Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

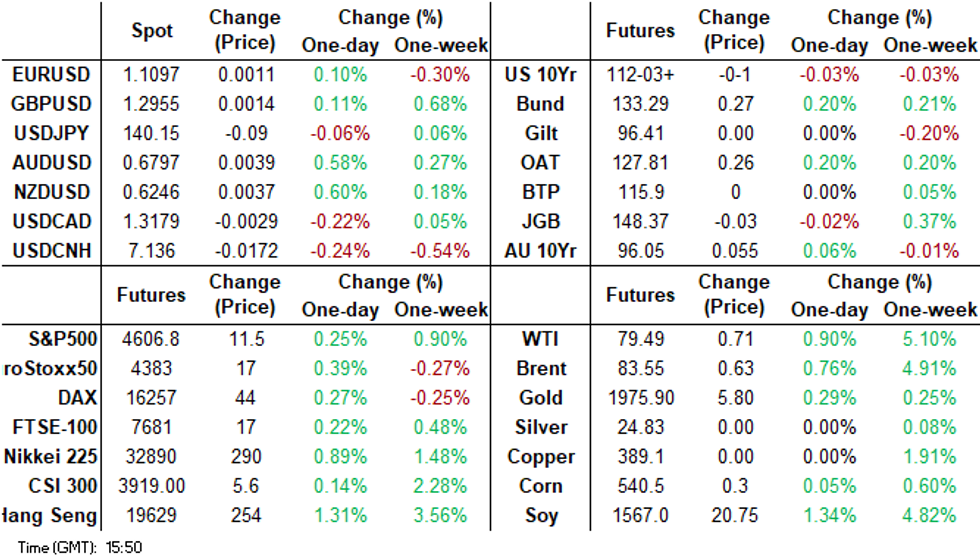

- Risk sentiment improved in Asia as participants digested yesterday's FOMC rate decision and Fed Chair Powell's press conference. US cash tsys sit 0.5-3bps richer across the major benchmarks, the curve has bull steepened.

- US equity futures are higher, albeit down from session highs, likewise for regional equities in Asia Pac. The USD is lower, but has re-couped some losses, most notably in terms of USD/JPY. This pair got to 139.35/40 but now sits back above 140.00. No policy changes are expected at tomorrow's BoJ policy announcement. Higher beta FX has outperformed.

- The latest monetary policy decision from the ECB headlines in Europe today (+25bps expected). Further out we have US GDP, durable goods orders, initial jobless claims and wholesale inventories.

MARKETS

ECB: MNI ECB Preview - Another 25bp Hike in July. September Remains Open

- The ECB will almost certainly hike by 25bp this week after President Lagarde guided markets to another hike at the June meeting. Although economic activity data has recently weakened and several policymakers have highlighted the lagged impact on the economy of previous policy rate hikes, the labour market remains tight and inflation is still someway from target.

- On balance, there is little to suggest that the ECB would feel compelled to ratchet up the hiking pace, or hit the pause button – both of which represent risk scenarios for this meeting that would be major market moving events.

- Full preview including summary of sell-side views here: https://roar-assets-auto.rbl.ms/files/54853/ECB%20...

US TSYS: Marginally Richer In Asia

TYU3 deals at 112-02, -0-02+, a 0-09 range has been observed on volume of ~80k.

- Cash tsys sit 0.5-3bps richer across the major benchmarks, the curve has bull steepened.

- Tsys firmed off session lows as risk sentiment improved in Asia as participants digested yesterday FOMC rate decision and Fed Chair Powell's press conference.

- The move in Tsys was seen alongside pressure on the USD, BBDXY is down ~0.2%, and US Equity Futures and Regional Equities moving higher.

- Tsys dealt in narrow ranges with little follow through for the remainder of the session.

- FOMC dated OIS remains stable, a ~5.4% terminal rate is seen in November with ~60 bps of cuts to June 2024.

- The latest monetary policy decision from the ECB headlines in Europe today. Further out we have US GDP, durable goods orders, initial jobless claims and wholesale inventories. The latest 7-Year Supply is also due.

STIR: $-Bloc Markets Are Softer Following FOMC Decision, AU Leading After Q2 CPI

After the Federal Reserve's widely anticipated decision to raise the funds rate to a range of 5.25% to 5.50%, terminal rate expectations for $-Bloc currencies have eased.

- Notably, Australia has been the outperformer, with its terminal rate softening by 12bp to 4.33% following the release of lower-than-expected Q2 inflation data yesterday.

Figure 1: $-Bloc STIR: Terminal Rate Expectations & Mar’24 Pricing

Source: MNI – Market News / Bloomberg

JGBS: Futures Holding Weaker, Tokyo CPI & BoJ Policy Decision Tomorrow

In the Tokyo afternoon, JGB futures are holding slightly weaker, -6 compared to the settlement levels, after paring overnight losses.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined international investment flow data.

- The move away from session lows has been assisted by an extension of the post-FOMC rally in US tsys in Asia-Pac trade.

- The cash JGB curve has twist flattened, pivoting at the 4-year zone, with yields +0.2bp to -2.2bp. The benchmark 10-year yield is 0.4bp lower at 0.451%, below BoJ's YCC limit of 0.50%.

- The 2-year is underperforming on the curve at -0.039% despite today’s 2-year auction showing solid demand.

- The swaps curve has bull flattened with rates 0.2bp to 2.0bp lower. Swap spreads are mixed.

- Tomorrow the local calendar sees July Tokyo CPI data along with the BoJ Policy Meeting Decision. Our analysis aligns with the prevailing consensus, which anticipates that the current easing policies will be maintained during this week's meeting. Market expectations also appear fairly low, with the 10yr JGB yield below the upper bound of the -/+0.50% permissible range, while the 10-yr Swap/JGB spread (which can be thought of as a proxy for BoJ YCC tweak speculation) sits around +15bps currently, not too far off multi-month lows going back to last August 2022. (See MNI BoJ Preview here)

BOJ: MNI BoJ Preview - July 2023: Holding Steady, Inflation Outlook Key

EXECUTIVE SUMMARY

- Our analysis aligns with the prevailing consensus, which anticipates that the current easing policies will be maintained during this week's meeting. Market expectations also appear fairly low, with the 10yr JGB yield below the upper bound of the -/+0.50% permissible range, while the 10-yr Swap/JGB spread (which can be thought of as a proxy for BoJ YCC tweak speculation) sits around +15bps currently, not too far off multi-month lows going back to last August 2022.

- This is likely to leave the focus on the inflation outlook. The FY23 forecasts are widely expected to be upgraded, but there is less certainty as to how the FY 24 and FY 25 forecasts evolve.

- October is seen as the more likely window, according to economics consensus for a YCC shift. It's important to consider that BoJ officials have acknowledged their reluctance to signal the timing of any policy changes in advance. Hence, if the BoJ were to surprise the market, we believe it could take one of two possible actions: either widen the trading band around the 10-year target of 0% or shorten the tenor of the YCC target to 2-5-year JGBs. While both scenarios are possible, we assign a higher probability to the latter.

- Full preview here:

AUSSIE BONDS: Richer, Near Session Highs, Retail Sales Tomorrow

ACGBs (YM +6.0 & XM +5.0) are dealing near session highs, adding to yesterday’s post-CPI rally. At current levels, ACGB futures are 10-13bp higher than pre-CPI levels. Other than the previously flagged weaker-than-expected Q2 terms of trade data, there haven’t been any domestic drivers of note.

- Today’s local session strength has been assisted by an extension of the post-FOMC rally in US tsys in Asia-Pac trade. US tsys sit 0.5-3bps richer across the major benchmarks.

- Cash ACGBs are 6-7bp richer with the AU-US 10-year yield differential -3bp at +10bp.

- Swap rates are 6-7bp lower with EFPs little changed.

- The bills strip bull flattens with pricing +1 to +7.

- RBA-dated OIS pricing is 2-6bp softer for meetings beyond October. A 27% chance of a 25bp hike in August is priced. The expected terminal rate sits at 4.31% versus 4.45% ahead of the CPI data.

- Tomorrow the local calendar sees Q2 PPI data along with June Retail Sales.

- The latest monetary policy decision from the ECB headlines in Europe today.

- With Fed Chair Powell emphasising data dependency, today's US calendar sees Q2 GDP, durable goods orders, initial jobless claims and wholesale inventories, ahead of Friday's Q2 ECI and monthly PCE reports.

- Tomorrow the AOFM plans to sell A$700mn of 4.50% 21 April 2033 bond.

NZGBS: Richer But Underperforms $-Bloc, Consumer Sentiment Data Tomorrow

Short to mid-curve NZGBs closed richer, but off session bests, with benchmark yields 1-3bp lower and the curve steeper. The 10-year benchmark closed 1bp cheaper.

- Although there were no significant domestic factors at play, the local market experienced strength during the session, likely due to an extension of the post-FOMC rally in US tsys and ACGBs in the Asia-Pac trade. The local market's gains were further supported by robust demand witnessed at the weekly auction, evident from cover ratios ranging from 3.35x to 4.00x.

- Despite the overall positive performance, NZGBs underperformed their counterparts in the $-Bloc. The NZ-US and NZ-AU 10-year yield differentials respectively 4bp and 5bp wider at +79bp and +64bp.

- Swap rates closed 3-4bp lower.

- RBNZ dated OIS closed with pricing flat to 3bp softer across meetings with Jul’24 leading.

- Tomorrow the local calendar sees ANZ Consumer Confidence.

- With Powell emphasising data dependency, later today sees an important US docket with the 1st release for Q2 GDP, preliminary durable goods for July, jobless claims and other second-tier releases (along of course with the ECB decision) before Friday's Q2 ECI and monthly PCE reports.

EQUITIES: Eminis Threatening Break Higher, March 2022 Levels Within Sight

Regional equities have mostly tracked higher today. Spillover has been evident from higher US equity futures, which has aided broader risk appetite in the region. At this stage, Eminis are around +0.30% higher, last in the 4609/10 region. This is right on fresh highs going back to March last year. Nasdaq futures are outperforming amid a softer US yield backdrop post the FOMC. The Sep contract is up 0.65% at the time of writing.

- China related markets have also performed well. The HSI is up 1.36% at the break, with the tech sub index now 20% above May's trough point. Today the HSTECH is up nearly 3%.

- On the mainland the CSI 300 is up 0.54%, with the real estate sub index +0.77%. Onshore analysts expect housing restrictions to be relaxed in H2, with renewed confidence in this outlook post the Politburo meeting at the start of the week.

- Japan stocks are firmer, with the Topix near +0.50%, the Nikkei 225 +0.75%. The yen was firmer in early trade, but is away from best levels. No policy changes are expected at tomorrow's BoJ meeting.

- The Kospi is +0.70%, but the Kosdaq has continued to retrace, down a further -0.80%, after yesterday's ~4% fall on valuation concerns for EV battery related companies. The BoK has boosted liquidity support for the banking sector.

- In SEA, gains are more modest, while Philippines and Thai equities are tracking weaker.

FOREX: USD Pressured In Asia

The greenback has been pressured in Asia today after yesterday's FOMC rate decision and press conference as Fed Chair Powell noted that any further hikes are data dependent. The Antipodeans are leading the bid, BBDXY is down ~0.2%.

- Kiwi is the strongest performer in the G-10 space at the margins. NZD/USD last prints at $0.6255/60 and is up ~0.8%. The pair has cleared its 200-Day EMA ($0.6229) in Asia and sits at its highest level since 20 July.

- AUD/USD is up ~0.7%, the pair last prints at $0.6805/10. Resistance comes in at $0.6847 (high from Jul 20) and $0.69 (high from June 16).

- Yen is ~0.3% firmer, USD/JPY has breached the ¥140 handle and last prints at ¥139.75/85. The pair found support below ¥139.75, the low from July 21, and losses have been marginally pared.

- Elsewhere in G-10, EUR and GBP are ~0.1% firmer. NOK and SEK are both up ~0.4% however liquidity is generally poor in the Asian session.

- Cross asset wise; E-minis are up ~0.3% and the Hang Seng is up 1.3%. US Tsy Yields have ticked lower, the 2 Year Yield is down ~3bps.

- The highlight of today's docket is the ECB monetary policy decision. We also have a slew of US data due including GDP, durable goods orders, initial jobless claims and wholesale inventories.

OIL: Rebounds, Offsetting Wednesday's Fall

Brent crude has tracked higher through Asia Pac trade, last near $83.70/bbl. We are threatening to push to fresh highs, with July 25 highs very close by. At this stage Brent is ~1% higher, more than offsetting Wednesday's -0.86% fall. We are tracking comfortably higher over the past week. WTI was last close to $79.70/bbl, up by a similar amount for the session.

- Broader risk appetite has been supported today post Wednesday's Fed outcome. US yields are lower, the dollar offered, while regional equities are tracking higher. This has spilled over to oil, with other commodities also pushing higher.

- This comes after Wednesday data showed weekly EIA petroleum data pointing to a smaller than expected crude draw with an unexpected drop in refinery utilisation.

- Saudi Arabia is also expected to extend the 1mbpd oil supply cut again into September according to a Bloomberg survey. 15 of 22 traders, analysts and refiners surveyed by Bloomberg predict it will continue into September.

- For Brent, mid April levels around $85.50/bbl could be targeted on a further upside push. Beyond that lies April highs close to $87.50/bbl. On the downside, the 200-day EMA comes in at $82.30/bbl.

GOLD: Stronger As Fears Of Further Fed Hikes Fade

Gold is +0.3% in the Asia-Pac session, after closing stronger (+0.4%) on Wednesday as traders priced in lower odds of further US monetary tightening in September after the Federal Reserve raised rates to a 5.25-5.50% range, the highest level in 22 years.

- Front-end US tsys finished 6bp richer than just before the FOMC statement to be 2bp lower in yield on the day. The presser leaned slightly dovish with reiteration of signs of progress for instance in labour market balance and noted the potential impact of tighter credit conditions. Higher rates are typically negative for bullion, which doesn’t yield any interest.

- The USD dropped alongside lower 2-year US tsy yield.

- According to MNI’s technicals team, resistance remains at the bull trigger of $1987.5 (Jul 20 high).

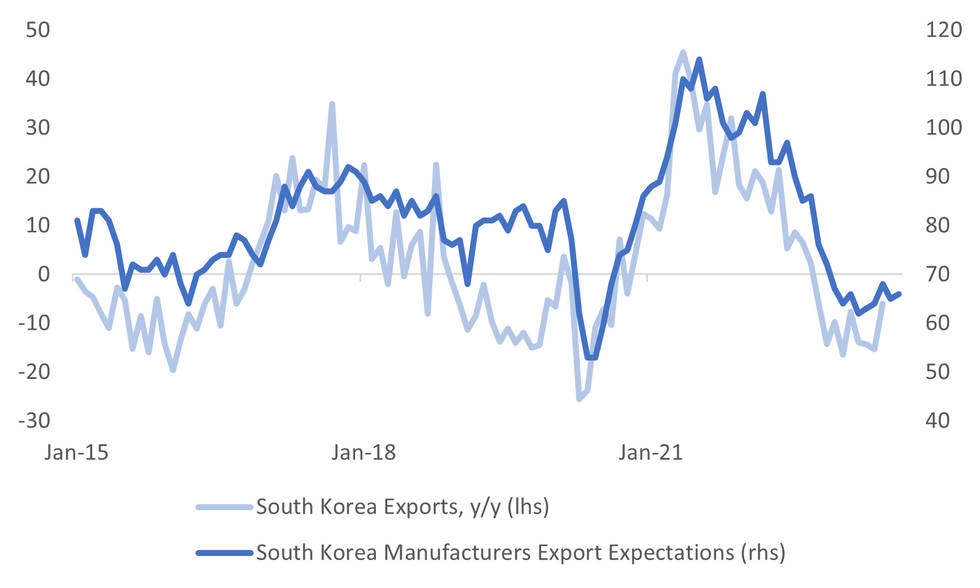

SOUTH KOREA: Business Sentiment Moderates, Export Expectations Hold Steady

The recent recovery in manufacturing sentiment has stalled in recent months. The BoK survey for the sector dipping to 69 from 72 for the headline August print. The chart below shows the headline index is still above Q1 lows, but is still fairly depressed from an historical standpoint. If current levels continue to hold, it suggests only a modest uplift in y/y GDP growth momentum. Earlier in the week we had the Q2 GDP update, which showed 0.9% y/y growth, which was slightly better than forecast.

- The detail showed a pull back across expected domestic sales and new orders also slipped. Most indices remain within recent ranges though. The seasonally adjusted reading for the manufacturing sector rose to 71 from 69, a slightly more positive result, but is only back to levels that prevailed at the start of the year.

- Profit expectations also slipped, back to 76 from 81.

Fig 1: South Korean Manufacturing Sentiment & South Korean Y/Y GDP

Source: MNI - Market News/Bloomberg/BoK

- Manufacturers export expectations firmed a touch, but at 66 remains well within recent ranges. The second chart below overlays these expectations against y/y export growth. Again, it isn't suggesting a sharp rebound in export growth. Next Tuesday delivers July trade data.

- On the non-manufacturing side, sentiment also eased to 76 from 78 prior. This unwinds some of the recent improvement in the series, but we remain above Q1 lows of 70 for the sentiment gauge.

Fig 1: South Korean Manufacturers Export Forecast & South Korean Exports Y/Y

Source: MNI - Market News/Bloomberg/BoK

MALAYSIA: PM Anwar Unveils Plan To Reset Economic Trajectory

Malaysian PM Anwar has unveiled a plan to reset the economy's growth trajectory whilst boosting incomes and participation of women in the workforce. The key goals are for Malaysia to be among the top 30 global economies in the next 10 years and improve its human development index ranking to the top 25.

- Anwar's plan outlined a goal to reduce the fiscal gap to 3% of GDP and boost economic growth to 6% in the short term. The government expects Malaysia to grow at 4%-5% in 2023.

- Also included in the plan is that adults earning below MYR100k will get MYR100 e-cash credits, digitalisation will be boosted with a MYR100mn grant and MYR100mn will be set aside for infrastructure. More here.

ASIA FX: USD/Asia Pairs Lower But Away From Best Levels

USD/Asia pairs are lower but away from best levels. USD/CNH got to fresh multi-week lows but has recovered some ground. 1 month USD/KRW is also higher, weighed by weaker small cap equities and higher USD/JPY levels. MYR and THB have outperformed though. For Malaysia, PM Anwar has unveiled a plan to reset the economy's growth trajectory. Tomorrow delivers South Korea IP, along with Q2 GDP in Taiwan.

- USD/CNH got to fresh lows of 7.1161 post the stronger CNY fixing and a buoyant equity risk mood. June industrial profits were -8.3% y/y, versus -12.6% prior. With USD/JPY recovering this afternoon though, USD/CNH has pared earlier losses. We sit back at 7.1370/80 currently, still around 0.20% stronger in CNH terms for the session.

- 1 month USD/KRW hasn't been able to sustain lows sub 1270. We sit back at the 1275/76 level currently. This is -0.50% weaker in won terms for the session so far. Weakness in the Kosdaq equity index, down a further 1.2% may be weighing at the margin, with valuation concerns continuing in the battery EV space. Higher USD/JPY levels (back to a 140.00 handle) have likely weighed as well. Earlier business sentiment readings for August moderated. The BoK also tweaked its lending facility to boost liquidity.

- USD/THB sits a touch above session lows in latest dealings, last in the 34.05/10 region. This is +0.50% from a baht standpoint and a continuation of yesterday's downtrend in the pair. Some catch up to USD weakness against the majors post yesterday's onshore spot close is another positive. On the political front - "The Constitutional Court will consider next Thursday whether it will accept for deliberation a petition regarding the renomination of Move Forward Party (MFP) leader Pita Limjaroenrat as prime minister" per the Bangkok post. IP growth for June was slightly weaker than expected at -5.24%y/y, -3.00% forecast).

- The rupee is little changed in early trade, the Rupee is lagging in the USD/Asia space as broader USD weakness dominates on Thursday. The Bloomberg Asia Dollar Index is up ~0.3%. USD/INR sits a touch above the 82 handle. Strong equity inflows have continued with $348.96mn on Tuesday, inflows for July now total $3.891bn.

- The Ringgit is firmer in early dealing as broader USD trends, which have seen the greenback weaken in Asia after yesterday's FOMC meeting, dominate flows. USD/MYR is down ~0.5% and last prints at 4.5250/70. The pair sits a touch off month to date lows and is at its lowest level since 14 July. Malaysian PM Anwar has unveiled a plan to reset the economy's growth trajectory whilst boosting incomes and participation of women in the workforce. The key goals are for Malaysia to be among the top 30 global economies in the next 10 years and improve its human development index ranking to the top 25.

- The SGD NEER (per Goldman Sachs estimates) is little changed in early dealing, the measure sits a touch off cycle highs and is ~0.2% below the top of the band. Broader USD trends are dominating in Asia, the greenback has been pressured after yesterday's FOMC rate decision and press conference. USD/SGD is down ~0.2% and sits at its lowest level since 18 July. The pair last prints at $1.3215/25. The Unemployment rate ticked higher to 1.9% from 1.8% in June, the uptick in unemployment has been expected.

- USD/IDR has drifted back sub 15000 on the back of broader USD weakness. Still, this is lagging broader Asia FX trends and higher beta FX, which have seen stronger gains against the USD. IDR has lagged the generally softer USD trend over the past month. Along with TWD, they are the only Asia FX currencies not to have risen against the USD (although INR gains are only very modest). Current USD/IDR levels leaves us within recent ranges. EMA levels are clustered nearby. On the topside is the 200-day at 15040, on the downside is the 50-day at 14985. A weak US yield backdrop should aid the rupiah all else equal and enable some catch up with softer USD trends.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 27/07/2023 | 0600/0800 | * |  | DE | GFK Consumer Climate |

| 27/07/2023 | 0700/0900 | ** |  | SE | Economic Tendency Indicator |

| 27/07/2023 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 27/07/2023 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 27/07/2023 | 1000/1100 | ** |  | UK | CBI Distributive Trades |

| 27/07/2023 | 1145/1345 | *** |  | EU | ECB Marginal Lending Rate |

| 27/07/2023 | 1215/1415 | *** | | EU | ECB Deposit Rate |

| 27/07/2023 | 1215/1415 | *** | | EU | ECB Main Refi Rate |

| 27/07/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 27/07/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 27/07/2023 | 1230/0830 | * |  | CA | Payroll employment |

| 27/07/2023 | 1230/0830 | ** | | US | Durable Goods New Orders |

| 27/07/2023 | 1230/0830 | *** | | US | GDP |

| 27/07/2023 | 1230/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 27/07/2023 | 1245/1445 | | EU | ECB President Lagarde post-rate meet press conference | |

| 27/07/2023 | 1400/1000 | ** | | US | NAR Pending Home Sales |

| 27/07/2023 | 1400/1000 | ** | | US | Kansas City Fed Manufacturing Index |

| 27/07/2023 | 1415/1615 | | EU | ECB Lagarde speaks on the ECB Podcast | |

| 27/07/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 27/07/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 27/07/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 27/07/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

| 27/07/2023 | 1700/1300 | | US | Fed proposal on capital |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.