Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

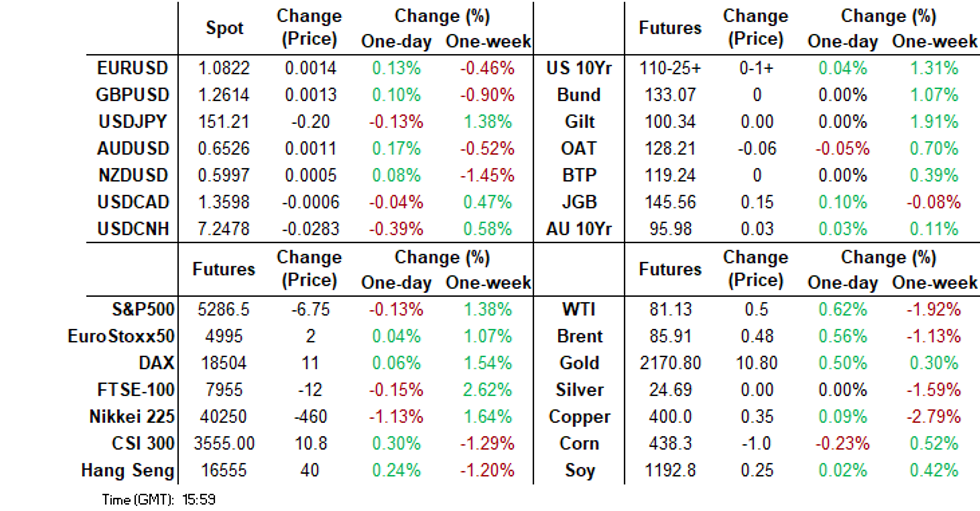

- The stronger CNY fixing weighed on broader USD sentiment. However, the USD was supported on dips for the most part. USD/JPY couldn't break Friday lows, despite a pick up in FX rhetoric from the authorities.

- Jun'24 10Y US futures started the week on a positive note reaching an earlier high of 110-30, before erasing most of the mornings gains to trade down at 110-25+ and now back below initial resistance of 110-26+. We have more Fedspeak coming up later.

- Rice prices have risen strongly since mid-2023 after weather-affected harvests and India banned the export of non-basmati varieties. This impacted the food CPI in some countries, but even in the worst affected there haven’t been second-round effects on underlying inflation, the focus of central banks. Falling global cereal prices have also helped to reduce the impact. Non-Japan Asian core inflation ex China was low at 2.2% in February and headline 3.7%.

- Later the Fed’s Bostic, Goolsbee and Cook speak and the Chicago & Dallas Fed indices are released as well as February new home sales. BoE’s Mann also appears.

MARKETS

US TSYS: Treasury Futures Off Earlier Highs Ahead Of Fed Speaker Later

- Jun'24 10Y started the week on a positive note reaching an earlier high of 110-30, before erasing most of the mornings gains to trade down at 110-25+ and now back below initial resistance of 110-26+.

- Looking at technical levels: Initial support lays at 109-24+ (Mar 18 low/ the bear trigger), further down 109-14+ (Nov 28 low). Futures now trade back below initial resistance of 110-26+ (Mar 21 high), if we can manage to get back above initial resistance the target becomes 111-00+ (50-day EMA), while a break above here would open a retest of 111-24 (Mar 12 high).

- Cash yields are flat to 1.5bps higher today with the curve slightly flatter today, the 2yr +0.8bps at 4.598%, 10yr -1bp at 4.208% while the 2y10yr is +0.129 at -39.190

- Atlanta Fed President Raphael Bostic now anticipates only one interest-rate cut this year, likely occurring later than previously expected, citing less confidence in inflation trajectory. Despite Fed officials' outlook for three rate cuts, Bostic notes the economy's resilience, advocating for patience and a slower pace in shrinking the central bank's balance sheet.

- Monday Data Calendar: Fed Speak, New Home Sales, Dallas Fed Mfg

JGBS: Firmer Bias, But Limited US Tsy Upside Curbs Gains

JGB futures have mostly traded with a positive bias in the first part of Monday trade. We were last at 145.60, +.19. Session highs came in at 145.70, while lows were at 145.42.

- The general tone in global yields through the latter stages of last week was to soften after some dovish shifts from EU central banks. This has spilled over to JGBs to some degree.

- US Tsy futures are off earlier highs (TYM 4 last at 110.25), which has likely kept JGB futures from extending higher. We do have more US Fed speak later on Monday.

- The BoJ mins for the Jan meeting came and went without much market reaction. They have obviously been superseded by last week's shift away from NIPR. The mins stated if there was a delay in exiting NIPR it could mean more aggressive rate hikes later, while financial conditions were expected to remain accommodative even when such a move was made.

- We also had a step up in FX rhetoric from FX chief Kanda earlier, but yen couldn't break higher.

- In the cash JGB yield space, most yield weakness is evident in the belly of the curve, with 7 and 10yr yields off around 1bps respectively. The 2 yr yield is holding above 0.20% at this stage. In the swaps space, the 10yr is down slightly, last near 0.86%.

- Looking ahead, tomorrow has the PPI and machine tool orders. On Wed we have BoJ board speak (Tamura), along with a 40yr debt sale.

AUSSIE BONDS: Yields Lower, CPI Wednesday, Min Wage To Rise

ACGBs (YM +4 & XM +3.5) are richer today tracking moves higher made by US treasuries. There is little in the way of eco data today, with the major focus on Wednesday's CPI data. President Of the Federal Reverse Bank of Atlanta now see's just one cut for the year down from two and the cut happening much later in the year than previously expected.

- (Bloomberg) -- Australian economy has 'rare trifecta': treasurer (see link)

- (Reuters) -- Australia to recommend minimum wage rise in line with inflation (See Link)

- Cash ACGBs are 2-4bps cheaper, the curve is flatter with the 2yr -3.5bp at 3.776%, the 10y now back below 4.0% down 3.7bps at 3.994%, while the 2y10y is -0.110 to 20.220

- The AU-US 10-year yield differential is back unchanged from Friday opening levels after pushing higher during the US session on Friday to -16bps and now trades back to at -21bps, while AU swap rates are 1-2bps lower.

- RBA-dated OIS pricing is 1-5bps softer for meetings beyond June. A cumulative 48bps of easing is priced by year-end.

- Looking ahead: The calendar is empty on Monday, while Tuesday we have Westpac Consumer Confidence

AUSTRALIAN DATA: Rising Petrol Prices May Produce Economic Headwinds

Global Brent crude is up over 11% this year and around 4.5% just in March and with refined product prices up too from geopolitical tensions and increased demand, it is unsurprising that fuel prices have risen in Australia too. Australian Institute of Petroleum national unleaded petrol prices fell 1.1% w/w last week to 200.5c/L after they rose 1% w/w to 202.7c/L the previous week, the highest since October 2023. The average for March is up around 4c/L or 2.1% m/m after February rose about 11c or 6% m/m. Westpac March consumer confidence, March MI inflation expectations and February headline CPI are all released this week. While there are many factors that impact these variables, the over 8% increase in petrol prices since January and their rise above 200c/L again may weigh on sentiment and put upward pressure on inflation data.

Australia CPI y/y% vs Brent crude US$

Source: MNI - Market News/ABS/Refinitiv

NZGBS: Yields Edge Lower, Conway To Speak Tuesday

NZGBs yield opened lower across benchmarks and continued to grind lower over the day finishing 2-4bps lower. A risk off tone has pushed yields on longer date bonds back to levels from early January, the 10y now trades at 4.479%. There has been very little in the way of local headlines, NZ will look to sell 84, 164 & 350-day Bills on Tuesday, while Conway to also speak.

- (Bloomberg) -- RBNZ Paper Suggests Use of Smaller Suite of Labor Indicators (See link).

- NZGBs yields closed lower today, with the curves bull flattening. The 2y is -2.7bps to 4.581%, while the 10y is -3.5bps to 4.521%

- Swap rates are 1-4bps lower today, while the 2s10s curve is flatter

- The NZ trade weight Index is just off earlier lows, down 0.14% to 70.56, while the AU-NZ 2yr swap is just off monthly highs at -0.8425, the NZD has managed to get back above 0.6000, trading at 0.6008, while Equities are up 0.82%.

- The NZ commodity price Index dipped for the first time since Earlier January now at 116.48, from 116.79 a yearly high after Milk prices fell slightly.

- RBNZ dated OIS is unchanged this morning with a cumulative 71bps of easing is priced by year-end.

- Today, the calendar is light. Upcoming RBNZ's Conway speaks about Feb MPS on Tuesday

FOREX: USD/JPY Shrugs Off Step Up In FX Rhetoric, Higher CNY Fixing Weighs On Broader USD Sentiment

The BBDXY index sits lower for the Monday session as we approach the London/EU cross over, last near 1245.15, off a little over 0.10%. We are up from earlier lows of 1243.55, which came post the stronger than expected CNY fixing.

- The CNY fixing was the main focus point today, as markets assessed whether we would see a run of further yuan weakness. In the event the fixing was set stronger than expected (back sub 7.1000), which has seen USD/CNY largely reverse Friday's gains.

- Prior to this we had a step up in official rhetoric from Japan's Chief currency diplomat Kanda. He described recent FX moves as being speculative and that the authorities wouldn't hesitate to act. Still, the pair could test Friday lows around 151.00 during this period or post the stronger CNY fixing. We track near 151.25/30 in recent trade, only marginally stronger in yen terms.

- The BoJ minutes for the Jan meeting were released, but have largely been superseded by last week's BoJ meeting, which ended NIRP.

- AUD/USD is higher, last near 0.625/30, nearly 0.20% firmer. Earlier highs were at 0.6544 as the currency benefited from a stronger yuan and a more positive HK/China equity tone.

- NZD/USD has lagged at the margins, last near 0.6000, up from fresh YTD lows of 0.5986.

- US yields have recovered from earlier lows, likely aiding the USD regaining some ground from earlier lows.

- Looking ahead, we have Fed speak (including Bostic again, along with Goolsbee and Cook) and some US data (new home sales and Dallas Fed Manufacturing). The BoE's Mann also speaks.

ASIA EQUITIES: Hong Kong & China Equities Erase Earlier Losses

Hong Kong and China equities are mostly higher post the break on Monday, after initially opening lower. Equities were helped higher after Premier Li Qiang downplayed investors concerns facing the economy. Focus this week will turn to corporate earnings as economic data is light. Earnings from Country Garden and China Vanke will be closely watched as investors wait to see the extent of China's property woes, while earnings from Chinese banks will also shed some light on where the market is heading. It has been announced that Treasury Secretary Janet Yellen will visit China in April to meet with the country's senior leaders.

- Hong Kong equities are slightly higher today, the Mainland Property Index opened slightly lower, however quickly erased those loses and now trade up about 3% to be the top performing sector. The HSTech is unchanged after plummeting as much as 4.35% on Friday while the wider HSI is up 0.40%. In China, equities indices have been grinding higher after initialy opening the session lower with the CSI300 up 0.42%, the smaller cap CSI1000 lags wider market moves and is up just 0.14% while the ChiNext is down 0.37%

- China Northbound flows were -3.1billion yuan on Friday, with the 5-day average at 1.55 billion, while the 20-day average sits at 2.27 billion yuan.

- In the property space today it has been quiet for company specific news however China’s Premier Li Qiang reviewed proposals to fortify the nation’s property market policies during a State Council meeting. Li emphasized the need for systematic planning of real estate support policies to stimulate demand effectively. He also advocated for augmenting the supply of high-quality housing and ensuring the stable advancement of the real estate market. addressing economic challenges by stepping up policy support to stimulate growth, citing low consumer price growth and manageable government debt levels. Despite positive economic indicators, including strong exports and industrial production, longer-term challenges such as deflation, a property downturn, and low foreign investment confidence persist, prompting a focus on boosting domestic demand and advancing strategic industries.

- Apple Inc. is reportedly considering using Baidu Inc.'s generative artificial intelligence technology in its devices within China, marking a potential collaboration between the two tech giants in the tightly regulated Chinese market. Baidu's expertise in AI could provide Apple with a significant advantage, with discussions ongoing as Apple explores partnerships with various AI providers for its products, similar to its arrangement with Google and OpenAI for search functionalities.

- Fears of a slowdown in Chinese luxury spending have impacted fashion giant Gucci, leading to a nearly 20% decline in sales this quarter, particularly in the Asia-Pacific region. This contributed to a $9 billion market value loss for Gucci's parent company, Kering SA. The broader luxury industry is also feeling the effects, with Swiss watch exports to China tumbling and analysts predicting further cooling of luxury demand in the country.

- Looking ahead, it's a quiet week for China econ data, while Hong Kong has Trade Balance data out on Tuesday.

ASIA PAC EQUITIES: Equities Mixed, Japan Equities Fall On Yen Support, Aus/NZ Higher

Regional Asian equities are mostly lower, today with Australia and New Zealand equities the exceptions. It has been a quiet day for market headlines and economic data, as markets await a busy end to the week for economic indicators, including the Fed's preferred inflation gauge. Earlier, Japan's currency chief warned of significant moves in the FX markets driven by market speculation rather than fundamentals, in relation to the weakening yen from the past week.

- Japan's equities are lower today as investors seek to lock in profits after the Nikkei hit new all-time highs on Friday, while the Topix marked a 6-day advance on Friday. Exporters are lower today as the yen edged higher following a warning from Japan's Currency Chief to the FX market. Japan has just released the Leading Index coming in at 109.5 vs 109.9 previously, while the Coincident Index rose to 112.1 from 110.2 previously, shortly Store Sales data will be released. The Topix is down 0.88%, while the Nikkei 225 is down 0.69%.

- South Korean equities are slightly lower to unchanged with tech names have leading the decline. Representatives from various international financial firms are visiting Korea to explore investment opportunities and discuss corporate governance practices amid the government's Corporate Value-up Program launch, aiming to enhance transparency and attract more overseas investments. The trip organized by the Asian Corporate Governance Association aligns with efforts to improve Korea's corporate governance standards and elevate the valuation of listed companies, potentially increasing foreign investor interest in the Korean market. The Kospi is down 0.19%.

- Taiwanese equities have edged higher today after initially starting the day lower, there has been very little in the way of market news and headlines out of the region. The Philadelphia SE Semiconductor Index was only slightly higher on Friday, while local semiconductor names including TSMC are lower. The Taiex is up 0.14%

- Australian equities are higher today, with banks leading the gains. Earlier, Fitch Ratings stated that "The ratings of the four major Australian banks have significant buffers to withstand a slowing economy and higher unemployment,". Miners are higher after ANZ called for the bottom for Iron Ore prices. The ASX200 finished up 0.53%.

- Elsewhere in SEA, New Zealand equities are higher, up 0.74%, Singapore equities down 0.20%, Indonesian equities down 0.33% after marking 5 straight days of foreign investors inflows, while Malaysian equities are down 0.35% and Indian equity markets are closed for a public holiday.

ASIA EQUITY FLOWS: Foreign Investors Buy Asian Equity, SK Benefits From Policy Changes

- China equities were lower on Friday as a raft of disappointing earnings hurt of the recent rally in stocks, while northbound flows were again negative at -3.13b. China EV maker Li Auto was one of the worst performing after it lower guidance. Looking ahead this week eyes will be on China property names after Longfor group also reported poor results. CSI300 has hit key technical resistance, unable to break above the 200-EMA, while the new proposed US bill aimed at banning US mutual funds from purchasing some Chinese Indices has been seen to be weighing on market sentiment. The 5-day average now sits at 1.55 billion yuan, below the 20-day average of 2.27 billion yuan.

- South Korean equities finished Friday lower on as markets took a bit of a break. Foreign investors inflows were again positive with $458m entering the market. Looking ahead this week multiple international financial firms are scheduled to visit SK this week as interest grows in the governments new corporate value-up program. The 5-day average is now $522 million, above the longer-term 20-day average at $153 million and the 100-day average at $172 million.

- Taiwan equities were pushed lower on Friday as regional tech names took a hit. US tech names brushed off the weakness which could support Taiwan semiconductor names today. Foreign investors equity flows were positive on Friday, after two large days of outflows on Tuesday and Wednesday last week. the 5-day average is still negative at -288m, while longer term trends still sit positive with the 20-day at $124m while the 100-day average is $177m

- Thailand equities seen another -$17m of net outflows, the $1b in outflows from earlier in the week did very little to equities prices suggesting it was an international fund leaving the market, while domestic accounts easily absorbed the supply.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| China (Yuan bn)* | -3.1 | -7.8 | 62.8 |

| South Korea (USDmn) | 458 | 2613 | 10649 |

| Taiwan (USDmn) | 138 | -1445 | 6582 |

| India (USDmn)** | -160 | -314 | 1436 |

| Indonesia (USDmn) | 24 | 136 | 1810 |

| Thailand (USDmn) | -17 | -1046 | -1930 |

| Malaysia (USDmn) ** | 61 | -132 | -128 |

| Philippines (USDmn) | -10 | 8.5 | 204 |

| Total (Ex China USDmn) | 494 | -180 | 18623 |

| * Northbound Stock Connect Flows | |||

| ** Data Up To March 21 |

OIL: Crude Higher Again Buoyed By Conflicts & Weaker USD

After falling moderately on Friday, oil prices have trended higher again today driven by events related to Russia. Brent broke through $86 earlier but couldn’t sustain the move and is now up 0.6% to $85.92/bbl. WTI has rallied above $81 to be up 0.6% at $81.14/bbl, after an intraday high of $81.28. Crude has been supported by a weaker US dollar. The USD index fell 0.2% but is now down 0.1%.

- The focus is on Russia with Friday’s terrorist attack in Moscow, the energy sector targeted by Ukrainian drones and sanctions impacting energy exports. Drone strikes are estimated to have taken around 12% of refining capacity offline.

- India has said that it won’t take Russian oil on state-run Sovcomflot tankers because of sanctions. India has become the second largest buyer of Russian crude after China since Russia invaded Ukraine. Commentators are noting that sanctions are now impacting Russian exports and raising shipping costs.

- Iran-backed Houthis fired a missile at a Chinese-owned oil tanker sailing in the Red Sea on Saturday.

- Conditions around crude remain bullish and money managers’ net long positions are at their highest in over a year, according to Bloomberg.

- Later the Fed’s Bostic, Goolsbee and Cook speak and the Chicago & Dallas Fed indices are released as well as February new home sales. BoE’s Mann also appears.

GOLD: Firms As USD Index Weakens Post Stronger CNY Fixing

Gold has moved higher in the first part of Monday trade. The precious metal was last near $2170.50 up close 0.25% for the session so far. Gold has largely followed broader USD gyrations in the first part of Monday trade.

- We rose earlier amid broad USD gains after the stronger than expected CNY fixing printed. Highs came in at $2178.36, while earlier lows (pre CNY fixing) were at $2164.08. These moves keep us within recent ranges for the metal. As USD sentiment stabilized somewhat, gold move off its session highs.

- Friday lows in the metal were $2157, while upside focus will remain on break back above the $2200 level.

- Goldman Sachs presented a generally positive commodity price outlook for 2024, with central bank cuts to aid sentiment, although the bank noted that gains won't be uniform. It expects gold to reach $2300 by year end (see this BBG link for more details).

ASIA DATA: Rice Prices Had Little Impact On Core Inflation, But Now Peaking

Rice prices have risen strongly since mid-2023 after weather-affected harvests and India banned the export of non-basmati varieties. This impacted the food CPI in some countries, but even in the worst affected there haven’t been second-round effects on underlying inflation, the focus of central banks. Falling global cereal prices have also helped to reduce the impact. Non-Japan Asian core inflation ex China was low at 2.2% in February and headline 3.7%.

- The good news is that rice prices appear to have peaked with processed rice down 22.7% this year and rough rice futures down 3.4% m/m in March. FAO cereals fell 5% m/m and 22.4% y/y in February.

- Philippines is one of the most impacted countries by higher rice prices with CPI rice rising 1% m/m to be up 23.7% y/y in February but core CPI still eased to 3.6% from 3.8% and from 7.4% in June 2023. The Philippines has been impacted by importers rice hoarding. The government made a deal with Vietnam to provide 50-67% of total imports over five years, according to JP Morgan, which should significantly improve supply.

- Thailand is a rice exporter but its rice CPI picked up in February to 5.2% y/y from 3.9% but government measures have helped keep it contained. Headline and core inflation remain very low at -0.8% y/y and +0.4% respectively.

- Government subsidies have kept a lid on Indonesia’s rice prices with retail prices falling in January. Inflation is well contained within Bank Indonesia’s target band, despite a 0.2pp uptick in February headline to 2.8%, with core close to the bottom of the band at 1.7%.

- Other Asian countries, such as HK, Singapore, Taiwan and Malaysia, have seen rice inflation tracking below 5% y/y in recent months.

Source: MNI - Market News/Refinitiv/FAO/IMF

ASIA FX: USD Support On Dips Post Stronger CNY Fixing

USD/Asia pairs are lower, aided by the stronger CNY fixing, but we are up from best levels. USD weakness has been slightly more evident against NEA FX, compared to SEA FX. Spot USD/CNY broke sub 7.2000 in earlier trade, but now sits back above this level. Still to come later today is Taiwan industrial production. Looking to tomorrow's calendar, we have consumer confidence early in South Korea, Thailand customs trade data and Singapore IP.

- All eyes were on the USD/CNY fix. In the event we printed lower, just back under 7.1000. This went against expectations of a higher result given the weaker CNY spot backdrop and higher USD index levels through Friday. This was a clear signal to the market of pushback to Friday's price action. USD/CNY spot fell to lows of 7.1943, completely unwinding Friday's gains. Aiding the move was headlines of state bank sellings USDs. We sit back near 7.2045 this afternoon though. USD/CNH got to 7.2325, which was around earlier highs in the pair from Jan/Feb this year. We have also recovered ground back to 7.2460/65.

- 1 month USD/KRW fell in sympathy with USD/CNH, but we found support sub the 1333 level and sit back near 1339 in current trade. Onshore spot is back above 1340. 1 month USD/TWD also fell, but sits comfortably above earlier lows, last at 31.85.

- The baht weakened sharply against the greenback on Friday by 0.9% reaching a high of 36.48 but today it pulled back a bit to a low of 36.23 helped by a lower US dollar and higher gold prices. USD/THB is currently little changed at 36.39 and is 1.6% higher over the last week as outflows continued.

- USD/PHP hasn't seen much downside, the pair last near 56.35, which is close to recent highs. The Bangko Sentral ng Pilipinas has rescheduled the Monetary Board's rate-setting meeting from April 4 to April 8 to await the release of March CPI data, which will be available on April 5. The press briefing to announce the rate decision will also take place on April 8.

INDONESIA: Indonesian Sov Debt Curve Flattens, Yields Lower, Budget Surplus

Indonesian USD sovereign debt curve has bull flattened on Monday, with yields 1-4bps lower across the curve. There has been little in the way of market headlines or economic data releases.

- The INDON sov curve has flattened on Monday with the 2Y yield -2bps at 4.925%, 5Y yield is -3bps at 4.875%, the 10Y yield is -3bps at 4.975%, while the 5-year CDS is also +1bp at 72.5bps

- The INDON to UST spread difference is mostly unchanged from Friday, the 2yr is 32bps (unchanged), 5yr is 68bps (+0.5bp), while the 10yr is 76.5bps (+1bps).

- In cross-asset moves, the USD/IDR is 0.11% higher, the JCI is 0.31% lower, Palm Oil is up 0.73%, while US Tsys yields are flat to 2bps lower.

- Foreign Investors sold bonds again on Thursday now marking 11 of 12 days of net selling. The 5-day average is now -$20m, the 20-day average is -$53m while the longer term 200-day average has turned negative at -$1.95m

- Indonesia reported a state budget surplus of IDR26 trillion in Feb, with state revenue at IDR400.4 trillion and state expenditure at IDR374.3 trillion. Notably, state revenue declined by 4.5% year-on-year, while state expenditure rose by 30.1%. Tax revenue amounted to IDR269 trillion, showing a 3.9% decrease year-on-year, resulting in a budget surplus equivalent to 0.11% of GDP.

- Looking ahead: Indonesia has a very quiet rest of the month in terms of data, with the next major data release not until April 1st

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 25/03/2024 | 0800/0900 | ** |  | ES | PPI |

| 25/03/2024 | 1000/1100 |  | EU | ECB's Lagarde at EIB Climate Council | |

| 25/03/2024 | 1100/1100 | ** |  | UK | CBI Distributive Trades |

| 25/03/2024 | 1225/0825 |  | US | Atlanta Fed's Raphael Bostic | |

| 25/03/2024 | 1400/1000 | *** | | US | New Home Sales |

| 25/03/2024 | 1415/1415 | | UK | BOE Mann At Royal Economic Society Annual Conference | |

| 25/03/2024 | 1430/1030 | ** | | US | Dallas Fed manufacturing survey |

| 25/03/2024 | 1430/1030 | | US | Fed Governor Lisa Cook | |

| 25/03/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 25/03/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 25/03/2024 | 1700/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.