Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

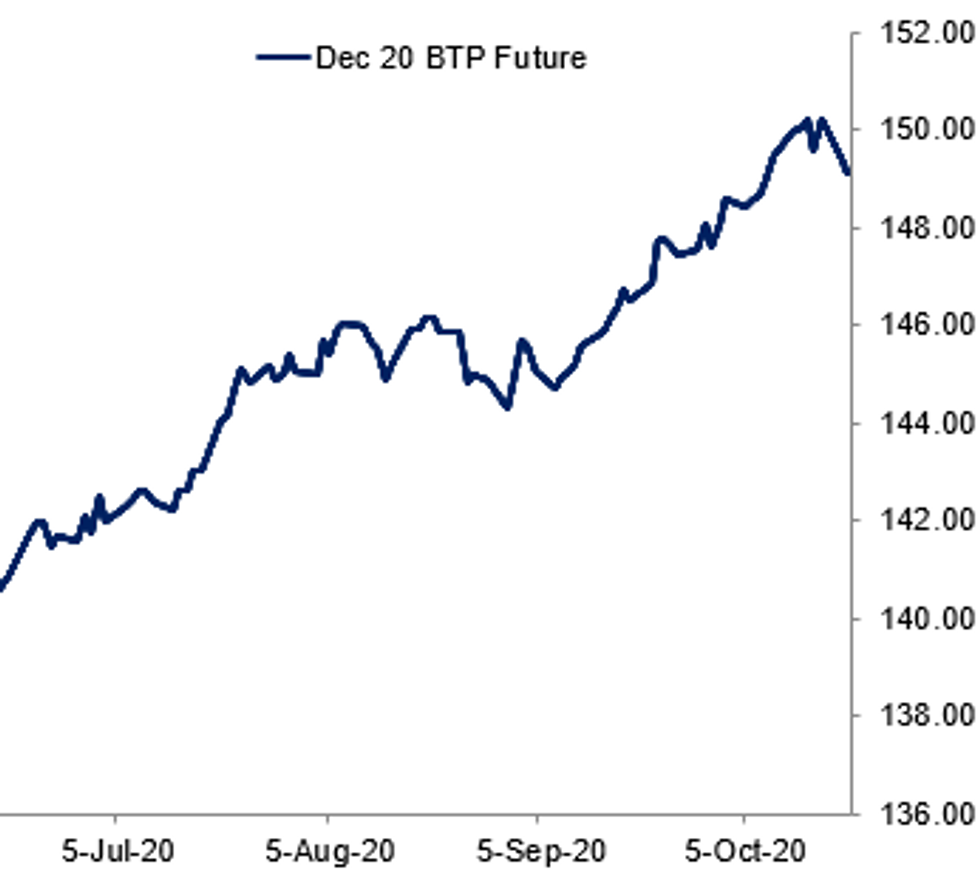

Fig. 1: BTPs Fade Gains Made On Issuance News

BBG, MNI

BBG, MNI

EGB SUMMARY: Supply headlines dominate

Familiar themes have been the drivers today with Brexit talks continuing and Covid-19 concerns lingering.

- The first EU SURE bonds were launched today via syndication with a dual tranche issue. EUR10bln of the 10-year was issued and EUR7bln of the 20-year with books over EUR233bln. Greece also announced a mandate for a tap of the 1.875% Feb-35 GGB.

- Reuters reported that a new 8-year BTP Futura would be launched next week. Furthermore, Reuters report that the Director General of the Italian Treasury said that funding for the remainder of the year will be 30% lower than last year - not a huge shock given Italy had already issued EUR50bln more than its previously published 2020 target and is due to receive EU SURE funds towards the end of the year. BTPs initially spiked to their highs of the day on the news, but have since retraced half of this gain.

- Bund futures are down -0.17 today at 175.94 with 10y Bund yields up 1.8bp at -0.611% and Schatz yields unch at -0.791%.

- BTP futures are down -0.14 today at 149.29 with 10y yields up 0.9bp at 0.728% and 2y yields down -0.1bp at -0.330%.

- OAT futures are down -0.03 today at 169.92 with 10y yields up 0.7bp at -0.336% and 2y yields down -0.4bp at -0.714%.

GILT SUMMARY: Bear Steepening

Follow a quiet initial start, gilts have sold off through the day with the long-end underperfroming and the curve bear steepening.

- Cash yields are 1-3bp higher on the day. Last yields: 2-year -0.0644%, 5-year -0.0786%, 10-year 0.1900%, 30-year 0.7406%.

- The Dec-20 gilt future trades at 136.46, near the bottom of the day's range (L: 136.44 / H: 136.75).

- The DMO earlier sold GBP600mn of the 1.25% Nov-32 linker.

- The BoE purchased GBP1.437bn of long-dated gilts with offer to cover of 2.55x.

- After talks between the government and Manchester city officials failed to reach a deal over new social restrictions, tier-three restrictions are expected to be implemented.

DEBT FUTURES/OPTIONS:

- 0LZ0/3LZ0 100c calendar, sold the 1yr at 4 and 3.75 in 1.5k

- OEZ0 135.50/25/00 p ladder, bought for 3 in 2.5k

- RXZ0 173.50/172.50ps, bought for 9 in 2k* RXZ0 175/177^^ bought for 99 up to 101 in 2k

- RXZ0 176^,sold at 181 in 600, 180 in 300, and 179 in 300

- RXZ0 178c, sold at 24.5 in 750 (ref 176.04)

- RXZ0179.5/181cs, bought for 5 in 1k

- RXZ0 174.5/173ps vs 178c bought for-1.5 in 5k

- DUZ0 112.40/30ps, bought for 3.5 in 3k

- DUZO 112.40/30/20p fly, bought for 2 in 2k

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok