Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

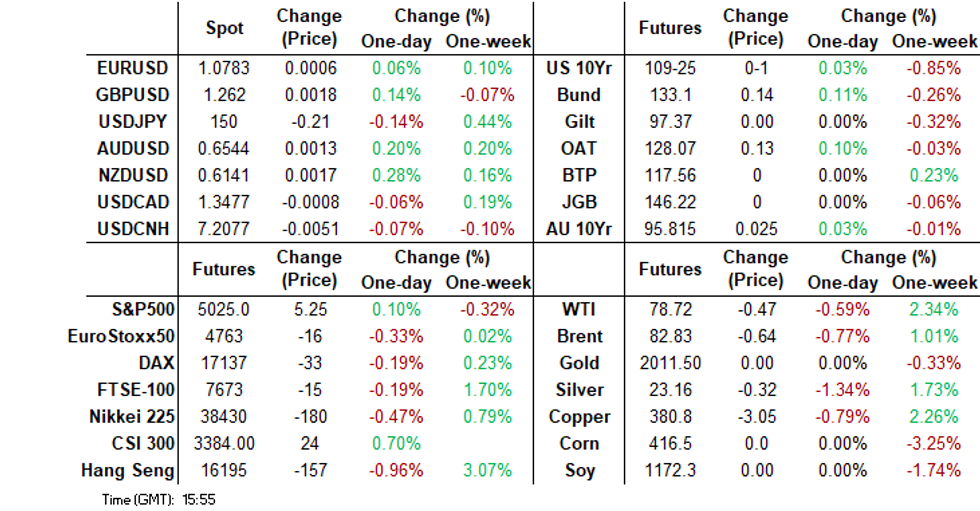

- Treasury futures are little changed in Asia trading, we have remained in a very tight range as volume has stayed on the light side. There has been little in the way of Asia data, the US is out today for President's day with no Cash treasury trading. The USD has drifted a little lower, with NZD outperforming at the margins.

- China Mainland equities reopened today but failed to deliver on expectations of a push higher. Mainland stocks outperformed Hong Kong equities, which gave up gains from last week. USD/CNH is down a touch, but hasn't been able to test 7.2000 at this stage.

- Oil prices have given up some of Friday’s gains during the APAC session today as China returned from holidays. Brent is down 0.7% to $82.87/bbl and has struggled to trade above $83 with equity sentiment mixed and demand again overtaking geopolitical concerns.

- Looking ahead it is a fairly quiet start to the week with the US President's Day holiday later.

MARKETS

US TSYS: Futures Steady Ahead of President's Day

TYH4 is currently trading at 109-24+, up + 00+ from New York closing levels.

Treasury futures are little changed in Asia trading, we have remained in a very tight range as volume has stayed on the light side. There has been little in the way of Asia data, the US is out today for President's day with no Cash treasury trading.

- Mar'24 10Y has traded in a tight range hitting a low of 109-23 in early trading before hitting a high of 109-27 as we head into Asia lunch we trade right in the middle of the range at 109-24+.

- Looking at technicals the break lower last week has confirmed a resumption of the down trend that started Dec 27. The 110-00 handle has been cleared and sights are on 109-17 while we tested this on Friday a clear break would open 109-05+, the Nov 28 low further down we would be looking at 108-19+ (61.8% of the Oct 19 - Dec 27 bull phase). While to the upside initial firm resistance is at 111-02+, the 20-day EMA.

- Looking head this week: President's Day today, while on Tuesday Philadelphia Fed Non-Manufacturing Activity and Leading Index (-0.1%, -0.3%). Treasury supply: $79B 13W, $70B 26W and $46B 52W bill auctions.

JGBS: Twist-Flattening, 20Y Supply Tomorrow, Wage Neg. Increase Chance Of March Policy Move

In Tokyo afternoon trade, JGB futures are unchanged compared to settlement levels on Friday.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Machinery Orders.

- (MNI) Recent BoJ communications and results from spring wage negotiations have increased the chance of policy adjustment at the upcoming March 18-19 meeting, a former BoJ board member told MNI. “The BoJ stands ready to exit from easy policy anytime,” noted Makoto Sakurai in an interview, pointing to a recent speech by Deputy Governor Shinichi Uchida and recent releases, such as the January meeting’s summary of opinions. “Everything is all arranged, and a final decision depends on Governor (Kazuo) Ueda’s determination.” (See link)

- With the domestic calendar light today and cash US tsys closed for the Presidents Day holiday, local market dealings have been subdued.

- Cash JGBs have twist-flattened, pivoting at the 7s, with yields 1.5bps higher to 3.2bps lower. The benchmark 10-year yield is 0.3bp lower at 0.732% versus the February low of 0.665% and the Nov-Dec rally low of 0.555%.

- Swaps and swap spreads are virtually unchanged.

- Tomorrow, the local calendar sees Tokyo Condominiums for Sale data, along with 20-year supply.

AUSSIE BONDS: Little Changed, Subdued Dealings, RBA Minutes Tomorrow

ACGBs (YM +1.0 & XM +0.5) are little changed in the Sydney session, amidst an overall subdued trading environment. Today, the domestic calendar has been light, and with cash US tsys closed for the Presidents Day holiday, local market activity has been quiet and lacking clear direction.

- Cash ACGBs are 1bp richer, with the AU-US 10-year yield differential 3bps lower at -9bps. At -9bps, the cash AU-US 10-year yield differential currently sits in the bottom half of the range of +/-30bps which has been observed since November 2022.

- Swap rates are flat to 1bp lower.

- Bills are little changed, with pricing +/- 1 across the strip.

- RBA-dated OIS pricing is little changed across meetings. A cumulative 35bps of easing is priced by year-end.

- Tomorrow, the local calendar will see the RBA Minutes of the Feb. Policy Meeting, ahead of the Wage Price Index (WPI) on Wednesday.

- The Q4 WPI is expected to rise 0.9% q/q with the annual rate rising to 4.1% y/y up from 4.0% in Q3. The RBA said in its February meeting statement that it didn’t expect wages growth “to increase much further” and that it “remains consistent with the inflation target” assuming productivity growth improves.

AUSSIE BONDS: AU-US 10-Year Yield Differential In The Bottom Half Of Range

Today, the AU-US 10-year cash yield differential has decreased by 3bps to -9bps after US tsys spiked to their highest levels for the year on Friday following the release of higher-than-anticipated PPI data.

- The 2-year yield surged to 4.72% following the data release before concluding 7bps points higher at 4.64%. Meanwhile, the 10-year yield experienced a 5bps increase to 4.28% after reaching an intraday peak of 4.33%. It is important to note, however, that cash US Treasuries are closed for the Presidents Day holiday.

- At -9bps, the cash AU-US 10-year yield differential currently sits in the bottom half of the range of +/-30bps which has been observed since November 2022.

- A simple regression of the AU-US cash 10-year yield differential against the AU-US 1Y3M swap differential over the current tightening cycle indicates that the 10-year yield differential is currently 16bps too low versus its fair value (i.e., -9bps versus +7bps).

- The 1y3m differential is a proxy for the expected relative policy path over the next 12 months.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: MNI – Market News / Bloomberg

NZGBS: Cheaper, NZ Treasury Secretary Warning About Long-Term Fiscal Pressures

NZGBs closed at session cheaps, with benchmark yields 2bps higher. That said, the session was subdued and directionless with the domestic calendar relatively light and cash US tsys closed for the Presidents Day holiday.

- Swap rates closed 4bps higher, with implied swap spreads wider.

- RBNZ dated OIS pricing is 1-9bps firmer across meetings, with November leading. A cumulative 38bps of easing is priced by year-end from a terminal rate of 5.64%. This compares with around 100bps of easing from an expected OCR peak of 5.53% in late January.

- NZ bonds held by foreigners rose to 61.6% in January from 61.3% prior.

- (Bloomberg) -- NZ Treasury Secretary McLiesh has issued a warning about the state of the country’s finances, saying it needs to address long-term fiscal pressures now even as persistent budget deficits make that more difficult. (See link)

- (Bloomberg) -- NZ Government is taking action “to curb the surge in welfare dependency that occurred under the previous government”. (See link)

- Tomorrow, the local calendar is empty, ahead of PPI data on Wednesday.

- RBNZ Governor Adrian Orr will speak at a Business Canterbury lunch on March 1. He will discuss factors impacting NZ’s economy from both a domestic and international perspective, and what to expect from the year ahead.

FOREX: USD Down Modestly, NZD Continues Outperformance

The dollar index sits lower, the BBDXY last near 1243.60, albeit up from earlier lows. Even with China markets returning today from the LNY break, it has been a relatively muted start to the week in terms of FX.

- With US markets closed later, there has been no cash Tsy trading today. Futures have been quiet, TYH largely unchanged versus end Friday levels in NY. US equity futures are positive, but away from best levels.

- NZD/USD has outperformed at the margins. The pair was last 0.6140, which is marginally above Friday highs and towards the top the monthly range. The 0.6150/55 level has been the barrier over the last month, a break above there could signal a test of the intraday highs from Jan 31 of 0.6174. While we trade above the 20 and 50-day EMAs of 0.6120/6135.

- Earlier local bank BNZ pushed back the timing of RBNZ cuts to November from August. The services PMI rebounded to 52.1 in Jan, from 48.8 prior.

- AUD/USD has lagged somewhat, albeit still marginally higher for the day. The pair was last 0.6540 , with weaker metal prices potentially weighing at the margin. SGX iron ore futures are off over 3%. Mixed anecdotes around China property sales through the LNY period may be a factor.

- For USD/JPY we have drifted lower, last near 150.00. We opened near 150.20. Speculation continues around the BoJ NIRP exit. The latest MNI policy insight is at this link, which looks at the chances of a shift at the March meeting.

- Looking ahead, US markets are closed later and there isn't much in the way of event risk elsewhere.

CHINA/HONG KOGN EQUITIES: Hong Kong Underperforming Mainland Equities Post LNY Break

China Mainland equities reopened today but failed to deliver on expectations of a push higher. Mainland stocks outperformed Hong Kong equities, which gave up gains from last week.

- As we head into the Asian lunch session, equities are mixed. Hong Kong equities are lower across the board, with the HSI down 1.00%, the HS Tech index lower by 2.71%, and mainland Property underperforming the market, down 3.00% today, erasing all gains from Friday. China Mainland equities have fared better today but fell short of the expected lofty heights. The CSI300 is currently trading up 0.37%, while the ChiNext trades 0.10% higher, and the CSI1000 is unchanged.

- Chinese property-developer shares declined due to weak holiday home sales following last week's rally. Home sales during the Lunar New Year holiday dropped 40%, indicating ongoing weak demand, leading to a retreat in Hong Kong-listed developers' stocks

- Consumer spending data looks promising, as state-owned media reported a 19% jump in travel during the LNY period compared to 2019. Box office sales reached 8.02 billion yuan, a record high, and railway travel surged 36% from the 2019 period.

- Looking ahead, Tuesday will see the 1-Year and 5-Year Loan Prime Rate due in China, while Hong Kong has Unemployment Rate data."

ASIA PAC EQUITIES: Regional Asian Equities Mostly Higher, South Korea Outperforms

Regional Asia Equities are mostly higher today, after a slow start this morning. The BBG Asia index 0.29% higher.

- Japan equities are mixed today, after a slow start this morning the weaker yen has helped equities move off their lows of the day. There has been little in the way of data today outside of Machinery orders coming in, inline with expected at 2.7% MoM, while a slight beat on YoY orders coming in at -0.7% vs -1.3%. The Nikkei 225 trades -.10%, while the Topix is 0.40% higher

- Taiwan is trading slightly higher today, led by Finance and Insurance names. While Spirox, who provide solutions and products to semiconductor sector is trading up 10% on very little news. Taiex is up 0.23%.

- South Korean equities are the top performers in the region today, hitting new highs not seen since May 2022. Foreign inflows have rebounded from a lull last week hitting $323m today, on expectations that the government will continue to support the market and close the "Korea Discount", Kospi is up 1.08%.

- Australian Equities are slightly higher today, up 0.26% led by the mining and industrials sectors. A2 Milk is up by 12.48% after an earnings beat.

- Thailand released GDP earlier coming in at 1.7% vs 2.6% estimated, equities trading 0.20% higher

- Elsewhere in SEA, New Zealand equities are the worst performers of the region down 0.60%, Philippines equities down ~0.20%, while Malaysia equities trade close to flat for the day

OIL: Crude Down As Excess Supply & Demand Uncertainties Drive Market

Oil prices have given up some of Friday’s gains during the APAC session today as China returned from holidays. Brent is down 0.7% to $82.87/bbl and has struggled to trade above $83 with equity sentiment mixed and demand again overtaking geopolitical concerns. WTI is 0.8% lower at $77.87 falling below $78 when China/HK markets opened. Trading is likely to be thin with the US closed for a holiday. The USD index is down slightly.

- The IEA wrote in its monthly report published last week that it expects demand will ease through 2024 and that the market will be in surplus throughout the year. China’s demand outlook remains a significant point of uncertainty.

- Geopolitical issues persist with no progress being made in resolving the conflict in the Middle East but they are yet to impact energy supplies apart from delays from rerouting around southern Africa. UKMTO reported today another vessel had been struck by Houthi rebels off the coast of Yemen with the crew abandoning the ship. The US said that it has struck five Houthi targets.

- The US and Canada are closed for holidays. There are no ECB or BoE speakers either. Attention this week is likely to be on geopolitical developments, US inventory data, the FOMC minutes and preliminary February PMIs.

POLITICAL RISK: Middle East Remains Tense, Ceasefire Talks “Not Promising”

Tensions in the Middle East have deteriorated with the conflict between Israel and Hezbollah in Lebanon escalating, further Houthi attacks on shipping and Qatar saying that ceasefire talks for Gaza were not progressing well. Issues in the region have supported oil prices, which are around 10% higher this year. But the last attack on US forces in the region was on February 4.

- The main risk of escalation in the region is between Israel and Hezbollah in Lebanon who have increased rocket attacks. Israel killed one of the group’s commanders last week. Hezbollah has said it will only stop attacking once there is a ceasefire in Gaza and will now not only attack military positions after it said Israel had killed civilians.

- An Iranian commander appears to have told Iranian-backed rebels to show restraint at the request of the Iraqi government, according to Reuters. Iran apparently wants to avoid the conflict expanding and Iraq wants discussions on the withdrawal of US troops from its soil to resume. The day after the visit one group, Kataib Hesbollah, said it would halt attacks. The US has 2500 troops in Iraq and 900 in Syria.

- Qatar said that ceasefire talks between Israel and Hamas were “not very promising” but PM Al Thani remained optimistic. Meanwhile an Israeli minister said that a ground offensive into Rafah will begin if the remaining Israeli hostages are not released by Ramadan which starts around the second week of March, according to Bloomberg. Israeli PM Netanyahu rejected unilateral recognition of a Palestinian state and said that it can only be negotiated with Israel.

- Attacks against merchant shipping around Yemen persist with the UK Maritime Trade Operations saying a vessel had reported a nearby explosion. These events have resulted in a large share of maritime traffic going around southern Africa instead of through the Suez Canal.

GOLD: Friday’s Gains Extended In Today’s Asia-Pac Session

Gold is 0.4% higher in the Asia-Pac session, after closing 0.5% higher at $2013.59 on Friday.

- Trading volumes have likely received a boost today as markets in China reopen following a week-long break.

- Bullion rose on Friday despite US Treasury yields spiking to their highest levels for the year following the release of higher-than-anticipated PPI data.

- The 2-year yield surged to 4.72% following the data release before concluding 7bps points higher at 4.64%. Meanwhile, the 10-year yield experienced a 5bps increase to 4.28% after reaching an intraday peak of 4.33%.

- Cash US Treasuries are closed today for the Presidents Day holiday.

- The market’s focus is now likely tuned to the release of the Federal Reserve minutes of its recent meeting midweek.

- While gold has edged back above its breakout level, a bearish theme does remain intact overall, according to MNI’s technicals team. The yellow metal needs to clear resistance at $2065.5, the Feb 1 high, to reinstate a bullish theme.

THAILAND DATA: Growth Disappoints, Rising Pressure On BoT

Thailand’s Q4 GDP print was disappointing showing the economy contracted 0.6% q/q sa to be up only 1.7% y/y in the final quarter of the year. 2023 growth slowed to 1.9% from 2022’s 2.6%. The economy was driven by private consumption and exports as government spending contracted and import growth improved. The government was already putting pressure on the Bank of Thailand to cut rates and that increased today with the NESDC saying monetary policy should boost the economy.

- BoT officials have pushed back against pressure saying that the economy’s underperformance is due to structural issues that monetary policy can’t affect and that the government needs to implement reform. There will be increased easing speculation ahead of the next BoT meeting on April 10.

Source: MNI - Market News/Refinitiv

- NESDC expects GDP growth of 2.2-3.2% in 2024 and that is to be driven by robust consumption but it is forecast to slow to 3% though.

- Domestic demand growth slowed in Q4 to 3.7% y/y from 4.1%. Private consumption growth remained robust rising 7.4% y/y slightly slower than Q3’s 7.9%. 2023 saw a pickup in growth to 7.1% from 6.2%.

- There is still considerable uncertainty re the implementation of the digital wallet scheme and if it will occur this year. It is expected to boost consumption once in place.

- Capex continued to be weak in Q4 falling 0.4% y/y after rising 1.5% y/y. Reform is needed to boost investment. There was an inventory build in Q4 but stocks detracted 0.7pp from annual growth.

- Government spending contracted 3% y/y an increase from Q3’s -5.0%. It is forecast to rise 1.5% y/y this year.

- Net exports continued to make a positive annual contribution to growth but significantly less than in Q3 as import growth picked up to +4% y/y from -9.4%. Exports rose 4.9% y/y up from 1.1%. NESDC projects a trade surplus in 2024 with the current account surplus at 1.4% of GDP.

Source: MNI - Market News/Refinitiv

ASIA FX: CNH Gains Slow On Modest Equity Bounce

USD/Asia pairs have been mixed to start the week. Much of the focus has been on the return of onshore China markets, but overall moves have been muted. USD/CNH sits a touch lower, last near 7.2100. The won has weakened a touch, despite another solid onshore equity rise. THB largely shrugged off a Q4 GDP miss. Tomorrow, we have the China 1yr and 5yr MLF decisions. The 5yr is expected to be cut by 10bps.

- USD/CNH was lower in the first part of trade, but couldn't test sub 7.2000. We last tracked bear 7.2090. Optimism was high around a positive equity open, which eventuated, but there wasn't much follow through. Weaker HK shares have weighed as well. Travel and spending data points to a pick up in activity through the LNY relative to prior years, but some housing market painted a still depressed picture.

- 1 month USD/KRW was supported sub 1330 in early trade, last tracking near 1333, slightly above end levels from NY trade on Friday. This comes despite a positive equity tone, although the correlation with the won is clearly lower over the past month. Tomorrow, consumer confidence prints for Feb. Later on this week the BoK is expected to remain on hold.

- USD/THB dipped in early trade, but found support just under 35.90, as Q4 GDP fell noticeably more than expected. We rebounded but couldn't get back above 36.00. Higher gold prices are likely helping THB at the margin. Thailand’s Q4 GDP print was disappointing showing the economy contracted 0.6% q/q sa to be up only 1.7% y/y in the final quarter of the year. 2023 growth slowed to 1.9% from 2022’s 2.6%. The economy was driven by private consumption and exports as government spending contracted and import growth improved. The government was already putting pressure on the Bank of Thailand to cut rates and that increased today with the NESDC saying monetary policy should boost the economy.

- USD/SGD sits lower, last near 1.3450. This is line with some USD softness against the majors. Earlier Feb lows rested back near 1.3350. The SGD NEER is little changed relative to the top end of the band compared to the end of last week, still -0.40%.

- USD/IDR has been relatively steady in spot terms, last near 15635. The 1 month NDF sits lower at 15650, versus closing levels at 15671 last week. This keeps us within recent ranges though. The BI decision is this Wednesday, with no change expected.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 19/02/2024 | 0700/0800 | *** |  | SE | Inflation Report |

| 19/02/2024 | 1330/0830 | * |  | CA | Industrial Product and Raw Material Price Index |

| 20/02/2024 | 0900/1000 | ** |  | EU | current account |

| 20/02/2024 | 1000/1100 | ** | | EU | Construction Production |

| 20/02/2024 | 1000/1000 | ** |  | UK | Gilt Outright Auction Result |

| 20/02/2024 | 1015/1015 | | UK | BOE's Bailey et al at TSC to discuss MPR | |

| 20/02/2024 | 1330/0830 | *** | | CA | CPI |

| 20/02/2024 | 1330/0830 | ** |  | US | Philadelphia Fed Nonmanufacturing Index |

| 20/02/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 20/02/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 20/02/2024 | 1800/1300 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 20/02/2024 | 1800/1300 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 21/02/2024 | 2350/0850 | ** |  | JP | Trade |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.