Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

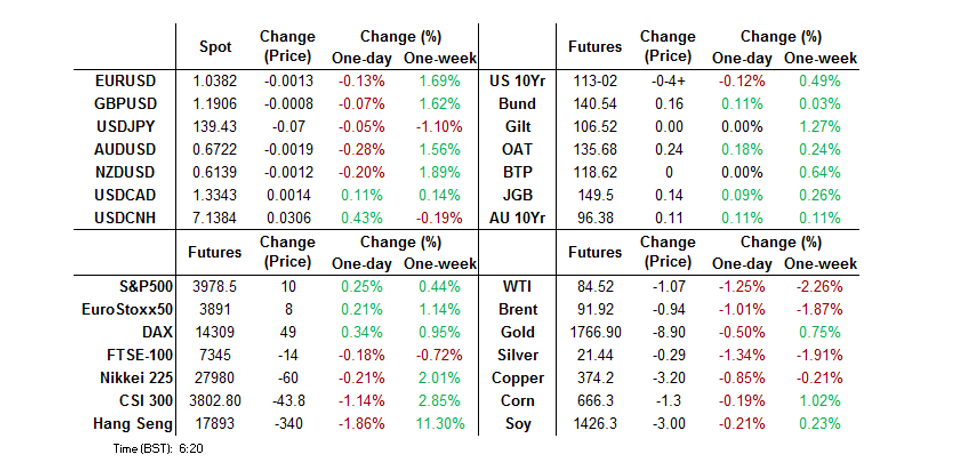

- Tsys have pulled away from session lows, which were facilitated by a combination of a block sale in FV futures (-3K), spill over from a bid in the broader USD, as well as pockets of screen selling in TY futures. A bid in the super long end of the JGB curve and some weakness in Chinese & HK equities may have resulted in some spill over demand for U.S. Tsys, allowing the space to stabilise. There was little in the way of Asia-Pac enthusiasm to extend on Wednesday’s bull flattening dynamic, with yesterday’s price action seeing the 2-/10-Year yield spread register the deepest levels of inversion witnessed during the current cycle, while 10-Year Tsy yields moved below the lower boundary of the Fed Funds target range.

- Higher U.S. Tsy yields & weakness in Chinese & HK equities generated greenback outperformance. The BBDXY index crept higher but the 1,280 level provided firm resistance.

- Data highlights today include U.S. jobless claims, housing starts, building permits & Philly Fed Survey, as well as final EZ CPI. Comments are due from Fed's Bullard, Bowman, Mester, Jefferson & Kashkari, BoE's Pill & Tenreyro, as well as ECB's Villeroy. There will also be plenty of interest in UK’s Autumn Fiscal Statement after the challenges surrounding that matter witnessed in recent weeks/months.

MNI UK Autumn Statement Preview

EXECUTIVE SUMMARY

- We look at some of the main measures that are expected to be announced (or have seen a lot of discussion in the media) in this week's Autumn Statement.

- We discuss the financial market and political implications of the statement.

- For markets, the focus is likely to be on the broader plan, rather than any specific policies - although if we get details of the replacement for the Energy Price Guarantee from April 2023 there will be huge interest in the details.

- For the full document see:Autumn_Statement_Nov2022.pdf

US TSYS: A Little Cheaper Overnight, Asia Not Willing To Extend The Bid

The major cash Tsy benchmarks run 1-2bp cheaper across the curve, with intermediates leading the weakness. TYZ2 sits -0-05 at 113-01+ into London hours, around the middle of its 0-10 Asia-Pac range, on volume of ~99K

- Tsys have pulled away from session lows, which were facilitated by a combination of a block sale in FV futures (-3K), spill over from a bid in the broader USD, as well as pockets of screen selling in TY futures.

- A bid in the super long end of the JGB curve and some weakness in Chinese & HK equities may have resulted in some spill over demand for U.S. Tsys, allowing the space to stabilise.

- There was little in the way of Asia-Pac enthusiasm to extend on Wednesday’s bull flattening dynamic, with yesterday’s price action seeing the 2-/10-Year yield spread register the deepest levels of inversion witnessed during the current cycle, while 10-Year Tsy yields moved below the lower boundary of the Fed Funds target range.

- On top of the previously covered flow we also saw some screen sales of the FVF3 107.75/108.50 call spread and a seller of FFF3 futures in the short-end.

- A deluge of Fedspeak headlines the NY docket on Thursday, with weekly jobless claims data, housing starts, building permits and regional Fed economic activity indicators also slated for release. Further afield, there will be plenty of interest in UK’s Autumn Fiscal Statement after the challenges surrounding that matter witnessed in recent weeks/months.

JGBS: Bull Flattening Dominates

The JGB curve has continued to flatten during the Tokyo afternoon, with a move away from session cheaps in U.S. Tsys and smooth enough digestion of the latest round of 20-Year JGB supply (crucially, the low price met wider dealer expectations, even with the remainder of the internal metrics presenting a more mixed picture) aiding the bid, after U.S. Tsy trade on Wednesday provided some early direction. The major JGB benchmarks are little changed to ~7bp richer across the curve, while JGB futures are +15 ahead of the bell, regaining some poise after initially ticking away from overnight highs.

- We have suggested that recent sessions have seen super-long demand from the domestic pension fund and life insurer cohort, given the lack of attractive offshore bond propositions noted at present (owing to elevated FX-hedging costs and ongoing market vol.).

- BoJ speak offered little tangible information for markets to trade off of, while Japanese Finance Minister Suzuki also went over old ground.

- Elsewhere, the latest BBG survey surrounding the BoJ questioned the analytical community on potential successors to BoJ Governor Kuroda when his current term ends in April ’23. It was no surprise to see BoJ veterans Masayoshi Amamiya & Hiroshi Nakaso at the top of the list, given their long-held status as front-runners in that race.

- Looking ahead, Friday’s local docket will be headlined by the latest round of national CPI data.

AUSSIE BONDS: Closing Around Early Sydney Levels After Two-Way Trade

Aussie bonds gravitated back towards early Sydney levels after the pre-data bid waned in the wake of a strong labour market report and as U.S. Tsys softened, although a recovery from Sydney cheaps was seen into the close as U.S. Tsys ticked away from session lows.

- YM finished +7.0, with XM +11.0, while cash ACGBS were 6-11bp richer across the curve, with the 10- to 20-Year zone outperforming.

- The labour market continues to perform strongly, while wage growth has accelerated in recent times. Still, we doubt that this week’s labour market and wage data will trigger a move back to 50bp hikes for the RBA, given the proximity to the recent downshift to 25bp steps and the Bank’s clear focus on the lagged impact of the already deployed tightening, as well as the risks (both domestic & global) that are swirling around the Australian economy.

- Bills finished 1-15bp richer, with RBA dated OIS printing just over 20bp of tightening for next month’s RBA meeting and a terminal cash rate of just under 3.80%, with the latter softening a touch early in Sydney dealing.

- Looking ahead, A$700mn of ACGB Nov-29 supply and the release of the weekly AOFM issuance slate headline the domestic docket on Friday.

AUSTRALIA: Strong Labour Data Across The Board, RBA Hikes To Continue

Australia’s labour market data for October came in significantly stronger than expected. The details are also strong and not only support consumption going forward but make a 25bp RBA hike in December highly likely. But it is unlikely to be enough to make it 50bp though, given that consistency is important to the RBA, their other concerns and the lagging nature of the labour market.

- The number of employed rose 32.2k, which was not only above the consensus 15k but at the upper end of expectations, and above the monthly average for 2022. The unemployment rate fell 0.1pp to 3.4% as the number of unemployed fell 21k (consensus 3.5%). The participation rate was stable from the downwardly revised September reading of 66.5%.

- The underutilisation rate fell 0.2pp to 9.3%, the lowest in 40 years. The underemployment rate fell 0.1pp to 5.9%, the lowest since the global financial crisis.

- Given the labour shortage, the trend of part-time jobs becoming full-time continued. Full-time employment rose 47.1k and is now 6.4% higher than a year ago, which is a new record high. While part-time fell 14.9k but is still up 4.8% y/y, it is now recording falling 3-month momentum. This trend towards working more was also reflected in the momentum in hours worked exceeding employment.

- There were a number of special factors impacting hours worked in both directions. 10% fewer people took annual leave in October than usual, but 30% more worked less due to sickness and recent floods also reduced hours worked.

Source: MNI - Market News/ABS

NZGBS: Off Best Levels, But Still Richer On The Day

NZGBs gave back some of their early gains as the major cash benchmarks finished the session 1-5bp richer vs. Wednesday’s closing levels, with the curve bull flattening. Swap spreads ran tighter, pointing to receiver side swap flow-based support for NZGBs.

- Local data failed to impact the space, with the PPi output metric softening in Q/Q terms, albeit running at still elevated levels when annualised.

- NZGBS found a base ahead of the local data, with the direction of travel for both U.S. Tsys and ACGBs (which saw a limited downtick in the wake of the latest labour market report) helping the space to nudge further away from best levels as the day wore on.

- RBNZ dated OIS is little changed on the day, with just under 65bp of tightening priced in for next week’s RBNZ decision, alongside a terminal OCR of ~5.05%.

- Friday’s domestic docket is empty.

FOREX: Safe-Haven FX In Demand, Cautious Risk Tone Dominates

The Asia-Pac session witnessed a flight to safety as Chinese tech shares dropped, while participants scrutinised the latest comments from U.S. central bankers/U.S. economic data for clues about Fed tightening outlook.

- The release of above-forecast retail sales data and signs of continued determination among Fed members to keep raising interest rates may have pushed U.S. Tsy yields higher in Asia hours, even as Fed Governor Waller said he feels "more comfortable" about slowing the pace of rate hikes.

- Higher U.S. Tsy yields generated greenback outperformance. The BBDXY index crept higher but the 1,280 level provided firm resistance.

- USD/JPY oscillated between gains and losses, holding a familiar range through the session. North Korea test-fired a ballistic missile in a reminder of the region's worrying geopolitical situation.

- A slightly softer commodity complex weighed on high-beta FX bloc, with the Antipodeans underperforming in the Asia-Pac timezone.

- The Aussie dollar showed a limited reaction to the domestic labour market report. Employment grew faster than forecast, which underpinned a surprise downtick in the unemployment rate, with participation steady versus its revised prior level.

- Data highlights today include U.S. jobless claims, housing starts, building permits & Philly Fed Survey, as well as final EZ CPI. Comments are due from Fed's Bullard, Bowman, Mester, Jefferson & Kashkari, BoE's Pill & Tenreyro, as well as ECB's Villeroy.

FX OPTIONS: Expiries for Nov17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0200(E978mln), $1.0300-05(E815mln), $1.0500(E590mln)

- USD/JPY: Y140.00-10($1.3bln)

- AUD/USD: $0.6300(A$1.4bln)

- USD/CAD: C$1.3300($1.0bln), C$1.3700($1.0bln)

- USD/CNY: Cny7.3000($2.0bln)

ASIA FX: Asia EM FX Broadly Weaker Amid Demand For Greenback

The greenback firmed across the board, which underpinned USD/Asia crosses, on the reassessment of Fed tightening outlook. December rate-hike pricing implied by meeting-dated OIS edged higher, while U.S. Tsys cheapened across the curve. The ADXY index extended Wednesday's rout, printing session lows at 98.38.

- CNH: Offshore yuan briefly strengthened after the PBOC set the USD/CNY mid-point 148 pips below the expected level. The resultant downtick in USD/CNH proved short-lived as greenback purchases gained traction.

- KRW: The South Korean won was the worst performer in the region, losing ~1.25% versus the U.S. dollar. Heightened geopolitical tensions may have facilitated won sales, with North Korea resuming its ballistic missile tests. FX markets opened one hour late due to the national college entrance exams in South Korea.

- IDR: The rupiah retreated amid softer commodity prices and ahead of today's monetary policy decision from Bank Indonesia. The central bank is expected to raise the 7-Day Reverse Repo Rate by 50bp, albeit some expect a 25bp hike.

- MYR: Spot USD/MYR advanced as palm oil futures most actively traded in Kuala Lumpur fell below the MYR4,000/MT level and their 50-DMA. Domestic front pages remained dominated by reports surrounding the upcoming general election; Malaysia will observe a public holiday tomorrow, ahead of Saturday's poll.

- PHP: Bangko Sentral ng Pilipinas effectively preannounced a 75bp rate hike, which is expected to take effect after the scheduled Monetary Board meeting today. The Philippine peso softened, but held a familiar range.

- THB: Baht losses were exacerbated by continued equity outflows. Spot USD/THB saw its RSI return from oversold territory, which is a bullish signal.

MNI Bank Indonesia Preview - November 2022: Another 50bp To Support IDR

EXECUTIVE SUMMARY

- Bank Indonesia (BI) meets on November 17 and is widely expected to hike rates another 50bp to 5.25%, bringing rates to their highest since September 2019.

- 8 of the 28 analysts surveyed by Bloomberg expect a lower 25bp move. The moderation in October headline CPI inflation and the slight appreciation of the USDIDR in recent days suggest that the risks to the 50bp forecast are skewed to the downside.

- Stabilising the IDR, bringing core inflation back to target, and ensuring financial stability in the context of a robust economy are again likely to be the focus of the November meeting. A 50bp move this month would still see the Indonesian-US rate differential narrow.

- For the full piece, see here.

MNI BSP Preview - November 2022: Keeping Up With Fed

EXECUTIVE SUMMARY

- Governor Medalla guided that the Bangko Sentral will be raising the key policy rate by 75bp come the end of this week's monetary policy review, in order to keep the interest-rate differential with the U.S. unchanged.

- Inflation continues to quicken amid higher food prices, with the local statistics authority warning that it may gather more pace in the coming months on the back of the recent typhoons.

- The Philippine peso has been the worst performer in emerging Asia this year, accentuating imported inflation. The onus is on the BSP to rescue the domestic currency, which comes under additional pressure from the Philippines' "twin deficit."

- For the full piece, see:MNI BSP Preview November 2022.pdf

GOLD: Softening In Asia

An uptick in U.S. Tsy yields and a firmer USD have weighed on bullion in Asia-Pac hours. This comes after a relatively contained, two-way Wednesday session, in which bullion failed to capitalise on the twist flattening observed on the broader U.S. Tsy curve.

- Spot deals ~$10/oz cheaper at $1,763/oz, with the technical picture little changed from what we outlined earlier in the week.

- The Fed pivot/pause debate (at least on the part of market participants, as opposed to via Fedspeak) and USD dynamics will continue to dominate for gold in the immediate term, with elevated sensitivity to inflation readings and indicators set to remain evident.

OIL: China Growth Concerns Weigh On Oil Prices

Oil prices are weaker again today with WTI down 1.4% to around $84.40 and Brent -1.1% to $91.80/bbl respectively, as the demand outlook became the focus once more and risk appetite deteriorated with most equity markets in the region down.

- Concerns regarding crude demand from China came to the forefront, as Covid cases continue to rise reducing the hope of any further near-term easing of restrictions.

- The spread between the two nearest Brent contracts continues to be in backwardation pointing to a tight market, but it has eased since the start of the month. (Bloomberg)

- Overnight the US EIA reported that there had been a drawdown in crude inventories of 5.4mn barrels, more than last week’s 3.9mn build and the largest weekly drop since August.

- Later numerous central bank officials speak including the Fed’s Bullard, Bowman, Mester, Jefferson and Kashkari. Any comments that move the USD are also likely to move oil prices.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/11/2022 | 0720/0220 |  | ID | Bank of Indonesia Rate Decision | |

| 17/11/2022 | 1000/1100 | ** |  | EU | Construction Production |

| 17/11/2022 | 1000/1100 | *** | | EU | HICP (f) |

| 17/11/2022 | 1230/0730 |  | US | Atlanta Fed's Raphael Bostic | |

| 17/11/2022 | 1230/1230 |  | UK | BOE Pill Speech at the Bristol Festival of Economics | |

| 17/11/2022 | - | | UK | Autumn Statement with New OBR forecasts / Updated DMO Remit | |

| 17/11/2022 | - |  | TH | APEC Leaders’ Summit | |

| 17/11/2022 | 1300/0800 | | US | St. Louis Fed's James Bullard | |

| 17/11/2022 | 1330/0830 | ** | | US | Jobless Claims |

| 17/11/2022 | 1330/0830 | *** | | US | Housing Starts |

| 17/11/2022 | 1330/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 17/11/2022 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 17/11/2022 | 1415/0915 | | US | Fed Governor Michelle Bowman | |

| 17/11/2022 | 1430/1430 | | UK | BOE Tenreyro Speech at Asociacion Argentina de Economia Politica | |

| 17/11/2022 | 1440/0940 | | US | Cleveland Fed's Loretta Mester | |

| 17/11/2022 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 17/11/2022 | 1540/1040 | | US | Minneapolis Fed's Neel Kashkari | |

| 17/11/2022 | 1540/1040 | | US | Fed Governor Philip Jefferson | |

| 17/11/2022 | 1600/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 17/11/2022 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 17/11/2022 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 17/11/2022 | 1800/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

| 17/11/2022 | 1800/1300 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 17/11/2022 | 1830/1930 | | EU | ECB Lagarde at F. v. Metzler Dinner | |

| 17/11/2022 | 1845/1345 | | US | Minneapolis Fed's Neel Kashkari |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.