Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

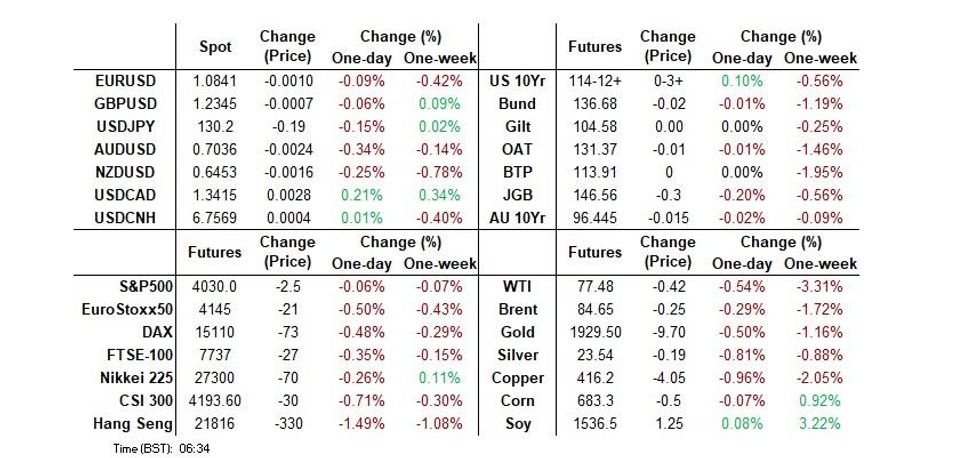

- The supportive USD tone has persisted through today's Asia session.

- The regional tone to Asia Pac equities is a weaker one.

- Looking ahead, preliminary euro area Q4 GDP is out and in the U.S. we will get Q4 employment cost index, Chicago PMI and November house price readings.

US TSYS: Marginally Cheaper in Asia, Fed In View

TYH3 deals at 114-11, +0-02, operating within a narrow 0-05 range, on volume of ~70K.

- Cash Tsys sit 0.5-1bp cheaper across the major benchmarks, with some late Tokyo weakness in JGBs applying modest pressure as we head into European hours.

- Tsys firmed in early Asia trade as a bid in ACGB's, in lieu of soft Australian retail sales data, fed through.

- Firmer than expected non-manf PMI data from China the applied some counter (the country's reopening drive and the LNY break were at the fore there), allowing Tsys to retreat from best levels.

- CPI data from France and Eurozone GDP headline during the London morning. Further out we have the house price index, MNI Chicago PMI and conference board consumer confidence, although more focus is set to fall on the ECI print.

JGBS: Sliding Into The Close

JGB futures have faltered into the bell, with participants seemingly unimpressed by the demand for the latest 1tn of 5-Year loans offered to banks via the BoJ’s Funds-Supplying Operations against Pooled Collateral channel (demand was actually a little higher than that seen at last week’s offering, while the average rate applied to the operation was a incrementally lower, ~30bp below prevailing 5-Year swap rates).

- That leaves the contract on the backfoot into the close, recently registering fresh session lows to print -34, while cash JGBs are 2.5bp cheaper to 0.5bp richer as 7s lead the sell off on the weakness in futures, while the curve twist flattens with a pivot around 20s.

- Local data had no tangible impact on the space.

- Local headline flow was dominated by comments from Finance Minister Suzuki, who outlined the government’s agreement with the BoJ view re: the need for more meaningful wage increases, while stressing that it is too early to discuss the idea of a revision to the BoJ-government accord (likely eying the impending departure of Governor Kuroda as the tipping point on that front).

- There was smooth enough digestion of the latest 2-Year JGB auction.

- Final manufacturing PMI data headlines the local docket on Wednesday.

AUSSIE BONDS: Twist Steepening As Retail Sales Bounce Fades

YM finished +1.0, while XM was -1.5. Cash ACGBs saw 1bp richening to 3bp of cheapening as the curve twist steepened, pivoting around 5s.

- Aussie bonds firmed in the wake of a much softer than expected outcome for domestic retail sales data, with the Black Friday impact continuing to distort the data at this time of year, while an upward revision to the November reading provided further downward pressure to the December outcome.

- A reminder that the health of the consumer is a focal point for the RBA as the lagged impacts of monetary tightening take hold.

- Bills were 1-4bp richer through the reds at the bell, bull steepening, with RBA dated OIS showing 23bp of tightening for next week’s meeting alongside a terminal cash rate of ~3.70% (the latter came in by ~10bp post-retail sales).

- The space then pulled away from best levels ahead of official Chinese PMI data, which saw the country’s well-documented move away from ZCS and the LNY holiday period combine to provide a much firmer than expected outcome for the non-manufacturing PMI print.

- A late downtick was then observed, probably aided by reports of the scheduling of a telephone call between the Australian & Chinese trade ministers (seemingly for some point next week), as Sino-Aussie relations continue to thaw.

- On the semi-issuance front, A$1.5bn of QTC’s new 4.50% Aug-35 bond was priced.

- Looking ahead, Wednesday will see the finial Judo Bank m’fing PMI print & CoreLogic house price readings, along with A$700mn of ACGB May-34 supply.

AUSTRALIA: Retail Sales Slump, Watch Q4 Real Data To Gauge Underlying Trend

Retail sales slumped 3.9% m/m in December after an upwardly revised 1.7% rise in November. This was the first fall since December 2021. This is unlikely to derail a 25bp hike in February, as there seems to be some seasonal issues around the shift to shopping during the Black Friday Sales.

- The December quarter rose 0.9% q/q after 2.5% in Q3. This is still solid and in line with Q4 2019, thus indicating that post-Covid pent up demand has probably been worked through. Going forward though we’re likely to see the impact of higher rates and prices, as discretionary inflation rose to a new high of 7.1% in Q4.

- The level of retail sales remains elevated and is up 7.5% y/y after 7.7% in November. 3-month momentum has been strong following Covid and remains positive but now stands at 3.8% annualised (November 9.9%).

- Sales were weakest in those sectors that benefited the most from Black Friday, such as department stores -14.3% m/m and clothing & footwear -13.1%. But food retailing rose another 0.3% reflecting not only higher prices but also the increase in domestic travel. There has been some shift in the post-Covid adjustment towards services spending.

- Given the extent of inflation pressures currently in the economy it will be important to monitor the real retail sales series for Q4 out on Monday to gauge spending trends in the face of monetary and cost headwinds.

Source: MNI - Market News/ABS

AUSTRALIA: ANZ Consumer Sentiment Suggests Consumer May Be More Resilient

The ANZ-Roy Morgan measure of consumer confidence rose 0.9 points in the week ending January 29 to bring the 4-week average to its highest since June 2022. It has now risen 3 of the 4 weeks recorded for January and while still depressed appears to have troughed, suggesting that consumers may be proving more resilient than expected in the face of rising rates and cost-of-living.

- Inflation expectations fell to 5.1% from 5.7% bringing the 4-week average to its lowest since end September. It is worth noting that national petrol prices fell in the survey week for the third consecutive week, which likely helped to reduce inflation expectations despite last week’s elevated inflation report.

- The improvement in confidence was broad-based with 4 of the 5 components rising and only “current economic conditions” down.

- “Time to buy a major household item” rose 1.4 points after falling 4.7 points over the previous two weeks.

Source: MNI - Market News/Refinitiv

AUSTRALIA: SEEK Advertised Salaries Post Another Solid Rise In Q4 2022

The SEEK advertised salary index for December showed a further rise in wages growth. Advertised salaries rose 0.3% m/m after 0.5% in November bringing the annual rate to 4.7% from 4.5%. It rose 1.2% q/q in Q4 in line with Q3 which saw a 5.2% increase in the national minimum wage. This data shows that the tight labour market and rising cost of living are putting upward pressure on wages, which the RBA will be monitoring closely. The official WPI series is published on February 22 and is likely to be followed by a further 25bp rate hike at the March RBA meeting.

Fig. 1: SEEK Advertised Salaries % - running ahead of pre-Covid rates

Source: MNI - Market News/SEEK

NZGBS: Off Session Cheaps

The major NZGB benchmarks cheapened by 4bp on Tuesday, with softer than expected retail sales data from across the Tasman likely allowing the space to correct from early session cheaps.

- The space generally looked through the latest cabinet reshuffle as the incumbent Labour Party looks to garner support ahead of this year’s general election, centring on new PM Hipkins putting his own mark on the ruling party post-Ardern (he named a Minister for Auckland as part of the post-flood rebuild push in the area).

- Swap rates were 2-6bp higher across the curve, with flattening apparent there, resulting in mixed swap spread performance.

- RBNZ dated OIS is showing 61bp of tightening for next month’s meeting, effectively a coin flip between a 50 or 75bp OCR hike. Meanwhile, terminal OCR pricing has edged back above 5.35%.

- Looking ahead, the latest quarterly labour market report headlines domestically on Wednesday. Unemployment is expected to hold steady at 3.3% (per the BG survey), with wage growth set to remain elevated even as Q/Q employment growth pulls back.

FOREX: USD Supported, AUD & NZD Down On Lower Equities & Commodities

The supportive USD tone has persisted through today's session. The BBDXY index is up only modestly, near +0.05% at this stage, putting the index above 1225.60. However, USD outperformance against higher beta FX has been more noticeably, with AUD and NZD both off by around 0.40% at this stage.

- The better than expected services China PMI did little to lift sentiment, with risk-off flows evident in the equity space for China and HK markets. This looks to be profit taking flows ahead of month end, with one eye also potentially on tomorrow's Fed meeting.

- AUD/USD sits at 0.7030/35 currently, off 0.40% and unwinding all of the post CPI rally we saw from Wednesday last week. The much weaker than expected Dec retail sales print weighed, with AU yields underperforming the firmer core tone. The AU-US 2yr spread is back at -112bps, versus recent highs closer to -102bps. Weaker commodity prices are also weighing, with copper and iron ore off recent highs.

- NZD/USD sits back at 0.6440/45, also around 0.40% off for the session.

- Yen has seen some outperformance, with USD/JPY close to unchanged for the session, last around 130.30/35. Japan data was mixed, while headlines from the Finance Minister didn't shift the needle from a BoJ standpoint.

- Looking ahead, preliminary euro area Q4 GDP is out and in the US Q4 employment cost index, Chicago PMI and November house prices.

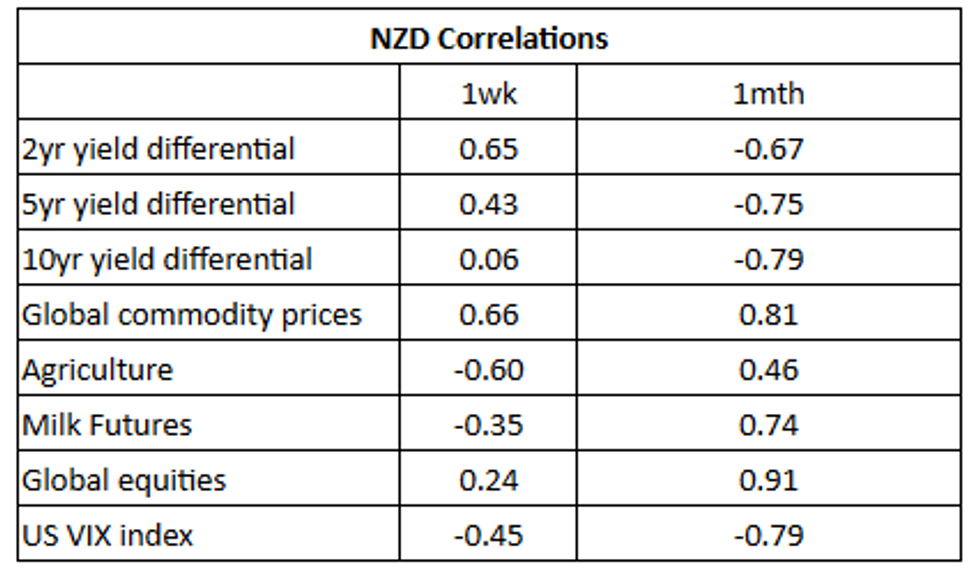

NZD: Correlation With 2-year Yields, Commodities Strengthen In Recent Trade

NZD/USD correlations with 2 year yield differentials and commodity prices have strengthened over the past week, standing out as a key macro driver in recent dealings. The table below presents levels of correlations between NZD and key macro drivers (note the yield differential reflects swap rates).

- The pair has been mostly range bound the last week, although dips are being supported. The continued recovery in commodity prices last week has helped on this front, while yield differentials are up off recent lows. The 2yr swap last around +56bps, we were at +50bps on Thursday last week.

- Through January the NZD/USD rose ~4% with strength in global equities and commodity prices, as well as an easing in the VIX all supporting the rally.

- Conversely, the recent weakness in Milk Futures hasn't weighed on the Kiwi, although the monthly correlation does remain relatively strong.

Source: Market News International (MNI)/Bloomberg

FX OPTIONS: Expiries for Jan31 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0700-25(E532mln), $1.0730-50(E591mln), $1.0850-55(E1.5bln), $1.0875-00(E1.7bln), $1.1100(E652mln)

- USD/JPY: Y127.50($500mln), Y130.00($511mln)

- USD/CAD: C$1.3400($1.2bln)

- USD/CNY: Cny6.8000($1.8bln)

ASIA FX: USD Mostly Firmer, Better China Data Has Little Impact

The bias for most USD/Asia pairs has been higher, albeit within modest ranges. TWD and PHP have seen some outperformance though. The market tone appears more cautious ahead of tomorrow's Fed meeting, with month end also potentially playing a role. Better China PMI data was largely ignored by the market. Still to come is Taiwan export orders and Thailand trade figures. Tomorrow, South Korea Jan trade figures print, along with the Caixin manufacturing PMI in China. Manufacturing PMIs are due elsewhere in the region, along with the Indian budget.

- USD/CNH has tracked recent ranges, albeit with a positive bias. The pair currently sits just above 6.7600, slightly above NY closing levels. The CNY fix was close to neutral. The PMI prints point to an improving outlook, particularly in the services sector (see this link for more details).

- 1 month USD/KRW sits little changed for the session, last around 1230. Local equities are down 0.84% at this stage, while offshore investors have turned net sellers (-$122mn in net outflows so far). IP data for Dec was weaker than expected.

- TWD continued to see some outperformance. Spot USD/TWD couldn't hold a break sub 30.00, although the 1 month NDF is already comfortably below this level, last around 29.90. This pair found some support around early Dec lows sub 29.85. Also note this pair is close to forming a death cross forming (50-day MA breaking below the 200-day MA). The firmer TWD tone looks to be a little at odds with steady CNH and KRW levels today. However, it looks to be somewhat of a catch up play. The currency has lagged the stronger ADXY tone through January.

- In Singapore, the December unemployment rate printed at 2% in line with expectations. This is the lowest unemployment rate since early 2016. The SGD NEER (per Goldman Sachs estimates) is drifting higher post the unemployment rate print, albeit a touch off last week's high. We sit ~0.5% below the upper end of the band. USD/SGD is dealing marginally firmer today, up ~0.1% today, last printing at $1.3145. Technicals remain bearish for USD/SGD.

- USD/PHP has had a modest 20pip range (54.47/54.67) so far today, last sitting just near 54.51. Note the 20-day EMA comes in at 54.87, while recent lows sit just under 54.30. The slump in local equities, down 3.00% at this stage isn't impacting FX sentiment. Equities are tracking sharply lower into month end, as the index lost 1.15% yesterday. BSP expects Jan inflation (due next Tuesday) to print between 7.5%-8.3%.

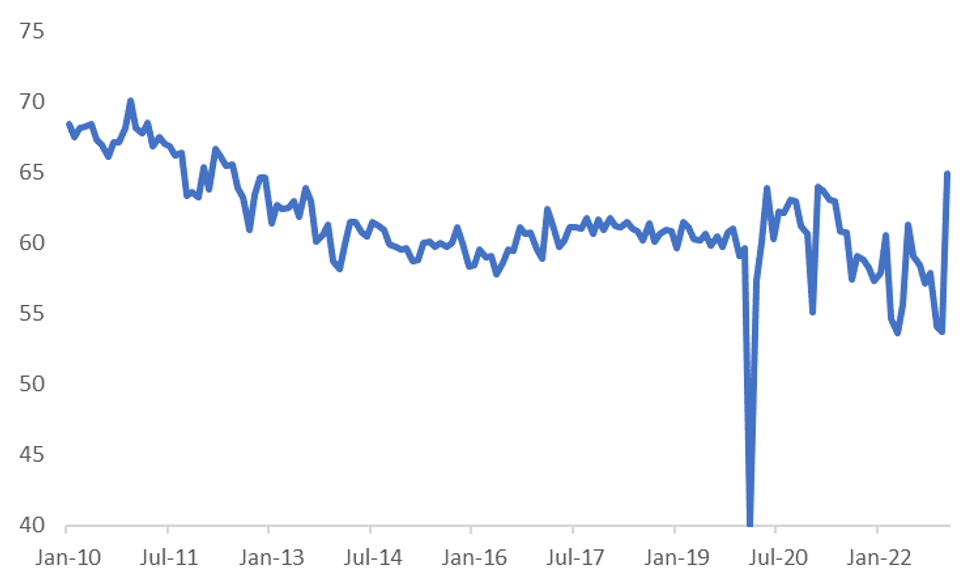

CHINA: Services PMI Beats, Business Expectations At Decade High

China's services PMI comfortably beat expectations, rising to 54.4 (versus 52.0 expected and 41.6 prior). This is the highest print since June 2022. The profile for this PMI matches what we saw in 2022 in terms of a sharp rebound post the end of the Shanghai lockdown, the market will be hoping for a more sustained recovery through 2023.

- The detail showed fairly uniform improvement across the sub-indices. Employment and new export orders remain in contraction territory though (46.7 & 45.9 respectively). The headline new orders index surged to 52.5 from 39.1, while the business activities expectation index rose to 64.9, which is fresh highs back to 2012, see the chart below.

- The manufacturing PMI met expectations, rising to 50.1, the prior month was 47.0. New orders were back to 50.9, highs back to the mid 2021. New export orders and the employment sub-indices remained comfortably below the 50.0 expansion/contraction point.

- Elsewhere, Dec industrial profits slipped to -4.0% YTD y/y, versus -3.6%.

- The IMF also upgraded the 2023 GDP outlook for China to 5.2% (from 4.4%). Note the consensus sits at 5.1%.

Fig 1: China Non-Manufacturing PMI Business Expectations Index

Source: MNI - Market News/Bloomberg

MACRO: Global Trade Flows Clearly Slowing

MNI (Australia): The November CPB world trade data are showing a clear slowdown is now in place. Global trade volumes fell 2.5% m/m after -1.4% in October to be down 1.5% y/y, the first contraction in just over two years. With momentum also clearly negative, the slowdown has more to go.

- Global export volumes fell 3% m/m to be down 1.6% y/y. Exports from emerging economies have been weaker than for developed countries at -3.7% y/y compared with -0.4%, driven by weakness in China (-10.2% y/y), which should now rebound somewhat following the end of lockdowns.

- Global IP fell for the second consecutive month in November and is now up 1.5% y/y after 3.1% last month, but 3-month momentum has turned negative. Metals prices appear to have troughed indicating that the turndown in global output may be shallow, however the global manufacturing PMI is yet to stabilise.

- Global trade prices rose 1.2% m/m in November after falling 1.9% the previous month with 3-month momentum very negative at -15.2% annualised. Energy prices are down 21% 3m/3m average annualised (up 25.1% y/y), and non-energy raw material prices are down 29.3%, which is good news for the inflation outlook.

Source: MNI - Market News/Refinitiv/CPB/Bloomberg

Fig. 2: Exports y/y%

Source: MNI - Market News/CPB

EQUITIES: Ending January On A Weaker Note

The regional tone to Asia Pac equities is a weaker one for Tuesday's session. The weaker lead from Wall St through Monday's session didn't help, while China/HK sentiment didn't get a lift from better PMI outcomes, particularly in the services sector. US futures are also lower, failing to hold early positive momentum. Weakness is most evident in the Nasdaq, off -0.35% at this stage.

- HK and China bourses look to be seeing a bout of profit-taking. The HSI is off by near 1.30% so far today, with the tech sub-index down by 1.70% after yesterday's 4.84% fall. The China Dragon index was also down sharply in Monday US trade, -4.1%. Still, the HSI is up 10.15% for the whole of the month.

- The CSI 300 is down by 0.80%, more than unwinding Monday's +0.47% gain. The official services PMI surged to 54.4 (versus 52.0 expected). The detail also suggest further improvement in the outlook. The result didn't drive better sentiment in the equity space.

- The Kospi is off by 0.70% at this stage. A weaker than expected earnings update from Samsung electronics didn't help, while offshore investors have sold around $115mn of local shares today. The Taiex is off by over 1.10%, which comes after yesterday's +3.8% gain and where offshore investors added +$2.5bn to local stocks.

- Philippine shares also continue to track lower into month end, down nearly 4% over the past two sessions (2.8% today). Indian shares also remain on the back foot (Sensex -0.40% at the moment).

GOLD: Bullion In Holding Pattern Ahead Of Fed Meeting

Gold prices have been trading in a tight range during the APAC session ahead of Wednesday’s FOMC meeting. They fell 0.2% on Monday, and are now down 0.1% from the NY close at $1921.30/oz and is close to the intraday low of $1920.91 after reaching a high of $1927.43. The USD fell earlier in the session and is now climbing back up and weighing on gold prices.

- Gold continues to trade between its resistance at $1949.20, January 26 high, and support at $1897, the 20-day EMA.

OIL: Crude Down Again As Waits For Fed And OPEC Outcomes

Oil prices are lower again today after falling 2.4% on Monday, despite positive China data. WTI is down another 0.4% during the APAC session and is currently trading around its intraday low at $77.60/bbl after reaching an intraday high of $78.14. Brent is at $84.85/bbl.

- WTI is around its 50-day simple moving average and Brent its 100-day. WTI broke through support of $78.45 and the next level to watch is $72.74, the January 5 low, and for Brent watch $82.37, the January 12 low. This month global growth fears have outweighed the improved China demand outlook but there is optimism with money managers building net-long Brent positions to their largest in 11 months (bbg).

- US API inventory data are released today, which have recently been showing rising crude stocks. But Bloomberg reported that there could be a gasoline shortage over much of the US East Coast during the summer driving season due to the EU ban on Russian oil products possibly impacting US supplies. Russia has also banned sales of crude to any countries applying the price cap.

- OPEC+ meets Wednesday.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 31/01/2023 | 0630/0730 | ** |  | FR | Consumer Spending |

| 31/01/2023 | 0630/0730 | *** | | FR | GDP (p) |

| 31/01/2023 | 0700/0800 | ** |  | DE | Retail Sales |

| 31/01/2023 | 0730/0830 | ** |  | CH | retail sales |

| 31/01/2023 | 0745/0845 | *** | | FR | HICP (p) |

| 31/01/2023 | 0745/0845 | ** | | FR | PPI |

| 31/01/2023 | 0855/0955 | ** | | DE | Unemployment |

| 31/01/2023 | 0930/0930 | ** |  | UK | BOE M4 |

| 31/01/2023 | 0930/0930 | ** | | UK | BOE Lending to Individuals |

| 31/01/2023 | 1000/1100 | *** |  | IT | GDP (p) |

| 31/01/2023 | 1000/1100 | *** |  | EU | EMU Preliminary Flash GDP Q/Q |

| 31/01/2023 | 1000/1100 | *** | | EU | EMU Preliminary Flash GDP Y/Y |

| 31/01/2023 | 1300/1400 | *** | | DE | HICP (p) |

| 31/01/2023 | 1330/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 31/01/2023 | 1330/0830 | ** |  | US | Employment Cost Index |

| 31/01/2023 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 31/01/2023 | 1400/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 31/01/2023 | 1400/0900 | ** | | US | FHFA Home Price Index |

| 31/01/2023 | 1445/0945 | ** | | US | MNI Chicago PMI |

| 31/01/2023 | 1500/1000 | *** | | US | Conference Board Consumer Confidence |

| 31/01/2023 | 1500/1000 | ** | | US | housing vacancies |

| 31/01/2023 | 1530/1030 | ** | | US | Dallas Fed Services Survey |

| 01/02/2023 | 2200/0900 | ** |  | AU | IHS Markit Manufacturing PMI (f) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.