Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

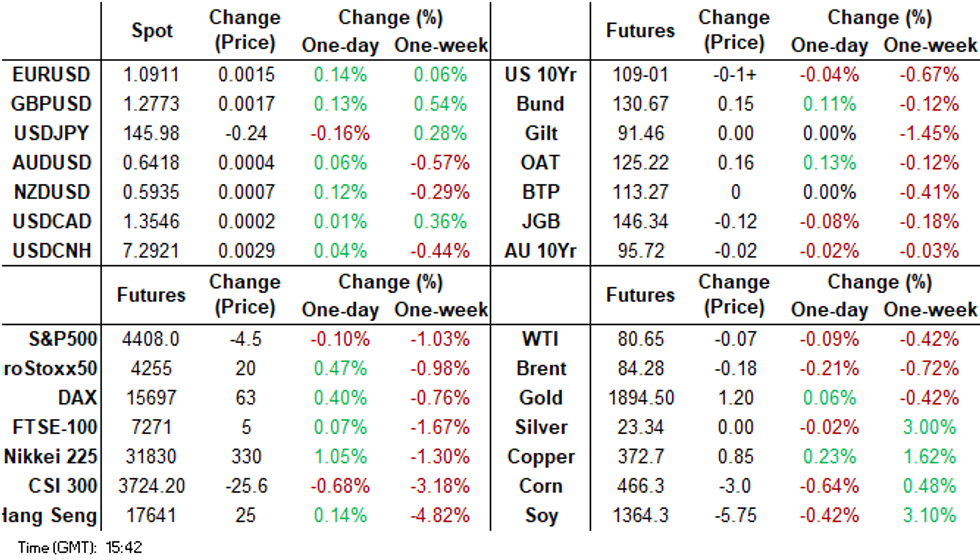

- In early dealing on Tuesday tsys were pressured as participants perhaps looked ahead to Fed Chair Powell's speech at the Jackson Hole Symposium on Friday, a Bloomberg Market Pulse Survey noted that 80% of those surveyed said the speech will reinforce the message of a hawkish hold. TY printed a fresh cycle low at 108-28+ and the 10 Year Yield printed at 4.362% its highest level since 2007. The move lower did not follow through, tsys ticked away from session lows alongside pressure on the USD.

- USD/CNH is bucking the softer USD trend elsewhere (BBDXY down 0.10%), with the pair back above 7.2900 this afternoon. Local equities unable to generate positive upside traction into the break has been a factor, after showing positive signs in early trade. The CNH's Hibor rate also shot higher, as the authorities sold CNH bills in Hong Kong to drain liquidity (35bn yuan total). The market may be taking a buy on dips mentality for USD/CNH given broader US-China policy and growth differentials currently in play. Northbound outflows via the stock connect continue, with a further -4.3bn yuan so far today. Since late July we have seen -65bn yuan in cumulative outflows.

- Looking ahead, there is a thin docket in Europe today, further out we have Existing Home Sales, Philadelphia Fed Non-Mfg Index and Richmond Fed Business Survey. Fedspeak from Richmond Fed President Barkin, Chicago Fed President Goolsbee and Gov Bowman cross.

MARKET

US TSYS: Losses Pared After TY's Fresh Cycle Low

TYU3 deals at 109-01, -0-01+, a 0-07 range has been observed on volume of ~84k.

- Cash tsys sit little changed across the major benchmarks.

- In early dealing on Tuesday tsys were pressured as participants perhaps looked ahead to Fed Chair Powell's speech at the Jackson Hole Symposium on Friday, a Bloomberg Market Pulse Survey noted that 80% of those surveyed said the speech will reinforce the message of a hawkish hold.

- TY printed a fresh cycle low at 108-28+ and the 10 Year Yield printed at 4.362% its highest level since 2007.

- The move lower did not follow through, tsys ticked away from session lows alongside pressure on the USD.

- There is a thin docket in Europe today, further out we have Existing Home Sales, Philadelphia Fed Non-Mfg Index and Richmond Fed Business Survey. Fedspeak from Richmond Fed President Barkin, Chicago Fed President Goolsbee and Gov Bowman cross.

JGBS: Futures Sit Just Above Session Lows, BoJ Gov Ueda & PM Kishida Discuss Financial Conditions

In the Tokyo afternoon session, JGB futures are dealing just above session lows, -11 compared to settlement levels.

- A thin local docket has left market participants on headlines and US tsys watch.

- US tsys sit little changed across the major benchmarks in Asia-Pac trading. The pivotal economic event of this week centres on the speech by Fed Chair Powell at the Jackson Hole gathering on Friday.

- Prime Minister Fumio Kishida and Bank of Japan Governor Kazuo Ueda met Tuesday to discuss financial conditions amid continued weakness in the yen and a rise in bond yields to the highest in nine years. (See link)

- The cash JGB curve bear steepens, with yields flat to 4.4bp higher (20-year).

- The 10-year JGB yield reached 0.665% on Tuesday, the highest since 2014, raising the prospect that the BoJ may come into the market with an unscheduled bond-buying operation to slow gains. (See link)

- The MoF’s Liquidity Enhancement Auction for OTR 5-15.5-Year JGBs sees weaker demand, with the cover ratio declining to 3.604x from 4.237x.

- The swaps curve has also bear steepened, with rates 0.1bp to 1.3bp higher. Swap spreads are narrower.

- Tomorrow the local calendar sees Jibun Bank PMI data for August (Preliminary), along with BoJ Rinban operations covering 1-5-year and 10-25-year JGBs.

AUSSIE BONDS: Cheaper, Narrow range, Tracking Tsys

ACGBs (YM -3.0 & XM -3.0) are weaker, after dealing in a relatively narrow range in the Sydney session. With the local calendar light today, local participants have been guided by US tsys.

- US tsys sit little changed across the major benchmarks in Asia-Pac trading. In early dealings on Tuesday US tsys were pressured as participants perhaps looked ahead to Fed Chair Powell's speech at the Jackson Hole Symposium on Friday. A Bloomberg Market Pulse Survey noted that 80% of those surveyed said the speech will reinforce the message of a hawkish hold.

- Cash ACGBs are 2-3bp cheaper, with the AU-US 10-year yield differential 2bp tighter at -5bp.

- Swap rates are 2bp higher, with EFPs 1bp tighter.

- The bills strip has bear steepened, with pricing -1 to -4.

- RBA-dated OIS pricing is little changed across meetings.

- Tomorrow the local calendar sees the only economic release of the week, namely Judo Bank’s PMI data.

- Tomorrow the AOFM plans to sell A$700mn of the 3.00% 21 November 2033 bond.

- (AFR) Retailers, builders and cafe owners are more likely than other company directors to default on their credit cards and home loans, missing payments to keep their embattled businesses afloat. (See link)

NZGBS: Closed On A Weak Note, Budget In Focus, Implied Swap Spreads Tighter

NZGBs closed on a weak note, with benchmark yields 9-10bp higher. A thin local data docket has left local participants on headlines and US tsys watch.

- Economic activity is slowing, broadly as anticipated in the Budget, with indicators of activity in July pointing to a sluggish start to the Q3, the Treasury Dept. says in Fortnightly Economic Update published Tuesday in Wellington. (See link)

- The RBNZ reports variation to the 2020-2025 funding agreement. Variation is to provide the additional funding required by the RBNZ to implement the new regulatory and supervisory regime under the recently enacted Deposit Takers Act. (See link)

- US tsys have ticked away from Asia-Pac session lows, with little macro newsflow crossing. US tsys are little changed across the major benchmarks.

- Swap rates are 5-7bp higher, with implied swap spreads 4bp narrower.

- RBNZ dated OIS 1-4bp firmer for meetings beyond Feb'24, with terminal OCR expectations at 5.71%.

- Tomorrow the local calendar sees Q2 Retail Sales Ex-Inflation on Wednesday. Spending appetites likely remained subdued through the June quarter. The softness in retail spending reflects that high inflation and interest rate rises have squeezed households' purchasing power.

STIR: US Lags Firming In $-Bloc Terminal Rate Expectations

Over the past week, there has been a firming in terminal rate expectations across the $-bloc, led by the NZ and Canadian markets. In contrast, the US STIR remained fairly stable as investors await the speech by Fed Chair Powell at the upcoming Jackson Hole event on Friday. As of now, terminal rate expectations and the aggregate tightening stand at:

- 5.45%, +12bp (FOMC);

- 5.27%, +27bp (BoC);

- 4.24%, +17bp (RBA); and

- 5.71%, +21bp (RBNZ).

Figure 1: $-Bloc STIR

Source: MNI – Market News / Bloomberg

EQUITIES: CHINEXT Back To May 2020 Lows, Positive Trends Elsewhere

Outside of China/HK equities, regional Asia Pac equity sentiment is mostly positive in Tuesday trade to date. Japan markets have been the strongest performers, with gains around 0.75%. Other markets are mostly seeing gains of around 0.50% at this stage. US equity futures sits slightly in the red. Eminis have largely been range bound, last near 4409. Nasdaq futures are also down a touch, last near 14968.5, but like Eminis largely holding onto gains from Monday's session.

- The Topix is +0.75% at this stage, while the Nikkei 225 is up by the same amount. Some excitement in the tech space is aiding sentiment, with spill over evident from the US Monday session and focus on Nvidia's earnings on Wednesday. The SoftBank Arm IPO is also generating some interest.

- China and Hong Kong equities were stronger in the first part of trade but had little follow through. At the break, the CSI 300 is down ~0.30%, after early gains of as much as 0.80%. The index is making fresh lows back to late November 2022. The CHINEXT index is back to May 2020 lows.

- The HSI is faring slightly better, up 0.16% at the break, but we opened around +1% higher.

- Tech related indices in terms of the Taiex (+0.45%) and Kospi (+0.40%) are modestly higher.

- In SEA, Indonesian and Thai stocks are the best performers, with both indices around 0.60% higher at this stage. Thai politics is in focus with the PM vote currently taking place and former PM Thaksin has returned from a 15yr exile.

FOREX: Greenback Marginally Pressured In Asia

The USD is marginally pressured in Asia today, the greenback has trimmed some of its recent gains and BBDXY now sits a touch above its 200-Day EMA. Ranges do remain narrow thus far on Tuesday and moves have been relatively limited thus far.

- Yen is a touch firmer, USD/JPY printed a low as news crossed that BoJ Governor Ueda will meet with Japan PM Kishida today however losses were pared and we now sit a touch above the ¥146 handle. Technically the uptrend in USD/JPY remains intact, resistance comes in at ¥146.56 (Aug 17 high) and ¥146.93 (8 Nov 22 high).

- Kiwi is up ~0.2%, last printing at $0.5935/40. NZD/USD does however remain well within recent ranges. Bulls look to regain the $0.60 handle to target the 20-Day EMA ($0.6039).

- AUD/USD is ~0.1% firmer sitting a touch above $0.6420. Resistance is at $0.6480 (high from Aug 16).

- Elsewhere in G-10 the Scandies are leading the bid, although liquidity is generally poor in Asia. EUR and GBP are both up ~0.1%.

- Cross asset wise; e-minis have erased early losses to sit little changed and the Hang Seng is a touch firmer. BBDXY is down ~0.1% last printing at 1238.30, the 200-Day EMA comes in at 1237.71. US Tsy Yields have trimmed early gains and sit unchanged across the curve.

- There is a thin docket in Europe on Monday.

OIL: Crude Down, WTI Breaks Below $80 Unsustained

Oil prices have been in a narrow range during APAC trading and are down marginally. WTI is currently around $80, and while it has broken below $80 a number of times today, it hasn’t been able to sustain the move. The intraday low was $79.92. Brent has held above $84 and is around $84.34/bbl. The USD index has trended lower and is down 0.1%.

- Oil has been under pressure from more positive supply news, despite the weaker greenback. Data is showing an increase in shipments from Iran and there are signs that the months-long dispute between Iraq and Turkey may be resolved (worth 500kbd).

- API US inventory data for last week is due to be released later. The previous week it showed crude stocks falling 6.2mn barrels, according to Bloomberg. In light of signs that supply is tightening, US inventory data is being monitored closely.

- In terms of LNG, Woodside has said that talks with unions have been “constructive” including “substantive” agreements on some items. There is the risk of industrial action as early as September 2. European gas prices rose 9.8% on Monday.

- Later the Fed’s Barkin, Goolsbee and Bowman speak and on the data front August Philly and Richmond Fed indices and July existing home sales print. Fed Chairman Powell speaks on Friday, which given demand concerns will be a key event for oil markets.

GOLD: Small Bounce On Monday As USD Weakens

Gold is little changed in the Asia-Pac session, after closing +0.3% at 1894.93 on Monday.

- A weakening in the USD index breathed some life into the yellow metal after touching a low of 1884.89. According to MNI's technicals team, support is seen at that the overnight low of $1884.9, whilst resistance is seen at $1920.7.

- Despite the overnight strengthening, bullion remained near a five-month low on increasing signs that US interest rates will need to stay higher for longer. On Monday, the US 10-year nominal and real yields rose to 4.35% and 2.0% respectively, marking their highest points since 2007 and 2009.

- The pivotal economic event of this week centres on the speech by Fed Chair Powell at the Jackson Hole gathering on Friday. The prevailing concern is that Powell might undermine investors' optimistic expectations, specifically the notion that the Federal Reserve has concluded its interest rate hikes and is poised to initiate rate cuts in the early months of the upcoming year.

ASIA FX: USD/Asia Pairs Find Support Post Early Dip

Most USD/Asia pairs are away from session lows, after a softer USD tone was evident in the first part of trade. This has been most evident for USD/CNH, which climbed nearly 300pips from earlier lows., USD/PHP and USD/IDR have also struggled for further downside. Thailand politics are in focus, but THB has been quiet so far. Tomorrow, we get South Korean business confidence early, along with Singapore CPI, then Taiwan IP later.

- USD/CNH is bucking the softer USD trend elsewhere (BBDXY down 0.10%), with the pair back above 7.2900 this afternoon. Highs for the session sit just under 7.2975. Earlier lows were at 7.2691. Local equities unable to generate positive upside traction into the break has been a factor, after showing positive signs in early trade. The CNH's Hibor rate also shot higher, as the authorities sold CNH bills in Hong Kong to drain liquidity (35bn yuan total). The market may be taking a buy on dips mentality for USD/CNH given broader US-China policy and growth differentials currently in play. Northbound outflows via the stock connect continue, with a further -4.3bn yuan so far today. Since late July we have seen -65bn yuan in cumulative outflows.

- USD/THB has tracked tight ranges today. The pair saw early support sub 35.10 emerge and we last tracked near 35.12. BoT vowed that it will curb excessive THB volatility. The new PM vote is currently underway with Pheu Thai's Srettha the only candidate put forward. PM candidate Srettha may struggle to gain support from the 61 senators he needs to become PM as the senate review into his tax affairs has raised more questions. Srettha denies the accusations. Pheu Thai’s commitment to reform the constitution is also putting some offside. Another senator has said that Srettha should receive around 190 votes from the senate, as they want the impasse to end. If he fails, Pheu Thai has two other candidates. Former PM Thaksin has also returned from 15yrs in exile but will serve a total of 8 years in prison per a Supreme Court statement.

- USD/IDR sits slightly above earlier lows, the pair last near 15330. The rupiah is modestly underperforming the softer USD trend seen elsewhere. Earlier lows in the pair came in at 15318. Recent highs from mid August recent around 15360, while support has been evident around 15280/85 in recent sessions. The nearest EMA is around 15207, for the 20-day. On the data front, the Q2 current account was weaker than expected, printing at -$1.9bn, versus -$268mn expected. The Q1 print was just under +$3bn. As a share of GDP the deficit was -0.5% in Q2. While the market expected the current account to shift back into deficit, the worst than expected result is likely weighing on IDR sentiment at the margins, particularly given the continued move higher in US real yields.

- USD/MYR prints at 4.6490/4.6525, the pair is little changed from Monday's closing levels dealing in a narrow range on Tuesday. The pair sits a touch off its highest level since mid-July as August's gains are consolidated in a narrow range. USD/MYR is up ~3.3% month to date. On the wires today we have Aug 15 Foreign Reserves, there is no estimate for the print and the prior read was $112.9bn.

- The SGD NEER (per Goldman Sachs estimates) sits a touch off its highest level since 10 Aug, we sit ~0.7% below the top of the band. USD/SGD is holding a narrow range below the $1.36 handle, broader USD trends continue to dominate flows in recent sessions. Tomorrow's July CPI print provides the highlight this week, headline CPI is expected to tick lower to 4.2% Y/Y and Core to 3.8% Y/Y.

- USD/PHP has rebounded from earlier lows, the pair last near 56.25. Earlier we touched below 56.10. The pair isn't too far away from the 20-day EMA near 55.96. Earlier August highs rest at 57.00. This week's data calendar is light with just the July budget balance on tap this Friday. The BSP expects economic growth this year to miss the government's target. HSBC also notes that the 57.00 level may be a firm intervention point to protect PHP from further depreciation pressures.

SOUTH KOREA: Consumer Sentiment Rebound Pauses, Inflation Expectations Steady In August

The recovery in South Korean consumer sentiment paused in August. The headline index eased back to 103.1, from 103.2 in July. Still, we are comfortably off recent cyclical lows, and the index is still suggesting an improved y/y GDP backdrop as we progress through H2, see the first chart below.

- The main headwind that appeared in August was sentiment around the domestic economy, which dipped to 80 from 84. Spending plans remain around recent highs though.

Fig 1: South Korean Consumer Sentiment & GDP Y/Y

Source: MNI - Market News/Bloomberg

- On the inflation front, the expected inflation level in 12 months time was unchanged at 3.3%. The rate of decline in inflation expectations has slowed in recent months. There is now a reasonable wedge between this metric and headline y/y CPI, see the chart below.

- Expected wages were steady at 118, although house price expectations rose to 107 from 102.

Fig 2: Consumer Inflation Expectations - Easing Trend Paused in August

Source: MNI - Market News/Bloomberg

SOUTH KOREA: Highlights From Local News Wires

Below is a collection of news wires reports from English versions of South Korean Newspapers from the past day or so.

ECONOMY: Korea trapped in state of declining productivity (link)

ECONOMY: Cooling Chinese demand may dampen Korea’s economic recovery (link)

ECONOMY: China risk and Korea's de-risking (link)

INFLATION: Korean inflation expectations stay flat in August: BOK poll (link)

INFLATION: Regional consumer inflation up 3.2 pct in Q2 (link)

DEBT: Household credit soars in Q2 despite high borrowing costs (link)

TRADE: South Korea Loses Ground to Taiwan, ASEAN in Chinese Market (link)

SHIPPING: S. Korean shipbuilders' new orders up 11.9 percent in H1 (link)

GEOPOLITICS: Korea, US, Japan Initiate ‘De-risking’ against China; from Supply Chain to Space (link)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 22/08/2023 | 0600/0700 | *** |  | UK | Public Sector Finances |

| 22/08/2023 | 0600/0800 | ** |  | NO | Norway GDP |

| 22/08/2023 | 0800/1000 | ** |  | EU | EZ Current Account |

| 22/08/2023 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 22/08/2023 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 22/08/2023 | - | * |  | FR | Retail Sales |

| 22/08/2023 | 1230/0830 | ** |  | US | Philadelphia Fed Nonmanufacturing Index |

| 22/08/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 22/08/2023 | 1400/1000 | *** | | US | NAR existing home sales |

| 22/08/2023 | 1400/1000 | ** | | US | Richmond Fed Survey |

| 22/08/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 22/08/2023 | 1830/1430 | | US | Chicago Fed's Austan Goolsbee | |

| 23/08/2023 | 2300/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.