Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

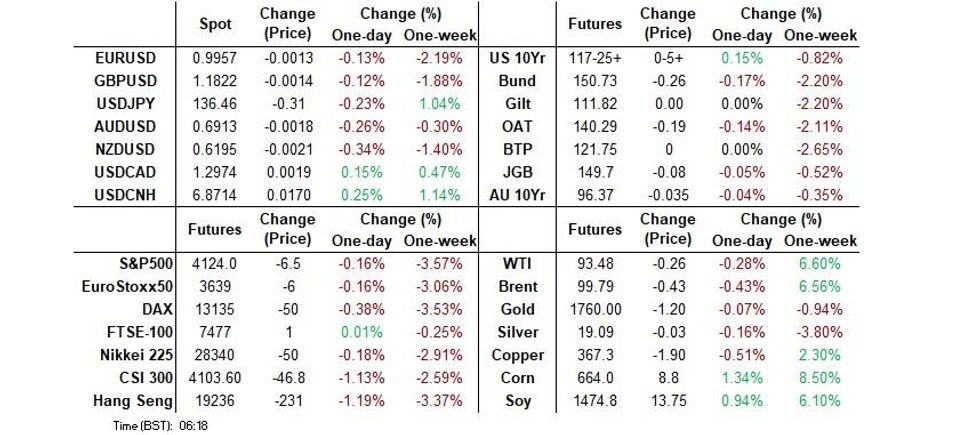

- Headwinds for the Chinese property sector weighed on Chinese equities, which helped to push the S&P 500 e-mini contract through Tuesday's low. U.S. Tsys saw some modest bull steepening overnight.

- Participants sought shelter in safe-haven currencies on the above and amid pre-Jackson Hole caution. Headline flow failed to offer much in the way of notable catalysts.

- Today's data highlights include flash U.S. durable goods orders. Elsewhere, comments are due from Riksbank's Floden.

US TSYS: Light Bull Steepening Overnight

Tsys richened at the margin in Asia with the major cash Tsy benchmarks running 1.0-2.5bp richer at typing, bull steepening.

- TYU2 stuck to a narrow 0-05+ range, last +0-05 at 117-25, running on volume of ~81K (~33K of which is roll-related).

- Weakness in Chinese equities, with focus back on woes for the property sector, provided some incremental support.

- Still, participants were seemingly happy to remain on the sidelines ahead of the upcoming Jackson Hole symposium.

- A Q&A session with Minneapolis Fed President Kashkari (’23 voter) failed to provide any surprises, as the former dove underscored the need to fight inflation, highlighting the lack of trade-off between the central bank’s inflation and employment mandates at present, noting the Fed can only relax re: rate hikes when there is compelling evidence of inflation heading towards 2%.

- TU (3,279) & UXY (1,014) blocks headlined on the flow side, crossing at the same time, although both appeared to be sellers (there was a clear DV01 overweighting to FV if it was a curve play).

- Wednesday will see the release of prelim durable goods data, pending home sales and MBA mortgage apps, in addition to 5-Year Tsy & 2-Year FRN supply

JGBS: Curve A Touch Flatter

JGB futures coiled for much of the day, sticking comfortably within the confines of their overnight range, last -8, consolidating modest overnight session losses as we head towards the bell.

- Cash JGB trade has seen some light twist flattening, with the major benchmarks running 0.5bp cheaper to 1.0bp richer. Note that there has been a lack of steepening pressure for JGBs today, despite what was seen in global bond markets on Tuesday (super-long JGBs had come under selling pressure during the first two sessions of the week).

- The latest round of speculation surrounding fiscal matters failed to generate anything in the way of a notable market reaction.

- Meanwhile, Japanese PM Kishida confirmed speculation that vaccinated travellers will not have to take COVID tests when visiting Japan (from 7 September), although there was no news on the potential upping of the number of permitted daily inbound travellers.

- BoJ Rinban operations covering 1- to 10-Year JGBs saw steady to slightly lower offer/cover ratios, which may have provided some light support to that area of the curve during early afternoon dealing, although that zone now underperforms on the day.

- Looking ahead, services PPI data, the weekly international security flows and an address from BoJ’s Nakamura provide the domestic highlights on Thursday. There will also be a liquidity enhancement auction for off-the-run 15.5- to 39-Year JGBs.

AUSSIE BONDS: Curve Twist Steepens

Aussie bonds have edged higher as we have worked our way through the Sydney day, alongside an uptick in U.S Tsys (aided by weakness in Chinese and Hong Kong equities), with front-end ACGBs more than unwinding their earlier cheapening bias derived from the overnight bear steepening in Aussie bond futures.

- Cash ACGBs run 4.0bp richer to 3.5bp cheaper across the curve, twist steepening, and pivoting around 5s. YM is +3.0 and XM is -4.0, with the former operating just shy of session highs at typing. EFPs have narrowed a little, while Bills run 3 to 8 ticks richer through the reds.

- The latest round of ACGB Nov-33 supply was smoothly absorbed, with the weighted average yield printing 0.82bp through prevailing mids (per Yieldbroker), while the cover ratio improved to 2.75x against 2.25x at the previous auction, albeit with a smaller amount on offer (A$800mn vs. A$1.0bn prev.)

- No domestic economic data releases of note are scheduled for Thursday.

FOREX: Yen Outperforms Amid Demand For Safety

Participants sought shelter in safe-haven currencies amid pre-Jackson Hole caution, with e-mini futures losing altitude as the Asia-Pac session progressed. Headline flow failed to offer much in the way of notable catalysts.

- The greenback garnered some strength, with the BBDXY index chewing into yesterday's losses, even as U.S. Tsy yields faltered across the curve.

- Softer U.S. Tsy yields allowed the yen to outperform the U.S. dollar; USD/JPY shed over 35 pips as a result, building on Tuesday's decline.

- There is a $1.3bn option expiry with strikes at Y136.80-00 due to roll off at today's NY cut, but USD/JPY moved away from these levels nonetheless.

- Antipodean currencies sagged amid aversion to risk. AUD/NZD printed one-month highs before easing off towards neutral levels.

- Today's data highlights include flash U.S. durable goods orders. Comments are due from Riksbank's Floden.

AUD: A$ Correlations Fall

AUD/USD correlations with traditional macro drivers have faltered over the past week or so. The table below presents AUD/USD levels correlations with a number of variables, for the both the past week and the past month.

- Across the board correlations are lower, except for iron ore. Correlations with yield differentials remain positive, particularly at the short end, but are down from recent highs.

- The general trend in yield spreads has been in favor of the AUD, with the AU-US 2yr spread back sub -30bps, from recent wides beyond -50bps. AUD/USD has been broadly range bound over this period though

- The bigger correlation drops are evident for both global commodities and global equity market trends. The correlation with global commodities has slumped into negative territory from a short-term standpoint, but interestingly is noticeably higher for iron ore compared to our last update.

- For global equities the correlation has dipped but remains in positive territory.

Table 1: AUD/USD Correlations With Key Macro Drivers

| 1wk | 1mth | |

| 2yr yield differential | 0.52 | -0.02 |

| 5yr yield differential | 0.48 | 0.39 |

| 10yr yield differential | 0.30 | 0.28 |

| Global commodity prices | -0.21 | 0.22 |

| Iron ore | 0.70 | 0.49 |

| Global equities | 0.22 | 0.31 |

| US VIX index | -0.16 | -0.45 |

Source: MNI/Market News/Bloomberg

FX OPTIONS: Expiries for Aug24 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9835-50(E811mln), $0.9925(E570mln), $1.0140-55(E972mln)

- USD/JPY: Y135.00($637mln), Y136.00-05($840mln), Y136.80-00($1.3bln)

- EUR/GBP: Gbp0.8750(E893mln), Gbp0.9000(E1.2bln)

- USD/CAD: C$1.2835-55($565mln)

- USD/CNY: Cny6.7900($1.0bln)

ASIA FX: CNH Weakens Amid Fresh Property Concerns

USD/Asia pairs have been mixed today, although the USD has still been supported on dips for the most part. USD/CNH rebounded amid fresh property woes for China. FX stability remains a focus for the South Korean authorities, while IDR hasn't seen much follow through support after yesterday's surprise rate hike.

- CNH: USD/CNH shrugged off a noticeably stronger than expected CNY fixing, with onshore equities weaker, particularly in the property sector. This follows fresh reports of corruption crackdowns in the sector. USD/CNH dipped towards 6.8550 post the fix but rebounded from here and edged above 6.8800 before selling interest emerged. We last tracked at 6.8730.

- KRW: Spot USD/KRW was lower in early trade, but got dragged higher by a weaker CNH trend. FX levels remain in focus with South Korean President Yoon stating FX volatility was on the rise. Dips below 1340 are supported but the pair hasn't tested resistance above 1345 today.

- IDR: The rupiah has weakened anew amidst risk aversion, despite catching a bid yesterday as Bank Indonesia delivered a surprise 25bp hike to the 7-Day Reverse Repo Rate. Spot USD/IDR has added 25 figs to last trade at IDR14,863. The central bank will also undertake an Operation Twist-style measure to stabilise the rupiah. The Bank will sell more short-term gov't debt in the market, while buying longer dated bonds.

- THB: Spot USD/THB trades +0.04 at THB36.14, shrugging off overnight greenback sales. The minutes from the BoT's most recent monetary policy meeting provided few, if any, surprises. The MPC judged that gradual policy normalisation will be consistent with sustainable growth, even as one member called for faster tightening. Foreign investors bought a net $133.0mn in Thai stocks on Tuesday, marking the 13th consecutive day of net inflows.

- MYR: USD/MYR couldn't sustain early downside, with the pair moving up from 4.4840 to 4.4880. A weaker CNH has arguably not helped onshore sentiment. We remain below recent highs above 4.4900 for now though. A reminder that we will get an update on Malaysia's CPI inflation this Friday.

BOK: MNI BoK Preview - August 2022: Back To A 25bps Hike Pace

EXECUTIVE SUMMARY

EQUITIES: Mostly Lower In Asia

Most Asia-Pac equity indices are lower at typing on a limited, negative showing from Wall St. (major cash indices closed flat to 0.4% softer on Tuesday), with domestic developments (particularly earnings) largely driving matters for regional stocks.

- The CSI300 sits 1.0% worse off, a little above fresh two-week lows at writing. Tech and semiconductor equities have struggled, with the ChiNext (-2.9%) underperforming, dragged lower by losses in large-cap CATL Ltd (-4.3%) after the latter reported weaker battery margins.

- The Hang Seng deals 1.4% softer at typing on losses in ~90% of its constituents, taking the index to fresh 15-week lows. The property (-2.1%) sub-index leads losses as Chinese developer Logan has resumed trading (suspended since May 12), with the latter falling by as much as 58% earlier after missing revenue expectations.

- China-based tech (HSTECH: -2.6%) struggled as well, with sentiment worsened by a sharp selloff in EV stocks after XPeng’s (-13.3%) dismal earnings beat on Tuesday.

- The ASX200 has bucked the broader trend of losses, dealing 0.5% at writing on strength in the energy (+2.0%) and materials (+0.9%) sub-gauges, countering underperformance in consumer staples mainly on losses in Coles Group (-3.3%) despite beating profit expectations. Tech outperformed as well (S&P/ASX All Technology Index: +1.1%), led higher after strong earnings from WiseTech Global (+11.0%).

- E-minis are 0.3-0.4% softer apiece, with Dow contracts operating through Tuesday's low, effectively ceding all of its gains for August at current levels.

GOLD: Little Changed In Asia; Some Reprieve As Dollar Rally Pauses

Gold deals ~$2/oz softer to print ~$1,746/oz in fairly limited Asia-Pac dealing, holding on to the bulk of Tuesday’s gains at writing.

- To recap, gold closed ~$12 firmer on Tuesday amidst a downtick in the USD (DXY) and U.S. real yields, snapping a six-day streak of lower daily closes as participants reacted to weak U.S. economic data prints (flash PMIs, new home sales, and the Richmond Fed m’fing index).

- Sep FOMC dated OIS currently price in ~63bp of tightening at that meeting (pointing to approx. even odds of a 50bp vs a 75bp hike at the meeting), a little below levels observed prior to Tuesday’s U.S. data prints.

- Comments from Minneapolis Fed Pres Kashkari (‘23 voter) provided little fresh insight against recent Fedspeak, emphasising the need to fight inflation, stating that the Fed would only relax rate hikes should “compelling evidence” point to inflation “well on its way back down to 2%”.

- From a technical perspective, conditions for gold remain bearish following its recent failure to break its trendline resistance. Initial support is seen at $1,727.8/oz (Aug 22 low), while initial resistance stands at ~$1,764.9/oz (20-Day EMA).

OIL: Just Off Recent Highs; U.S. Response To Iran Eyed

WTI and Brent are ~$0.10 weaker apiece at writing, consolidating a little below their respective two- and three-week highs made on Tuesday.

- To recap, both benchmarks closed ~$3.50 firmer apiece on Tuesday, rallying after Saudi Arabia raised the prospect of OPEC+ supply cuts, with the prompt spread for Brent rising to highs of ~$1.15 (vs. opening at ~$0.67), reflecting exacerbated worry re: tightness in global crude supplies.

- WTI and Brent nonetheless capped gains after RTRS source reports suggested that potential OPEC+ production cuts are unlikely to be implemented in the near-term, and may coincide with the return of Iranian crude to global oil markets upon a U.S.-Iran nuclear deal.

- On the latter issue, the U.S. is expected to formally respond to the latest offer from Iran by “as early as Wednesday” this week.

- Elsewhere, major crude benchmarks were little changed near session highs on Tuesday after the release of U.S. API crude inventory estimates, with reports pointing to a larger than expected decrease in crude stockpiles, with builds observed in gasoline, distillate, and Cushing hub stocks.

- Looking ahead, U.S. EIA inventory data is due later on Wednesday, with BBG estimates calling for a drawdown in crude and gasoline stockpiles.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/08/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 24/08/2022 | 1230/0830 | * |  | CA | Quarterly financial statistics for enterprises |

| 24/08/2022 | 1230/0830 | ** | | US | durable goods new orders |

| 24/08/2022 | 1400/1000 | ** | | US | NAR pending home sales |

| 24/08/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 24/08/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 24/08/2022 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 24/08/2022 | 1700/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.