Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- DONALD TRUMP BECOMES FIRST FORMER US PRESIDENT GUILTY OF CRIMES - BBG

- WILLIAMS SAYS FED HAS TIME TO WAIT FOR MORE DATA - MNI BRIEF

- FED’S LOGAN SAYS POLICY MAY NOT BE AS RESTRICTIVE AS BELIEVED - BBG

- JAPAN MAY TOKYO CORE CPI RISES 1.9% VS. APRIL’S 1.6% - MNI BRIEF

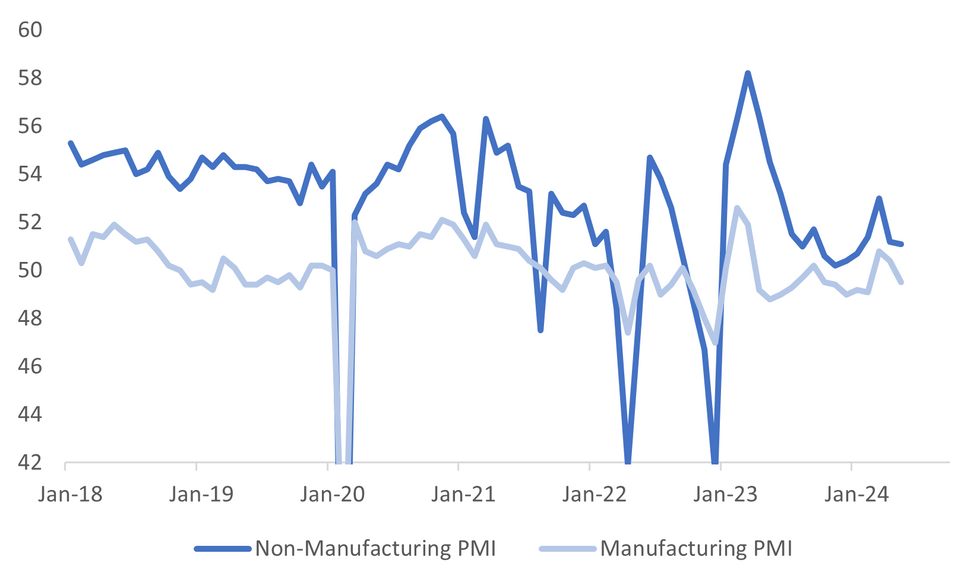

- CHINA MAY MFG. PMI CONTRACTS TO THREE-MONTH LOW - MNI BRIEF

- CHINA PAPER WARNS PBOC WILL SELL BONDS IF DEMAND SURGE CONTINUES - FINANCIAL NEWS

Fig. 1: China Manufacturing PMI Back Into Contraction Territory

Source: MNI - Market News/Bloomberg

UK

POLITICS (BBG): Keir Starmer’s purge of the left wing of his Labour Party has had a single, laser-focused aim: to make Britain’s opposition electable again after over a decade in the cold. But an escalating row over the treatment of the UK’s first Black woman MP risks undermining his control of the UK election campaign.

EUROPE

ECB (BBG): Economists are dialing back their expectations for how far the European Central Bank will lower interest rates after it starts cutting next week, according to a Bloomberg survey.

UKRAINE (BBG): President Joe Biden will allow Ukraine to launch US-provided munitions against military targets inside a limited area of Russia, overcoming concern that any such move could provoke a wider war with the West.

US

POLITICS (BBG): Donald Trump was found guilty in the first criminal trial of a former US president in the nation’s history, a verdict that could reshape the political landscape five months before Election Day.

FED (MNI BRIEF): A strong economy means the Federal Reserve does not need to be in a rush to make any imminent decisions about the future path of interest rates, New York Fed President John Williams said Thursday.

FED (MNI BRIEF): New York Fed President John Williams said Thursday interest rates will come down "at some point" without referencing any specific dates. The central bank has now held its benchmark overnight rate at a 23-year high for close to a year.

FED (BBG): Federal Reserve Bank of Dallas President Lorie Logan said high interest rates may not be restraining the economy as much as policymakers anticipate, emphasizing it’s important for officials to keep their options open for future adjustments.

US/CHINA (RTRS): U.S. Deputy Secretary of State Kurt Campbell and deputy national security adviser Jon Finer met China's Vice Foreign Minister Ma Zhaoxu in Washington on Thursday, a day after Washington accused Beijing's leadership of supporting Russia's war in Ukraine and warned that China could face further Western sanctions.

OTHER

JAPAN (MNI BRIEF): The year-on-year rise in the Tokyo core inflation rate accelerated to 1.9% in May from April's 1.6%, its first increase in three months but still below the Bank of Japan's 2% target for the second straight month, data from the Ministry of Internal Affairs and Communications showed on Friday.

JAPAN (MNI BRIEF): Japan's industrial output fell 0.1% m/m in April, its first drop in two months, following March's 4.4% gain, due to weaker production of transport equipment excluding motor vehicles, data released by the Ministry of Economy, Trade and Industry showed on Friday.

COMMODITIES (BBG): OPEC+ is pressing on with informal talks aimed at finalizing an agreement on oil-output cuts this weekend, officials said.

CHINA

MANUFACTURING (MNI BRIEF): China's manufacturing Purchasing Managers' Index dropped by 0.9 points to 49.5 in May, falling below the breakeven 50 level after expanding for two consecutive months, tamed by weak demand and the high base formed by rapid manufacturing growth earlier, data from the National Bureau of Statistics showed Friday.

BONDS (FINANCIAL NEWS): China’s current 10-year government bond yield is “relatively low” as the potential economic growth rate in the country is estimated at around 5%, and the central bank may sell bonds “when necessary,” according to a front-page report in the Financial News, a publication backed by the People’s Bank of China, citing analysts.

PRICES (ECONOMIC DAILY): China’s pork farmers became profitable in May after prices rebounded, surpassing production costs, the Economic Daily said in a report Friday.

FLOWS (SHANGHAI SECURITIES NEWS): Overseas investment in China’s equity markets rebounded in 2Q because policies supporting the property sector have improved risk appetite, Shanghai Securities News said in a report that cited analysts and fund managers.

MONEY SUPPLY (SECURITIES TIMES): China’s financial data including M2 money supply growth this month may largely decelerate as some resident and corporate deposits are converted into investment on long-term treasury bonds, with market liquidity converged, Securities Times reported.

CHINA MARKETS

MNI: PBOC Net Injects CNY98 Bln Via OMO Fri; Rate Unchanged

The People's Bank of China (PBOC) conducted CNY100 billion via 7-day reverse repo on Friday, with the rates unchanged at 1.80%. The operation has led to a net injection of CNY98 billion after offsetting the CNY2 billion maturity today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8000% at 09:27 am local time from the close of 1.9177% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 40 on Thursday, compared with the close of 41 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1088 on Friday, compared with 7.1111 set on Thursday. The fixing was estimated at 7.2398 by Bloomberg survey today.

MARKET DATA

AUSTRALIA APR PRIVATE SECTOR CREDIT M/M 0.5%; MEDIAN 0.4%; PRIOR 0.4%

AUSTRALIA APR PRIVATE SECTOR CREDIT Y/Y 5.2%; PRIOR 5.2%

JAPAN APR JOBLESS RATE 2.6%; MEDIAN 2.6%; PRIOR 2.6%

JAPAN APR JOB-TO-APPLICANT RATIO 1.26; MEDIAN 1.28; PRIOR 1.28

TOKYO MAY CPI Y/Y 2.2%; MEDIAN 2.2%; PRIOR 1.8%

TOKYO MAY CPI EX FRESH FOOD Y/Y 1.9%; MEDIAN 1.9%; PRIOR 1.6%

TOKYO MAY CPI EX FRESH FOOD, ENERGY Y/Y 1.7%; MEDIAN 1.8%; PRIOR 1.8%

JAPAN APR P INDUSTRIAL PRODUCTION M/M -0.1%; MEDIAN 1.5%; PRIOR 4.4%

JAPAN APR P INDUSTRIAL PRODUCTION Y/Y -1.0%; MEDIAN -1.1%; PRIOR -6.2%

JAPAN APR RETAIL SALES M/M 1.2%; MEDIAN 0.6%; PRIOR -1.2%

JAPAN APR RETAIL SALES Y/Y 2.4%; MEDIAN 1.7%; PRIOR 1.1%

JAPAN APR HOUSING STARTS Y/Y 13.9%; MEDIAN -0.1%; PRIOR -12.8%

CHINA MAY MANUFACTURING PMI 49.5; MEDIAN 50.5; PRIOR 50.4

CHINA MAY NON-MANUFACTURING PMI 51.1; MEDIAN 51.5; PRIOR 51.2

CHINA MAY COMPOSITE PMI 51.0; PRIOR 51.7

SOUTH KOREA APR INDUSTRIAL PRODUCTION M/M 2.2%; MEDIAN 1.0%; PRIOR -3.0%

SOUTH KOREA APR INDUSTRIAL PRODUCTION Y/Y 6.1%; MEDIAN 4.4%; PRIOR 1.0%

SOUTH KOREA APR CYCLICAL LEADING INDEX CHANGE 0.1; PRIOR -0.1

MARKETS

US TSYS: Treasuries Little Changed Ahead Of US PCE Later

- Treasury futures are little changed ahead of the US core PCE data later tonight. TU is -0.125 at 101-25.125, after hitting a session high of 101-25.75, while TY did briefly trade above Thursday's highs, however now trade little changed at 108-18.

- Volumes: TU 44.5k, FV 80.5k TY 110k

- Tsys flow: 2/5/10 Block, buyer FV on the fly in 636k DV01.

- Cash treasury curve is little change, yields are flat to 0.5bps lower. The 2Y unchanged at 4.925% while the 10Y -0.2bp at 4.544%.

- US overnight indexed swaps are now pricing more than 80% odds for a 25bps rate cut in November

- Local rates market: ACGB yield are 3-5bps lower, 5yr supply was well supported, NZGBs are 6-10bps lower as market digests the budget and following strong auction results across 7, 10 & 15yr tenors, while JGBs are 1-3bps higher, with the 10Y yield at 1.069% just off recent highs.

- Looking ahead; PCE, Personal Income/Spending and MNI's Chicago PMI, while Atlanta Fed Pres Bostic will speak.

JGBS: Weaker, As Bear Trend Remains Intact, Wages & BoJ Speak Next Week

JGB futures sit close to session lows in recent dealings. JBM4 was last at 143.02, -.18 versus settlement levels. This remains consistent with the broader technical backdrop, with a bear trend in place. Lows from yesterday rest sub 142.90.

- Post the earlier data flurry there hasn't been much in the way of major drivers. The BoJ bond ops were unchanged from the prior outcome, while the 3 month bill sale didn't impact sentiment.

- The data earlier showed close to expected Tokyo May CPI outcomes. Some of the core measures showed further deceleration versus the April y/y pace and services inflation looked to have cooled.

- Other data was mixed with retail sales better than expected (+1.2% m/m, versus 0.6% forecast), but IP fell 0.1% m/m (against a +1.5% forecast).

- In the cash JGB space, yields sit higher. The 10yr firming back towards 1.07%. The 30yr is up 2bps to 2.23%. In the swaps space, the 10yr is back above 1.09%.

- Next week Q1 Capex is out along with April wages. We also have BoJ speak, along with 10y and 30y debt auctions.

AUSSIE BONDS: ACGBS Richer, Curve Slightly Flatter Post 5yr Auction

ACGBs (YM +5.0 & XM +4.0) are richer and trade near session's best. Earlier, we had Private Sector Credit come in just above consensus at 0.5%m/m vs 0.4% est, while we also had the Nov-29 Bond auction, which was well received with a bid/cover ratio of 3.2286%

- Cash US tsys are are about 0.5bp richer today, the curve is unchanged. Tsys futures have traded in very tight ranges, will the only notable flow a 2/5/10 Block, buyer FV on the fly in 636k DV01.

- Cash ACGBs are 3-4.5bps richer, the curve is slightly flatter with the AU-US 10-year yield differential 1bps higher at -15bps.

- Swap rates are 1-3bps lower

- The bills strip is flat to 3bps higher, curve has bear-steepened

- RBA-dated OIS pricing is 2-5bps softer at the Sept & Nov meetings today, with a17% cut into year end.

- Looking ahead; MI Inflation on Monday, and GDP on Wednesday

NZGBS: Richer Post The Budget, FinMin Says Budget To Assist RBNZ

NZGBs closed 5-9.5bps richer, the curve bear-steepened, the calendar was empty today although we did have a 7, 10 & 15yr bond auction, bid/cover across all lines increased from prior auction, although total successful bids were well done.

- NZGB curve is tighter today, the 2y is -6.2bps at 4.877%, while the 10yr is -7.5bps at 4.800%.

- NZ FinMin Nicola Willis has received a letter alleging RBNZ Governor Orr breached the bank’s code of conduct, prompting discussions about the central bank's independence and its handling of employment matters, following Orr's response to criticism from the NZ Initiative regarding prudential regulation and banking competition.

- The FinMin has also defended her budget, stating that despite tax cuts, its overall effect is disinflationary, aiming to assist the RBNZ rather than hinder it. Economists raised concerns that the budget's less contractionary fiscal stance may complicate the central bank's efforts to tackle inflation and could make it more nervous about potential growth.

- Swap rates are flat to 1.5bps, the curve has bear-flattened

- RBNZ dated OIS pricing is 2-4bps lower heading into Nov meeting with A cumulative 23.5bps of easing is priced by year-end.

- Looking ahead: ANZ Commodity Price on Thursday

FOREX: USD Marginally Higher, Japan MoF Intervention Figures Out Later

The BBDXY index sits marginally higher, last just above the 1253.25 level. Overall FX moves have been fairly contained though in the first part of Friday trade.

- The BBDXY sits higher for the week, albeit away from Thursday highs (near 1256.6). Today, cross asset signals have been mixed. US equity futures sit lower, but regional Asia Pac markets are higher. US yields are close to unchanged.

- USD/JPY got just under 156.60 earlier, but sits back at 156.80 in latest dealings, unchanged for the session. FinMin Suzuki reiterated familiar FX verbal jawboning, which provided some yen support but there was no follow through.

- Japan had a number of data releases, with most focus on the Tokyo CPI print. IT was close to expectations, albeit with some further loss of momentum for y/y core prints.

- AUD/USD is around 0.6630, down a touch for the session. We had softer than forecast China PMI prints. This didn't impact sentiment greatly. NZD/USD is a touch higher but at 0.6120 remains comfortably within recent ranges.

- EUR/USD sits lower last near 1.0815, aiding the broader recovery in USD indices.

- Looking ahead, we have Japan MoF intervention data (out early evening Tokyo time). Eurozone CPI figures will be the focus of the European session before US April PCE deflator and Canadian GDP round off the week’s calendar.

ASIA STOCKS: Hong Kong & China Equities Higher, China To Target Property Supply

Hong Kong & Chinese equities are higher today, largely tracking global markets. Earlier China Manufacturing PMI was below consensus coming in at 49.5 vs 50.5 and non-manufacturing was 51.1 vs 51.5 composite PMI was 51 in May down from 51.7 in Apr, later today we have Hong Kong Retail Sales, with consensus at -6.3%, up from -7% in March. China Vanke is in talks with banks to secure a $6.9b loan.

- Hong Kong equities are higher today, with property indices are again the worst performing, the Mainland Property Index is down 0.10%, while the HS Property Index is up just 0.20%, elsewhere HSTech Index is faring better up 1%, while the wider HSI is up 0.95%. In China onshore markets, the CSI300 is 0.20% higher, the CSI 300 Real Estate Index is up 1.67%, small cap indices the CSI1000 & CSI2000 are up 0.67% and 0.90% respectively, while the ChiNext is up 0.54%

- (MNI): China May Mfg. PMI Contracts To Three-Month Low - (See link)

- In the property space, Chinese policymakers are targeting the reduction of a massive housing inventory, with over 60 million unsold apartments, to address the nation's property slump. Despite recent government initiatives, including a 300 billion yuan initiative to purchase unsold homes, challenges remain in reviving home sales and alleviating oversupply issues, particularly in larger cities. China Vanke is in advanced talks with major banks for a record-breaking loan of about 50 billion yuan ($6.9 billion), aimed at alleviating liquidity concerns and avoiding potential defaults, with the facility backed by real estate assets totaling around 80 billion to 90 billion yuan, part of an asset package for collateralization.

- Looking ahead: Caixin China PMI Mfg on Monday

ASIA PAC STOCKS: Asian Equities Higher, Japanese Banks Benefit From Higher Yields

Asian equities have climbed Friday as the latest round of US economic data signaled momentum is slowing, boosting the case for the Federal Reserve to start cutting interest rates this year. The MSCI Asia Pacific is trading up over 0.60% led by gains in Japan and Australia. Earlier we had Japanese Jobs, Tokyo CPI, Industrial Production and Retail Sales, South Korean Industrial Production and Australian Private Sector Credit. Elsewhere local rates have found some support, although JGBs yields are a touch higher this morning however off highs made on Thursday.

- Japanese equities are higher today, banking stocks are the top performing sector today they are being well supported by higher yields as the 10Y trades just off multi year highs. Further moves higher may be limited as the market now awaits the Fed Reverse's favorite price gauge due out later today. Earlier, we had had a flurry of local data - Jobless rate was in line at 2.6%, Job-To-Applicate Ratio was 1.26 vs 1.28 est, Tokyo CPI was 2.2% vs 2.2% est, Industrial Production was -0.1% vs 1.5% est, while Retail Sales was 2.4% vs 1.7% est. The Topix is up 1.50%, with the Topix Bank Index up 2.02%, while the Nikkei 225 lags, trading up just 0.95%.

- Taiwan equities are slightly lower today, foreign investors have been selling local stocks recently with a total outflow of just over $2b. Late on Thursday, GDP came in slightly above estimates at 6.56% vs 6.50% est and saw the economy grow at the fastest pace since 2021, while the bureau of statistics now expected GDP to hit 3.94% this year up from their most recent forecast of 3.43%. The Taiex is down 0.13% today and trades off 1.10% for the week. The index still trades above all major moving averages, although the 14-day RSI has fallen about 15pts to 60 and the MACD indictor is showing decreasing green bars.

- South Korean equities are higher today. Earlier today we had industrial production come in well above consensus at 6.1% vs 4.4%, and SK chip stockpiles shrank at the fastest pace in 10 year showing just how much demand there currently is for especially for customers developing AI technologies. Samsung has contributed the most to the gains in the Kospi, although we are off morning highs and now trade just 0.50% higher for the session, the small-cap Kosdaq is up 0.35%.

- Australian equities are higher today, although we are on track to close the week lower. Earlier, we had Private Sector Credit, which beat estimates coming in at 0.5% vs 0.4% and up from a revised 0.4% in March we also had a bond auction which was well recovered with a bid/cover ratio of 3.22x up from 2.57x from the last auction in March. Most sectors are in the green today, other than Material and Tech stocks. Currently the ASX200 is up 0.43%.

- Elsewhere in SEA, New Zealand equities closed up 1.75% following the release of the budget on Thursday, Indonesian equities are 0.65% lower and have broken below Thursday and the YTD lows, Singapore equities are 0.30% higher, Indian Equities are 0.30% higher while Philippines & Malaysian equities are little changed.

COMMODITIES: Oil Tracking Lower Ahead Of OPEC Meeting, Gold Steady

Oil prices have continued to track lower, following sharp losses in Thursday trade. The front month WTI contract is off a further 0.45%, last tracking near $77.60/bbl. For Brent, front month is just under $81.60/bbl. Both benchmarks are tracking slightly lower for the week.

- Markets are looking ahead to the OPEC+ meeting June 2 where the group are widely expected to rollover current cuts into the second half of the year. OPEC+ members who have agreed to voluntary cuts totalling 2.2m b/d are discussing extending them until year-end, Reuters said, citing sources within the bloc.

- Thursday's dip also came even despite a larger than expected draw in US stocks. Broader risk off/concerns around the Fed outlook weighed in the space.

- Brent prompt time spreads are also painting a more amply supply backdrop.

- For WTI, the trend direction remains down, and the recovery from earlier in the week appears to be a correction - for now. A resumption of weakness would signal scope for a move towards $75.64, the Mar 11 low. Initial firm resistance to watch is at $83.63, the Apr 26 high.

- Gold hasn't shown a strong directional trend in the first part of trade. We were last near $2343, little changed for the session. We are still tracking higher for the week. Recent lows came in at $2322.8, which is close to the 50-day MA.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 31/05/2024 | 0600/0800 | ** |  | DE | Retail Sales |

| 31/05/2024 | 0600/0800 | ** | | DE | Import/Export Prices |

| 31/05/2024 | 0600/0700 | * |  | UK | Nationwide House Price Index |

| 31/05/2024 | 0630/0730 | | UK | DMO to release FQ2 (Jul-Sep) gilt operations calendar | |

| 31/05/2024 | 0630/0830 | ** |  | CH | Retail Sales |

| 31/05/2024 | 0645/0845 | *** |  | FR | HICP (p) |

| 31/05/2024 | 0645/0845 | ** | | FR | PPI |

| 31/05/2024 | 0645/0845 | ** | | FR | Consumer Spending |

| 31/05/2024 | 0645/0845 | *** | | FR | GDP (f) |

| 31/05/2024 | 0800/1000 | *** |  | IT | GDP (f) |

| 31/05/2024 | 0830/0930 | ** | | UK | BOE M4 |

| 31/05/2024 | 0830/0930 | ** | | UK | BOE Lending to Individuals |

| 31/05/2024 | 0900/1100 | *** |  | EU | HICP (p) |

| 31/05/2024 | 0900/1100 | *** | | IT | HICP (p) |

| 31/05/2024 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 31/05/2024 | 1230/0830 | *** |  | CA | GDP - Canadian Economic Accounts |

| 31/05/2024 | 1230/0830 | *** | | CA | Gross Domestic Product by Industry |

| 31/05/2024 | 1230/0830 | *** | | CA | CA GDP by Industry and GDP Canadian Economic Accounts Combined |

| 31/05/2024 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 31/05/2024 | 1345/0945 | *** | | US | MNI Chicago PMI |

| 31/05/2024 | 1500/1100 | | CA | Finance Dept monthly Fiscal Monitor (expected) | |

| 31/05/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 31/05/2024 | 2215/1815 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.