Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

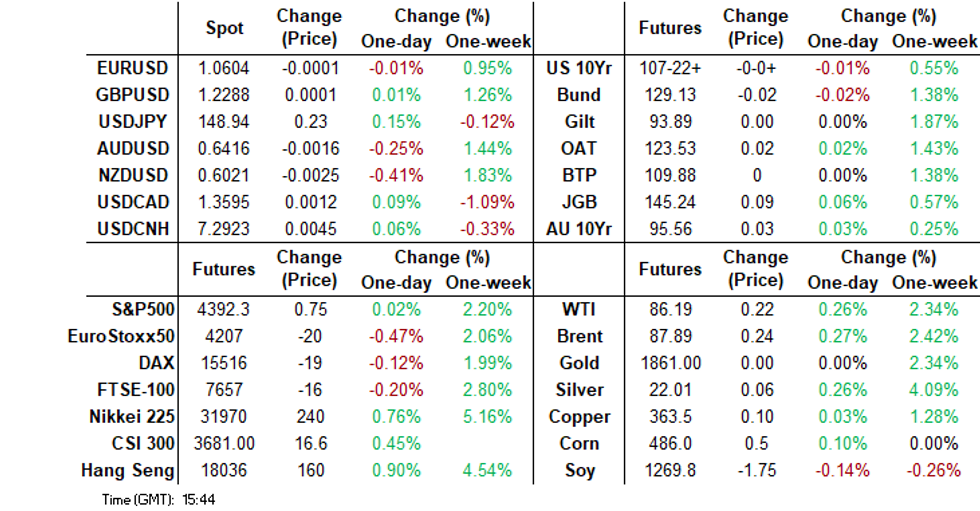

- US cash tsys sit 2bps cheaper to 4bps richer across the major benchmarks, the cure has twist flattened pivoting on 7s. Early in today's session SF Fed President Daly noted the neutral rate of interest could be higher than pre-pandemic. USD FX indices sit close to unchanged, although AUD and NZD have underperformed somewhat.

- Regional equity sentiment has been mostly positive, led by tech sensitive plays. This has dragged USD/Asia pairs lower, but USD/CNH has remained steady.

- Elsewhere, the IMF published its updated World Economic Outlook from Morocco on Tuesday. It painted a picture of soft but not collapsing growth but with inflation remaining “uncomfortably high”, see below for more details.

- Looking ahead, in Europe today we have the final read of September CPI from Germany, and ECB 1- and 3-Year Inflation Expectations for August. Later the Fed’s Bowman, Waller, Bostic and Collins speak plus the September Fed minutes are released. On the data front, US September PPI is released. The ECB’s Lagarde and Panetta will attend the IMF/World Bank annual meetings.

MARKETS

GLOBAL: IMF Sees Growth “Limping Along, Not Sprinting”

The IMF published its updated World Economic Outlook from Morocco on Tuesday. It painted a picture of soft but not collapsing growth but with inflation remaining “uncomfortably high”. IMF Director Research Gourinchas said “the global economy is limping along, not sprinting”. Global growth projections were unchanged from July for 2023 but down for 2024 but they hide significant variations.

- Risks to growth remain skewed to the downside but “some of the extreme risks have moderated since April”. China, oil prices, climate, geopolitics, and impact of further greenback strengthening on EM capital outflows remain concerns.

- Global growth was left at 3% this year down from 3.5% in 2022 but down 0.1pp to 2.9% next year. Gourinchas noted that the “slowdown is more pronounced” in advanced than developing countries with the latter expected to grow only 1.5% in 2023 and 1.4% in 2024 compared with 4% for both years in EM.

- Developed market growth was unrevised and while there were upward revisions to the US of around 0.4pp in both years to 2.1% and 1.5%, the euro area was revised down 0.2pp to 0.7% and 0.3pp to 1.2% due to sharp revisions in Germany, Italy and Spain. German growth is expected to contract 0.5% this year. The US was chastised for its procyclical fiscal policy.

- While developing country growth forecasts were also little changed, they were equally mixed with China and Africa seeing downward revisions, whereas Latin America and Russia were revised higher. The IMF noted that China is “facing growing headwinds” particularly from its property sector problems. GDP was revised down around a quarter point in both 2023 and 2024 to 5% and 4.2% respectively. The 0.2pp upward revision to India for 2023 helped reduce the impact on emerging Asia with forecasts down -0.1pp to 5.2% and -0.2pp to 4.8% respectively.

Source: MNI - Market News/IMF/World Bank/OECD

GLOBAL: IMF Tells Central Banks To “Avoid Premature Easing”

While global growth remains lacklustre, inflation remains too high and the IMF warned in its October World Economic Outlook that most countries won’t return to their inflation targets until 2025. They noted that inflation expectations need to come down. It still expects that inflation can fall to target while still ensuring a soft landing, but it warned central banks to “avoid premature easing” and noted that they still had more to do.

- Global inflation has been revised up 0.1pp to 6.9% in 2023 down from 8.7% last year and by 0.6pp to 5.8% in 2024, due to higher core inflation expectations. Global core CPI should ease to 6.3% this year (+0.3pp) from 6.4% last year and then to 5.3% (+0.6pp) in 2024, with the changes a bit misleading as they were due to upward revisions to Turkey. Core is generally proving more persistent though across countries due to tight labour markets and elevated services inflation.

- The increase in 2024 headline CPI expectations was driven by slower than thought disinflation in developing economies with inflation now expected to be 1pp higher at 7.8% up from 8.5% this year. 2024 OECD CPI was revised 0.2pp to 3% after 4.6% in 2023.

- See IMF World Economic Outlook here.

Source: MNI - Market News/Refinitiv

US TSYS: Curve Flattens In Asia

TYZ3 deals at 107-24, +0-01, a 0-06+ range was observed on volume of ~67k.

- Cash tsys sit 2bps cheaper to 4bps richer across the major benchmarks, the cure has twist flattened pivoting on 7s.

- Ranges were relatively narrow in today's Asian session, the early move higher was unwound in the short end of the curve as local participants perhaps used the opportunity to close long positions/add fresh shorts.

- The highlight flow was a FV (11,950 lots) - US (3,850 lots) flattener.

- Early in today's session SF Fed President Daly noted the neutral rate of interest could be higher than pre-pandemic.

- The docket is light in Europe today, further out we have PPI and the minutes of the September FOMC meeting. Fedspeak from Gov Bowman, Gov Waller and Atlanta Fed President Bostic is also due. The latest 10-Year Supply is also due.

JGBS: Futures Richer & At Session Highs, 5Y Supply Digestion Adequate

In afternoon dealings, JGB futures are sitting near Tokyo session highs, +9 compared to settlement levels.

- Today the local calendar has been light, with Machine Tool Orders due later today.

- Hence, local participants have likely been on headlines and US Tsys watch. Cash US Tsys are 3bps cheaper to 3bps richer in Asia-Pac dealings, with the curve flatter.

- Cash JGBs are mixed, with yield movements bounded by +0.2bp (1-year) to -2.5bps (30-year). The benchmark 10-year yield is 1.0bps lower at 0.773%. It is also lower than the cycle high of 0.814% set late last week.

- The 5-year JGB yield is 0.4bp lower at 0.311%, after today’s supply. Today's supply saw only adequate demand, with the low price meeting dealer expectations. The cover ratio of 4.056x was lower than the 4.415x recorded at the previous month's auction. However, it is worth noting that today's cover was the third highest for a 5-year auction in the past 12 months.

- The swaps curve has bull-flattened, with rates 0.4bp to 4.2bps lower. Swap spreads are tighter.

- Tomorrow the local calendar sees PPI, Core Machine Orders, Bank Lending Incl Trusts and Tokyo Avg Office Vacancies data. BOJ Board Member Noguchi is also due to give a speech in Niigata.

AUSSIE BONDS: Twist Flattening Of the Curve Remains, Household Spending Holds Up

The ACGB futures curve (YM -2.0 & XM +3.0) has twist-flattened further in Sydney’s afternoon.

- CBA’s household spending insights (HSI) for September showed that consumption is holding up in value terms with Q3 seeing stronger growth than Q2 as consumers continue to spend savings and labour income remains robust. However, the HSI suggests that spending volumes are still contracting. It has a very high correlation with the ABS retail sales data and suggests a small rise for September.

- The RBA Assistant Governor Kent spoke today on the “Channels of Transmission”. His comments on the central bank’s monetary stance were consistent with the latest meeting statement including that “some further tightening” may be needed and the RBA remains very data-dependent.

- Cash ACGBs are 2bps cheaper to 3bps richer, with the AU-US 10-year yield differential 3bps lower at -21bps.

- Swap rates are flat to 5bps lower, with the 3s10s curve flatter.

- Bills strip pricing is flat to -2.

- RBA-dated OIS pricing is little changed across meetings.

- (AFR) Australians devote a greater share of their income to mortgage repayments than any other advanced economy, the IMF has revealed, as it downgraded its forecasts for the local economy and warned inflation will be higher than previously thought. (See link)

- Tomorrow, the local calendar sees Consumer Inflation Expectations data.

RBA: RBA Very Data Dependent While Uncertainty So High

The RBA Assistant Governor Kent has spoken on the “Channels of Transmission”. He gave details on how monetary tightening feeds through to the economy. His comments on the central bank’s monetary stance were consistent with the latest meeting statement including that “some further tightening” may be needed and the RBA remains very data dependent.

- The 400bp increase in the OCR has fed through into not just mortgage rates but also business rates, funding costs and 3m BBSW rates. Around 75% has been passed on to deposit rates, higher than many other countries.

- Kent reiterated that monetary policy is working and that there are currently wide bands of uncertainty. The bank is hearing that retailers are discounting due to slower demand. It will only become concerned about higher oil prices if they persist and feed into inflation expectations.

- The RBA estimates that “the 4 percentage point increase in the cash rate target since May 2022 will have reduced overall household spending by around 0.4–0.8 per cent per year through the cash-flow channel” and that business capex would be 4% lower than baseline over 2-3 years.

- Australia’s cash flow channel works faster than other countries, such as the US, due to a higher share of variable rate loans. Since May 2022, household mortgage payments have risen to almost 10% from 7% of disposable income compared with 7.25% at the 2008 peak.

- “Each 1 per cent decline in wealth results in a fall in consumption of around 0.1–0.2 per cent” but in the Q&A Kent said that the RBA is currently not concerned about rising house prices due to other factors pressuring households, including tighter credit - “the borrowing capacity for a typical household” is 30% lower than in May 2022. Also only half of mortgages have been rolled off fixed rates with the rest to occur over the next year. So policy lags are still in play.

NZGBS: Closed On The Local Session’s Best Levels, Net Migration Strong

NZGBs closed at local session highs, with benchmark yields 3bps lower. There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined net migration data.

- Bloomberg reports that the record inflow of migrants adds to risks that inflation pressures may persist longer than the central bank expects, quoting ASB Bank Senior Economist Mark Smith, who said “We expect the RBNZ to take out insurance and to retain restrictive OCR settings.” (See link)

- Hence, local participants have likely been guided by US Tsy dealings in the Asia-Pac session. Cash US Tsys are 1bp cheaper to 5bps richer in Asia-Pac dealings, with the curve flatter.

- Swap rates are flat to 6bps lower, with the 2s10s curve and implied swap spread box flatter.

- RBNZ dated OIS pricing is little changed across meetings, with terminal OCR expectations at 7.70%.

- Tomorrow, the local calendar sees Food Prices, ahead of Business NZ Mfg PMI and Card Spending data on Friday.

- Tomorrow, the NZ Treasury plans to sell NZ$200mn of the 4.5% May-30 bond, NZ$225mn of the 2.0% May-32 bond and NZ$75mn of the 2.75% May-51 bond.

FOREX: Greenback Steady In Asia

The USD is little changed in Asia, for the most part ranges have been narrow with little follow through on moves. The US Tsy Curve has flattened, and US Equity Futures are a touch firmer.

- Kiwi is pressured and is the weakest performer in the G-10 space at the margins. NZD/USD has trimmed yesterdays gains sitting at $0.6030/35 down ~0.3%.

- AUD/USD is also lower, however the pair has observed a narrow range for the most part. Technically the outlook remains bearish, support comes in at $0.6287 2.00 projection of the Jun 16-Jun 29-Jul 13 price swing. Resistance is at $0.6501, high from Sep 29.

- Yen unwound early gains and now sits little changed from opening levels. The pair is still in an uptrend, key support is at ¥147.43 the low from Oct 3 and resistance is at ¥150.16 high from Oct 3 and bull trigger.

- Elsewhere in G-10, EUR and GBP are a touch firmer however ranges have been narrow.

- In Europe today we have the final read of September CPI from Germany, and ECB 1- and 3-Year Inflation Expectations for August.

EQUITIES: Regional Markets Higher, Led By South Korea

Regional equities are higher across the board. South Korean markets are the standout performers (Kospi +2.5%). These moves follow positive sentiment in Tuesday US and EU trade. US futures sit slightly higher in latest dealings, with the Nasdaq slightly outperforming (+0.17%), while Eminis were only marginally higher, last near 4394.

- In the cross asset space, the US Tsy curve has flattened, while USD FX indices are close to steady.

- The Kospi has benefited from a Samsung earnings beat. The Kospi is up over 2.5% at this stage, the Kosdaq, +3%. Offshore investors have added +$152.3mn to local shares so far today.

- The Taiex is also tracking higher in Taiwan, up 0.85%. TSMC may reportedly see stronger AI-related demand next year per EDN (see this BBG link).

- The Hang Seng is +1.44% at the break. We had a strong rally in the Golden Dragon index during US trade on Tuesday. Renewed China stimulus hopes is aiding sentiment. For mainland China shares, the CSI 300 is +0.38% higher at the break.

- Japan stocks are higher, but the Topix is around +0.10% firmer, so lagging some of the gains seen elsewhere in North East Asian markets.

- The ASX 200 is +0.60% higher in Australia, while in SEA, only the Singapore bourse is tracking lower at this stage.

OIL: Crude Range Trading While Watching Geopolitical Events

Oil prices are moderately higher during the APAC session today as they range trade given the significant uncertainty stemming from recent events in Israel. Markets are watching closely for any expansion of the tensions into Iran. A risk premium was added to oil on Monday but it hasn’t widened while the aggression is contained within Israel/Gaza. The USD index is flat.

- Brent is up 0.3% to $87.96/bbl. It approached $88 earlier but only reached $87.99, the intraday high. Earlier it fell to $87.70. WTI is 0.3% higher at $86.20 and has also been in a narrow range between $85.83 and $86.26.

- The Saudi Press Agency is relating that Saudi Arabia will continue to support OPEC+ in ensuring a balanced oil market.

- There are tentative hopes that demand from China may increase after reports that the government deficit will be allowed to widen to boost growth.

- Russian product exports fell to a 3-year low in the first week of October due to its diesel export ban and a drop in refinery utilisation due to seasonal maintenance, according to Bloomberg.

- Later the Fed’s Bowman, Waller, Bostic and Collins speak plus the September Fed minutes are released. On the data front, US September PPI is released. There is also US crude and petroleum inventory data. The ECB’s Lagarde and Panetta will attend the IMF/World Bank annual meetings.

GOLD: Steady As Global Market Consolidate Moves Sparked By The Middle East Conflict

Gold is steady in the Asia-Pac session, after closing little changed on Tuesday at $1860.40.

- Bullion is dealing near the highest level this month after the conflict in the Middle East drew haven demand.

- The recent surge in precious metal prices can also be attributed to an emerging change in the sentiment regarding the Federal Reserve's policy outlook. There is a growing consensus among US policymakers that the recent spike in US Treasury yields, which reversed course on Monday, could potentially serve as an alternative to implementing further hikes in the Fed funds rate. It's worth noting that higher interest rates typically have a negative impact on gold, which doesn't yield interest.

- According MNI’s technicals team, the bearish theme in gold was put on pause Monday after a second session of gains. Monday’s bounce put prices back above $1850. Nonetheless, the recent sell-off resulted in a break of support at $1901.1 and this was followed by a breach of $1884.9, the Aug 21 low. This confirmed a resumption of the downtrend that started early May. The focus is on $1804.9, the Feb 28 low and a key support. On the upside, firm resistance is at $1878.2, the 20-day EMA.

SOUTH KOREA DATA: Goods Trade Surplus Back To Q1 2022 Levels

The August goods balance rose to $5060.9mn, from a revised $4438.5mn in July. This is the highest goods surplus since Q1 2022. Both exports and imports were higher, but the export gain outpaced the rise in imports.

- The services deficit fell to -$1603mn, as the travel deficit narrowed modestly. This was offset to some extent by a lower primary income surplus to $1467mn (form $2922mn). Lower dividend inflows from offshore equity investments drove this result.

- The current account surplus still rose to $4810mn in August from $3737mn in July. We are a touch below June highs in terms of the surplus.

- Focus will remain on the export outlook, with recent prints showing the worst of the downside momentum in growth is now behind.

- Note we get the first 10-days of October trade data today.

SOUTH KOREA DATA: Export Trend Shows Further Signs Of Improvement, But Trade Deficit Widens

South Korea's first 10-days of trade data for October hints at further improvement in the external demand backdrop. Exports were still down y/y but at -1.7%, this is a noticeable improvement on the equivalent September reading of -7.9%. Also note that the average daily export print was +9.2%y/y.

- The other detail also suggests less of a drag from 2023 headwinds. Chip exports were down -5.4%. Note for the full month of September we were down -13.60%y/y. Cars exports remained an area of strength, +14.7%.

- Exports to China were -4.2% y/y, (versus -17.6% y/y for the full month of September). External demand from the US appears to holding up, +14.7% y/y. The EU was weaker though -27.3% y/y.

- Imports were up 8.4% y/y in the first 10-days of October, versus -11.3% y/y for the first 10 days of September. The trade deficit ballooned to -$5.3bn for the first 10-days of October, -$1.6bn was the equivalent read last month.

ASIA FX: Most USD/Asia Pairs Lower, CNH & The High Yielders Lag

USD/Asia pairs are mostly lower, although CNH remains on the sidelines. Regional equity sentiment has been positive for the most part, led by South Korea. The won and THB have been the outperformers. Still to come today is the Taiwan trade figures for September. Tomorrow, we have South Korea bank lending to households, along with India IP and CPI prints due. Malaysia IP growth is also out.

- USD/CNH has held relatively steady, maintaining a narrow range during Wednesday trade to date. The pair was last near 7.2900, slightly above NY closing levels from Tuesday. he generally firmer equity backdrop isn't aiding sentiment today, although mainland equities are only a touch above recent lows. The latest insights from the MNI policy team suggests headwinds around the China economic backdrop, coupled with limited fiscal, monetary policy room (see this link).

- 1 month USD/KRW has broken lower, last near 1336, close to lows for the session. Earlier data showed a healthy goods trade surplus, along with signs of a further recovery in export demand. Local equities (Kospi +2.3%) have been buoyed by better Samsung earnings. Offshore investors have bought $133.1mn of local shares so far today.

- USD/HKD sits lower, last just under 7.8180. Lows today came in at 7.8159, while a spike above 7.8200 drew selling interest. A continued move lower could see September lows close to 7.8140 targeted. The pair is sub all its key EMAS, which remain clustered back near 7.8300. US-HK yield differentials have rolled over modestly. The 3 month spread is back to +26bps, which is still above late September lows near +14bps, but the broader move lower in yields, softer USD backdrop, have no doubt aided HKD.

- Spot USD/TWD has continued to track lower, last under 32.10, amid an improved mood for tech equity related sentiment. Later September trade data prints, which is expected to show better y/y momentum for exports, albeit still in negative territory.

- USD/IDR sits off recent highs. The pair last near 15700, around 0.25% stronger in IDR terms for the session so far. Yesterday's high was 15740, close to late 2022 highs. The 20-day EMA still sits lower at 15525, so unlike elsewhere in the region, the pair remains some distance away from a downside test of this support level. IDR remains the worst performer in Asian FX month to date, down 1.53% against the USD.

- The Rupee has opened dealing a touch firmer, however ranges for USD/INR remain narrow as the pair continues to consolidate above the 83.20 handle. A reminder that the data docket is empty today. The next release of note is tomorrow September CPI print, inflation is expected to tick lower to 5.40% Y/Y.

- USD/PHP sits back at 56.74, around 0.22% firmer in PHP terms versus yesterday's close. Like for some other parts of the region, the pair is testing downside support at the 20-day EMA. Still, for USD/PHP we remain well within recent ranges. Lows this month have been marked near 56.50, while resistance at 57.00 remains in place on the topside. BSP Governor Remolona has spoken today, and stated the central bank can't say that they are done with monetary tightening, while a 25bps hike won't be ruled out (as upside risks to inflation have materialized).

- The SGD NEER (per Goldman Sachs estimates) is little changed in early dealing on Wednesday and remains well within recent ranges. The measure sits ~0.5% below the top of the band. USD/SGD has held below the 20-Day EMA ($1.3654) after breaking the measure yesterday, improving sentiment through yesterday's session saw broad based pressure on the greenback.

- USD/THB continues to track lower, last near 36.42, +0.90 stronger in baht terms. We are through the 20-day EMA downside support point. Aiding sentiment has been a pick up in equity sentiment, the SET up +1% so far today. The BoT mins pointed to policy settings being at neutral.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/10/2023 | 0600/0800 | *** |  | DE | HICP (f) |

| 11/10/2023 | 0815/0415 |  | US | Fed Governor Michelle Bowman | |

| 11/10/2023 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 11/10/2023 | 1100/0700 | ** | | US | MBA Weekly Applications Index |

| 11/10/2023 | 1230/0830 | * |  | CA | Building Permits |

| 11/10/2023 | 1230/0830 | *** | | US | PPI |

| 11/10/2023 | 1415/1015 | | US | Fed Governor Christopher Waller | |

| 11/10/2023 | 1615/1215 | | US | Atlanta Fed's Raphael Bostic | |

| 11/10/2023 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 11/10/2023 | 1800/1400 | * | | US | FOMC Rate Decision |

| 11/10/2023 | 2030/1630 | | US | Boston Fed's Susan Collins |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.