Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

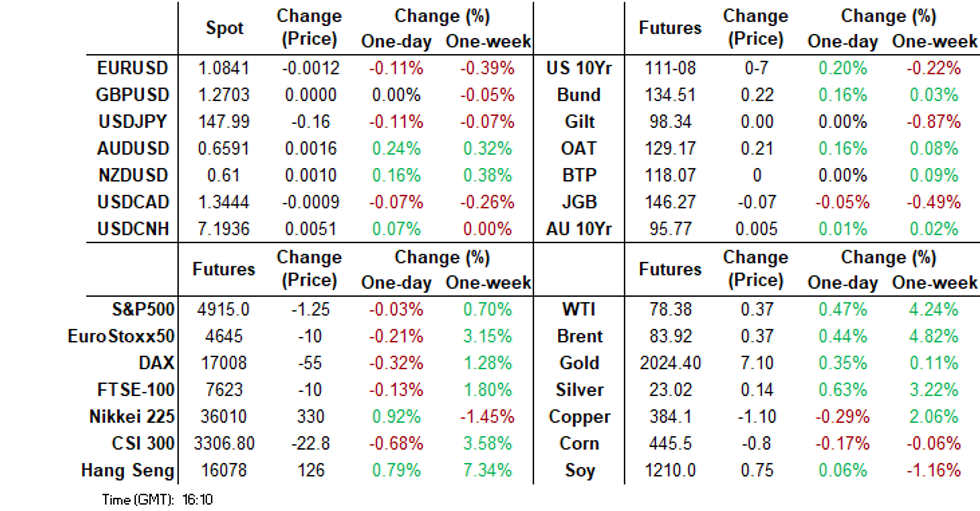

- The oil price spike was the early focus, as the market digested the news around the late Friday Houthi attack on shipping in the Red Sea. We have also had news of US soldiers under attack in Jordan on Sunday, near the border with Syria, reportedly by Iranian backed militia (with 3 fatalities). There wasn't much spill over to broader markets though, with US Tsy futures reversing an opening spike.

- US equity futures also largely recovered earlier weakness. Regional equity sentiment has mostly been positive. China mainland markets have been the exception. Court orders for troubled property developer Evergrande to wind up weighed, along with concerns around fresh tech curbs from the US.

- USD/Asia pairs are mostly higher, with weaker CNH levels and higher oil prices weighing. G10 currencies have mostly been steady, with some outperformance from AUD and NZD.

- Looking ahead, it is a quiet start to the week, with ECB speak and the Dallas Fed manufacturing survey on tap.

MARKETS

US TSYS: Cautious Tone Ahead of FOMC, China Evergrande Ordered Into Liquidation

TYH4 is trading at 111-06+, + 05+ from NY closing levels. Futures have been rangebound all day with very little to note. There was a very brief spike early this morning but this has been pared, with Tsys brushing off Friday night news around the Russian Oil tanker being hit in the Red Sea, and the weekend news about US soldiers being attacked in Jordan. The upcoming FOMC decision has most traders sitting on the sidelines ahead of the announcement on Wednesday. Heading into the meeting the market is predicting about a 50% chance of a rate cut in March.

A quick recap, US Treasuries opened 111-06, and briefly spiked to 111-09+ before settling and trading in a very small range for the remainder of the day, however around the 111-07+ level. Cash yields have been uneventful all day trading within the 0.5 to -0.5 range.

- Cash bonds are trading -0.5 to -0.9bp richer across the curve, 2y at 4.343% (-0.6) and 10y at 4.13% (-0.8).

- China Evergrande headlines out earlier, as creditors were unable to reach an agreement on a restructure, this pushed the share price to records lows before being suspended and ordered into liquidation by a Hong Kong court

- Data is light on tonight, with FOMC policy announcement on Wednesday the major focus.

JGBS: Futures Downtick As Middle East-Induced Haven Buying Quickly Fades

JGB futures are dealing with a downtick in the Tokyo afternoon session, -6 compared to settlement levels, after quickly reversing early strength sparked by the weekend’s Middle East developments. Nevertheless, spillover from higher oil prices will likely remain in focus today, after the attack on a Russian Oil tanker in the Red Sea late Friday and the weekend attack on US soldiers in Jordan near the border with Syria.

- Cash US tsys are dealing ~1bp richer in today’s Asia-Pac session.

- Today, the local calendar has been empty, apart from BoJ Rinban Operations covering 3-10-year and 25-year+ JGBs. The results were mixed, with lower offer cover ratios across the buckets but positive spreads. The impact on the market has been minimal.

- Cash JGBs remain cheaper on the day, but slightly richer than lunchtime levels. The 20-year is underperforming, with its yield 2.3bps higher at 1.547%. The benchmark 10-year yield is 0.9bp higher at 0.726% versus the Nov-Dec rally low of 0.555%. The 2-year is outperforming (+0.4bp) ahead of tomorrow’s supply.

- Swaps curve is witnessing a bear-steepening, with rates flat to 3bps higher. Swap spreads are mostly wider, apart from the 20-year.

- Tomorrow, the local calendar sees Jobless Rate and Job-To-Applicant Ratio data.

AUSSIE BONDS: Light Calendar, Narrow Ranges, Limited Impact From Middle East

ACGBs (YM flat & XM +1.0) are flat after dealing in narrow ranges in today’s Sydney session. The local market was closed on Friday in observance of the Australia Day holiday. With the domestic calendar empty today, the focus has been abroad following the weekend’s events in the Middle East. Nevertheless, the bond market's reaction has so far been muted, with cash US tsys dealing little changed in today’s Asia-Pac session.

- (AFR) Treasurer Jim Chalmers says he will discuss the investment direction of the $212 billion Future Fund with incoming chairman Greg Combet, after both the Labor figures previously backed the $3.5 trillion superannuation sector playing a more active role in funding the energy transition. (See Bloomberg link)

- Cash ACGBs are 3-4bps richer relative to Thursday’s close, with the AU-US 10-year yield differential 1bp tighter at +8bps.

- Swap rates are 2-4bps lower, with the 3s10s curve steeper.

- The bills strip is little changed, with pricing flat to +2.

- RBA-dated OIS pricing is flat to 4bps softer across meetings, with December leading. A cumulative 43bps of easing is priced by year-end.

- December retail sales are out tomorrow. The main focus will however be Wednesday's CPI print for Q4, which comes before next week's RBA meeting.

NZGBS: Cheaper But Volumes Low Due To Auckland Holiday

NZGBs closed 3bps cheaper, with volumes low due to Auckland being out for a public holiday. There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined trade balance data for December. The Australian and Japanese calendars were also light today.

- Early session strength following the weekend’s Middle East developments proved to be fleeting, with cash US tsys currently dealing flat to 1bp richer in today’s Asia-Pac session.

- Nevertheless, spillover from higher oil prices will remain the focus today, along with broader risk trends, after the attack on a Russian Oil tanker in the Red Sea late Friday and the weekend attack on US soldiers in Jordan near the border with Syria.

- Swap rates closed 1-3bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed slightly firmer across meetings. A cumulative 91bps of easing is priced by year-end.

- RBNZ Chief Economist Conway will deliver a keynote speech tomorrow. The speech will focus on the significant changes to the global economy since the COVID-19 pandemic. He will also make brief comments on domestic data developments since the November Monetary Policy Statement.

FOREX: USD Off Earlier Highs, A$ Marginally Outperforms

G10 FX markets have had a reasonably muted start to the week. The USD was mildly supported in early trade, as the market started off in risk averse fashion amid higher oil following further shipping attacks late last week and US troops in Jordan (near the Syrian border) coming under drone attack (with 3 reported casualties).

- However, the BBDXY couldn't breach the 1238 level, with US Tsys futures showing little follow through after spiking higher at the open. US equity futures opened weaker, but have clawed back losses, with Nasdaq futures back in positive territory. Oil prices moving off earlier highs has helped at the margins (Brent is still up around 0.50%). The BBDXY was last near 1237.

- AUD has outperformed marginally, up 0.20%, but hasn't been able to retake the 0.6600 handle. Outside of oil, other commodities are tracking higher, which is supportive at the margin.

- NZD/USD is also marginally higher, but hasn't drifted far away from 0.6100. Earlier trade data saw a narrower deficit in Dec, but the impact on sentiment was minimal.

- USD/JPY has stayed above 148.00 for the session, but couldn't sustained an earlier break above 148.30.

- Looking ahead, it is a quiet start to the week, with ECB speak and the Dallas Fed manufacturing survey on tap.

EQUITIES: Asia Equities Mostly Higher, China Evergrande Ordered Into Liquidation

Asia equities are mostly higher to start the trading week, with China equities mixed. US Equity futures opened lower this morning on the back of the attack on a Russian Oil tanker in the Red Sea (late on Friday) and the weekend attack on US soldiers in Jordan near the border with Syria, but along with other markets have recovered most of the initial move lower. Eminis are 015% lower, while the Nasdaq trades flat today. China Evergrande news has dominated the headlines here in Asia, after creditors were unable to come to an agreement on a restructurer pushing shares to lowest on record before a trading halt was put in place.

- Japan Equity indices are in the green today, energy producers are leading the way as the price of oil jumped, while Toyota is trading higher by 3.27% as the leading contributor to the Topix. The Nikkei 225 is up 1.09%, while the Topix is up 1.34%

- Hong Kong was up as much as 1.81% today, but has given a large chuck of that up now to be trading just 0.88% higher, Alibaba has contributed to most of the gain, Property names are also higher in Hong Kong today after the southern city of Guangzhou eased home-buying restrictions and pledged more financing support.

- China mainland stocks are underperforming today. News around China Evergrande, seemed to weigh on sentiment, with creditors unable come to a restructuring agreement and courts ordering Evergrande to be liquidated. China announced early last week that they were looking into a stock market rescue package and an MLF rate cut, and over the weekend the securities regulator said they will halt the lending of certain shares for short selling from this morning, however these measures haven't been enough to give the market the push higher it's been after. There has been concerns over the Biden administrations announcement around requiring US cloud firms to reveal foreign clients developing AI applications, and that some US lawmakers had proposed legislation targeting Chinese biotech companies. Currently the CSI 300 is close to flat while the ChiNext is 2.30% lower.

- Taiwan continues its winning streak from last week, trading 0.60% higher today, with energy names leading the way.

- In Korea, strong start to the week with the Kospi up 1.65%.

- Australia, is on track to make it six straight sessions of gains, and is currently 50 points away from all time highs, the market is being lead higher today Oil & Gas names. ASX 200 is currently 0.30% higher.

- In SEA, Nifty 50 is up 1.15%, Indonesia is up 0.90% while the Philippines are lower by 0.25%

OIL: Off Earlier Highs, But Positive Bias Intact On Mid-East Supply Concerns

Oil prices sit off earlier highs. Brent was last near $84/bbl, against an earlier high of $84.80/bbl. WTI was last tracking close to $78.40/bbl. Both benchmarks are around 0.50% higher, building on last week's +6% gains.

- The early spikes followed the late Friday Houti attack on a Russian linked carrier in The Red Sea. We have also had news of US soldiers under attack in Jordan on Sunday, near the border with Syria, reportedly by Iranian backed militia (with 3 fatalities).

- US President Biden has stated "We shall respond" at a campaign event in the US on Sunday. The Houthi attack from Friday raised concern that attacks on Red Sea shipping are expanding and not just confined to US, UK or Israeli linked ships.

- This is keeping Middle East supply concerns still front and center from a market concern standpoint.

- Elsewhere, Russia stated it has carried out its pledge to cut oversea oil supplies (see this BBG link for more details).

- For Brent, we tested late Nov highs close to $85/bbl earlier. This will remain the upside focus. On the downside the 200-day EMA sits back near $82.84/bbl.

GOLD: Pressured By A Resilient US Economy

Gold is 0.4% higher in the Asia-Pac session, after closing 0.1% lower at $2018.52 on Friday. Haven buying is likely behind today’s strength after the attack on a Russian Oil tanker in the Red Sea late Friday and the weekend attack on US soldiers in Jordan near the border with Syria.

- On Friday, a slight appreciation in the USD and higher US treasury yields pressured bullion after Friday’s data showed a resilient US economy, which could influence the Federal Reserve’s messaging about the pace of interest-rate cuts when it hands down its decision on Wednesday. Fed speakers have been in blackout ahead of this week’s FOMC meeting.

- It was a busy US data session on Friday. Inflation data was close to expected, while spending was firmer than forecast. US Pending Home Sales were also higher than expected, printing a whopping 8.3% m/m increase vs. 2.0% estimate.

- The market is currently assigning around a 50% chance to a 25bp rate cut in March. This compares to the near 70% chance seen a couple of weeks ago. Lower interest rates are typically positive for non-interest-bearing gold.

- Friday’s dip failed to test previously established technical levels, with support at $2001.9 (Jan 17 low) and resistance at $2039.4 (Jan 19 high), according to MNI’s technicals team.

SINGAPORE: MAS Holds Steady, Core Inflation Expected To Fall Gradually

The MAS left all of its policy parameters unchanged at the January meeting. The slope, width and mid-point of the currency band unchanged. This was widely expected by the consensus and was our own firm bias.

- The accompanying statement was fairly optimistic about the growth outlook. The central bank noted, "Prospects for the Singapore economy should continue to improve in 2024, with GDP growth projected to come in between 1–3%."

- A further recovery in the electronics sector and easier policy settings global should support external demand. This should a further normalization in terms of domestically orientated growth.

- The inflation backdrop is expected to show continuing easier momentum as we progress further into 2024. This is after the impact of the January GST hike subsides. "MAS Core Inflation is projected to slow to an average of 2.5–3.5% for 2024 as a whole, unchanged from the October 2023 MPS. Excluding the impact of the increase in the GST rate this year, core inflation is forecast at 1.5–2.5%."

- "CPI-All items inflation in 2024 is now forecast to be lower at 2.5–3.5%, down from the previous range of 3–4%. Excluding the effects of the increase in the GST rate, headline inflation is forecast at 1.5–2.5%." This reflects expected lower COE prices.

- Importantly, core inflation is expected to fall in the later stages of this year and into next.

- This is ultimately likely to pave the way for easier policy settings, which would be in line with expected global trends.

- However, the April meeting may be too soon for such a shift as the central bank highlighted balanced risks for both the growth and inflation backdrops as we progress through this year.

ASIA FX: USD/Asia Pairs Firm, MAS Unchanged As Expected

USD/Asia pairs are mostly higher in the first part of Monday, slightly underperforming the steadier tone the majors have seen against the USD (although EUR is down a touch). Given most in the region are net oil importers, the threat of higher energy oil prices will be weighing at the margin. PHP has fallen 0.35%, while USD/CNH is back to 7.1950, with weaker local equities not helping. The MAS was unchanged as expected. Tomorrow, the data calendar is light in the region.

- USD/CNH has been biased higher, but dollar gains have been modest, the pair last near 7.1950, around 0.1% weaker in CNH terms. China mainland stocks are underperforming today (the CSI 300 down around 0.4%). News around China Evergrande, seemed to weigh on sentiment, with creditors unable come to a restructuring agreement and courts ordering Evergrande to be liquidated. There has also been concerns around fresh US tech curbs. USD/CNH is close to the 7.2000 level, a move above may see greater push back from the China authorities.

- 1 month USD/KRW has stuck to recent ranges, the pair currently little change, last at 1335. Onshore equities are up comfortably over 1% to start the week, but some offset has come from higher USD/CNH levels, while a firmer oil price backdrop also hasn't helped.

- The Singapore MAS decision came and went without much market reaction The as expected outcome, left all policy parameters unchanged. The central bank looks to be gearing up for an eventual easing, but that may not happen at the next policy meeting in April. USD/SGD sits off session highs, last near 1.3415, little changed versus end Friday levels.

- USD/THB was biased lwoer in earlier trade, but found support close to 35.50. Baht sentiment was aided by headlines around the China/Thailand Visa waiver agreement. However, USD/THB now sits back above 35.60, erasing earlier gains. Further local calls for a BoT rate cut, coupled with weak domestic confidence is not helping, while broader USD gains have also weighed.

- Spot USD/PHP is 0.35% higher, putting the pair back close to earlier January highs. A clean break above this level is likely to see the market target a move back into the 56.75-57.00 region, highs from Aug-Oct last year. Outside of higher oil prices, local political is another potential headwind. A wedge is apparent between current President and former leader Duterte (see this BBG link).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/01/2024 | 0700/0800 | *** |  | SE | GDP |

| 29/01/2024 | 0700/0800 | ** | | SE | Retail Sales |

| 29/01/2024 | 1200/1300 |  | EU | ECB's de Guindos on Investment Outlook | |

| 29/01/2024 | 1530/1030 | ** |  | US | Dallas Fed manufacturing survey |

| 29/01/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 29/01/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 30/01/2024 | 2330/0830 | * |  | JP | labor forcer survey |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.