Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

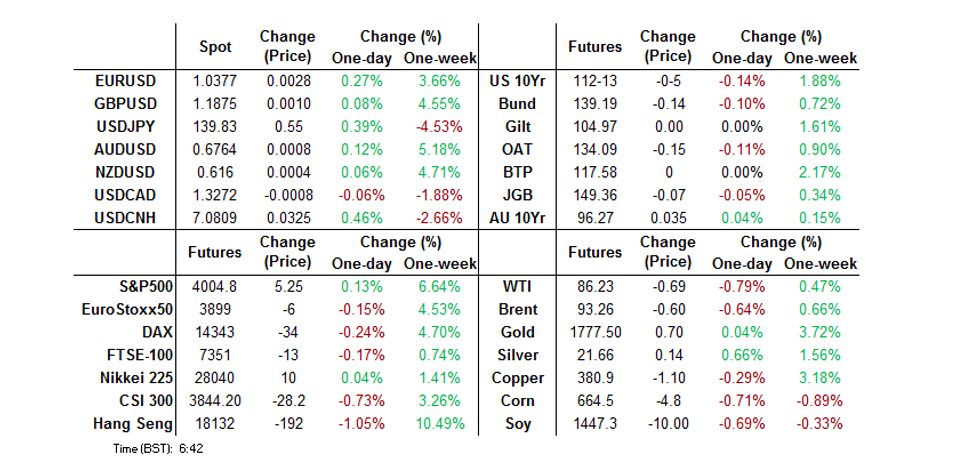

- G10 currencies with exposure to Eastern European geopolitics gained after U.S. President Joe Biden said it was "unlikely" that the missile that killed two people in Poland on Tuesday was fired from Russia, based on preliminary assessment of its trajectory. While Poland has announced an international probe into the incident, the broader perception was that the blast was likely a tragic accident rather than a deliberate strike, which would reduce the risk of a direct Russia-NATO confrontation.

- E-minis reversed early losses, while Chinese property developers were pressured by another capital raise in the sector.

- Inflation data from the UK and Canada, U.S. advance retail sales and industrial output, as well as a busy central bank speaker slate dominated by ECB members take focus from here.

US TSYS: Signs Of ‘Friendly Fire’ On Poland Allow Tsys To Cheapen

Tsys cheapened a touch in Asia, as U.S. President Biden suggested that the missile that hit Polish soil on Tuesday (killing 2 civilians) was “unlikely” to have been fired from Russia, with subsequent source reports pointing to a ‘friendly fire’ type incident surrounding the Ukrainian defence against the ongoing Russian missile attacks. This removed worry re: a direct Russian attack on a NATO member state, pressuring Tsys and supporting e-minis. There was little else to note in the way of tier 1 headline flow.

- That leaves the major cash Tsy benchmarks 3-5bp cheaper across the curve into London hours, with the intermediate zone leading the weakness, while the wings lagged the move.

- TYZ2 deals at the base if its 0-15 overnight range, -0-06 at 112-12, on above average volume of ~125K lots.

- A TY block sale (-1.3K) headlined on the flow side in Asia, with some desks indicating regional real money demand in several pockets of the curve.

- Wednesday’s NY docket is headlined by retail sales data, 20-Year Tsy supply and Fedspeak from Williams, Waller & Barr. Also note that the 2022 U.S. Treasury Market Conference will be held on Wednesday.

JGBS: Curve Twist Flattens, Signs Of Domestic Demand Propping Up Long End

JGB futures traded off of external factors, with the previously alluded to situation surrounding Tuesday’s missile situation in Poland (which killed 2 civilians) front and centre. Ultimately blame re: the matter was not laid at the feet of Russia and signs of a ‘friendly fire’ type of incident started doing the rounds.

- This saw the contract more than unwind its overnight gains, printing -9 into the bell.

- Meanwhile, cash JGBs saw some twist flattening, running 1.5bp cheaper to 2.5bp richer, pivoting around 10s. The lack of appeal when it comes to foreign bonds on the part of Japanese investors (owing to ongoing market vol. and elevated FX-hedging costs) may have contributed to this twist flattening, with the life insurer and pension fund community perhaps enticed by outright super-long JGB yield levels given the recent downside surprises in (still elevated) U.S. inflation ppints and the BoJ’s on hold stance.

- Local headline flow was limited at best.

- Looking ahead, Thursday’s local docket will be headed by trade balance data and 20-Year JGB supply. The weekly international security flow ledger from the MoF will also cross.

AUSSIE BONDS: Local Data Vs. Geopolitics

ACGBs came under some light pressure into the bell after AP source reports suggested that the missile that hit Polish land on Tuesday (killing two Polish civilians) “was fired by Ukrainian forces at an incoming Russian one,” per preliminary assessments flagged by U.S. officials. This came after U.S. President Biden suggested that it was” unlikely” that the missile was fired from Russia, while the G7 failed to lay the blame for the events at the feet of Russia. This left YM +4.0 & XM +3.5 at the close. Wider cash ACGBs print 3.5bp richer to 2.0bp cheaper, twist steepening with a pivot around 15s.

- Some light narrowing in EFPs provided modest support for ACGBs.

- Marginally firmer than expected Q3 WPI data was largely in line with the picture painted in the survey measures that have helped to guide monetary policy in recent months, so the readings don’t really represent much in the way of game changing information for the RBA at this juncture. This comes after the Bank slowed its pace of tightening to 25bp hikes over its last couple of meetings. Some post-data vol. ensued, before a bid came back in, aided by some firming in U.S. Tsys at the time.

- Bills were 1-11bp richer through the reds, bull flattening, generally following bonds, while RBA dated OIS was little changed on the day.

- Looking ahead, the monthly labour market report headlines the domestic docket on Thursday.

AUSTRALIA: Wages Rising But Not Yet A Concern For The RBA

The Wage Price Index rose slightly more than expected in Q3 at 1.0% q/q and 3.1% y/y. This was well above Q2’s 0.7% q/q and 2.6% y/y but still consistent with the RBA’s inflation target and below other developed countries. This data is not yet giving an indication of a wage-price spiral that the RBA is watching for signs of, but it is showing the effect of labour shortages.

- This was the highest quarterly increase in wages in over 10 years, driven by labour shortages, the 5.2% increase in the national minimum wage in July and end of financial year pay reviews. The latter two won’t be factors in the Q4 data.

- Private sector wages rose 1.2% q/q while public sector increased only 0.6%. The public sector is likely to catch up, as multi-year pay agreements expire and are re-negotiated. The trough in private sector wages led the public sector by around 3 quarters. 30% of public sector employees received a pay increase in Q3 but it averaged a muted 2.3%.

- The average size of private sector hourly pay increases rose further to 4.3% from 3.8% last quarter and 2.8% a year ago. This measure of wages has been running ahead of the private sector WPI.

- Almost half of private sector employees received an hourly wage increase (46.4%) compared to 33.9% in Q3 2021. Over half of these people had received their last pay rise a year ago.

- The July increase in the minimum wage was a major contributor to pay increases in the retail, administrative, accommodation and food sectors.

Source: MNI - Market News/ABS/SEEK

NZGBS: Off Best Levels, But Still Richer

NZGBs finished off best levels after an extension of the early richening linked to Tuesday’s firming of global core FI markets reversed a touch as it became apparent that Western powers were not willing to lay the blame of the missile that hit Polish territory (and killed two Polish civilians) on Tuesday squarely at the feet of Russia.

- Still, cash NZGBs were 3.5-4.5bp richer across the curve come the bell, with light bull flattening in play.

- Swap spreads were little changed come the close after some mixed performance at different stages of the session.

- RBNZ dated OIS pricing was incrementally softer, with ~63bp of tightening priced for next week’s meeting, while terminal OCR pricing sits around 5.05%.

- Local data revealed an uptick in non-resident NZGB bond holdings.

- Looking ahead, tomorrow will see the release of Q3 PPI data.

FOREX: European FX Get Reprieve From Missile Updates, Greenback Buoyed By Higher U.S. Tsy Yields

G10 currencies with exposure to Eastern European geopolitics gained after U.S. President Joe Biden said it was "unlikely" that the missile that killed two people in Poland on Tuesday was fired from Russia, based on preliminary assessment of its trajectory. While Poland has announced an international probe into the incident, the broader perception was that the blast was likely a tragic accident rather than a deliberate strike, which would reduce the risk of a direct Russia-NATO confrontation.

- Biden's comments allowed EUR to become the best performer among major currencies, with the likes of DKK and SEK also finding poise. The Norwegian Krone lagged behind its Scandie cousins amid softer crude oil prices. Spot EUR/PLN topped out at at PLN4.7848 but then trimmed the bulk of its initial gains on Biden's remarks.

- The BBDXY index came under pressure as the POTUS spoke, virtually erasing its initial 0.26% upswing. Selling interest quickly dissipated, with the index advancing to new session highs, as the greenback rebounded towards the top of the G10 scoreboard, supported by higher U.S. Tsy yields.

- The combination of geopolitical relief and sell-off in U.S. Tsys generated yen underperformance. Spot USD/JPY rallied past the Y140 mark, lodging session highs at Y140.29 but falling short of testing yesterday's peak.

- Data showing continued decline in China's new home prices facilitated the upswing in USD/CNH. The value of new residential properties fell 0.37% M/M last month, which was the fastest pace of decline since Feb 2015.

- Inflation data from the UK and Canada, U.S. advance retail sales and industrial output, as well as a busy central bank speaker slate dominated by ECB members take focus from here.

FX OPTIONS: Expiries for Nov16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0200-10(E1.8bln), $1.0250-55(E1.0bln), $1.0500(E508mln)

- USD/JPY: Y137.50($500mln), Y140.00-10($777mln), Y140.75-00($840mln), Y147.90-00($1.1bln)

- USD/CNY: Cny7.2000($2.6bln), Cny7.3000($3bln)

ASIA FX: Geopolitical Risk, China's Home Price Data Dent Asia EM Currencies

Asia EM FX underperformed the greenback across the board amid concerns over the Poland/Russia situation and continued decline in China's new home prices. The Bloomberg/J.P. Morgan Asia Dollar Index (ADXY) snapped a four-day winning streak and pulled back below the 99 mark.

- CNH: The upswing in spot USD/CNH was facilitated by the release of data on China's new home prices. The value of residential properties fell 0.37% M/M last month, the fastest pace of decline since Feb 2015, after September's 0.28% contraction. The PBOC fix matched the sell-side estimate.

- KRW: South Korean won was the worst performer in the region amid heightened geopolitical risk associated with a Russian-made missile blast in Poland. There was speculation that the news may have triggered profit-taking after the recent retreat in USD/KRW.

- IDR: Spot USD/IDR advanced on the eve of Bank Indonesia rate decision, which will likely see policymakers raise the 7-Day Reverse Repo Rate. Palm oil futures operated near unchanged levels.

- MYR: The ringgit was firmer than its peers from emerging Asia but struggled to gain versus the greenback, even as spot USD/MYR briefly showed below the MYR4.5 figure.

- PHP: Bangko Sentral ng Pilipinas is expected to deliver the pre-announced 75bp rate hike at tomorrow's meeting. The Philippine peso weakened through the session.

- THB: The baht faltered as foreign investors were net sellers of Thai stocks for the second consecutive day Tuesday.

MNI Bank Indonesia Preview - November 2022: Another 50bp To Support IDR

EXECUTIVE SUMMARY

- Bank Indonesia (BI) meets on November 17 and is widely expected to hike rates another 50bp to 5.25%, bringing rates to their highest since September 2019.

- 8 of the 28 analysts surveyed by Bloomberg expect a lower 25bp move. The moderation in October headline CPI inflation and the slight appreciation of the USDIDR in recent days suggest that the risks to the 50bp forecast are skewed to the downside.

- Stabilising the IDR, bringing core inflation back to target, and ensuring financial stability in the context of a robust economy are again likely to be the focus of the November meeting. A 50bp move this month would still see the Indonesian-US rate differential narrow.

- For the full piece, see here.

MNI BSP Preview - November 2022: Keeping Up With Fed

EXECUTIVE SUMMARY

- Governor Medalla guided that the Bangko Sentral will be raising the key policy rate by 75bp come the end of this week's monetary policy review, in order to keep the interest-rate differential with the U.S. unchanged.

- Inflation continues to quicken amid higher food prices, with the local statistics authority warning that it may gather more pace in the coming months on the back of the recent typhoons.

- The Philippine peso has been the worst performer in emerging Asia this year, accentuating imported inflation. The onus is on the BSP to rescue the domestic currency, which comes under additional pressure from the Philippines' "twin deficit."

- Please use the following link to access the full preview: MNI BSP Preview November 2022.pdf

GOLD: Edging Away From Tuesday’s Peak

The yellow metal has ticked away from Tuesday’s highs in Asia-Pac trade, last dealing a little over $5/oz softer on the day, printing just above $1,770/oz.

- A reminder that Tuesday’s session high was a product of softer than expected U.S. PPI data, with a re-test coming on the back of news of a missile falling in Polish territory (which killed two Polish civilians).

- An Asia-Pac rally in the greenback, which has seen the broader DXY pare the bulk of Tuesday’s losses, alongside a light uptick in U.S. Tsy yields, after western powers chose not to lay the blame re: the Polish missile situation at the feet of the Russians (U.S. President Biden suggested that it was “unlikely” that the missile was launched from Russia), has weighed on gold overnight.

- Fedspeak & policy trajectory, as well as U.S. inflation dynamics, continue to present the most meaningful fundamental inputs for gold in the immediate term.

- Technically, last week’s gains resulted in the break of a number of important resistance points. The yellow metal has cleared the Oct 4 high ($1729.50/oz). This strengthens the current bullish theme and paves the way for an extension towards $1800/oz, with key resistance located above that particular round number resistance in the form of the Aug 10 high ($1807.90/oz). On the downside, initial firm support is seen at the Nov 9 low ($1,702.30/oz).

OIL: Prices Range Bound Again On Difficult Political Environment

Oil prices have been trading in a tight range. Even the short-lived bounce in reaction to reports of a Russian-made missile exploding in Poland didn’t break out. WTI has been between $87.50 and $86.35/bbl and is now at the lower end of the range on the back of USD gains. Brent traded between $93.40 and $94.10 and is now around $93.40. Prices are about 0.5%below the NY close.

- US API data showed that the previous week’s build in crude was more than unwound in the latest week with stocks falling 5.835mn bbl. Distillate stocks rose slightly by 0.9mn bbl and gasoline by 1.7mn.

- The IEA noted in its November report that crude inventories in developed countries were at their lowest since 2004, making them vulnerable to further supply disruptions. It also reported that OPEC+ output remains more than 1mbd below the quota.

- Tight supply conditions balancing uncertainty regarding the demand outlook continue to keep oil prices range bound. Deterioration in the situation in the Ukraine could increase supply fears and reopening in China could improve the demand outlook and thus push prices higher again.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 16/11/2022 | 0700/0700 | *** |  | UK | Consumer inflation report |

| 16/11/2022 | 0700/0700 | *** | | UK | Producer Prices |

| 16/11/2022 | 0900/1000 | *** |  | IT | HICP (f) |

| 16/11/2022 | 0900/1000 | ** | | IT | Italy Final HICP |

| 16/11/2022 | 0930/0930 | * | | UK | ONS House Price Index |

| 16/11/2022 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 16/11/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 16/11/2022 | - |  | ID | G20 Summit in Indonesia | |

| 16/11/2022 | - |  | TH | APEC Leaders’ Summit | |

| 16/11/2022 | 1315/0815 | ** |  | CA | CMHC Housing Starts |

| 16/11/2022 | 1330/0830 | *** | | CA | CPI |

| 16/11/2022 | 1330/0830 | *** | | US | Retail Sales |

| 16/11/2022 | 1330/0830 | ** | | US | Import/Export Price Index |

| 16/11/2022 | 1415/0915 | *** | | US | Industrial Production |

| 16/11/2022 | 1415/1415 | | UK | BOE Treasury Select Committee hearing on Nov Monetary Policy Report | |

| 16/11/2022 | 1450/0950 | | US | New York Fed's John Williams | |

| 16/11/2022 | 1500/1000 | * | | US | Business Inventories |

| 16/11/2022 | 1500/1000 | ** | | US | NAHB Home Builder Index |

| 16/11/2022 | 1500/1600 |  | EU | ECB Lagarde Speech at European School Frankfurt Anniversary | |

| 16/11/2022 | 1500/1600 | | EU | ECB Panetta at ABI's Executive Committee Meeting | |

| 16/11/2022 | 1500/1000 | | US | Fed Vice chair for Supervision Michael Barr | |

| 16/11/2022 | 1530/1030 | ** | | US | DOE weekly crude oil stocks |

| 16/11/2022 | 1800/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 16/11/2022 | 1935/1435 | | US | Fed Governor Christopher Waller | |

| 16/11/2022 | 2100/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.