Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

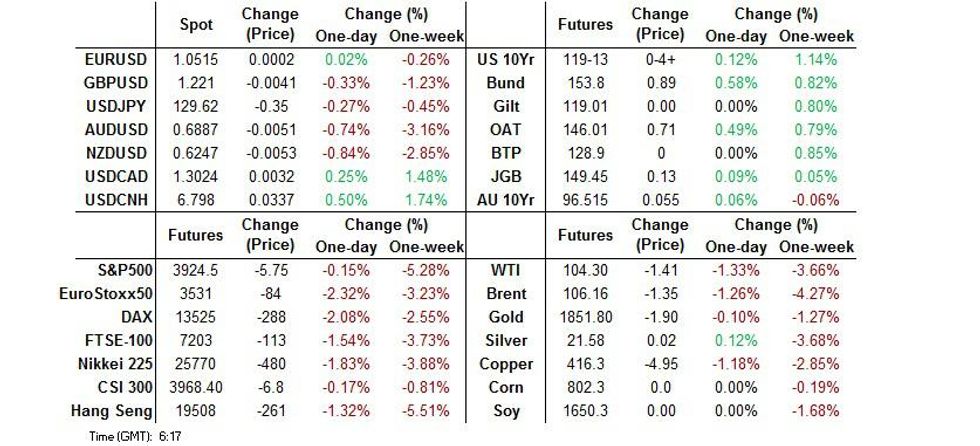

- Early defensive flows were seen in Asia after a couple of COVID infections were found outside of Shanghai’s quarantine system (resetting the clock re: the move towards a loosening of social mobility restrictions in the city), while North Korea also declared its “first” case of COVID, triggering a lockdown across all cities in the country. We also saw Chinese property developer Sunac note that it has missed interest payments on several US$ bonds (the grace period on one of the payments has now elapsed, with no payment, which could trigger cross-default on other offshore debt), with liquidity issues remaining evident in the sector. Those moves then moderated/reversed, before fresh risk-off fows were seen into London dealing.

- This came even as the PBoC pointed to greater focus on growth stabilsation. JPY sits atop the G10 FX table as a result, while e-minis are 0.4% lower. USD/CNH trades above CNH 6.8000.

- On the data front, focus turns to UK GDP (flash) & Swedish CPI as well as U.S. PPI & weekly jobless claims. The central bank speaker slate features ECB's de Cos & Makhlouf as well as Riksbank's Ingves.

US TSYS: Twist Flatter In Asia, Some Vol. Evident

A flurry of defensive flows were evident during early Asia-Pac trade, with TYM2 moving through Wednesday’s peak and e-minis on the backfoot after a couple of COVID infections were found outside of Shanghai’s quarantine system (resetting the clock re: the move towards a loosening of social mobility restrictions in the city), while North Korea also declared its “first” case of COVID, triggering a lockdown across all cities in the country. We also saw Chinese property developer Sunac note that it has missed interest payments on several US$ bonds (the grace period on one of the payments has now elapsed, with no payment, which could trigger cross-default on other offshore debt), with liquidity issues remaining evident in the sector.

- Still, the space quickly moved away from richest levels as risk assets regained some poise and e-minis moved back into positive territory, although there was a lack of meaningful headline flow to trigger such a move.

- TYM2 is now operating just below the middle of its 0-15+ Asia-Pac range, with e-minis dealing around neutral levels. The former is +0-01+ at 119-10 on volume of ~160K. Cash Tsys have twist flattened, pivoting around 3s, with 2s running ~1bp cheaper while 7s provide the firmest point across the curve, sitting 2bp richer. It would seem the twist flattening impetus witnessed after yesterday’s CPI print left its imprint on regional participants, despite the aforementioned vol.

- Later in the session we saw one of the PBoC Vice Governors note that the Bank is making growth stabilisation a “higher priority” while also flagging the Bank’s guidance re: lower loan interest rates.

- PPI & weekly jobless claims data are due during NY hours, in addition to 30-Year Tsy supply.

JGBS: Wider Impulse Driving The Space

There has been a lack of domestic input when it comes to today’s JGB market moves, with wider cross-asset flows at the fore.

- The early bout of risk-off flows linked to COVID headlines covering the Chinese city of Shanghai & North Korea, and perhaps some worry linked to the Chinese property sector given Sunac’s warning re: its ability to service its immediate interest payments on debt requirements, provided some support, before the wider risk-off impulse faded.

- JGB futures pushed through their overnight highs before fading from best levels and then turning bid again. The contract is last +12.

- Cash JGBs are little changed to 1bp richer across the curve. 30+-Year paper cheapened in early afternoon dealing, post-supply, after outperforming during the Tokyo morning, but has since regained some poise.

- In terms of specifics, the latest 30-Year JGB auction was soft on the pricing side, with the low price softer than wider expectations (99.40 vs. the BBG dealer median of 99.60), while the price tail widened vs. the previous round of 30-Year JGB supply. Elsewhere, the cover ratio was little changed vs. the previous round of 30-Year JGB supply, holding below the 6-auction average of 3.32x. Ongoing market vol. & the risk of fresh offshore FI-led cheapening is seemingly keeping some prospective bidders sidelined at present, even with yields hovering around multi-year highs.

AUSSIE BONDS: A Touch Firmer & Flatter, Back From Extremes

Aussie bonds continue to trade to the beat of the wider macro drum, with a lack of idiosyncratic drivers evident once again on Thursday.

- In his latest pre-election address, Australian PM Morrison noted that sizeable pay growth may fan the inflationary flames further, despite various unions and business bodies calling for such a move in recent days (Morrison’s ruling coalition still trails Labor in the polls ahead of the May 21 election).

- The previously outlined COVID case-related headlines surrounding China, and to a lesser extent, North Korea, in addition to the Sunac bond payment worries, allowed futures to move to best levels of the session during the Sydney morning, before the move pared back a little as wider risk appetite recovered a little.

- A very modest moderation in domestic consumer inflation expectations (to a still lofty +5.0% in Y/Y trimmed mean terms) had no impact on the space.

- YM is dealing +4.0, with XM +5.5, which much of the overnight/early Sydney flattening unwound.

- 10+-Year cash ACGB trade has seen a fairly parallel 5.5-6.5bp of richening.

- A$1.0bn of ACGB May-32 supply, the release of the weekly AOFM issuance slate and panel participation by RBA Deputy Governor Bullock at the Regulators 2022 (FINSIA) headline the local docket on Friday.

JAPAN: No Change In Direction In High Frequency Bond & Equity Flow Data

The latest round of international security flow data out of Japan revealed nothing in the way of meaningful trend changes, with net flows moderating owing to the holiday period in Japan. Japanese investors extended their run of net selling foreign bonds and buying foreign equities, while foreigners sold Japanese bonds and bought Japanese equities.

FOREX: Sentiment Sours As COVID Returns To Shanghai Community, PBOC Speak Adds Pressure To Yuan

Risk sentiment soured as disappointing news re: China COVID-19 situation added to the concerns over the prospect of decisive Fed tightening. Shanghai reported two infections in the community, which quashed hopes for imminent loosening of restrictions. The authorities would only be able to ease curbs after three consecutive days of no community transmission and there were zero cases outside designated quarantine facilities on Wednesday. The official confirmation of first COVID-19 infections in North Korea helped fuel worries over the resurgence of the virus.

- The redback got some reprieve as firm appreciation bias returned to the daily yuan fixing, but USD/CNH staged a strong rebound as the session progressed. The rate's upswing seemed driven by comments from PBOC Dep Gov Chen, who noted that the central bank has guided loan interest rates to decline. USD/CNH extended gains upon the breach of Nov 4, 2020 high of CNH6.7745 on its way to a fresh cycle high at CNH6.7890.

- The Aussie and Kiwi dollars were hardest hit among G10 currencies, owing to the dependence of Antipodean economies on demand from China. The kiwi dollar paced losses, paying little attention to the RBNZ's Q2 Survey of Expectations, which showed a further uptick in two-year inflation expectations.

- The yen took the lead on safe haven demand but USD/JPY failed to test yesterday's low. By contrast, regional risk barometer AUD/JPY retreated past yesterday's worst levels to a new multi-week low, consolidating under the Y90.00 mark.

- The HKMA intervened in defence of its currency peg for the first time since 2019 after USD/HKD tested the upped end of its permitted trading band late doors Wednesday.

- On the data front, focus turns to UK GDP (flash) & Swedish CPI as well as U.S. PPI & weekly jobless claims. Central bank speaker slate features ECB's de Cos & Makhlouf as well as Riksbank's Ingves.

FOREX OPTIONS: Expiries for May12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0400(E507mln), $1.0600(E1.3bln), $1.0625(E793mln), $1.0675-85(E1.1bln)

- GBP/USD: $1.2400(Gbp690mln)

- EUR/GBP: Gbp0.8580-00(E503mln)

ASIA FX: Risk Aversion Takes Toll On Asia EM FX

Participants were reluctant to take more risk as onshore Asia EM markets digested above-forecast U.S. inflation data released overnight, while concerns over China's outbreak of COVID-19 continued to linger.

- CNH: The PBOC pushed back against yuan depreciation, increasing the appreciation bias in the daily USD/CNY fixing to 49 pips. This provided only modest, fleeting reprieve to the redback, which came under pressure from domestic COVID-19 developments and dovish PBOC rhetoric. Shanghai reported two community cases of the disease, which stopped the three-day countdown to the point when the authorities could ease restrictions. Elsewhere, PBOC Dep Gov Chen noted that the central bank has guided loan interest rates to decline. These comments seemed to drive an upswing in USD/CNH, which took out resistance from Nov 4, 2020 high of CNH6.7745 and rallied to a fresh cycle high.

- KRW: The won was the worst performer in the Asia EM basket amid risk-off sentiment. Spot USD/KRW soared to KRW1,290, its highest point since Mar 23, 2020. Worth noting that North Korea locked down its cities after confirming first COVID-19 cases, which provokes questions over the implications for stability in the Korean peninsula.

- IDR: Spot USD/IDR surged to its best levels in more than a year. Bank Indonesia said Wednesday that core inflation remains manageable, seemingly pouring some cold water on prospects of any front-loaded tightening.

- MYR: Gains registered by the ringgit on the back of a surprise rate hike delivered by the BNM Wednesday evaporated as focus turned to U.S. inflation figures & China's COVID situation. Spot USD/MYR advanced to levels not seen since Apr 2020.

- PHP: Spot USD/PHP surged towards key resistance from PHP52.500 as broader-picture developments outweighed the Philippines' strong Q1 GDP data. The economy grew 8.3% Y/Y in the three months through end-March, beating consensus forecast of +6.8%, extending a streak of better than expected growth readings.

- THB: The baht printed its weakest levels versus the greenback in almost exactly five years. FinMin Arkhom warned that Thailand's economic recovery "may not be fast" despite growing exports, as the critical tourism sector will need some time to return to normal.

- INR: The rupee plunged to an all-time low, depreciating in line with regional trend. Bloomberg sources said that the RBI would be open to bond buying buy may prefer other measures to boost demand for government debt. Focus turns to April inflation figures, due for release in a few hours' time.

- HKD: The HKMA bought about HKD1.59bn to defend its currency peg after USD/HKD tested the upper end of its permitted trading range. The rate is still flirting with the HKD7.85 cap as we type.

CROSS-ASSET: MNI Global Macro Outlook - May 2022: USD Breakout Implications

The US dollar is breaking higher against key global counterparts, including the Euro and yen. MNI looks at the potential for further USD gains and the associated macroeconomic implications; as well what could derail further dollar appreciation.

For full PDF publication: USD Breakout Implications - May 2022.pdf

EXECUTIVE SUMMARY

- The Federal Reserve wants to tighten financial conditions - implicitly endorsing a stronger US dollar.

- The DXY dollar index is on the cusp of breaking through significant chart resistance, having already broken out to multi-year / decade highs vs key currencies such as the Euro and yen.

- Fundamentals point to further USD gain potential, but despite this, market sentiment isn't particularly dollar bullish.

- A stronger USD could further weigh on US and global financial conditions, helping achieve disinflation but at the cost of growth.

- This slide deck is excerpted from our most recent Global Macro Outlook - the previous edition highlighted nascent breakouts for the USD and why the US is “different” in this macro cycle vs its peers.

EQUITIES: Lower Post-CPI; Australian Tech Gets Crushed

Most Asia-Pac equity indices are lower at typing, tracking a negative lead from Wall St. High-beta stocks across the region broadly sold off following Wednesday’s above-expectations U.S. CPI reading, with the latter largely confirming recent hawkish Fed tightening expectations, sending that basket of rate-sensitive stocks lower in Asian hours.

- The Hang Seng Index sits 1.1% worse off at typing, with debate re: capital outflow doing the rounds after the HKMA stepped in to intervene in the HKD for the first time since 2019. The Hang Seng Tech Index struggled, dealing 1.5% softer at typing on losses in Tencent, Alibaba, Baidu. A note that major internet platform companies broadly pared losses mid-way through the morning session, following a report that Chinese officials are due to meet with business executives from the country’s largest private-sector companies next week, with Chinese Vice Premier Liu He reportedly scheduled for attendance as well (BBG sources).

- The CSI300 has risen from a 0.7% lower open to sit just below neutral levels at writing, heading into the mid-session break. Remarks from senior PBOC and government officials earlier in the session emphasising supportive policy for “weak links” in the economy (from the PBOC) and “incremental policies” to support growth (from the government), lent a bid to equities, balancing against broader weakness amongst real estate stocks.

- The ASX200 sits 1.6% softer, with the S&P/SPX All Technology Index dragging overall sentiment lower, shedding 5.9% at typing. The bulk of the losses are attributed to Block Inc (-15.6%) and Xero Limited (-11.3%), with the latter tumbling after reporting full-year results for FY22. Block Inc on the other hand, likely tracked a broader decline in the cryptocurrency space due to the spectacular implosion of the stablecoin UST (third largest by market cap), with large-cap crypto token LUNA diving to ~$0.35 at typing (started the week at ~$64).

- U.S. e-mini equity index futures are 0.1% to 0.3% firmer apiece, albeit operating just above their respective cycle lows made earlier in the session.

GOLD: Higher Post-CPI

Gold sits $5/oz better off to print $1,857/oz, operating around Wednesday’s best levels at typing. The move higher has been facilitated by a limited downtick in nominal U.S. Tsy yields, with the USD (DXY) continuing to trade a little below recently made cycle highs.

- To recap Wednesday’s price action, U.S. inflation figures initially spurred a knee-jerk ~$20/oz decline in gold, reversing gains made earlier in the session pre-CPI. The yellow metal rapidly rebounded to close $14/oz higher amidst a retreat in U.S. real yields, erasing the bulk of Tuesday’s losses in the process. The bounce comes as the firmer-than-expected CPI print mixes with recent Fedspeak coalescing around support for back-to-back 50bp hikes for near-term FOMCs.

- To elaborate, known hawk Bullard (St. Louis Fed Pres, voter) said after Wednesday’s CPI print that 50bp hikes were “a good benchmark for now” while re-iterating previously issued views that 75bp hikes are “not my base case”, flagging data-dependence. Atlanta Fed Pres Bostic (‘24) separately voiced support for 50bp moves “until we get to neutral” (FOMC estimate: ~2.4%), while again not ruling out a 75bp hike.

- Elsewhere, June FOMC dated OIS now price in ~61bp of tightening for that meeting, reviving the prospect of a 75bp hike (>40% chance). A look further out points to a more muted change in expectations for the July FOMC, with dated OIS pricing in a cumulative ~106bp of tightening by that meeting, a little higher than pre-CPI levels.

- From a technical perspective, gold remains vulnerable despite its recent move higher, with initial support seen at $1,832.1/oz (May 11 low). Immediate support is a relatively short distance away at $1,865/4/oz (May 10 high), although our technical analyst flags that a break of resistance at $1,909.8/oz (May 5 high) may be needed to confirmation a short-term reversal of the bearish trend.

OIL: Lower In Asia; Shanghai Resets Lockdown Counter

WTI and Brent deal ~$1.30 weaker apiece, extending a pullback from Wednesday’s best levels at writing.

- Virtually no discernible progress has been made re: overcoming Hungarian opposition to EU sanctions on Russian energy, with Budapest on Wednesday notably demanding “hundreds of millions of dollars” to replace Russian crude - a move that senior European diplomats have reportedly voiced opposition to, despite a European Commission (EC) plan to do so. Looking ahead, the EC is due to schedule a video conference between European Leaders and Hungarian leader Viktor Orban.

- Looking to China, elevated hope for an end to lockdowns in Shanghai took a hit earlier in the session after two cases were reported “in the community” for Wednesday, keeping in mind that officials have stated that three days of zero community spread is required for there to be an easing in restrictions. Zooming out, COVID cases in the city and nationwide remain relatively low however, coming in below 2K for another day.

- The latest round of U.S. EIA crude inventory data crossed on Wednesday, with a large surprise build in U.S. crude stockpiles observed, adding to the increase observed last week as well. On the other hand, there was a drawdown in gasoline, distillate, and Cushing hub stocks, with distillate inventories noted to have previously hit 14-year lows in last week’s data release.

- The ongoing drawdown in U.S. distillate stockpiles comes as analysts have flagged the start of the “driving season” in the U.S., set to begin in end-May.

- Up later today, the International Energy Agency is due to release their monthly Oil Market Report at 0900 BST.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/05/2022 | 0600/0700 | ** |  | UK | Index of Services |

| 12/05/2022 | 0600/0700 | ** | | UK | UK Monthly GDP |

| 12/05/2022 | 0600/0700 | *** | | UK | Index of Production |

| 12/05/2022 | 0600/0800 | *** |  | SE | Inflation report |

| 12/05/2022 | 0600/0700 | ** | | UK | Output in the Construction Industry |

| 12/05/2022 | 0600/0700 | ** | | UK | Trade Balance |

| 12/05/2022 | 0600/0700 | *** | | UK | GDP First Estimate |

| 12/05/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 12/05/2022 | 1230/0830 | *** | | US | PPI |

| 12/05/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 12/05/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 12/05/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 12/05/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 12/05/2022 | 1535/1135 |  | CA | BOC Deputy Gravelle speech on commodity shocks. | |

| 12/05/2022 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 12/05/2022 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 12/05/2022 | 1800/1400 | *** |  | MX | Mexico Interest Rate |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.