Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

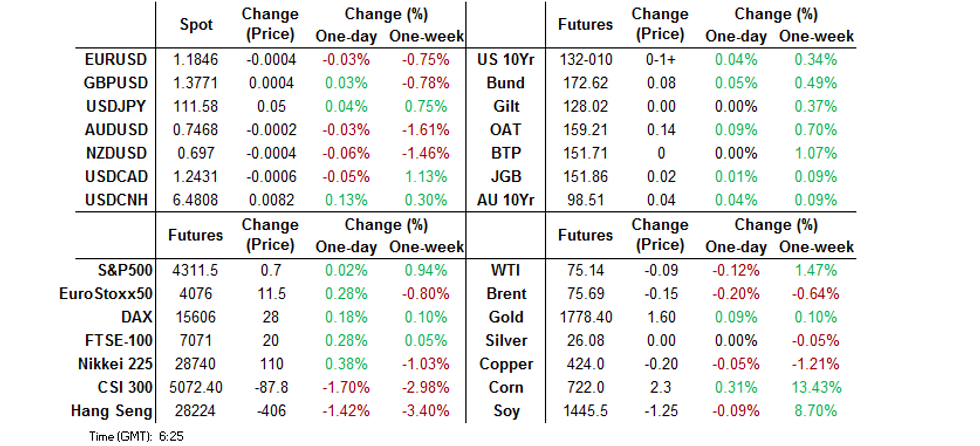

- Chinese equities struggle after the passage of the CCP's 100th anniversary and removal of the related "safety window."

- USD holds onto yesterday's gains.

- The elongated OPEC meeting and the monthly U.S. NFP print will garner most of the attention on Friday.

BOND SUMMARY: Core FI Little Changed Ahead Of NFPs, JGBs Give Back O'night Gains

T-Notes stuck to a 0-02+ range in Asia, last +0-02 at 132-10+, while the major cash Tsy benchmarks print little changed to 1.0bp cheaper, with the curve seeing some light bear flattening after Thursday's late twist flattening. Headline and market flow was light overnight, in what was a typical pre-NFP, pre-Independence Day weekend Asia-Pac session (note that SIFMA has recommended a 14:00 Eastern close for cash Tsys on Friday). Ahead of NFPs J.P.Morgan note that "overall, valuations remain rich but we do not think all bearish curve positions have been unwound; thus, we think there risks are skewed to a larger decline in yields should this number disappoint to the downside."

- JGB futures gradually gave back their overnight gains during the Tokyo morning, and last trade +1 on the day. The major cash JGB benchmarks trade little changed to ~1.0bp richer, with some light underperformance for the front end of the curve, while the belly was perhaps limited by the previously noted move in futures. There were steady and lower bid/cover ratios in the 1- to 3- and 10- to 25-Year BoJ Rinban buckets, even with the purchase sizes of the buckets being trimmed by Y25bn and Y50bn respectively from this round of Rinban operations going forwards (which was announced in the Jul-Sep Rinban plan). The 3- to 5-Year cover saw a very modest uptick, but the levels and degree of movement were relatively inconsequential. Local headline flow was dominated by speculation surrounding the spectator situation at the Olympics and a potential elongation of the state of emergency covering Tokyo. Monday's local docket is fairly empty, although participants will be more than aware of the proximity to Tuesday's 30-Year JGB auction.

- A sedate session for the Aussie bond space, outside of the previously discussed early tick higher in YM (likely linked to some pre-RBA positioning adjustment, as evidenced by the movement in the ACGB Apr '24/Nov '24 yield spread, as some of the more hawkish calls are pared back/profit is taken), with that contract now +1.5 on the day, while XM prints +4.5 (most of the move in XM came during the overnight session on the late flattening of the U.S. Tsy curve during NY hours). A drab AOFM issuance outline for the first half of the current FY, with the AOFM failing to introduce a new conventional ACGB line, as well as the proximity to the U.S. NFP report and next week's RBA decision, has left the space to operate in narrow ranges. Retail sales, ANZ job ads and building approvals data headline the local docket on Monday, with the latest round of scheduled ACGB purchases from the RBA also due. However, the proximity to Tuesday's key RBA decision should render these releases/events fairly inconsequential.

FOREX: USD Waits For NFP, Antipodeans Lose Ground

The DXY operated in close proximity to its three-month highs in a typically quiet pre-NFP Asia-Pac session. Upbeat ADP employment data and weekly initial jobless claims released over the last two days raised expectations surrounding the upcoming NFP report. The greenback is poised to finish the week as the best G10 performer, before the U.S. closes for the observance of its Independence Day on Monday.

- USD/JPY round tripped from a fresh multi-month high (Y111.66) over the Tokyo fix, while holding a tight 15 pip range. Participants eyed the expiry of $2.0bn of options with strikes at Y111.00 at today's NY cut, with a further $2.0bn of USD calls with strikes at Y111.40-50 due to roll off.

- The Antipodeans lost ground amid continued sense of concern about Australia's Covid-19 situation and the economic fallout from virus containment measures. Their commodity-tied peers NOK and CAD were resilient.

- USD/CNH climbed to a fresh weekly high. The PBOC set its central USD/CNY mid-point at CNY6.4712, 8 pips above sell-side estimate.

- The NFP provides the main point of note today, with U.S. trade balance, factory orders & final durable goods orders also coming up. Speeches are due from ECB's Lagarde & de Cos.

FOREX OPTIONS: Expiries for Jul02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1750(E1.0bln), $1.1820-25(E1.5bln-EUR puts), $1.1850-55(E2.6bln), $1.1865-66(E1.1bln), $1.1895-1.1900(E2.0bln), $1.1940-50(E3.9bln), $1.2025-35(E543mln)

- USD/JPY: Y109.35-50($1.2bln), Y109.75($650mln), Y110.20-25($656mln), Y110.70-80($1.8bln), Y111.00($2.0bln), Y111.40-50($2.0bln-USD calls), Y111.75($1.9bln-USD calls)

- EUR/JPY: Y132.00-20(E582mln)

- AUD/USD: $0.7495-00(E514mln), $0.7625(A$593mln)

- USD/CAD: C$1.2250($988mln), C$1.2300($730mln), C$1.2325($855mln), C$1.2500-15($830mln)

- USD/CNY: Cny6.32($1.6bln-USD puts), Cny6.40($950mln), Cny6.45($875mln)

ASIA FX: Elevated Coronavirus Numbers Continue To Weigh

A cagey session ahead of US NFP data later today; the greenback continues to firm while coronavirus concerns in Asia sapped risk sentiment.

- CNH: Offshore yuan is weaker, USD/CNH rising above 6.48 for the first time since June 24. Sino-US tensions continue to bubble. Thursday saw US Commerce Secretary Raimondo note that the US "will make sure that the Chinese play by the rules, protect IP, allow our markets, our companies to access that market."

- SGD: Singapore dollar is weaker, USD/SGD making its way above the 1.35 handle for the first time since March. On the coronavirus front the health ministry has said Singapore plans to announce a further easing of COVID-19 restrictions in mid-July as part of a strategy for reopening.

- TWD: Taiwan dollar is weaker for a second day, USD/TWD rising towards the 28.00 handle pre-NFP. On the coronavirus front the government is said to be working on guidance for various industries in case of the outbreak re-emerges after restrictions are eased.

- KRW: The won is weaker as new coronavirus cases jump to 826, the highest since January. Elsewhere inflation was above the BoK's target for the third month, but did slow slightly from the May print.

- MYR: Ringgit softened. Malaysia's Defence Min Ismail Sabri announced the implementation of stricter curbs on mobility (EMCO) in most of the Klang Valley. New virus counter-measures in the Klang Valley will take effect from Jul 3 through Jul 16.

- IDR: Rupiah is weaker for the fifth straight day. Indonesia unveiled a slew of new restrictions for Java and Bali, which will take effect for two weeks starting tomorrow (i.e. Jul 3 - 20). All non-essential workers have been told to work from home, while most essential sectors will operate at 50% capacity.

- PHP: Peso lost ground, the Philippines marginally relaxed capacity restrictions in the NCR+ region. Elsewhere, the Dept of Health said that the Philippines is now a low-risk country for Covid-19, as the two-week rate of increase in new cases has been faltering.

- THB: Baht is lower and near a 13-month nadir. PM Prayuth said that Thailand has to accept the risks associated with launching the Phuket sandbox. The national Covid-19 task force warned that if the average number of infections on the island tops 15 per 100,000 people in one week, the project can be delayed or cancelled.

ASIA RATES: PBOC Drains For Second Day; Indian Auctions Eyed

- INDIA: Yields higher in early trade, bonds under pressure due to some auction concession and disappointment that the RBI did not announce any purchase operations for next week. Markets await the results of an INR 320bn bond sale later in the session. There is a chance that the sale could be left to primary dealers; last time out the auction of the 5.63% 2026 bond had INR 28bn devolved to primary dealers, while last week's sale saw the RBI devolve the whole INR 140bn 5.85% 2030 bond sale on primary dealers. Meanwhile the RBI did announce plans to hold an INR 2tn 14-day reverse repo operation today.

- SOUTH KOREA: Futures are higher but off best levels, risk sentiment is mixed in Asia and South Korean equity markets are struggling to make gains. There is some concern over elevated coronavirus figures, with loosening of lockdown measures facing further delays. Markets have looked through inflation figures which were above the BoK's target again. The pace of gains in consumer prices did slow though which supports comments made by the Central Bank that inflation would overshoot in the short term and then pull back with the Bank now forecasting 1.8% for the year.

- CHINA: The PBOC drained CNY 20bn of liquidity from the system via OMOs again today, the second day in a row. The central bank has now removed CNY 40bn of the CNY 100bn injection in the five days up to month-end. The PBOC has maintained the refrain that open market transactions are aimed at keeping the country's liquidity "adequate at a reasonable level." After jumping earlier this week repo rates have declined to normal levels; overnight repo rate down 4.5bps at 1.605%, 7-day repo rate down 14bps to 1.86% after touching 3.60% earlier this week. Futures in China are higher with equity markets coming under heavy selling pressure.

- INDONESIA: Yields higher across the curve, some bear flattening seen. Indonesia unveiled a slew of new restrictions for Java and Bali, which will take effect for two weeks starting tomorrow (i.e. Jul 3 - 20). All non-essential workers have been told to work from home, while most essential sectors will operate at 50% capacity. The reopening of Bali to foreign visitors will be delayed, while all large social gathering will be banned. Elsewhere, Health Min Sadikin pledged to expand the vaccination campaign and increase hospital bed capacity, with bed occupancy rate topping 90% in Jakarta, Banten or West Java.

EQUITIES: China Markets Come Under Heavy Pressure

A mixed day for equities in the Asia-Pac region. Chinese equities have come under notable pressure, the downtick in margin balances lodged at the Shanghai exchange and withdrawal of the PBoC's late June seasonal liquidity injections over the last couple of days weighed, while some noted that the perceived "period of safety" ahead of the CCP's 100th anniversary (which was celebrated on Thursday) has now passed, which could be applying some pressure. Elsewhere, Sino-US tensions continue to bubble. Thursday saw US Commerce Secretary Raimondo note that the US "will make sure that the Chinese play by the rules, protect IP, allow our markets, our companies to access that market." Markets in Japan are higher alongside small gains in Australia, Taiwan and South Korea following a positive lead from the US; in South Korea inflation rose above the BoK's target but slowed down from last month. Futures are mixed in the US ahead of the NFP report later today; e-mini-Dow Jones and e-mini S&P contracts are higher while the Nasdaq has slipped slightly. Johnson & Johnson continued to gain after saying that its single-shot coronavirus vaccine is effective against the delta variant.

GOLD: Tight Ahead Of NFP

Conflicting inputs from a stronger USD and marginally lower U.S. real yields (although our weighted U.S. real yield monitor continues to operate comfortably off of the cycle lows) leave gold within the confines of a tight range. The initial technical lines in the sand remain untouched, with today's NFP print the key input ahead of the elongated U.S. weekend. Spot last deals little changed, just shy of $1,780/oz.

OIL: Oil Holds Gains Ahead Of OPEC+ Talks Resumption

WTI & Brent futures are virtually unchanged on the day. WTI gained 2.4% yesterday and briefly rose above $76/bbl after OPEC+ members failed to reach a final agreement on oil production plans in coming months. If the resumption of talks later today doesn't result in an agreement, the group would fall back on existing agreements and keep oil supply unchanged until April 2022 which could exacerbate deficit conditions in oil markets. The group had reportedly agreed in principle to boost oil production by 400k bpd a month from August to December but the deal was blocked by UAE at the last minute. The UAE said it would only back a deal if the baseline for its output cuts was increased.

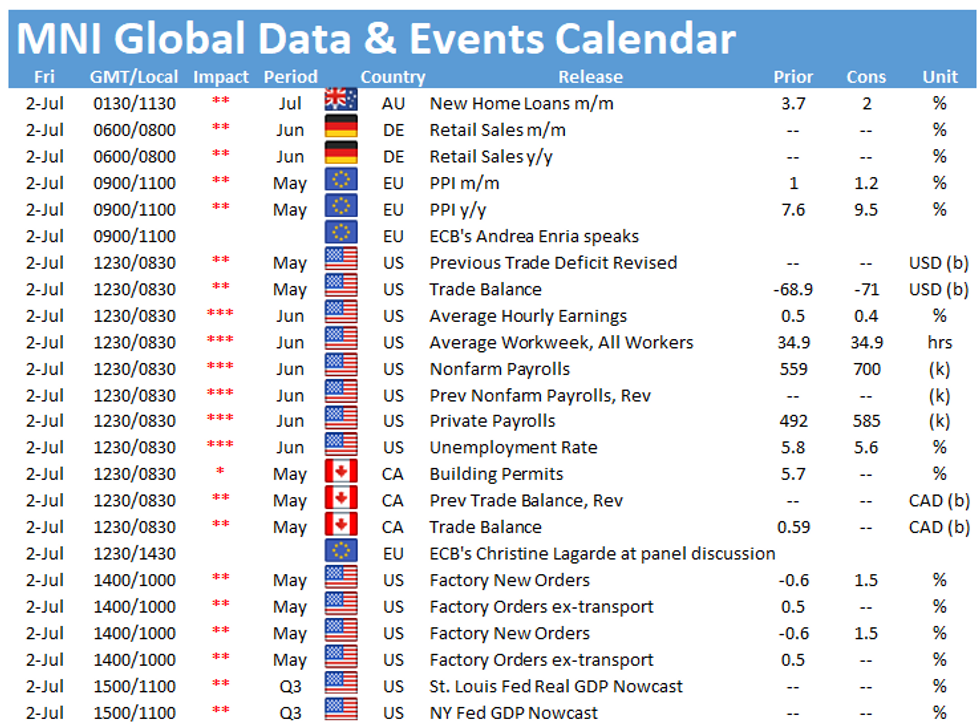

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.