Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- ACGBs (YM +4.0 & XM +4.5) sit 5-6bps richer after the RBA Policy Decision, with OIS also lower. The on hold outcome was expected, but the RBA noted monthly inflation figures pointed to a further moderation in inflation. AUD/USD has softened, underperforming the rest of the G10.

- JGB futures are higher, +5 compared to settlement levels, after holding a small loss at the lunch break. This shift into positive territory surprisingly coincided with news that today’s 10-year supply saw lacklustre demand metrics.

- Elsewhere, China related equities remain under pressure, with no let up in selling pressure. A better than expected Caixin services PMI print didn't improve the mood. USD/CNH is off highs though, Reuters reporting that state banks have been supporting the onshore yuan.

- Later, ECB CPI Expectations and Eurozone PPI are due in Europe, further out we have ISM Services and JOLTS Job Openings.

MARKETS

US TSYS: Firm From Session Lows Alongside ACGBs, Ranges Narrow

TYH4 deals at 110-15+, +0-09+, a 0-07 range has been observed on volume of ~61k.

- Cash tsys sit 1-2bps richer across the major benchmarks, light bull flattening is apparent.

- Tsys firmed from session lows as a bid in ACGBs, in lieu of the RBA holding the cash rate steady at 4.35% and the statement noting that inflation is continuing to moderate.

- Earlier in the session Tsys were muted dealing in a narrow range for the most part.

- ECB CPI Expectations and Eurozone PPI are due in Europe, further out we have ISM Services and JOLTS Job Openings.

JGBS: Futures Stronger Despite A Poor 10Y Auction

JGB futures are higher, +5 compared to settlement levels, after holding a small loss at the lunch break. This shift into positive territory surprisingly coincided with news that today’s 10-year supply saw lacklustre demand metrics. The low price failed to meet wider expectations, the tail lengthened, and the cover ratio declined to the lowest level seen at a 10-year auction since 2021.

- Demand seems to have faced a setback due to an outright yield that was approximately 20bps lower, along with a 2/10 yield curve that was 13bps flatter compared to the levels seen in early November. Despite the prevailing bullish sentiment towards long-end global bonds and the relative affordability of 10-year JGBs compared to futures with a 7-year maturity, these factors were not enough to bolster the bid during today's auction.

- There wasn't much in the way of domestic data to flag, outside of the previously outlined Tokyo CPI, which surprised on the downside.

- Cash JGBs remain mixed, with yield movements bounded by +/-1bp. The benchmark 10-year yield is 0.8bp lower at 0.691% versus a pre-auction high of 0.704%.

- Swaps are also dealing mixed, with swap spreads tighter.

- (Reuters ICYMI) Japan plans to issue Y1.6tn of climate transition bonds with five- and 10-year tenors in February, three people with direct knowledge of the matter said.

- Tomorrow, the local calendar is empty.

JAPAN DATA: Tokyo Nov CPI Weaker Than Expected

Tokyo Nov CPI printed below expectations across all measures. The headline was 2.6%y/y versus 3.0% expected and a revised 3.2% print for Oct. The ex fresh food measure printed at 2.3%, versus 2.4% expected and 2.7% prior. The ex fresh food, energy metric was 3.6% y/y (3.7% forecast and 3.8% prior).

- Headline CPI is now back to mid 2022 levels, while core (ex fresh food and energy) has edged away from recent cyclical highs near 4%. The core measure which excludes all food and energy was stable at 2.7% y/y though.

- In m/m terms the core measures were either flat or down. Goods inflation fell -0.6% m/m (+1.6% prior), services inflation eased back to 0.2% (prior 0.4%)

- Food was -0.9% m/m, utilities -0.4%, household goods -0.9% and entertainment at -0.3% were the main drags.

- In y/y terms, utilities remain a large drag -15.3%. 9 out of 11 of the sub categories saw either lower or unchanged y/y momentum versus Oct.

Fig 1: Tokyo CPI Y/Y Trends - Resume Shift Lower

Source: MNI - Market News/Bloomberg

RBA: RBA Dated OIS Shunts Softer After The RBA Policy Decision

Figure 1: RBA-Dated OIS – Pre-RBA Vs. Post-RBA

Source: Bloomberg / MNI - Market News

RBA: RBA On Hold, Waiting And Watching

The RBA left rates at 4.35%, as expected, at its last meeting for 2023. There was some shuffling of the statement but the content was little changed. It reiterated why rates were increased in November but then said that given “limited information received on the domestic economy”, there was “time to assess the impact” of previous tightening. The final guidance paragraph was unchanged and thus the central bank retained its tightening bias.

- There will be a lot more information before the February 6 meeting, which remains “live” for the Board to judge if inflation is slowing fast enough, including the domestic components. There will be the usual monthly releases but also Q4 CPI data on January 31. The meeting will also include updated staff forecasts. It reminded us that it remains “resolute” in returning inflation to target in a “reasonable timeframe”.

- The RBA acknowledged that the monthly CPI for October did not include “much more information on services inflation”, an area of concern given its persistence and the experience overseas. It notes though that the data “suggested that inflation is continuing to moderate”.

- The tight but easing labour market was repeated but the central bank doesn’t expect wages to “increase much further”. It reiterated though that they are consistent with the inflation target as long as “productivity growth picks up”. We will get the Q3 reading on this in Wednesday’s national accounts.

- See December statement here.

AUSSIE BONDS: Richer After RBA Policy Decision, RBA Noted Monthly CPI Suggests CPI Moderating

ACGBs (YM +4.0 & XM +4.5) sit 5-6bps richer after the RBA Policy Decision. As widely expected, the cash rate was left unchanged at 4.35%, following last month’s increase. In the statement, the RBA noted that:

- “While the economy has been experiencing a period of below-trend growth”, inflation and housing prices have exceeded projections.

- The Board believed “the risk of prolonged high inflation has risen, justifying the earlier rate hike”.

- Nevertheless, the RBA noted that “the monthly CPI indicator for October suggested that inflation is continuing to moderate”.

- While the impact of recent rate increases is ongoing, uncertainties persist, including global economic trends, the Chinese economic outlook, and domestic factors affecting household consumption.

- The Board emphasised its commitment to returning inflation to target. “Whether further tightening of monetary policy is required to ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks.”

- Cash ACGBs are 4-6bps richer following the decision, with the 3/10 curve slightly steeper and the AU-US 10-year yield differential 5bps tighter at +15bps.

- The swaps curve is 4-6bps richer after the decision, with rates 3-4bps lower on the day.

- The bills strip is now richer on the day, with pricing +2 to +5. Late whites/early reds leading.

- RBA-dated OIS pricing is 2-8bps softer across meetings, with Sep’24 leading.

AUSTRALIAN DATA: Q3 Trade To Weigh On GDP As Current Account In Deficit

The Q3 current account posted a deficit of $0.2bn compared to a surplus of $3.2bn that was forecast. This sharp narrowing from the $7.8bn surplus in Q2 was driven by the impact of lower commodity prices on the trade balance. The terms of trade deteriorated 2.6%. The net export share of GDP was also worse than expected at -0.6% after +0.8% in Q2.

- The trade balance narrowed $8bn to $22.8bn with both goods and services narrowing. Exports fell 2.1% q/q and -4.8% y/y and imports rose 3.3% and +0.1%, due to higher fuel prices and capex goods. Goods exports fell 3.1% q/q to be down 11% y/y due to key mining goods (especially coal) but services rose 2.7% q/q and 41.7% y/y as overseas student numbers reached a new record high.

- The ABS reports that prices of goods exports fell 1.9% q/q and -13.3% y/y, the fifth straight quarterly drop, due to coal and agricultural products.

- A slightly narrowed primary income deficit also contributed to the shift in the current account. Lower dividends from ASX listed mining companies weighed on the total.

Source: MNI - Market News/ABS

Australia terms of trade

Source: MNI - Market News/ABS

AUSTRALIAN DATA: PMI Points To Slowing Growth, Costs Still Being Passed On

The Judo Bank November final services PMI was revised down to 46 from the 46.3 preliminary estimate and 47.9 in October. This left the composite at 46.2 down from 47.6 the previous month. The Q3 average is consistent with another 0.4% q/q GDP read but the Q4 average to date is signalling that the final quarter may be softer than this. The PMIs are pointing to shrinking activity at the worst rate since the pandemic-affected Q3 2021.

- Higher wage, transport and energy costs pushed the input price measure up again in November for the third consecutive month and increased the gap with the historical average. Rising costs and the demand outlook weighed on business confidence.

- The November RBA minutes noted that businesses have the pricing power to be able to pass on higher costs to customers and Judo Bank reported that this continued but at a “quicker pace” than last month. This is likely to keep the central bank alert to upside inflation risks, although it is widely expected to leave rates on hold in December.

- Services demand for labour picked up in November despite lower new business but additional staff helped to reduce backlogs. Employment growth has been positive for over 2 years and is putting upward pressure on wages.

- The weakness in activity was driven by higher rates and deteriorating economic conditions weighing on domestic and foreign demand, according to Judo Bank.

- See Judo Bank note here.

Source: MNI - Market News/Refinitiv/Bloomberg

NZGBS: Subdued Session But Closed On A Positive Note

NZGBs closed on a strong note, with the benchmarks flat to 2bps richer on the day. The 2/10 curve finished flatter. The session was however subdued, with ranges narrow, after today’s domestic newsflow failed to provide a market-moving event.

- In addition to the previously outlined softer-than-expected 3Q Construction Work Done, the NZ Treasury published financial statements for the three months ended Oct. 31. These showed an operating deficit of NZ$3.85bn. The deficit was NZ$91m wider than projected in the pre-election fiscal update. (See Bloomberg link)

- Also potentially keeping local participants on the sidelines was the fact that the RBA Policy Decision coincided with the local market closing. The post-decision rally in ACGBs will therefore be reflected at tomorrow’s local market open.

- The swaps curve twist-flattened, with rates 2bps lower to 3bps higher.

- RBNZ dated OIS pricing is little changed.

- Tomorrow, the local calendar is empty.

- Later today, the US calendar sees ISM Services and JOLTS Job Openings.

EQUITIES: Regional Markets Lower, No Let Up For China Related Equity Weakness

Regional equities are mostly lower in Tuesday Asia Pac trade. Weakness in China/HK markets remains a focus point. Only Indian markets are tracking higher at this stage. Weakness follows a negative US lead from Monday's session, after a recovery in US yields. US equity futures are weaker in the first part of trade today, Eminis last 4567 (-0.20%), while Nasdaq futures are down 0.24%. A tick down in nominal US yields in Tuesday trade hasn't aided sentiment much.

- At the break, the HSI is off 1.76%, the index near 16354, which is fresh lows back to Nov last year. The HSTECH index is off by slightly more, down 2% at this stage.

- The better Caixin services PMI print in China has done little to improve sentiment. The CSI 300 index is off 0.80% at the break, with the real estate sub index down a further 1.62%, tracking lower for the 8th straight session.

- WuXi Biologics weak guidance has continued a run of generally softer earnings outcomes, which has weighed on broader sentiment, amid concerns of a still tepid China economic recovery.

- Comments from the regulator after yesterday's close stated that it will ensure the stable operation of capital markets.

- Other NEA markets are lower, the Nikkei 225 off over 1%, South Korea's Kospi -0.35%, the Taiex -0.70%, following some tech equity underperformance on Monday.

- SEA markets are weaker, although losses are under 0.50% at this stage for most markets.

- India remains an outperformer, with the Nifty +0.40% in early Tuesday trade.

FOREX: AUD Pressured After RBA Holds Cash Rate Steady

The Aussie is the weakest performer in the G-10 space at the margins. AUD/USD was pressured in early trade as regional equities ticked lower before extending losses as the RBA held rates steady and noted that inflation is continuing to moderate.

- AUD/USD is down ~0.6% and has breached the $0.66 handle to last print at $0.6580/85. Support is at the 20-Day EMA ($0.6539).

- Kiwi has been pressured on spillover from the weakness in the AUD however losses have been pared and NZD/USD is down ~0.2%. AUD/NZD is pressured and sits a touch above the $1.07 handle.

- Yen is firmer but only marginally so, USD/JPY has observed a ¥147.00/40 range for the most part with little follow through on moves. Support comes in at ¥146.23, the low from Dec 4. Resistance is at ¥148.51, high from Nov 30.

- Elsewhere in G-10 moves have been muted, CAD is a touch softer but well within recent ranges.

- Cross asset wise; US Tsys are little changed as is BBDXY. US Equity futures are marginally lower, and the Hang Seng is down ~1.8%.

OIL: Crude Steadies, Putin To Travel To Saudi Arabia

Oil prices have been trading in a narrow range during the APAC session holding onto the losses from the previous three days. WTI is flat at $73.07/bbl, close to the intraday low and off the high of $73.45. Brent is hovering around $78. The USD index is flat.

- Comments from the Saudi energy minister that cuts can easily be extended beyond Q1 2024 seem to have provided a floor to the market. Markets have questioned the compliance with the new quotas given the internal divisions in the lead up to the announcement. It is also focussed on rising non-OPEC supply, especially in the US.

- Russian President Putin is apparently scheduled to travel to the UAE and Saudi Arabia this week, according to Bloomberg.

- Futures contracts are in a bearish pattern signalling a looser market.

- Later US API inventory data is released and also US services PMI/ISM for November print as well as October JOLTS job openings. There are also European PMIs.

GOLD: Slightly Higher Today After A Spike Reversal From An All-Time High Yesterday

Gold is 0.4% higher in the Asia-Pac session, after closing -2.1% at $2029.42 on Monday following a sharp pullback from an all-time high of $2135.4. The decline came alongside USD strength and higher US Treasury yields.

- The jump to an all-time high was triggered by comments from Fed Chair Powell on Friday that traders interpreted as signalling a pivot to rate cuts was nearing. However, those bets were deemed overdone, with gold falling as US Treasury yields and the dollar rose.

- US Treasuries finished with yields 2-10bps higher and the curve flatter. The markets now await a slew of US labour market data this week, including Friday’s Non-Farm Payrolls.

- The pullback has already breached support at $2052.03 (Nov 29 high) to open $2001.5 (20-day EMA), according to MNI’s technicals team.

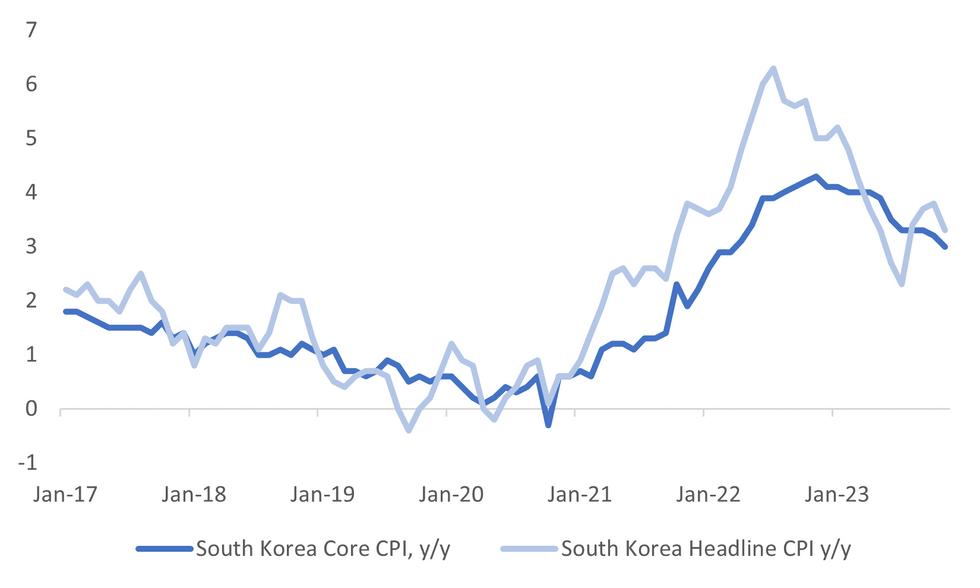

SOUTH KOREA: Core CPI Trend Continues To Moderate

South Korea Nov CPI was a little weaker than expected. The m/m headline was -0.6%, versus -0.3% forecast and 0.3% prior. This left the y/y headline at 3.3% (forecast 3.5% prior 3.8%). Core inflation, ex food and energy, was also sub estimates, printing 3.0%y/y (3.1% forecast and 3.2% prior).

- The m/m drag was driven by a 2.6% drop in food prices. Housing/utilities, furnishings, transport and recreation/culture also recorded m/m drops. Clothing and alcohol/tobacco were the main positives.

- In y/y terms, 5 out of 12 sub indices saw firmer y/y momentum, while the rest were down or unchanged on the Oct outcome. This fits with a slightly softer core y/y backdrop.

- The data is likely to give the authorities/BoK some comfort that the recent spike up in the headline y/y CPI is unlikely to be the start of a sharply higher inflation backdrop.

- Other data released showed Q3 GDP revisions unchanged from the original estimate (0.6% q/q and 1.4% y/y).

Fig 1: South Korea CPI Trends

Source: MNI - Market News/Bloomberg

PHILIPPINES DATA: Nov CPI Weaker Than Expected, BSP Likely On Hold Next Week

Philippines Nov CPI has printed weaker than expected. We came in at 4.1% y/y, versus 4.3% forecast and 4.9% prior. The m/m outcome was +0.2% (+0.4% forecast and -0.2% prior).

- This outcome was also towards the bottom end of the BSP's projected range (4.0% to 4.8% y/y). Core CPI stepped down to 4.7% y/y from 5.3% prior. This is back to mid 2022 levels for the core print.

- The detail showed slower m/m momentum across most sub-indices except for food. In y/y terms not a single category saw accelerating y/y momentum.

- Transport is only category in negative y/y terms (-0.8%).

- This should keep the BSP happy from an inflation trend standpoint. The next policy meeting is on Dec 14 (next Thursday), with no change likely. The current policy rate is 6.50%.

ASIA FX: Most USD/Asia Pairs Higher, CNH Outperforms

USD/Asia pairs are mostly higher, in line with a recovery in the USD backdrop and weaker regional equity sentiment. CNH has outperformed (last under 7.1500), with RTRS reporting state bank support for the onshore yuan. The better Caixin services PMI didn't shift sentiment. KRW and IDR have underperformed. Looking to tomorrow, we just have Taiwan CPI in a fairly light data day for the region.

- USD/CNH is off session highs, last under 7.1500, despite a weaker equity backdrop. The CSI 300 continues to make fresh lows. The better than expected Caixin services PMI only benefited FX sentiment briefly. Reuters headlines crossed indicating that state banks are selling USD/CNY onshore (via swaps), with the aim of encouraging exporters to convert earnings proceeds into the yuan before year end.

- 1 month USD/KRW has mostly been on the front foot in Tuesday Asia Pac dealings. We were last near 1311/12, above Monday session highs. Broader risk aversion has aided the USD, with regional equities underperforming. The Kospi is off 0.70%. Earlier we had slightly weaker than expected CPI for Nov, but the central bank still sounded cautious on the outlook.

- USD/IDR sits back near 15495 in latest dealings. This is off session highs (15517) but is still nearly 0.25% weaker in IDR terms versus Monday closing levels. After the THB and KRW, IDR is the weakest performer in spot terms within the Asia Pac region. We remain within recent ranges for the pair, with recent dips sub 15400 not sustained. On the topside the 20 and 50-day EMAs are in the 15540-60 range. Note the 100-day EMA is back at 15463.• A weaker IDR is in line with a firmer US yield backdrop. The US real 10yr yield climbing back to 2.07% on Monday against recent lows of 2.0% from the end of last week.

- The Ringgit has softened a touch in early trade this morning as onshore participants digested Monday's rise in US Tsy Yields, losses have been marginally pared and we do remain well within recent ranges. USD/MYR sits at 4.6640/60, ~0.2% higher today. A 4.63/70 range has persisted for the most part since early November.

- The Rupee has opened dealing a touch below yesterday’s closing levels however ranges are narrow. Onshore participants are digesting yesterday's uptick in US Tsy Yields as 2024 rate cut expectations were wound back. USD/INR prints at 83.36/38. On the wires today we had November S&P Global Services and Composite PMIs, Services PMI fell to 56.9 from 58.4 and Compostite PMI fell from 58.4 to 57.4.

- The SGD NEER (per Goldman Sachs estimates) is little changed this morning, we remain a touch off recent cycle highs and well within recent ranges. The measure sits ~0.3% below the top of the band. USD/SGD is holding below the $1.34 handle, the pair firmed ~0.3% yesterday as US Tsy Yields ticked higher. Participants wound back 2024 rate cut expectations which supported the USD. In early dealing on Tuesday we sit at $1.3380/85. In November S&P Global Whole Economy PMI rose to 55.8 from 53.7. This was the highest print since November 2022 and marks the ninth consecutive month of expansion. Retail Sales fell 0.1% Y/Y in October, a rise of 0.2% had been expected.

- PHP has outperformed today, the pair back near 55.34, versus earlier highs of 55.43. Nov CPI data was weaker than expected, which should see the BSP remain on hold next week, although BSP still sees upside inflation risks.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 05/12/2023 | 0745/0845 | * |  | FR | Industrial Production |

| 05/12/2023 | 0800/0900 | ** |  | ES | Industrial Production |

| 05/12/2023 | 0815/0915 | ** | | ES | S&P Global Services PMI (f) |

| 05/12/2023 | 0845/0945 | ** |  | IT | S&P Global Services PMI (f) |

| 05/12/2023 | 0850/0950 | ** | | FR | IHS Markit Services PMI (f) |

| 05/12/2023 | 0855/0955 | ** |  | DE | IHS Markit Services PMI (f) |

| 05/12/2023 | 0900/1000 | ** |  | EU | IHS Markit Services PMI (f) |

| 05/12/2023 | 0900/1000 | ** | | EU | ECB Consumer Expectations Survey |

| 05/12/2023 | 0930/0930 | ** |  | UK | S&P Global Services PMI (Final) |

| 05/12/2023 | 1000/1100 | ** | | EU | PPI |

| 05/12/2023 | 1000/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 05/12/2023 | 1355/0855 | ** |  | US | Redbook Retail Sales Index |

| 05/12/2023 | 1445/0945 | *** | | US | IHS Markit Services Index (final) |

| 05/12/2023 | 1500/1000 | ** | | US | IBD/TIPP Optimism Index |

| 05/12/2023 | 1500/1000 | *** | | US | ISM Non-Manufacturing Index |

| 05/12/2023 | 1500/1000 | *** | | US | JOLTS jobs opening level |

| 05/12/2023 | 1500/1000 | *** | | US | JOLTS quits Rate |

| 05/12/2023 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.