Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The BBDXY almost halved yesterday's advance in Asia amid broad-based aversion to the greenback. General risk sentiment improved, with e-mini futures posting gains in a promising sign after U.S. equity benchmarks closed in the red on Wednesday. U.S. Tsy yields were slightly weaker, facilitating the dip in the U.S. dollar.

- Fitch moved the UK's sovereign credit rating outlook to ngative in the wake of the mini-budget, following S&P.

- German factory orders, EZ retail sales and U.S. initial jobless claims take focus on the data front today. There is central bank rhetoric galore, as BoJ, Fed and BoE members will speak, while the ECB will publish the minutes from its September monetary policy meeting.

US TSYS: Little Changed In Asia

Cash Tsys run little changed to 1bp richer into London dealing, with marginal flattening of the curve observed. TYZ2 operated within a 0-07 range during Asia hours, last dealing in the middle of that tight band, +0-02 at 112-19, on ~79K lots.

- An early Asia uptick in Tsys was facilitated by a couple of block buys in TY futures (+3.0K & +2.5K), with a weaker dollar alongside a move higher in e-minis seen at the same time.

- We then moved back from best levels of the day in Tsys.

- Outside of the previously outlined block buying in TY futures, we saw some mixed block flow in that contract (-1.6K & +1.6K), while downside expressions in FVZ2 via 107.25 puts (2x +1,875) were also executed via blocks.

- Asia headline flow was light at best, with nothing in the way of notable movement stemming from the latest North Korean missile test.

- The mix of a Chinese hioliday, lack of meaningful headline flow and proximity to Friday’s NFP release left most on the sidelines.

- Looking ahead, weekly jobless claims data, the latest challenger job cuts reading and a deluge of Fedspeak (headlined by Governors Waller & Cook) provide the highlights of Thursday’s NY docket.

JGBS: Curve Runs Steeper

The combination of Wednesday’s weakness in core global FI markets and the BoJ’s relative lack of control over yields beyond the 10-Year point allowed the JGB curve to steepen on Thursday, with the major benchmarks running 1bp richer to 3bp cheaper, pivoting around 3s. JGB futures print -17, operating in the lower end of their overnight range during Tokyo hours.

- The super-long end has recovered from worst levels of the session, with 10-Year JGB yields hovering around the upper limit of the BoJ’s permitted trading band.

- A liquidity enhancement auction for off-the-run 5- to 15.5-Year JGBs went well.

- The latest round of regional assessments from the BoJ saw it upgrade its economic assessment of 1 region, while the remaining 8 assessments were unchanged.

- Participants now await an address from BoJ Governor Kuroda after the conclusion of the branch managers’ meeting.

- Looking ahead to Friday, household spending and wage data provide the highlights of the domestic docket.

AUSSIE BONDS: Holding Cheaper

YM pushed below its overnight base in the second half of Sydney dealing, with XM lacking any real conviction after a brief and shallow look below its own overnight low. That leaves the former -16.0 and the latter -16.5 ahead of the bell (both off lows), with wider cash ACGBs running 13-16bp cheaper across the curve, with 10s providing the weakest point.

- Aussie bonds looked through a modest richening in U.S. Tsys (which faded) and narrower than expected Australian trade surplus in August. The latter saw a more meaningful upside surprise in imports than in exports (the headline trade surplus remains elevated in a historical sense).

- Bills run 9-20bp cheaper through the reds, with dated OIS pricing of the RBA’s terminal rate moving back up to 3.80%.

- Looking ahead, A$700mn of ACGB Nov-25 supply is due on Friday, along with the release of the AOFM’s weekly issuance slate.

NZGBS: Off Worst Levels But Comfortably Cheaper On Broader Impetus

NZGBs held on to the bulk of their early cheapening (derived from wider core FI moves on Wednesday), running 10-12bp cheaper across the major benchmarks at the close, with light bear flattening seen.

- A brief round of support in the U.S. Tsy space helped NZGBs off of session cheaps,

- Today’s weekly NZGB supply passed smoothly enough (cover ratios on the May-28, Apr-33 and May-51 auctions all printed above 2.50%, aided by the move away from recent outright cheaps), with yields pulling further away from session highs post-auction.

- Comments from NZ Finance Minister Robertson failed to move the needle, as he pointed to NZ’s ability to avoid a recession (despite clear challenges), a focus on boosting worker availability via improving Visa processing , while underscoring the responsible fiscal approach that NZ has undertaken, sticking with previous forecasts re: a return to budget surplus (with any quickening of that timeline requiring austerity).

- Robertson also played down any sense of long-term worry re: the NZD, while noting that debt usage should be geared towards financing longer term projects (with some focus on productivity), stressing that he is comfortable with borrowing costs.

- A modest uptick in RBNZ terminal rate pricing has come alongside the move higher in yields, with dated OIS pricing a peak rate of 4.65%.

JAPAN: No Changes In Direction Of International Security Flows

There was no changes in net direction across the 4 major metrics within the weekly Japanese international security flow data.

- Japanese investors pared back their net sales of foreign bonds last week, but still lodged a 4th consecutive week of net sales.

- They also upped their net purchases of foreign stocks, registering a 3rd consecutive week of net buying in the process.

- Foreign investors pared back their net sales of Japanese bonds in the week that came after the latest BoJ decision (with the BoJ reaffirming its stance), although net selling still comfortably topped the Y1tn mark, allowing the 4-week rolling sum of the metric to plummet to fresh lows.

- Finally, offshore net sales of Japanese equities slowed from the sharpest rate observed since ’20 (observed in the prior week), with international investors now shedding Japanese equities for 6 consecutive weeks.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | -886.3 | -1102.5 | -3330.6 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 569.8 | 264.8 | 874.5 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | -1565.6 | -2862.8 | -6441.6 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | -501.8 | -1178.9 | -2601.0 |

Source: MNI - Market News/Bloomberg/Japanese Ministry Of Finance

AUSTRALIA: Skill Shortages Likely To Keep Pressure On RBA

The National Skills Commission (NSC) has published its skills priority list. The Australian reports that the number of occupations considered to be in shortage has risen to 286 this year from 153 a year ago. This is 31% of all occupations (19% 2021).

- Continued labour shortages suggest that while the RBA may have slowed the pace of rate hikes this month, the tightening cycle is not yet over and may now take longer.

- The NSC report shows that shortages in Australia’s labour market continue to be a problem in a wide range of areas (health, mining, transport, care, education, IT, construction).

- Employers apparently prefer to re-advertise, restructure or change job descriptions rather than increase pay to attract staff, according to the Australian. Thus partially explaining the moderate pick up in wage growth so far seen in Australia, and consistent with SEEK advertised salaries not accelerating and continuing to rise in line with the 2022 average of 0.3%m/m.

Source: MNI - Market News, Refinitiv, ABS

FOREX: Risk-On Flows Sap Strength From USD & JPY

The BBDXY almost halved yesterday's advance amid broad-based aversion to the greenback. General risk sentiment improved, with e-mini futures posting gains in a promising sign after U.S. equity benchmarks closed in the red on Wednesday. U.S. Tsy yields were slightly weaker, facilitating the dip in the U.S. dollar.

- Safe-haven currencies fell out of favour. The yen generally outperformed the greenback, but only by a narrow margin. U.S./Japan yield differentials were little changed.

- The Antipodeans benefitted from better sentiment, with the kiwi leading gains after the RBNZ's hawkish monetary policy review yesterday.

- The Aussie dollar was unfazed by an unexpected contraction in Australia's trade surplus, driven by a surprise 4% M/M jump in imports.

- Spot USD/CNH posted a 0.5% drop. Financial markets in mainland China remained closed for a public holiday.

- German factory orders, EZ retail sales and U.S. initial jobless claims take focus on the data front today. There is central bank rhetoric galore, as BoJ, Fed and BoE members will speak, while the ECB will publish the minutes from its September monetary policy meeting.

FX OPTIONS: Expiries for Oct6 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9900-02(E1.3bln)

- USD/JPY: Y142.00($1.1bln), Y144.00($800mln), Y145.00($836mln), Y145.50($1.2bln), Y145.90-00($855mln)

- EUR/GBP: Gbp0.8700(E649mln), Gbp0.8850(E695mln)

- AUD/USD: $0.6475(A$590mln)

ASIA FX: Won Outperforms On Robust Exports

The greenback rose in Asia on Wednesday, the dollar index rising above Tuesday's high briefly, risk sentiment was mostly positive which helped temper Asia EM losses.

- CNH: Offshore yuan is slightly weaker, the yuan showed limited reaction to the first contractionary print of China's Caixin Manufacturing PMI since April '20, with spot USD/CNH posting a small blip higher.

- SGD: Singapore dollar is flat, sticking to a narrow range through the session. On the coronavirus front there were 156 new cases in the past 24 hours, above 100 for the eighth consecutive day.

- KRW: Won is stronger, the best performer in Asia. Data earlier showed the trade surplus widened more than expected, exports grew for the tenth straight month in August driven by sales of chips and automobiles.

- TWD: Taiwan dollar is stronger, on track to gain for the seventh session of the past eight, data earlier showed Markit Taiwan manufacturing PMI slipped slightly to 58.5 from 59.7.

- MYR: Ringgit gained, the Finance Ministry released its first-ever pre-budget statement yesterday, noting that the 2022 federal budget will focus on the "recovery from the pandemic, rebuilding of national resilience and catalysing reforms".

- IDR: Rupiah dipped slightly, Indonesia's manufacturing sector remained deep in contraction in August, even as its pace decreased a tad, with Markit M'fing PMI edging higher to 43.7 from 40.1. CPI rose in line with estimates at 1.59% Y/Y.

- PHP: Peso is weaker, the Philippine manufacturing sector has plunged into contraction in August, according to the latest Markit PMI survey. The index fell to 46.4 from 50.4 recorded in July.

- THB: Baht is lower, nationwide count of new Covid-19 infections registered below 15,000 for the second straight day. As a reminder, Thailand is relaxing some of its mobility curbs from today.

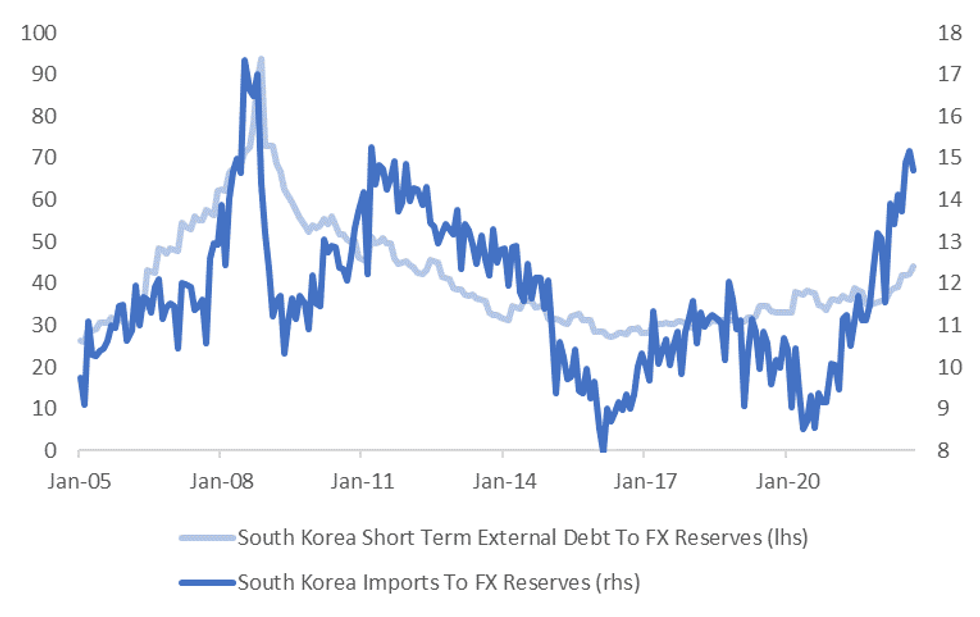

SOUTH KOREA: Ratio Of Imports/Short Term External Debt To FX Reserves Remains Below 2008 Highs

South Korea's FX reserves fell by $19.7bn in September. This is the largest monthly drop since the GFC in 2008. Headline FX reserves are now back to $416.8bn. As we noted yesterday, with September's USD/KRW gain of close to 7%, the strongest since September 2011, and the pair breaking through 1400, today’s print was likely to be a market focus point.

- The BoK also noted valuation impacts were a factor as well in terms of the headline drop. Note South Korean holdings of foreign securities fell to $379.4bn in September, down $15.53bn from August.

- We won't get official intervention estimates for several months though for Q3. For Q2 the BoK sold over $15bn to stem won losses.

- Such a fall will maintain focus on the country's vulnerability to further external shocks, particularly from a commodity price/energy bill standpoint. The chart below plots the ratio of imports and short term external debt to FX reserves.

- Both metrics are trending in the wrong direction, although we remain below 2008 highs, particularly on the short term external debt side.

Fig 1: South Korean Imports & Short Term External Debt Ratio To FX Reserves

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

EQUITIES: Equity Rally Extends; Chip Stocks Outperform

Most Asia-Pac equity indices are firmer at writing, bucking a mildly negative lead from Wall St. (major cash benchmarks closed ~0.1-0.3% softer on Wednesday), with a gauge of Asian stocks on track for a third straight higher daily close (MSCI Asia APEX 50: +0.3%).

- The TAIEX (+0.3%) was lifted by outperformance in semiconductors (+0.5%), reflecting a region-wide bid in semiconductor stocks ahead of heavyweight Samsung Electronics’ earnings on Friday (likely also benefiting from tailwinds after a Morgan Stanley note earlier in the week expressed bullishness on South Korean and Taiwanese chip stocks).

- South Korean equities have rallied for a third day, with the tech-heavy KOSDAQ (+2.7%) outpacing the benchmark KOSPI (+1.4%), reflecting the session’s chipmaker-led bid.

- The Nikkei 225 (+0.9%) is on track for a fourth consecutive higher daily close, operating a little below freshly-made three-week highs at typing, with the Information Technology sector (+1.8%) leading gains.

- The Hang Seng (-0.4%) bucked the broader trend of gains amongst regional peers, dragged lower by underperformance in China-based tech (HSTECH: -0.9%).

- E-minis deal 0.4-0.6% firmer apiece at writing, reversing earlier losses, but have failed to meaningfully break above their respective best levels established on Wednesday.

GOLD: Steadying Above $1,700/oz

Gold deals ~$4/oz firmer to print ~$1,721/oz at writing, operating towards the upper end of its range established on Wednesday.

- To recap, the precious metal closed ~$10 lower on Wednesday, paring gains from its recent two-day rally after above-expectations U.S. ISM services and ADP employment data contributed to a limited rally in the USD (DXY) and U.S. real yields.

- The recent rise in the DXY and nominal U.S. Tsy yields comes as sentiment re: a “Fed pivot” has moderated from its extremes following softer-than-expected JOLTS job data on Tuesday.

- Atlanta Fed Pres Bostic (‘24 voter) weighed in on the matter late on Wednesday, stating that the “inflation battle is likely still in early days”, reiterating that weaker economic data would not deter further Fed rate hikes.

- Looking ahead, a swathe of Fedspeak is due later on Thursday, ahead of the U.S. NFP print on Friday.

- From a technical perspective, gold has established a short-term bull cycle. Initial resistance is seen at ~$1,729.5 (Oct 4 high), with further resistance located at $1,735.1 (Sep 12 high and key resistance). On the other hand, initial support is seen at $1,695.2 (former trendline resistance).

OIL: Just Off Multi-Week Highs As OPEC+ Output Cut Lifts Sentiment

WTI and Brent are ~$0.20 firmer apiece, having struggled to stage a meaningful break above their respective Wednesday’s highs in Asia as the bullish impetus from OPEC+’s production quota cuts has moderated.

- To elaborate on the latter, both benchmarks notched fresh highs on Wednesday after OPEC+ announced a 2mn bpd cut to output quotas for November, closing ~$1.50-2.00 firmer apiece for a third straight higher daily close.

- WTI and Brent later hit session highs after U.S. crude inventory data pointed to a surprise drawdown in crude stocks (corroborating reports on API inventories on Tuesday). Gasoline and distillate stocks declined as well, while there was a small build in Cushing hub stocks.

- A note that despite the 2mn bpd headline cut in the OPEC+ target production quota, the actual decrease in output is likely to be significantly smaller, with the group continuing to miss collective output targets ahead of Wednesday’s meeting.

- Elsewhere, the White House has denied an earlier WSJ source report of the U.S. preparing to relax sanctions on Venezuela, potentially allowing energy giant Chevron to resume oil production in the country.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 06/10/2022 | 0600/0800 | ** |  | SE | Private Sector Production |

| 06/10/2022 | 0600/0800 | ** |  | DE | Manufacturing Orders |

| 06/10/2022 | 0700/0900 | ** |  | ES | Industrial Production |

| 06/10/2022 | 0730/0930 | ** |  | EU | IHS Markit Final Eurozone Construction PMI |

| 06/10/2022 | 0830/0930 | ** |  | UK | IHS Markit/CIPS Construction PMI |

| 06/10/2022 | 0900/1100 | ** | | EU | retail sales |

| 06/10/2022 | 1230/0830 | * |  | CA | Ivey PMI |

| 06/10/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 06/10/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 06/10/2022 | 1250/0850 | | US | Cleveland Fed's Loretta Mester | |

| 06/10/2022 | 1315/0915 | | US | Minneapolis Fed's Neel Kashkari | |

| 06/10/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 06/10/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 06/10/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 06/10/2022 | 1535/1135 | | CA | BOC Governor Macklem speech | |

| 06/10/2022 | 1700/1300 | | US | Fed Governor Lisa Cook | |

| 06/10/2022 | 1700/1300 | | US | Chicago Fed's Charles Evans | |

| 06/10/2022 | 1700/1300 | | US | Minneapolis Fed's Neel Kashkari | |

| 06/10/2022 | 2100/1700 | | US | Fed Governor Christopher Waller | |

| 06/10/2022 | 2230/1830 | | US | Cleveland Fed's Loretta Mester |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.