Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

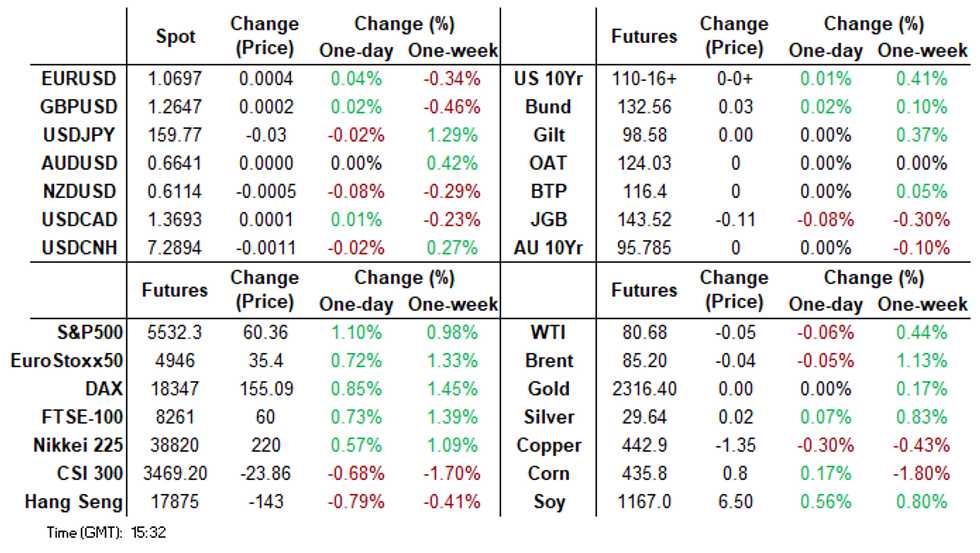

- The Japanese Yen continues it's recent sell-off and now now trading just under 160.00 vs the USD. Investors remain cautious around whether or not the BoJ will intervene in the market

- China & Hong Kong markets declined as investor sentiment soured amid a weak macroeconomic outlook and heightened geopolitical tensions

- NZ Exports To US Strong While Struggling To China, the country recorded a merchandise trade surplus of $204mn for May after a small deficit of $3mn

- The BoJ board members were divided on the timing of rate hike at the June meeting

Source: MNI - Market News/Bloomberg

MARKETS

US TSYS: Tsys Futures Steady Ahead Of Fed Speakers Later

- Treasuries futures are little changed today as traders are awaiting remarks from Federal Reserve officials later on Monday to get any clues about the timing of a future interest-rate cut. TUU4 is -0-00+ at 102-05⅝, while TYU4 is +0-00+ at 110-16+

- Volumes: TU 28k FV 35k TY 71k

- Tsys Flows: Block Fly TU, TY, WN, buyer of TY, DV01 315k

- Cash treasury curve is little changed today, ranges have been very tighter with the 2Y +0.2bps at 4.734%, 5Y -0.5bp at 4.269% while the 10Y is -0.6bp at 4.250%

- APAC markets: ACGBs are +/- 1bps, earlier there was a 29 auction which went smoothly but less demand than prior auctions, NZGBs are 2-3bps lower, while the JGB curve has bear-steepened, yields are 1-4bps higher, while the JPY eyes 160.00

- Projected rate cut pricing remains steady to mildly lower vs. this morning's levels (*): July'24 at -10% w/ cumulative at -2.5bp at 5.302%, Sep'24 cumulative -17.6bp (-18.4bp), Nov'24 cumulative -26.6bp (-27.8bp), Dec'24 -46.7bp (-47.2bp).

- Looking ahead, Dallas Fed Manf. Activity and Fed speak

ACGBS: Slightly Cheaper, Focus On Wednesday’s CPI Monthly

ACGBs (YM -2.0 & XM flat) are slightly cheaper after dealing in narrow ranges in a data light Sydney session.

- Cash US tsys are flat to 1bp richer in today’s Asia-Pac session after finishing last week with a directionless NY session.

- Cash ACGBs are flat to 1bp cheaper, with the AU-US 10-year yield differential at -4bps.

- Swap rates are flat.

- The bill strip pricing is flat to -1.

- RBA-dated OIS pricing is little changed. A cumulative 14bps of easing is priced by year-end.

- Tomorrow, the local calendar will see Westpac Consumer Confidence. The slightly more hawkish sounding RBA on June 18 is likely to keep sentiment weak and maybe even drive a further fall.

- However, the focus will be on May’s CPI Monthly on Wednesday. The May CPI is expected to post an increase of 3.8% y/y up from 3.6% the previous month. Forecasts range from 3.5% to 4.0% with most around 3.7-3.8%. April did not include a comprehensive update of the services components, but May will. Housing costs, insurance, electricity prices and personal services are likely to rise.

- RBA Assistant Governor Kent speaks on Wednesday at 0935 AEST and Deputy Governor Hauser on Thursday at 2000 AEST.

NZGBS: Closed Richer, Light Local Calendar Until Thursday

NZGBs closed near the session’s best levels, 2-3bps richer, after subdued trading.

- The previously outlined Trade Balance data failed to be a market-mover despite total exports hitting a record monthly high.

- Domestic spending on all cards fell 0.6% m/m, -0.1% y/y, in May according to RBNZ data.

- NZ-US and NZ-AU 10-year yield differentials closed ~2bp tighter and flat respectively.

- Swap rates are 3-4bps lower.

- RBNZ dated OIS pricing is slightly softer for 2025 meetings. A cumulative 30bps of easing is priced by year-end.

- “Investors are pricing in more rate cuts through end-2025 for New Zealand than Australia, but that divergence won’t last, according to a note Friday from Goldman Sachs strategists led by George Cole.” About 120bp of cuts are priced for the RBNZ through the end of next year vs ~50bp for the RBA, Goldman says (per BBG).

- Tomorrow, the local calendar is empty, with the next data release being Consumer and Business Confidence on Thursday.

JGBS: Futures Holding Weaker, PPI Services & 20Y Supply Tomorrow

JGB futures are weaker, -9 compared to the settlement levels, but well above session lows.

- (MNI) BoJ board members were divided on the timing of rate hike at the June 13-14 policy-setting meeting, the summary of opinions showed on Monday. Some board members saw the need to consider raising the policy interest rate appropriately. Another member noted, that although price developments were on track to achieve the 2% price-stability target in the second half of fiscal 2025, "upside risks to prices have become more noticeable.” (See link)

- (MNI BoJ Watch) The BoJ wants to establish a broad framework that will make buying and selling JGBs easier, as the bank contemplates how it will execute a reduction to its purchases should the Board direct it to do so at July's meeting, MNI understands. (See link)

- Cash US tsys are flat to 1bp richer in today’s Asia-Pac session.

- Cash JGBs are flat to 4bps cheaper across benchmarks. The benchmark 10-year yield is 2.0bps higher at 0.995% versus the cycle high of 1.101%.

- The swaps curve has bear-steepened, with rates flat to 4bps higher. Swap spreads are tighter.

- Tomorrow, the local calendar will see PPI Services, Leading & Coincident Indices and Machine Tool Orders data alongside 20-year supply.

GOLD: Hurt By Strong US Flash PMIs

Gold is slightly higher in the Asia-Pac session, after closing 1.6% lower at $2321.98 on Friday following stronger-than-expected US PMI data, which in turn provided a USD bid.

- The US composite flash PMI rose to 54.6, marginally above the May reading, and a two-year high suggesting growth is holding up reasonably well.

- Over the week, the yellow metal fell a modest 0.5%. Nevertheless, it remains up ~12% this year.

- According to MNI’s technicals team, bullion’s sharp sell-off on Jun 7 reinforced a short-term bearish theme. The yellow metal recently pierced the 50-day EMA, at $2,317.69, a clear break of which would open $2,277.4, the May 3 low. Initial firm resistance is $2,387.8, the Jun 7 high.

OIL: Crude Down Slightly, Attacks On Shipping Continue

Oil is off the day’s lows to be only slightly lower during APAC trading. Brent is down only 0.1% to $85.20/bbl after a low of $84.71 despite softer risk appetite. WTI is also 0.1% lower at $80.65/bbl following a fall to $80.23. The USD index is flat.

- Oil fell on Friday after it flashed overbought according to the relative strength index. Market participants remain bullish though with net longs in Brent rising 68k last week, the most since 2011, according to data from ICE Futures Europe and Bloomberg. The market is expected to tighten over Q3 and prompt spreads are consistent with this.

- A ship was struck by Houthi drones off the coast of Yemen on Sunday. According to the UK Navy, the ship had to be abandoned. Today the US reported another vessel had been damaged in the area. Threats to shipping persist and are pushing costs higher.

- Later the Fed’s Waller, Goolsbee and Daly appear as well as the ECB’s Buch, Schnabel and BoC’s Macklem. The Dallas Fed June index and German Ifo for June print.

LNG: Gas Prices Fall As Supply Disruptions Ease

European LNG prices fell 1.5% on Friday to EUR 33.95 on an improved supply situation after trending lower from its EUR 34.70 high early in the session as the supply situation improved. They are now down slightly in June.

- The EU agreed on further sanctions on Russia, according to Reuters. Russian ships carrying LNG will also not be able to use European imports unless they’re unloading LNG for European consumption, which will impact supplies going to Asia. Investment in and supply of materials/services to Russian LNG projects will also not be allowed. Pipeline flows through Ukraine continue as normal.

- While Norway’s gas facilities continue to undergo planned seasonal maintenance, flows are at their highest since 2021 for this time of year.

- The repairs at Australia’s Wheatstone are completed and full LNG and domestic gas activity resumed on the weekend, which should reduce risks to Asian supplies.

- US natural gas fell 2.2% to $2.68 to now be up 3.3% this month. Prices peaked on June 11 at $3.16 and have trended lower since. The EIA reported a 71bcf inventory build in the week to June 14.

- North Asian prices were also lower down 1.4% on Friday to be up 3.3% in June. Hot weather has boosted demand through increased air conditioning usage. But the resolution of recent supply disruptions has put downward pressure on prices.

ASIA STOCK: Mixed Equity Flows Across Asia On Friday

- South Korean equities experienced outflows of $176 million on Friday. Despite this, the past 5 trading sessions have netted a total inflow of $778 million. This recent activity aligns with the 5-day average inflow of $155.6 million, which is significantly above the 20-day average of $58.4 million and the longer-term 100-day average of $151.3 million. Year-to-date, South Korean equities have seen a substantial inflow of $16,776b.

- Taiwanese equities saw significant outflows of $486 million on Friday. However, the past 5 trading sessions recorded a strong net inflow of $2,579b. This recent activity surpasses the 5-day average inflow of $515.9 million, which is well above the 20-day average of $40.1 million and the 100-day average of $106.7 million. Year-to-date, Taiwan has accumulated a total inflow of $6,575b.

- Thai equities had outflows of $43 million on Friday, bringing the 5-day total to a net outflow of $291 million. The 5-day average outflow is $58.1 million, which is slightly above the 20-day average of $52.7 million and more than double the 100-day average of $23.9 million. Year-to-date, Thailand has seen significant outflows amounting to $2,992b.

- Philippine equities experienced outflows of $23 million on Friday, contributing to a 5-day total outflow of $49.2 million. The 5-day average outflow of $9.8 million is less than the 20-day average outflow of $11.7 million and the 100-day average outflow of $5.8 million. Year-to-date, the Philippines has seen outflows totaling $528 million.

- Indonesian equities experienced inflows of $70 million on Friday. Over the past 5 trading days, Indonesia recorded a total net inflow of $159 million. The 5-day average shows an outflow of $31.7 million, which is an improvement compared to the 20-day average outflow of $26.0 million and the 100-day average outflow of $7.0 million. Year-to-date, Indonesia has experienced outflows totaling $457 million.

- Indian equities attracted inflows of $149 million on Friday, contributing to a robust 5-day total inflow of $2,157b. The 5-day average inflow of $431.4 million is notably higher than the 20-day average of $87.3 million. Despite this, the 100-day average still shows a slight outflow of $16.7 million. Year-to-date, India has seen outflows amounting to $1,561b.

- Malaysian equities recorded outflows of $37 million on Friday. The past 5 trading days have seen a total net outflow of $64 million. The 5-day average outflow of $21.2 million is higher than the 20-day average outflow of $5.8 million and the 100-day average outflow of $1.8 million. Year-to-date, Malaysia has experienced outflows totaling $97 million.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | -176 | 778 | 16776 |

| Taiwan (USDmn) | -486 | 2579 | 6575 |

| India (USDmn)* | 149 | 2157 | -1561 |

| Indonesia (USDmn) | 70 | 159 | -457 |

| Thailand (USDmn) | -43 | -291 | -2992 |

| Malaysia (USDmn) | -37 | -64 | -97 |

| Philippines (USDmn) | -23 | -49.2 | -528 |

| Total | -546 | 5269 | 17716 |

| * Up to 20th June |

ASIA STOCKS: HK & China Equities Head Lower, On Lack Of Policy Support

The China and Hong Kong markets experienced declines on Monday as investor sentiment soured amid a weak macroeconomic outlook and heightened geopolitical tensions. The Shanghai Composite Index and CSI 300 Index both faced significant losses, with the Shanghai index set to erase its year-to-date gains. Similarly, the Hang Seng Index in Hong Kong fell to its lowest levels in nearly two months, driven by a lack of significant policy support and disappointing economic data.

- Hong Kong equities are lower today with the HSI Index dropping 1.02% heading towards its lowest close since April 30, the HSTech Index also declined by 1.75%, in the property space the Mainland Property Index dropped 1.00%, while the HS Property Index fell 0.78% Investor sentiment was further dampened by the lack of fresh supportive measures and underwhelming economic data, including a 28.2% drop in foreign direct investment from January to May.

- In mainland China, equities are well off morning lows with the Shanghai Composite Index down 0.70% vs 1.28% early morning. The CSI 300 Index is down 0.16%, and was less than 2% away from erasing its year-to-date gains. The MSCI China Index is also nearing a similar milestone, being about 5% away. Broader market indices faced even sharper declines, with the CSI 1000 and CSI 2000 indices falling by 2.26% and 3.03%, respectively. The CSI 300 Real Estate Index decreased by 1.63%, while the ChiNext Index was down by 0.61%.

- Property space, Kaisa Group Holdings, a Chinese developer facing liquidation in a Hong Kong court, must demonstrate progress in restructuring its $11 billion debt. Despite defaulting on offshore bonds over two years ago, Kaisa has yet to present a public restructuring plan. This week, several Chinese property companies, including DaFa Properties, Shimao Group, and Redsun Properties, also face court hearings amid the ongoing property debt crisis. Recent government measures to rescue the sector have had limited impact, with many firms' dollar notes trading at deeply distressed levels.

- China and the European Union have agreed to start talks on the EU's plans to impose tariffs of up to 48% on Chinese electric vehicles, following EU investigations into alleged unfair trade practices. This agreement was reached during a video conference between Chinese Commerce Minister Wang Wentao and EU Trade Commissioner Valdis Dombrovskis, with further discussions expected in the coming weeks to avoid a tariff war.

- Looking ahead, it is a quiet week for China, while Hong Kong has trade balance data on Tuesday

ASIA STOCKS: Regional Asian Equities Mixed, Japanese Equities Gain On Weaker Yen

Asian markets are experiencing a mixed trading session today. The MSCI Asia Pacific Index is down by as much as 0.6%, marking its third consecutive day of losses. The decline is led by drops in tech shares, with notable decreases seen in companies like TSMC, Tencent, and SK Hynix. Japanese stocks fluctuated within a tight range as automakers benefited from a weaker yen while chip-related stocks declined following a selloff led by Nvidia in the US. Investors are eagerly awaiting key US inflation data later this week, which could provide further insights into the Federal Reserve's monetary policy direction. Geopolitical concerns, including the upcoming US presidential debate and the French election, are also contributing to cautious trading sentiment across Asian markets.

- Japanese stocks are higher this morning with the Topix up 0.80% & Nikkei up 0.63%. The weaker yen has help exporter, the yen hovered around 159.89 per dollar, nearing the intervention levels seen earlier this year. Japan's top currency official reiterated the readiness to intervene if necessary, maintaining pressure on the yen's depreciation.

- South Korean equities are 0.85% lower this morning, as investors remained cautious ahead of key US data and corporate earnings. Samsung Electronics was flat, while SK hynix declined by 2.56%. Hyundai Motor and Kia pulled back by 0.18% and 0.23%, respectively. Battery shares also started in negative territory. On the other hand, steel giant POSCO Holdings gained 0.55%, and leading chemical producer LG Chem rose by 0.28%. The calendar is empty in the region today.

- The Taiex is 1.75% lower today, led by declines in semiconductor stocks. TSMC decreased by 2.3%, contributing the most to the index decline. Min Aik Precision Industrial Co. had the largest drop, falling by 5.7%. Later today we have unemployment and industrial production data due out.

- In Australia, the S&P/ASX 200 is 0.75% lower as investors await inflation reading later in the week that could influence the Reserve Bank of Australia's monetary policy. Australia's 10-year real yields rose by 1.8 basis points to 1.87%. The upcoming inflation data is expected to show an acceleration in annual inflation, which may present a policy challenge for the Reserve Bank of Australia, given the need to balance inflation control with economic growth.

- Elsewhere, New Zealand equities are 0.48% lower, Singapore equities are 0.05% lower, Malaysia are 0.05% lower, India is 0.30% lower while Indonesia up 0.15% and Philippines equities up 0.55%.

FOREX: FX Range Trading, IDR Weaker Than At Last Week’s BI Meeting

FX moves have been limited during APAC trading today. The US dollar is little changed with the BBDXY index around 1267.92, close to the mid-April high. Kiwi has been the largest mover in the G10 in a generally weaker risk environment with NZDUSD falling 0.1% to 0.6114 off the intraday low of 0.6105.

- USDJPY rose to 159.92 as FX chief Kanda spoke about being prepared to intervene if yen moves are “excessive”. It trended lower on the release of the BoJ summary of opinions. The pair found a floor around 159.63 when finance minister Suzuki spoke on FX stability. The pair is currently down slightly on the day at 159.77.

- AUDUSD has range traded and is little changed at 0.6640 despite weaker equities but is off the intraday low of 0.6626. AUDNZD is 0.1% higher at 1.0861.

- European currencies are little changed with EURUSD at 1.0698 and GBPUSD 1.2649.

- The USDCNY fix printed at 7.1201 today after 7.1196 on Friday. This resulted in USDCNH jumping to 7.2946 briefly but currently it is around 7.2892 after a low of 7.2871.

- Asian currencies are also little changed with USDKRW up slightly to 1388.80.

- USDIDR is down 0.1% to 16440 after starting today around 16478, still higher than where it was when Bank Indonesia left rates unchanged last week. Governor Warjiyo said today that BI will continue to intervene and use its other instruments to support the rupiah but it sees the currency appreciating towards its “fundamental value”.

- The baht is struggling again with USDTHB up 0.2% to 36.74 but off the intraday high of 36.81. The pair is lower than its June 10 high of 36.94 to be down 0.1% this month but the market has been concerned about the government’s fiscal plans and political stability.

NZ DATA: Exports To US Strong While Struggling To China

NZ recorded a merchandise trade surplus of $204mn for May after a small deficit of $3mn. The YTD deficit narrowed moderately to $10.05bn from $10.22bn and appears to have stalled around here. Exports rose 2.9% y/y outpacing imports at 0.6% y/y. The trade position is being helped by strong demand from the US, NZ’s second largest destination.

NZ merchandise trade balance $bn YTD

Source: MNI - Market News/Refinitiv

- Exports to the US rose 33.2% y/y in May, driven by beef, compared with shipments to China falling 11.6% y/y. They were weak to Australia but rising solidly to both Japan and Europe. Statistics NZ observes that May was the first time that exports to the US reached the $1bn mark.

Source: MNI - Market News/Refinitiv

- Imports are soft in line with the weakening domestic economy. Consumer goods rose only 1.6% y/y while plant & equipment fell 13.5% y/y.

- Export growth in May was driven by wine, food preparations and precious metals & jewellery. Imports of petroleum, cereals and sugar were strong. The data is nominal and so is impacted by price movements, especially for volatile commodities.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/06/2024 | 0700/0300 |  | US | Fed Governor Christopher Waller | |

| 24/06/2024 | 0800/1000 | *** |  | DE | IFO Business Climate Index |

| 24/06/2024 | 1000/1100 | ** |  | UK | CBI Industrial Trends |

| 24/06/2024 | 1300/1500 | ** |  | BE | BNB Business Sentiment |

| 24/06/2024 | 1430/1030 | ** | | US | Dallas Fed manufacturing survey |

| 24/06/2024 | 1530/1730 |  | EU | ECB's Schnabel in panel on 'Investing in Sovereignty" | |

| 24/06/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 24/06/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 24/06/2024 | 1730/1330 |  | CA | BOC Governor Macklem speech in Winnipeg. | |

| 24/06/2024 | 1800/1400 | | US | San Francisco Fed's Mary Daly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.