Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Ahead of the BoJ tomorrow, our analysis aligns with the prevailing consensus, which foresees the BOJ maintaining its existing policies in the upcoming announcement. Regarding the BOJ's YCC policy, most market participants do not foresee any changes this week, although many hesitate to completely rule out the possibility.

- Elsewhere, risk appetite has had a modestly firmer start to the week. Oil is lower, as we didn't see a dramatic escalation in Mideast tensions over the weekend, although Israel's ground offensive into Gaza will be watched closely. US equity futures are higher, while higher beta FX (AUD and NZD) has outperformed in the G10 space. US cash tsys sit 3-4bps cheaper across the major benchmarks, the belly is leading the cheaps.

- Later US October Dallas Fed manufacturing, euro area October confidence, Q3 German GDP and September CPI are released. Also ECB’s de Guindos speaks.

MARKETS

BOJ: MNI BOJ Preview - October: BOJ To Maintain Its Existing Policies, YCC The Focus

EXECUTIVE SUMMARY

- In the most recent Monetary Policy Meeting (MPM) held on September 21-22, the BOJ made the expected decision to maintain its current policy stance. This included the continuation of its more flexible framework for yield curve control (YCC) introduced in July, retention of the 1.0% yield for its fixed-rate purchase operations, and the continuation of its large-scale bond purchases designed to shape the yield curve as needed.

- As for the decision expected this week, our analysis aligns with the prevailing consensus, which foresees the BOJ maintaining its existing policies in the upcoming announcement. This would involve keeping the short-term interest rate at -0.1%.

- Regarding the BOJ's YCC policy, most market participants do not foresee any changes this week, although many hesitate to completely rule out the possibility.

- For proponents of a YCC adjustment, the precise nature of such an adjustment remains uncertain. Some posit that the YCC ceiling will be raised from its current 1.0% to 1.5%. Others suggest the BOJ might opt to increase its 10-year JGB target from the current level of around 0% to 0.25% or even 0.5%.

- While no policy changes are anticipated at this week's meeting, swap market indicators now suggest stronger expectations for the near-term elimination of subzero rates by March than for a further widening of the band around the BOJ's 10-year yield target.

- Full preview here:

US TSYS: Narrow Ranges In Asia

TYZ3 deals at 106-07, -0-06+, a 0-08+ range has been observed on volume of ~80k.

- Cash tsys sit 3-4bps cheaper across the major benchmarks, the belly is leading the cheaps.

- Tsys ticked lower in early trade alongside Oil in early trade as demand for safe haven assets after Israel's military action in Gaza was moving more cautiously than expected.

- The move lower didn't follow through and Tsys ticked away from session lows dealing in narrow ranges for the remainder of the Asian session.

- On the wires today we have the Dallas Fed Mfg Activity Index. Further out the latest monetary policy decision from the Fed provides the highlight of this week's docket.

JGBS: Poor 2Y Supply Weighs Ahead Of BOJ Policy Decision Tomorrow

JGB futures are weaker and near session lows, -11 compared to the settlement levels.

- There hasn’t been much in the way of domestic drivers to flag, with the data calendar empty ahead of the BOJ policy decision tomorrow.

- As for the decision expected tomorrow, our analysis aligns with the prevailing consensus, which foresees the BOJ maintaining its existing policies in the upcoming announcement.

- Regarding the BOJ's YCC policy, most market participants do not foresee any changes this week, although many hesitate to completely rule out the possibility. See the MNI BOJ Preview here.

- Cash JGBs are at or near Tokyo session cheaps across the curve following poor demand metrics observed at today’s 2-year supply. It was notable that today’s cover ratio was the lowest for a 2-year auction since 2010. Yields are 0.3bp lower (40-year) to 1.5bps higher (20-year). The benchmark 10-year yield is 1.1bps higher at 0.892% versus the cycle high of 0.897% set today.

- The 2-year is 1.0bp higher at 0.103% versus Friday’s close of 0.093%.

- Swap rates are slightly higher across maturities. Swap spreads are mixed across the curve.

- Tomorrow, the local calendar sees Jobless Rate, Retail Sales, Dept. Store and Supermarket Sales and Industrial Production data, ahead of the BOJ Policy Decision.

AUSSIE BONDS: At Session Cheaps After Retail Sales Beat, 70% Chance Of A Nov Hike

ACGBs (YM -5.0 & XM -7.5) are sitting weaker, at or near the Sydney session’s worst levels, after Retail Sales for September printed much stronger than expected. That said, the strength was due to a number of special factors (e.g. warmer spring boosting clothing) so is unlikely to be repeated in October. The Q3 average rose a 3-month annualised rate of 3.4% up from 1.7% in Q2. Sales were positive in every month in Q3 signalling resilience in consumption.

- Cash ACGBs are 5-7bps cheaper on the day, with the AU-US 10-year yield differential 6bps higher at +1bp. The last time the differential was in positive territory was in mid-August.

- Swap rates are 5-7bps higher on the day, with EFPs little changed.

- The bills strip is cheaper, with pricing -3 to -8, late whites/early reds the weakest.

- RBA-dated OIS pricing is 1-8bps firmer across meetings, with late’24 leading. The market is attaching a 71% chance of a 25bp hike from the RBA at next week’s policy meeting. Terminal rate expectations have jumped to 4.51% (+44bps), the highest level since mid-July.

- Tomorrow, the local calendar sees Private Sector Credit, CoreLogic House Prices and Judo Bank PMIs data.

AUSTRALIAN DATA: Special Factors Boost Sales, Q3 Strengthens Though

Retail sales grew a stronger-than-expected 0.9% m/m in September after 0.3% to be up 2% y/y. The strength was due to a number of special factors and so is unlikely to be repeated in October. The Q3 average rose a 3-month annualised rate of 3.4% up from 1.7% in Q2. Sales were positive in every month in Q3 signalling resilience in consumption. Q3 sales volume data are released on Friday but with nominal sales up 0.8% q/q another contraction in volumes is likely.

- The ABS said that September’s strength was due to a number of factors. It cited the “warmer-than-usual start to spring” boosted department store, household goods and clothing sales. The new iPhone also increased sales as well due to the start of Queensland’s Climate Smart Energy Savers Rebate to upgrade appliances. Thus household goods retailing rose 1.5% m/m but was still down 4% y/y.

- All of the major components of retail sales posted increases in September. Food retailing rose 1% m/m and 3.5% y/y but restaurants were flat although still the strongest category in annual terms at 6.1% y/y, but it appears to be slowing. Department stores rose 1.7% m/m and 1.3% y/y. Other retailing rose 1.3% m/m and 1.6% y/y due to the start of 60-day prescriptions.

Source: MNI - Market News/ABS

NZGBS: Closed Slightly Weaker, Focus Abroad

NZGBs closed 1-3bps cheaper, at session worst levels, with the 2/10 curve steeper. With the local calendar empty today, local participants have been guided from abroad ahead of this week's policy meetings for the BOJ (tomorrow), FOMC (Wednesday) and the BOE (Thursday). Although no substantial changes in policy are anticipated at these meetings, their potential to influence the market still looms large. Notably, there is a level of uncertainty surrounding the possibility of the BOJ making further adjustments to its yield curve control.

- Cash US tsys are 3-4bps cheaper so far in the Asia-Pac session. There has been little by way of newsflow today.

- Swap rates closed with a twist-steepening, rates 1bp lower to 2bps higher.

- RBNZ dated OIS pricing closed little changed across meetings, with terminal OCR expectations at 5.61%.

- Tomorrow, the local calendar sees Building Permits and ANZ Business Confidence.

- The US calendar sees the US Treasury's quarterly borrowing estimates later today. Wednesday sees the FOMC policy announcement along with ADP Private Employment data, ahead of Friday’s Non-Farm payrolls.

FOREX: Antipodeans Firm In Asia

The Antipodeans have firmed in the Asian session today, a strong Retail Sales print in Australia and firmer US Equity Futures are aiding the bid.

- AUD/USD is up ~0.3% at $0.6355/60, Fridays high remains intact for now. September Retail Sales printed at 0.9% M/M vs 0.3% expected. Technically the trend remains bearish, support comes in at $0.6270 Oct 26 low. Resistance is at $0.6411 the 50-day EMA.

- Kiwi is ~0.2% firmer, NZD/USD last prints at $0.6820/25. AUD/NZD is consolidating in a narrow range above the $1.09 handle.

- Yen is marginally firmer as USD/JPY consolidates below the ¥150 handle. Technically bulls remain in the drivers seat, resistance is at ¥151.09 2.764 projection of the Jul 14-21-28 price swing. Support comes in at the 20-Day EMA (¥149.46).

- Elsewhere in G-10 ranges have been narrow with little follow through on moves.

- Cross asset wise, WTI is down ~1.4% and e-minis are ~0.4% firmer. US Tsy Yields are ~3bps higher across the curve.

- Regional German CPI and National GDP provide the highlight in Europe today.

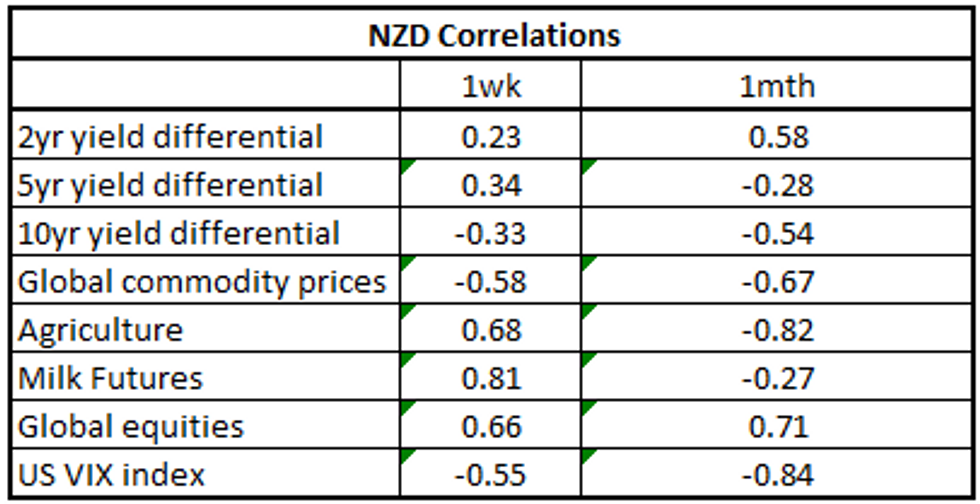

NZD: Milk Futures, Agriculture & Global Equities Main Drivers Last Week

NZD/USD correlations with Milk Futures, Agriculture and Global Equities have strengthened over the past week, standing out as a key macro driver in recent dealings. The table below presents levels of correlations between NZD and key macro drivers (note the yield differential reflects swap rates).

- NZD/USD fell ~0.3% yesterday in a volatile week of trading observing a $0.5770/5870 range for the most part. The Kiwi's main drivers look to be associated with Milk Futures, Global Equities and Agriculture.

- The pair looked through a rise in Global Commodity Prices last week and also in the longer time frame.

- Over the longer time frame Global Equities and 2-Year Yield Differentials continue to be the dominant macro drivers in the pair.

Fig 1: NZD/USD Correlation with Global Macro Drivers:

Source: MNI/Bloomberg

EQUITIES: Mixed Start To The Week For Asia Pac, US Futures Higher

Regional Asia Pac equities have started Monday trade in a mixed fashion. Japan markets and parts of SEA are softer, while China and South Korean markets are trading more resiliently. US equity futures have started the week higher. Eminis last near 4152, +0.33%, while Nasdaq futures are outperforming modestly, last up 0.51%.

- Oil prices are lower, with some reports (BBG) suggesting the Israel ground invasion into Gaza was not as strong as feared. The move lower in oil has aided risk appetite more broadly, including curbing USD sentiment.

- In China markets, the CSI 300 is up a further 0.67%, tracking above 3586 in index terms. The ChiNext is also up strongly (+2%). A key financial forum kicks off today in China, where LGFV's and property market risks will be discussed. China's number 2 military head also stated that the country will develop military ties with the US (RTRS), which may be signs of a further thawing in tensions with the US. Hong Kong markets are down, but away from session lows (HSI last -0.28%).

- Japan markets are weaker, off -0.85% for the Topix as tomorrow's BoJ meeting comes into view. No major policy changes are expected, although it is likely to be a close call.

- South Korea's Kospi is higher, +0.55%, in line with higher beta markets outperforming. The Taiex is +0.20%.

- In SEA, Indonesia and Malaysian shares are lower. Thailand and Singapore are modestly higher.

OIL: Crude Lower But Watching And Waiting

Oil prices are down over a percent during APAC trading following Friday’s rally. Stronger-than-expected US data at the end of last week ahead of the November 1 Fed meeting, and the restrained start to the ground offensive into Gaza have meant that there has been payback for the sharp rise in prices. The USD index is flat.

- WTI is down 1.5% to $84.24/bbl and off the intraday high of $85.30. Brent fell 1.2% to $88.10 after a low of $87.51. It approached $89 earlier but reached a high of $88.94.

- Bloomberg is reporting that Israel is taking the offensive into Gaza one day at a time rather than making one large incursion. Markets are watching closely for signs that the conflict is spreading outside of Israel/Gaza.

- Physical indicators are showing the market is easing. And net futures positions as reported by CFTC fell almost 6k contracts to 300.8k in the latest week.

- Later US October Dallas Fed manufacturing, euro area October confidence, Q3 German GDP and September CPI are released. Also ECB’s de Guindos speaks. The Fed meeting on Wednesday and payrolls on Friday are the key events this week for oil markets.

GOLD: Holding Above $2000 For The First Time Since May

Gold is 0.2% lower in the Asia-Pac session, after closing 1.1% higher at $2006.37 on Friday as Israel expanded its military operations in Gaza. Tel Aviv sent troops and tanks into the northern Gaza Strip in what it called the second and longer phase of its war against Hamas.

- Friday’s move marked the first time since May that bullion had traded above $2000.

- The yellow metal now sits more than 9% higher, fueled by haven demand, since the Hamas attack on Israel.

- The Middle East conflict has taken over the path of US interest rates as the main driver of gold. Nevertheless, the market will closely watch this week’s FOMC policy decision on Wednesday.

- According to MNI’s technicals team, Friday’s move cleared resistance at $2003.4 after which lies $2022.2 (May 15 high).

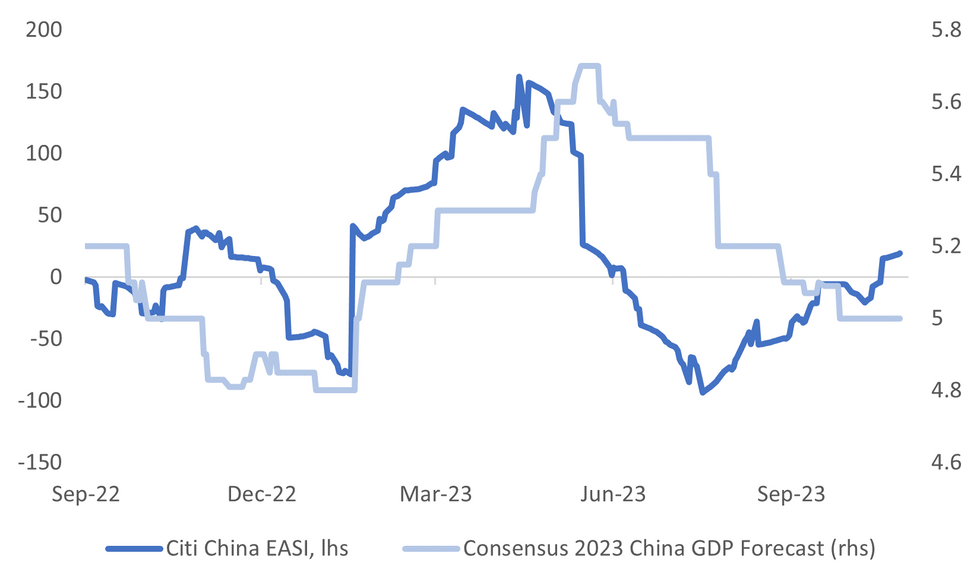

CHINA DATA: Official PMIs On Tap Tomorrow - Manufacturing Expected To Be Steady, Services Higher

A reminder that the official October PMIs for China print tomorrow. The market looks a steady manufacturing trend, projected at 50.2, prior 50.2, with a forecast range of 49.9 to 50.6. On the non-manufacturing or services side, the market is projecting a 52.0 outcome versus 51.7 prior (forecast range is 50.5 to 52.2).

- Recall earlier this month the China Emerging Industries PMI rose further in October to 57.8 from 54.0. This bodes well for the official manufacturing index, although the beta between the two series has been fairly low in recent months.

- More broadly, China data surprises have been turning more positive. The Citi China EASI is at multi month highs (see the chart below), which is driving some sell-side names to nudge their 2023 growth forecasts higher (although the aggregate consensus is unchanged at this stage).

- An additional positive for the growth backdrop is increased government bond issuance in Q4.

- If we see any upside surprises in the PMIs tomorrow it should drive further confidence in the near term growth outlook, although China related assets in terms of FX and local equities are only modestly above recent lows.

Fig 1: Citi China EASI Versus 2023 China GDP Growth Expectations

Source: Citi/MNI - Market News/Bloomberg

ASIA FX: Most USD/Asia Pairs Lower As Risk Appetite Starts The Week Tentatively Firmer

Most USD/Asia pairs are lower, with THB and MYR the standouts. Gains are more modest elsewhere, as overall sentiment remains cautious given Mideast risks and the Fed later this week. USD/CNH has drifted lower, but remains within recent ranges. Tomorrow, we have official PMIs for China, South Korean IP, Taiwan Q3 GDP and Thailand trade figures.

- USD/CNH has remained comfortably within recent ranges during today's session. We sit near 7.3280 currently, down slightly from opening levels near 7.3300. An earlier dip sub 7.3250 saw no follow through. Onshore equities are higher, albeit away from session bests. Focus is on the Financial Work Conference which kicks off today, with LGFVs and property the headline discussion points. Tomorrow, we have official PMI prints for October. Tentative signs of some improvement in US-China relations will be the other watch point.

- 1 month USD/KRW sits below opening levels (near 1354), last tracking close to 1351. An earlier dip sub 1350 was supported though. The won is benefiting from some outperformance by higher beta FX, as US equity futures are higher and oil prices lower to start the week. This reverses some of the trends seen at the end of last week. This keeps us firmly within recent ranges for USD/KRW. Local South Korean equities are outperforming modestly within EM Asia markets, the Kospi last +0.40% and holding above 2300. The index is only modestly above recent lows, but the correlation with the won has been strong with USD/KRW in recent months, -77% in levels terms for the past 3 months.

- The Rupee has opened dealing little changed from Fridays closing levels at 83.2550/2650 in a muted start to the weeks trade. On Friday USD/INR firmed above the 20-Day EMA, ranges remain narrow with little follow through on moves. Tomorrow the September Fiscal Deficit is released, Eight Infrastructure Survey also crosses. On Wednesday we have S&P Global Mfg PMI, and the Services and Composite components cross on Friday.

- Baht is the best performing Asian currency in Monday trade to date. USD/THB is down around 0.55%, last near 36.03 for spot (earlier lows were at 35.99). Some of this may reflect catch up to USD trends, although broader dollar indices aren't too different from where Thailand markets closed on Friday. In terms of technicals, we are very close to the 50-day EMA (36.01), which we traded meaningfully below since August of this year. The 100-day sits further south at 35.58, while the 20-day is at 36.32. Bond inflows were more positive at +$303mn last week, with signs the government is potentially tempering its fiscal support aiding sentiment in this space at the margin. Over the weekend, BoT Governor Sethaput Suthiwartnarueput stated the central bank will assess risks from the Middle East but the current stance of policy is appropriate (BBG).

- The Ringgit has opened dealing firmer on Monday, USD/MYR is ~0.4% lower. According to RBC, link here, authorities may have stepped in to reign in the currency’s weakness. The pair sits at 4.7540/65, the lowest level in ~2 weeks. S&P Global Mfg PMI for October is due on Wednesday. On Thursday the latest monetary policy decision from the BNM rounds off the week.

- The SGD NEER (per Goldman Sachs estimates) sits little changed this morning and remains well within recent ranges. The measure is ~0.5% below the top of the band. USD/SGD sits a touch below the $1.37 handle on Monday, ranges have been narrow in recent trade as the pair see-saws around $1.37. The MAS Chief Menon noted this morning that Singapore's monetary policy remains "appropriately tight" (BBG). There is a busy local docket this week. On the wires tomorrow we have September Money Supply, on Thursday the Purchasing Managers Index for October is due. S&P Global Mfg PMI for October and September Retail Sales round off the week on Friday.

- USD/IDR sits modestly off highs from the end of last week. Last near 15925, after getting to 15950 late in Friday trade. Earlier lows today were just under 15910, but had little follow through. This leaves us within recent ranges, as the market remains wary of intervention risks around 15960 and likely closer to 16000. This week we have CPI figures for October out on Wednesday. Little change is seen relative to September data in terms of these prints (core near 2%y/y, headline 2.6%).• Events outside Indonesia may dictate currency trends more forcefully, with markets watch Mideast developments closely. We ended last week with weaker sentiment, but the start of this week has had a more positive start to it in terms of US equity futures.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 30/10/2023 | 0630/0730 | *** |  | DE | North Rhine Westphalia CPI |

| 30/10/2023 | 0800/0900 | *** |  | ES | HICP (p) |

| 30/10/2023 | 0800/0900 | * |  | CH | KOF Economic Barometer |

| 30/10/2023 | 0900/1000 | *** | | DE | Bavaria CPI |

| 30/10/2023 | 0930/0930 | ** |  | UK | BOE M4 |

| 30/10/2023 | 0930/0930 | ** | | UK | BOE Lending to Individuals |

| 30/10/2023 | 0930/1030 | *** | | DE | Baden Wuerttemberg CPI |

| 30/10/2023 | 1000/1100 | ** |  | EU | EZ Economic Sentiment Indicator |

| 30/10/2023 | 1000/1100 | *** | | DE | Saxony CPI |

| 30/10/2023 | 1300/1400 | *** | | DE | HICP (p) |

| 30/10/2023 | 1300/1400 | | EU | ECB's De Guindos speech at Leadership forum | |

| 30/10/2023 | 1430/1030 | ** |  | US | Dallas Fed manufacturing survey |

| 30/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 30/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 30/10/2023 | 1930/1530 |  | CA | BOC's Macklem testifies at House committee. | |

| 31/10/2023 | 2330/0830 | * |  | JP | labor force survey |

| 31/10/2023 | 2350/0850 | ** | | JP | Industrial production |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.