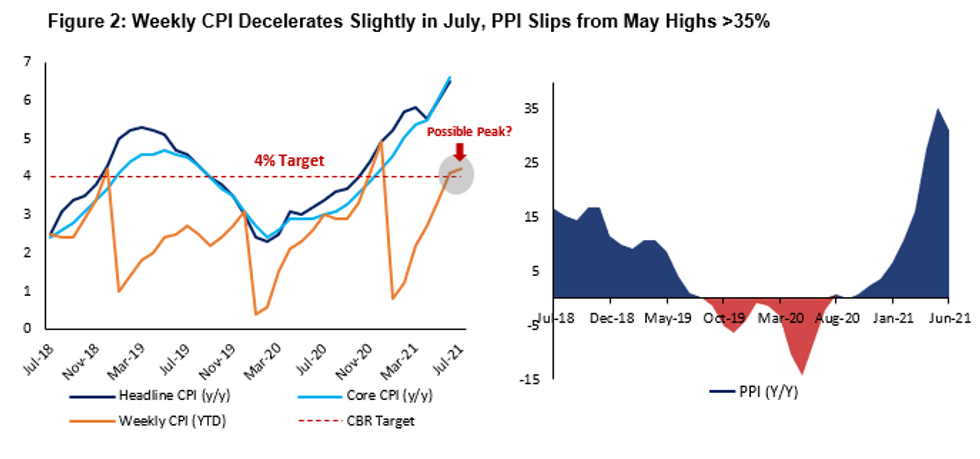

- Headline & Core CPI rose to 6.5% & 6.6% Y/Y in June, with expected to tick higher to 6.7% Y/Y in July

- However, demand-side drivers evident in growth-related high-frequency data have shown signs of moderation in June alongside weekly CPI prints in July

- Although base effects are expected to filter through in the coming months, CBR will not wish to continue chasing data and rather act decisively to anchor runaway expectations through a larger hike than the prior two +50bp meetings - which have done little to temper overshooting pressures in CPI

- Guidance in the prior meeting and subsequent TV interviews has also been hawkish, stressing that "the balance of risks had shifted significantly towards pro-inflationary ones"

- Nabiullina will likely also be careful to retain the prior meeting's relatively hawkish tone - alluding to data-dependent future developments until the decceleration in pro-inflationary factors becomes more deeply ensconced.

- Medium term forecasts are expected to be revised higher in terms of average and year-end inflation. 2021 Growth forecasts may also be revised higher towards 4.0%.

Full Preview Here:

Despite the broad uncertainty surrounding this meeting, as reflected in the +50-100bps range of expectations, we see the CBR delivering a +75bps hike with risks to +100bps as sharply overshooting CPI continues to drive policy rates beyond the 5-6% neutral range in the near-term. Elevated uncertainty in the pricing outlook may see the CBR seek to retain the optionality of a further +25-50bps in the pipeline for September, should prices fail to moderate on favourable base effects.

MNI London Bureau | +44 020-3983-7894 | murray.nichol@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok