Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

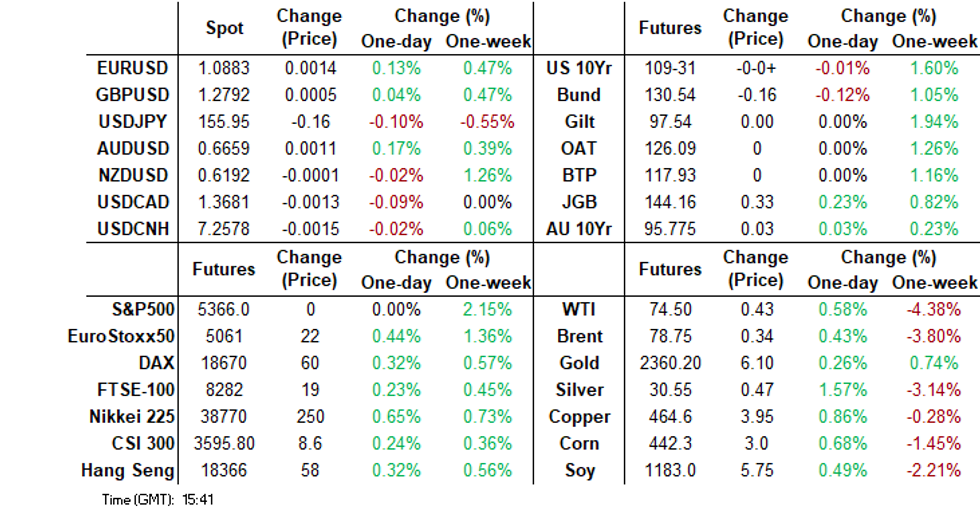

- JGB futures richer and just off session highs, +32 compared to the settlement levels. The market responded positively to strong demand metrics at today’s 30-year auction. USD/JPY dipped in the first part of trade, but has recouped most losses.

- BoJ board member Nakamura stated current easy policy settings were appropriate. Governor Ueda, appearing before parliament, emphasized the need for caution on interest rates due to uncertainties in measuring the neutral rate and suggested that it is appropriate to reduce bond buying as part of the exit process.

- US Tsy futures sit slightly lower, but ranges have been tight. Australian data showed strongly lending to households, while export growth weakened.

- Later US jobless claims, May Challenger job cuts, April trade and final Q1 productivity/ULC as well as April German orders and euro area retail sales print. The ECB decision is announced and a 25bp cut is expected.

MARKETS

US TSYS: Tsys Futures Edge Lower, 10Y Yield Tests Trendline

- Treasury futures are slightly lower today, ranges have been tight. Futures made highs on the opened and have since edged lower TU is -0-00⅝ at 102-05⅜, while TY - 01+ at 110-08.

- Volumes: TU 33k, FV 55k TY106k - largely in line with Wednesday.

- Tsys flows: 5,606k Block UXY at 114-00, likely seller.

- The 10Y yield is now testing trendline support, while the recent move in Oil (down ~8% over the past week) could point to a break of the trendline support as the 10y yield has largely followed Oil prices over the past year by a few weeks. See chart 1 - Source BBG

- Cash treasury curve have moved wider today, yields are 1-2bps higher, the 2Y +1.6bp to 4.739%, the 10Y +1.7bps at 4.293%, the 2y10y +0.078 at -44.808.

- Late year rate cut projections have gradually gained vs. late Tuesday levels (*): June 2024 at -1.3% w/ cumulative rate cut -.3bp at 5.328%, July'24 at -18% w/ cumulative at -4.8bp (-4.3bp) at 5.283%, Sep'24 cumulative -19.8bp (-19.3bp), Nov'24 cumulative -28.9bp (-27.8bp), Dec'24 -47bp (-44.3bp).

- Looking ahead; Weekly Claims & Trade Balance as well as ECB policy announcement.

JGBS: Bull-Flattener Post-30Y Auction

JGB futures richer and just off session highs, +32 compared to the settlement levels.

- The market responded positively to strong demand metrics at today’s 30-year auction. The low price beat dealer expectations, the cover ratio increased and the auction tail narrowed. The 30-year JGB is dealing 6bps lower in post-auction trade.

- Like Tuesday's 10-year supply, today's outcome established a more optimistic tone ahead of next week’s BoJ monetary policy decision for a market that has experienced mounting pressure since mid-December, fueled by expectations of policy tightening from the BoJ.

- BoJ Governor Ueda stated in Parliament that price expectations must be around 2% to meet the price target, but current inflation expectations are still below 2%. He emphasised the need for caution on interest rates due to uncertainties in measuring the neutral rate and suggested that it is appropriate to reduce bond buying as part of the exit process.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session.

- The cash JGB curve has bull-flattened, with yields 2-9bps lower. The benchmark 10-year yield is 5.3bps lower at 0.963% versus the cycle high of 1.101% set late last week.

- Swap rates are lower across maturities, with the 4-7-year zone outperforming.

- Tomorrow, the local calendar will see Household Spending data, and Coincident and Leading Indices alongside BoJ Rinban Operation covering 1-3-year and 5-25-year JGBs.

AUSSIE BONDS: Richer, ECB Policy Decision In Focus

ACGBs (YM +3.0 & XM +4.0) are richer and just off Sydney session highs.

- Outside of the previously outlined Home Loan Values and Trade Balance data, there hasn't been much in the way of domestic drivers to flag.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session after the recent rally extended to a fifth day yesterday following weaker-than-expected ADP Private Employment data.

- The focus now turns to Thursday's Weekly Claims and Unit Labor Costs as well as the ECB Policy Decision. Non-Farm Payrolls data is due on Friday.

- Cash ACGBs are 4bps richer, with the AU-US 10-year yield differential at -9bps.

- Swap rates are 3-4bps lower.

- The bills strip has bull-flattened, with pricing flat to +4.

- RBA-dated OIS pricing is 1-4bps softer for meetings beyond September. A cumulative 9bps of easing is priced by year-end.

- Tomorrow, the local calendar is relatively light, with the highlights being the Foreign Reserves data and RBA Deputy Governor Andrew Hauser’s Fireside Chat at Australia’s Economic Outlook event.

AUSTRALIAN DATA: Home Lending Very Strong Especially To Investors

New lending for housing is strong and remained so in April. It rose a stronger than expected 4.8% m/m, the third consecutive monthly rise, to be up 24.6% y/y, the highest since December 2021. Robust demand from strong population growth and rising house prices and rents are pushing up loan values.

- The value of lending for owner occupiers rose 4.3% m/m to be up 18.7% y/y but this was outpaced by investors rising 5.6% m/m to be up 36.1% y/y. Both types of borrowers are seeing double-digit 3-month momentum.

- The ABS notes that robust lending to investors “reflects expectations of higher rental yields and the greater borrowing capacity of investors”. Loans have been growing very strongly in NSW and Queensland at close to 50% y/y.

- The value of loans to first time home buyers rose 3.4% m/m to be up 18.6% y/y. The number of loans rose 3% m/m to be up 10.8% y/y.

- Personal loan values rose 0.8% m/m due to a 1.2% rise in car loans.

Source: MNI - Market News/ABS

AUSTRALIAN DATA: Trade Surplus Trending Lower On Weak Export Growth

The merchandise trade surplus widened more than expected in April to $6548mn from $4841mn due to a sharp drop in imports. Exports fell 2.5% m/m while imports sank 7.2% with the weakness broad-based across the major components. The series is nominal and so price fluctuations are important especially for commodities.

- The trade surplus has now been trending lower for almost two years.

Source: MNI - Market News/ABS

- Goods exports are down 5.9% y/y and have been negative year-on-year for the last 13 months. Both rural and non-rural goods fell on the month but the weakness was driven by Australia’s major commodity exports. Non-monetary gold shipments have been very strong up 83% y/y in April.

- Merchandise imports are up 2% y/y. The April weakness was seen across consumer (-5.4% m/m), capital (-5.8%) and intermediate goods (-9.6%) but looking through the volatility 3-month average annual rates are still solid.

- Clothing & footwear and consumer goods imports were weak reflecting soft consumption but vehicles rose. In terms of the investment outlook, machinery & equipment and industrial transport fell while telecoms equipment rose.

Source: MNI - Market News/ABS

AUSTRALIAN DATA: Exports To Asia Broadly Soft

Exports to most of Asia remain weak compared to a year ago pressured by lower commodity prices but also softer volumes. Exports to the US, UK and NZ continue to hold up. With over a third of Australian merchandise exports going to China, current weakness will be concerning and soft demand remains a significant uncertainty that the RBA is monitoring closely.

- Exports to China fell 3% y/y in April, the fourth straight month of contraction. Japan is Australia’s second largest destination worth around 15% of total exports and shipments fell 16.9% y/y, the 13th consecutive decline. Korea is the third largest and exports fell 9.4% y/y. Shipments to Taiwan fell 23.7% y/y and to India 28.5% y/y. But they were up 5.1% y/y to the US and 3.3% to NZ.

Source: MNI - Market News/ABS

- Exports of Australia’s major commodities were weak with metal ores & minerals down 4.3% m/m, coal -4% m/m and other mineral fuels -4.9% m/m.

- The value and volume of iron ore exports fell in April after a large rise in the latter in March but prices have now fallen for three straight months. The weakness in quantities shipped was due to China.

- Semi-soft and thermal coal volumes both fell in April due to Japan and China but hard coking rose driven by demand from Indonesia and Taiwan. The last monthly rise in unit values for thermal & hard coking was in November 2023.

- LNG export volumes fell 2.7% m/m after a similar rise in March while prices fell for the third consecutive month.

NZGBS: Closed Richer & At Session Bests, May-28 Tap Showed Strong Demand

NZGBs closed at the session’s best levels, 3bps richer. The previously outlined domestic data drop (CoreLogic House Prices, Construction Work and ANZ Commodity Prices) failed to provide much of a market moving catalyst.

- The market appeared more focused on today’s syndicated tap of the May-28 bond. News that an additional NZ$3.5bn of the line was issued, the high end of the issuance range of NZ$2-4bn, seemed to buoy the market. The bonds were issued at 4bps under the April 2027 nominal bond versus guidance 3-6bps under. There will be no further issuance of the bond prior to September 2024.

- Cash US tsys are dealing 1-2bps cheaper in today’s Asia-Pac session ahead of Weekly Claims and Unit Labor Costs as well as the ECB Policy Decision. Friday will see Non-Farm Payrolls data.

- Swap rates closed 4bps lower.

- RBNZ dated OIS pricing closed little changed. A cumulative 25bps of easing is priced by year-end.

- Tomorrow, the local calendar will see Mfg Activity data.

NEW ZEALAND DATA: Housing Market Soft As Affordability Very Low

Data released in NZ today showed a soft housing sector with Q1 residential construction down 4.8% q/q and CoreLogic house prices for May falling 0.2% m/m, the second straight monthly drop but they are 1% higher than a year ago. As a result, the RBNZ is unlikely to be concerned that the sector is adding to inflationary pressures.

- With the working age population rising 3.1% y/y in Q1 demand for housing has been strong reflected in rents rising 4.7% y/y and house sales up sharply.

- Strong population growth and weak residential construction has resulted in strong price rises in Australia since early 2023, but in NZ CoreLogic prices are still 10.7% below the March 2022 peak and only 2.9% above the September 2023 trough. Australian prices in May were 13.8% above their trough.

- CoreLogic notes that there has been a shift with policy changes impacting the market. The first home buyers grant has been abolished and a debt-to-income cap has been introduced but the LVR rules have been eased which should be supportive.

- The RBNZ has made it clear that rates are on hold for now and so with mortgage rates unlikely to ease this year and housing affordability at its worst since 2008 (HAI is 36.5% below trend), the housing market is likely to remain soft and rental growth high.

- Housing has been undervalued in NZ for the last year and that increased slightly in Q1 to 4.8% from 4.6%.

Source: MNI - Market News/Bloomberg/Refinitiv

FOREX: USD Up From Lows, Dovish BoJ Rhetoric Curbs Yen Gains

The USD BBDXY index sits lower for the first part of Thursday's session, lats near 1250.10, but we are comfortably up from earlier lows (1248.99).

- USD/JPY got to lows of 155.37, but we sit back at 155.80 in recent dealings. The trough for the pair coincided with a speech from dovish BoJ board member Nakamura, who stated that the current easy policy settings are appropriate.

- Governor Ueda is before parliament at the moment and stated inflation expectations are rising but not yet at 2%. JGB yields are lower across the board, aided by a strong local debt auction, which is likely curbing yen appetite as well.

- AUD/USD is around 0.6660 currently, up 0.20%, but off earlier highs of 0.6683. Locally data showed better housing finance and trade surplus figures, although export growth is slowing.

- NZD/USD is back under 0.6200, drawing some selling interest on a move above this level, which is a fresh multi month high.

- In the cross asset space, US yields are 1-2bps higher, aiding the USD at the margins. The regional equity backdrop is positive, although gains are mostly sub those seen in Wednesday moves in EU/US markets.

- Looking ahead, US jobless claims, May Challenger job cuts, April trade and final Q1 productivity/ULC as well as April German orders and euro area retail sales print. The ECB decision is announced and a 25bp cut is expected.

ASIA STOCKS: HK & China Equities Mixed As Property Weigh On Sentiment

Hong Kong & Chinese equities are mixed today, is has been a quiet past week for local markets. Property remains front and center on investors minds, with the BI property gauge falling 20% from recent highs as doubts remain on Beijing’s efforts to bolster the sector while developers’ liquidity pressure still persists as sales remain weak. Regulators are considering suspending data feeds to financials institutions in order to stop speculations and volatility.

- Hong Kong equities are higher today, tech stocks are the top performing largely tracking moves made overnight in the US after the Philadelphia Semiconductor Index finished the session up 4.50%. The HSTech Index is up 1.30% and is now trading back above all EMAs, while the RSI is back above 50. Property is underperforming wider markets today with the Mainland Property Index is down 1.40% and the HS Property Index is up 0.42%, the wider HSI is currently trading 0.59% higher.

- China equites are slightly lagging their HK peers , small-cap indices are the worst performing with the CSI 1000 down 1.65% and the CSI2000 down 3.27% while the Growth focused ChiNext Index is down 0.17%, the large-cap CSI 300 is up 0.37%

- In the property space, Greentown China has repurchased $150 million of its 2.3% credit enhanced bonds due 2025, representing 37.5% of the originally issued amount, leaving $250 million outstanding, with the bonds backed by an irrevocable standby letter of credit from China Zheshang Bank.

- The Shanghai and Shenzhen stock exchanges are considering suspending granular market data feeds to institutions, including quantitative funds, to combat market volatility, according to Reuters.

- (MNI): MNI China Press Digest June 6: NIM, Car Sales, Carbon (See link)

- Looking ahead: Tomorrow we have China Trade Balance data.

ASIA PAC STOCKS: Asian Stocks Higher, As US Tech Names Rally

Asian equities are higher Today following moves made overnight after US tech names help push markets to new all time highs. Indian stocks rose after Prime Minister Narendra Modi secured crucial support from two key coalition allies, enabling him to extend his decade-long tenure in power. Global yields continue tighten as markets price in two fed rate cuts into year-end, while lower Oil prices could also help bring yields down further. Overnight, private payrolls showed hiring at companies grew at the slowest pace since the start of the year, with eyes now on the US jobs data out on Friday. Earlier, NZ ANZ commodity export prices rose, while construction work fell, AU April Trade Surplus widen, and Japan's Tokyo May Office vacancies rose.

- Japanese equities are higher today, although well of earlier highs, sentiment around fed cuts improve follow a slowdown in private job growth have help stocks. Tech stocks are performing well, following moves made overnight. While the yen weakens a touch and JGB yields falling is helping the local market. Earlier, the Japan Tokyo may office vacancies rose to 5.48% from 5.38% prior. The tech heavy Nikkei 225 is up about 0.60%, while the Topix is 0.30%.

- Taiwan equities have surged higher today and are now testing all time highs, the moves can be attributed to strong tech prices in the US overnight and weaker than expected US employment change which saw rate cut projections gain. The Taiex is up 2%

- Australian equities also higher today, earlier the Trade Surplus widened to 6,548M m/m in May vs. 5,500M expected, while home loan value jumped as higher rental yields attract property investors. All sectors are in the green today, with Financials the top performing, followed by industrial names. The ASX200 is up 0.80%.

- Elsewhere in SEA, New Zealand Equities are 0.10% lower as the NZD currency continues to tick higher. Singapore equities are 0.50% higher following weaker-than expected Retail Sales yesterday. The Indonesian JCI is 0.10% higher, earlier we broke back above 7,000 and were up over 1%. The Philippines PSEi is up 0.80% following the unemployment rate rising to 4$ from 3.9%. Indian equities are 0.70% higher after President Modi secured support.

JAPAN DATA: Offshore Buying Of Local Equities Continues For 6th Straight Week

Japan weekly investment flows showed offshore momentum continued into local equities. We saw ¥282bn in net equity purchases, marking the 6th straight week of positive flows into this space. Offshore investors also purchased local bonds, but the trend for this segment remains mixed in recent weeks and negative since mid-March. Japan yields have moved off recent highs in the first part of June.

- In terms of domestic outflows, Japan investors purchased offshore bonds last week. The ¥1323bn in outflows more than offset last week's net sales, although the cumulative flow backdrop is negative for the past few months. Local investors sold offshore equities for the second straight week.

Table 1: Japan Weekly Investment Flows

| Billion Yen | Week ending May 31 | Prior Week |

| Foreign Buying Japan Stocks | 282.0 | 82.4 |

| Foreign Buying Japan Bonds | 337.4 | -789 |

| Japan Buying Foreign Bonds | 1323.4 | -310.4 |

| Japan Buying Foreign Stocks | -588.7 | -433.3 |

Source: MNI - Market News/Bloomberg

ASIA EQUITY FLOWS: Equity Flows Remain Negative, India See Largest Outflow On Record

- South Korean equities followed global markets higher on Wednesday, SK GDP was slightly below consensus coming in at 3.3% vs 3.4%. The short-term has seen better selling from foreign investors, although Wednesday did see a decent inflow of $470m, the past 5 session have seen a total outflow of $693. The 5-day average is now -$138m, well below the 20-day average of -$47m, and the longer term 100-day average at $136m.

- Taiwan equities were higher on Wednesday and we bounced off the 20-day EMA again. Foreign investors have been better sellers of local equities recently although the trend is slowing, with the past 5 sessions seeing an outflow of $3.1b, Wednesday saw just a small $94m outflow. Later today we have CPI. The 5-day average is -$620m, well below the 20-day average at $57m and the 100-day average at $17m.

- Thailand equities were little changed on Wednesday and the SET is continues to test yearly lows made on Apr 19th. Foreign investors have sold equities for the past 10 sessions, with the past 5 seeing a net outflow of $352m. Focus this week will be on CPI due out on Friday. The 5-day average is now -$62m, below both the 20-day average at -$21m and the 100-day average at -$23m.

- Indonesian equities have now marked 10 straight sessions of selling from foreign investors, with the past 5 session seeing a net outflow of $130m. The JCI made new fresh ytd lows and closed below 7,000 for the second time this week. The 5-day average is now -$26m, below both the 20-day average at -$37m and the 100-day average at -$2m.

- Philippines equities also continue to see selling from foreign investors, we have now marked 8 straight days of net selling, with the past 5 sessions seeing a total outflow of $145.9m. The PSEi was able to close teh session higher and back above the 6,400 level. The 5-day average is -$29m, below the 20-day average at -$8.6m and the 100-day average at -$5.1m.

- Indian equities have been very volatile over the past few days due to the presidential elections, the Nifity 50 dropped over 5% on Tuesday tapping the the 200-day EMA before recovering some of those moves yesterday. Tuesday also marked the largest outflow from foreign investors on record for a outflow of $1.4b. The 5-day average is now -$206m, 20-day average is -$166m, both below the 100-day average at $13m

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | 470 | -693 | 13933 |

| Taiwan (USDmn) | -94 | -3101 | 2127 |

| India (USDmn)* | -1466 | -1033 | -3404 |

| Indonesia (USDmn) | -35 | -130 | -388 |

| Thailand (USDmn) | -3 | -310 | -2345 |

| Malaysia (USDmn) ** | 54 | -173 | -106 |

| Philippines (USDmn) | -10 | -145.9 | -466 |

| Total | -1085 | -5585 | 9351 |

| * Data Up To June 4 |

OIL: Crude Holding Onto Gains But Outlook Soft

Oil prices have continued Wednesday’s rise during today’s APAC trading. Crude found a floor when the market appeared oversold. Better risk sentiment and a softer US dollar (USD index -0.1%) have also provided support. WTI is up 0.5% to $74.47/bbl, close to the intraday high of $74.59, while Brent is 0.4% higher at $78.71 after reaching $78.84.

- On Sunday OPEC announced that it would reduce its production cuts from October but it retains the flexibility to alter that plan depending on market developments. Saudi Aramco has cut prices for June shipments to Asia for the first time since February though, which is a sign that it is concerned about demand in the region.

- The EIA reported a US crude inventory build of 1.23mn barrels with gasoline up 2.1mn, highest in just over 2 months, and distillate 3.2mn. Refinery utilisation rose 1.1pp to 95.4%, higher than expected. Implied demand for gasoline and distillate were both lower.

- Later US jobless claims, May Challenger job cuts, April trade and final Q1 productivity/ULC as well as April German orders and euro area retail sales print. The ECB decision is announced and a 25bp cut is expected.

GOLD: Lower US Treasury Yields Provide Support

Gold is 0.5% higher in the Asia-Pac session, after closing 1.2% higher at $2355.32 on Wednesday. The yellow metal has been in a $2,320-2,360 for most of the last nine sessions.

- Bullion was supported by US Treasuries, which extended their recent rally to a fifth day.

- US Treasuries cheered further signs of a slowing job market and cooling price pressures, with the BoC's policy easing and plans for another in July bolstering hopes for global rate cuts.

- ADP jobs gain was lower than expected at +152k vs. +175k est (192k prior down-revised to +188k).

- Fast two-way flow reported after mixed ISM Services data: Index higher than exp (53.8 vs. 51.0 est) but lower Prices Paid (58.1 vs. 59.0 est).

- The focus now turns to Thursday's Weekly Claims and Unit Labor Costs as well as the ECB Policy Decision, followed by Friday's Non-Farm Payrolls data.

- According to MNI’s technicals team,a bear cycle in gold remains in play for now, although the medium-term trend structure is bullish, and the recent move down appears to be a correction that is allowing an overbought condition to unwind.

- A resumption of gains would open $2,452.5 next, a Fibonacci projection. The 50-day EMA, at $2,312.0, represents a key support.

RBI: MNI RBI Preview - June 2024: On Hold, Food Inflation In Focus

- None of the 34 economists polled by Bloomberg see an RBI shift at tomorrow’s policy. This is also our strong bias, which if realized, will see the policy rate held 6.50%. This has been the policy rate since February last year. The cash reserve ratio is also expected to be held steady at 4.50%.

- Rate cuts for India are seen more towards the end of this year, rather than a near term risk, which is also our bias in terms of the outlook.

- Full preview here:

ASIA FX: USD/Asia Pairs Lower, But Limited Moves Outside Of Baht Gains

USD/Asia pairs are mostly lower in line with USD weakness against the majors and a positive equity tone through most of the Asia Pac region. However, outside of strong spot THB gains and a move lower in the 1month USD/KRW NDF, other pairs have exhibited more modest trends. Tomorrow, we get the China trade figures for May, along with the RBI decision as the main focus points. No change is expected from the RBI. Thailand CPI and Taiwan trade figures are also out.

- USD/CNH has exhibited low volatility with respect to broader USD moves. The pair last around 7.2570, slightly lower for the session. the USD/CNY fix moved above 7.1100 but remains sub recent highs. Onshore equities are higher despite property market names struggling, as the May rally continues to be unwound.

- 1 month USD/KRW is back to 1363/64 region, around +0.30% stronger in won terms. Earlier lows were at 1361.4. The better equity mood, particularly in the tech space has aided sentiment, although onshore markets have been closed today (returning tomorrow).

- USD/TWD post is back under 32.30, a +0.15% TWD gain. Local equities are around +2% higher, following the surge in tech/chip stocks in Wednesday US trade (led by Nvidia).

- USD/THB has fallen a little over 0.60% in the first part of Thursday trade. We were last near 36.45, slightly up from session lows near 36.42. This puts us back sub the 50-day EMA (around 36.51). Yesterday's moves above the 20-day (36.64) couldn't be sustained. The 100-day EMA is back near 36.23. Concerns around BoT independence, amid reports the government will look to exert more influence over the central bank weighed on baht yesterday. Still, broader USD/US yield trends will also be a key near term driver for USD/THB. US-TH 2yr government bond yields sit back at +237bps, lows in the spread back to early March this year.

- USD/IDR holds a touch below recent highs, last around 16285. Headlines have crossed of BI being in the market to support the rupiah, but downside momentum in the pair has proven to be limtied at this stage.

INDONESIA: INDON Sov Continues Twist-Flattening Move, 7yr 30bps Tighter Past Week

The INDON sov curve has continued it twist-flattening move, again seeing better buying at the 7yr. There hasn't much in the way of data out of the region today, earlier it was reported that Bank Indonesia was seen in the FX market managing USD supply.

- The INDON curve has again twist-flattened today, yields are 2-5bps lower, the 2Y yield is -1bps at 5.245%, 5Y yield is -3bps at 5.015%, the 10Y yield is -4bps at 5.085%, while the 5-year CDS is 1bps lower at 72bps.

- The 7yr is 30bps tighter over the week, outperforming nearby tenors by about 5bps.

- The INDON to UST spread diff the 2Y is now 51bps (+3bp), 5yr is 70bps (+1bps), while the 10yr is 79bps (+0.5bps). The INDON curve has widened 12-17bp vs UST curve over the past week.

- In cross-asset moves, USD/IDR is little changed today, the JCI is also unchanged today after earlier trading 1% higher and breaking back above 7,000, while tsys futures are edged lower through the day, yields are 1-2bps higher.

- Looking ahead, it is a quiet week with just Foreign Reserves for May on Friday.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 06/06/2024 | 0545/0745 | ** |  | CH | Unemployment |

| 06/06/2024 | 0600/0800 | ** |  | DE | Manufacturing Orders |

| 06/06/2024 | 0700/0900 | ** |  | ES | Industrial Production |

| 06/06/2024 | 0730/0930 | ** |  | EU | S&P Global Final Eurozone Construction PMI |

| 06/06/2024 | 0800/1000 | * |  | IT | Retail Sales |

| 06/06/2024 | 0830/0930 | ** |  | UK | S&P Global/CIPS Construction PMI |

| 06/06/2024 | 0830/0930 | | UK | BOE's Decision Maker Panel Data | |

| 06/06/2024 | 0900/1100 | ** | | EU | Retail Sales |

| 06/06/2024 | 1215/1415 | *** | | EU | ECB Deposit Rate |

| 06/06/2024 | 1215/1415 | *** | | EU | ECB Main Refi Rate |

| 06/06/2024 | 1215/1415 | *** | | EU | ECB Marginal Lending Rate |

| 06/06/2024 | 1230/0830 | *** |  | US | Jobless Claims |

| 06/06/2024 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 06/06/2024 | 1230/0830 | ** | | US | Trade Balance |

| 06/06/2024 | 1230/0830 | ** | | US | Non-Farm Productivity (f) |

| 06/06/2024 | 1230/0830 | ** |  | CA | International Merchandise Trade (Trade Balance) |

| 06/06/2024 | 1245/1445 | | EU | ECB Monetary Policy Press Conference | |

| 06/06/2024 | 1400/1000 | * | | CA | Ivey PMI |

| 06/06/2024 | 1415/1615 | | EU | ECB's Lagarde presents monpol decision on podcast | |

| 06/06/2024 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 06/06/2024 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 06/06/2024 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.