Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI BanRep Preview - December 2021

Executive Summary

- Analysts are unanimous that BanRep will continue their tightening cycle in December, with the majority forecasting another hike to the overnight lending rate of 50bp to 3.00%.

- Continued upward pressures on inflation and inflation expectations, together with a solid growth profile, justify a further withdrawal of monetary stimulus.

- Calls for even bolder action at the December meeting seem unwarranted given the previously divided board, the desire for gradual monetary policy normalisation and ongoing uncertainty surrounding the evolution of the pandemic.

Click to view the full preview: MNI BanRep Preview - December 2021.pdf

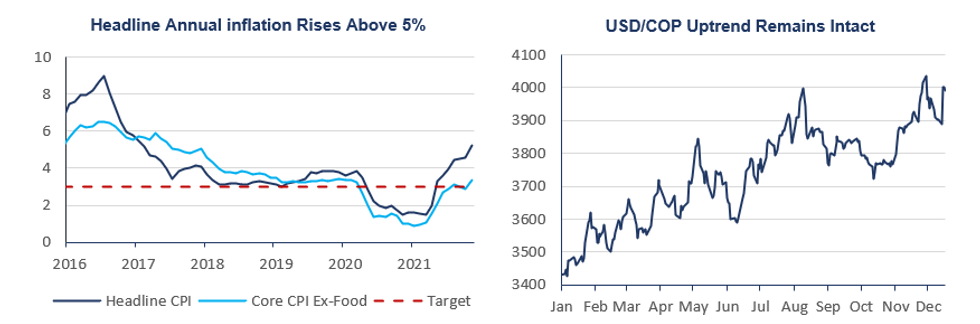

Core Inflation Rises Back Above Target Mid-Point

Despite October headline inflation printing well below estimates at 4.58%, renewed upward pressures were evident in the November data. Annual CPI rose to 5.26% versus a median estimate of 4.95%. Furthermore, core CPI, despite dipping below the 3% level in October, accelerated to 3.37% and therefore back above the target mid-point.

From the latest central bank survey, the median estimate from approximately 40 economists showed 2021 year-end inflation fairly consistent at 4.85% versus 4.9% in October. However, one-year inflation expectations rose to 3.65% from 3.5%, while two-year inflation expectations rose to 3.23%. The contamination of medium-term expectations and the likely continued pressure on these metrics confirm the need for firm action at the December meeting.

Growth Profile Warrants Additional Monetary Tightening

Economic activity has continued to recover at a faster rate than anticipated. Third quarter GDP beat estimates at 5.7% Q/q, prompting the annual figure to jump to 13.2%. The data is consistent with a negative, but quickly narrowing output gap with increasing domestic demand accounting for most of the advance. Indeed, in the presentation of the financial stability report, Governor Villar said “macroeconomic indicators and financial indicators coincide in showing that the worst of the crisis is over”. Additionally, Villar commented that “not only is it over, but we are in a recovery process that has been so fast that the level of activity is already above the pre-pandemic level”.

Source: MNI/Bloomberg

Source: MNI/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.