Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

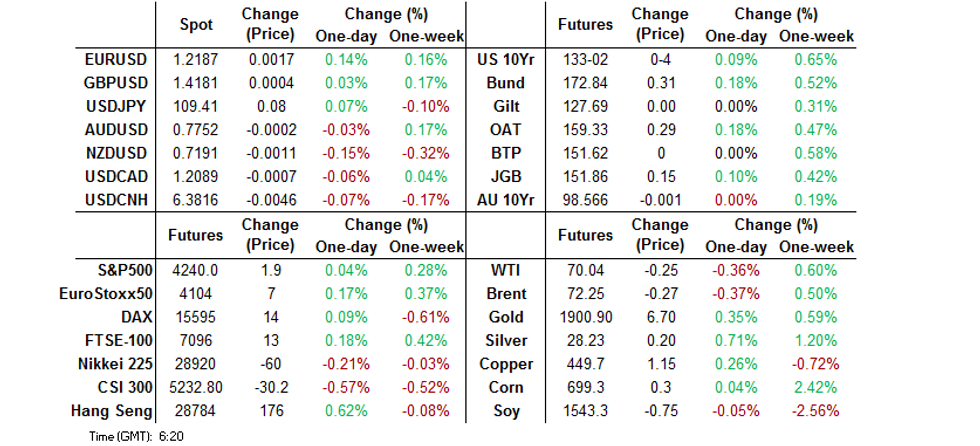

- Next week's risk events, namely surrounding the Fed & RBA, get most of the focus in Asia given a lack of meaningful news flow.

- U.S. Tsys consolidate the bulk of their recent rally.

- Central bank speak from the ECB & BoE headlines the broader docket into the weekend.

BOND SUMMARY: Plenty To Note Moving Into The Weekend

The latest fiscal headlines from the U.S. pointing to an agreement between a bipartisan group of Senators re: infrastructure have done little for the market, with the blessing of both party leaderships still required and questions from the White House emerging (although the latter has expressed a willingness to work with the group). T-Notes have stuck to a 0-04 range overnight dealing just off of best levels at typing, last +0-04+ at 133-02+ on decent enough volume of just over 103K, with cash Tsys trading roughly 0.5-1.0bp cheaper across the curve. Flow was headlined by a 5.0K block seller of FVU1.

- JGB futures have built on their overnight rally but trade a little off of best levels, with JBU1 now trading +15 on the day. Cash JGBs have richened across the curve, with focus on the offshore market impetus and then the local spill over. The 5- to 10-Year sector outperforms, richening by a little over 2.0bp, with 10-Year yields moving decisively below 5bp for the first time since late January. Long end swap spread tightening has been evident for a second day, with signs of foreign receiving showing up in the JSCC/LCH basis for 30-Year swaps. Broader news flow remains light. Locally, speculation in the local press re: spectators at the Olympics continues to do the rounds, while the latest quarterly BSI survey failed to impact markets.

- Outside of an early blip lower at the Sydney re-open there has been little to note for the Aussie bond space, with the tail end of the futures rolls taking most of the focus ahead of an elongated weekend. YM -0.4, XM +0.3 at typing, while cash ACGB trade sees the major benchmark yields trade either side of unchanged across the curve. The release of the latest weekly AOFM issuance slate threw up nothing in the way of notable surprises. Participants are already looking to several key risk events slated for next week, namely the release of the RBA's June meeting minutes, the latest labour market report and an address from RBA Governor Lowe (titled "From Recovery to Expansion").

FOREX: Mixed Asia-Pac Session, DXY Extends Losses

The Antipodeans sold off in muted Asia-Pac trade, which saw little in the way of notable headline catalysts. JPY also landed near the bottom of the G10 pile, while the greenback seemed poised for its first weekly loss this month.

- GBP faced some pressure as reports re: potential delay to the UK's reopening plans continued to do the rounds.

- NOK traded on a firmer footing, even as WTI slipped back below $70/bbl. It Scandinavian peers rose in tandem.

- The PBOC set it central USD/CNY mid-point at CNY6.3856, 9 pips above sell-side estimates. USD/CNH lost some altitude, but yesterday's trough remained intact.

- Focus turns to the UK's monthly economic activity data & preliminary U.S. Univ. of Mich. Survey. Central bank speaker slate features ECB's Holzmann & Knot, as well as BoE's Bailey, Ramsden & Cunliffe.

FOREX OPTIONS: Expiries for Jun11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2100(E2.2bln), $1.2150-55(E2.1bln), $1.2175-90(E768mln), $1.2200(E1.7bln-EUR puts)

- USD/JPY: Y108.90-109.10($2.2bln-USD puts), Y109.75-80($1.2bln-USD puts), Y110.00($1.6bln), Y110.50-60($1.0bln)

- AUD/USD: $0.7740-50(A$796mln), $0.7800(A$557mln)

- USD/CAD: C$1.2035($550mln), C$1.2080-90($2.7bln-USD puts), C$1.2150($1.2bln-USD puts)

- USD/CNY: Cny6.3700($950mln), Cny6.4000-10($815mln), Cny6.45($830mln)

ASIA FX: Gained As USD Dropped Back

US yields fell and the greenback moved lower in the wake of US CPI data yesterday, news flow was light with holiday's in the region next week.

- CNH: Offshore yuan is higher, USD/CNH losing ground as the greenback retreated.

- SGD: Singapore dollar continued to gain, moving towards its 2021 highs. Singapore will increase group gathering sizes and allow dining-in at food outlets to resume after aggressive virus restrictions over the past month

- TWD: Taiwan dollar gained, on track for its fourth straight weekly gain.

- KRW: Won is higher, BoK Governor Lee said the bank would start to normalize policy when the recovery was assured. Data showed exports remain robust.

- MYR: Ringgit is stronger, data showed April manufacturing sales rose 72.5% Y/Y while industrial production rose 50.1%.

- IDR: Rupiah gained, Indonesia's Covid-19 case count increased by the most since Feb yesterday. Local Covid-19 task force spokeswoman Tarmizi said that the gov't wants to start offering jabs to all adults as soon as by the end of this month, while Jakarta earlier said that it was already inoculating the general population.

- PHP: Peso rose, BSP Gov Diokno said Thursday that Bangko Sentral will maintain loose monetary policy settings "as long as necessary," while remaining on watch for developments in the labour market and any potential impact on inflation.

- THB: Baht is higher, Thai Parliament approved the gov't's THB500bn borrowing plan to fund economic measures amid the Covid-19 outbreak.

ASIA RATES: GSAP Expected To Support India Auction

- INDIA: Yields lower in early trade. Markets look ahead to today's INR 260bn auction, the sale is expected to be supported by the inclusion of the issues at auction in the final GSAP operation next week. . The RBI will buy INR 400bn of bonds on June 17 including INR 100bn of state debt. Eligible sovereign issues include: 6.97% 2026, 6.79% 2027, 7.17% 2028, 7.59% 2029, 5.85% 2030, 6.64% 2035

- SOUTH KOREA: 10-year futures are higher but off best levels. BoK Governor Lee spoke and said the economic recovery would become clearer in the second half of this year and the bank would start to normalize when the recovery was certain, noting that the bank was taking the virus and financial imbalances into account around the recovery. Elsewhere South Korea's exports jumped 40.9% Y/Y in the first 10 days of June on the back of robust shipments of chips and autos.

- CHINA: Repo rates are higher today but have stuck within recent ranges. Futures are lower but have seen sluggish moves and the contract still holds opening gains from Wednesday this week. A quiet session in terms of news flow, markets continue to digest comments from PBOC Governor Yi Gang who said he sees inflation well below the government's official target of around 3%.

- INDONESIA: Yields lower across the curve, some bull flattening seen. Bonds are on track for their third weekly gain. The World Bank approved a $400mn loan to Indonesia, which will support the local financial sector. The loan is expected to help Indonesia implement reforms, which will "increase the depth, improve the efficiency, and strengthen the resilience" of Indonesia's financial markets.

EQUITIES: Muted

Equity markets in the Asia-Pac region are mixed with moves in either direction muted. Bourses in Japan and mainland China are lower while Hong Kong, Taiwan and South Korea are higher, the latter after strong export data. Australia also seeing some gains with iron ore higher. In the US futures are marginally higher with markets still digesting yesterday's jump in US inflation and assessing just how much is transitory.

GOLD: U.S. CPI Dynamic Forces Re-Test Of $1,900/oz

The lower U.S. real yield/higher breakeven backdrop in the wake of yesterday's stronger than expected U.S. CPI print supported bullion, although bulls still haven't managed to force a clean break above $1,900/oz, with spot trading just shy of that level at typing. Participants now switch focus to next week's FOMC decision.

OIL: Retreats From Key Level

Oil is lower in Asia-Pac trade on Friday, with WTI & Brent sitting ~$0.25 below their respective settlement levels. Still, there are positive demand cues with an OPEC+ report on Thursday predicting demand will rise by around 5m bpd in the second half of 2021, while estimates of spare capacity could be lowered.

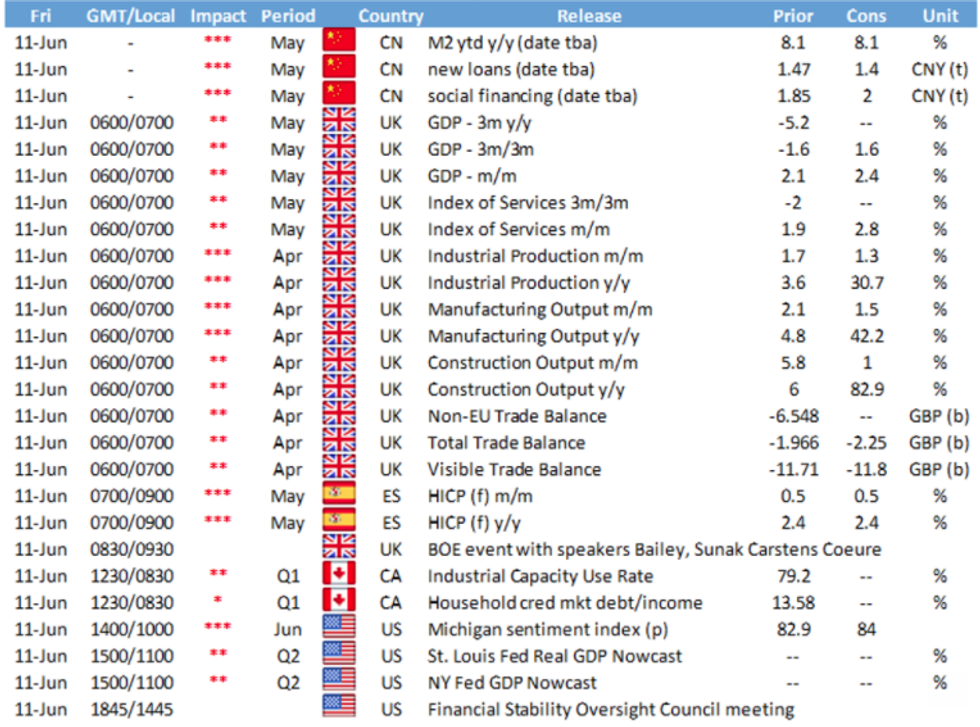

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.