EXECUTIVE SUMMARY

- FED’S COLLINS, MESTER - INFLATION DROP TO TAKE LONGER - MNI BRIEF

- ECB’s LAGARDE SEES JUNE CUT WITH INFLATION ‘UNDER CONTROL’ - BBG

- UK APRIL WAGE SETTLEMENTS EDGE HIGHER - BRIGHTMINE - MNI BRIEF

- JAPAN APRIL EXPORTS RISE, AUTO SHIPMENTS HIGHER - MNI BRIEF

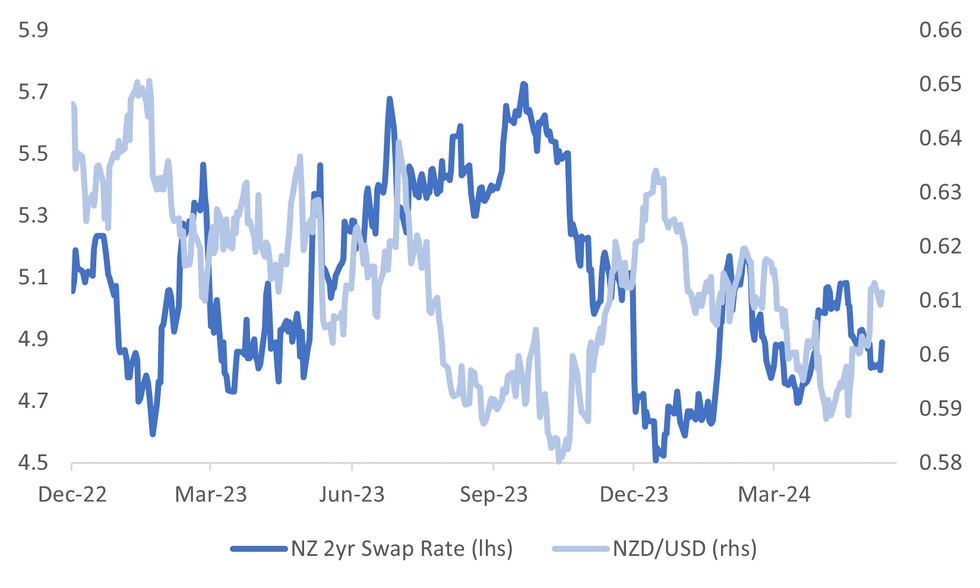

- RBNZ MPC HOLDS OCR AT 5.5% - MNI BRIEF

Fig. 1: NZD/USD & 2yr Swap Rates

Source: MNI - Market News/Bloomberg

UK

WAGES (MNI BRIEF): UK wage settlements edged higher in the three months to April, but came in lower than corresponding deals a year ago, a Brightmine survey showed.

BOE (MNI BRIEF): Central bank balances will shrink to the point where it meets the minimum level desired by commercial banks and other counterparties, Bank of England Governor Andrew Bailey said in a speech at the LSE, noting an inevitablity that there will be a significant increase in repo operations to meet demand.

UK/CHINA (MNI BRIEF): British firms in China have not seen a "meaningful opening up" despite government efforts aimed at boosting foreign business environment, according to the British Chamber of Commerce annual sentiment survey published Wednesday.

EUROPE

ECB (BBG): European Central Bank President Christine Lagarde indicated that an interest-rate cut is probable next month with the rapid gain in consumer-price growth now largely contained.

ECB (HANDELSBLATT): European Central Bank Governing Council member Joachim Nagel sees a positive trend in euro-area salaries, but urged caution on interest rates after a likely first cut in June.

EU (MNI BRIEF): European Commission President Ursula von der Leyen called on Tuesday for a European Air Defence Shield funded either by national contributions or by giving the EU the right to levy more direct taxes.

POLITICS (POLITICO): Less than three weeks before the EU election and Europe’s far right appears to be in crisis after France’s National Rally said it won’t sit alongside Germany’s Alternative for Germany (AfD) party in the next European Parliament.

U.S.

FED (MNI BRIEF): It will take more time than previously believed for inflation to return to the Federal Reserve’s 2% target, Boston Fed President Susan Collins and Cleveland Fed President Loretta Mester said Tuesday.

FED (MNI): Recent U.S. economic data indicate high interest rates are helping to cool off demand and disinflation has likely resumed, but the Federal Reserve needs to see several more months of good inflation data before cutting rates, Governor Christopher Waller said Tuesday.

HOUSEHOLDS (MNI): Ongoing price increases continued to pressure U.S. households' sense of financial security at the end of 2023, the Federal Reserve reported Tuesday, with those doing at least okay financially still well below highs in 2021 and parents feelings particularly gloomy.

US/CHINA (NYT): German carmaker BMW AG imported thousands of vehicles that included parts banned under a US law targeting forced labor in China, the New York Times reported, citing a Senate committee investigation.

OTHER

JAPAN (MNI BRIEF): Japan's exports posted their fifth straight y/y rise in April, up 8.3% following higher automobile and semiconductor shipments, data released by the Ministry of Finance showed on Wednesday.

NEW ZEALAND (MNI BRIEF): The Reserve Bank of New Zealand monetary policy committee held the Official Cash Rate steady at 5.5% Tuesday, lifting its end of year CPI projection 40 basis points to 2.9% and its OCR outlook 10bp to 5.7% by December. In a statement, the MPC said its current stance is sufficient to bring inflation back to its 1-3% target.

CHINA

TRADE (BBG): China may consider raising temporary tariffs on imported cars with large engines to a maximum of 25%, a Chinese trade lobby group said. The China Chamber of Commerce to the EU said the potential move carries implications for European and US carmakers, and comes after the Biden administration raised tariffs on Chinese electric cars to 100% and as the EU investigates alleged unfair advantages provided to Chinese automakers by government subsidies, according to a statement posted on X.

MORTGAGE RATES (CSJ): Several cities including Wuhan and Hefei have lowered housing mortgage rates to 3.25-3.45% for first-time buyers following the People’s Bank of China’s move to scrap the lower limit of the rates last week, China Securities Journal reported.

HOUSING (21ST CENTURY BUSINESS): Government real estate support may stabilize declines in local government land sale revenue in H2, after falling 21% in April y/y, according to Luo Zhiheng, chief economist at Yuekai Securities. Zhao Wei, chief economist at Guojin Securities, said fiscal intensity in H2 depended on land sale revenue performance, but analysts needed time to assess the impact of recent policy support.

REAL ESTATE (21ST CENTURY BUSINESS): Authorities must coordinate to prevent and control interwoven risks involving real estate, local-government debt, and small and medium-sized financial institutions, Vice Premier He Lifeng has told senior government leaders at a financial conference in Beijing.

CHINA MARKETS

PBOC conducts CNY2 bln via Omo weds; liquidity unchanged

The People's Bank of China (PBOC) conducted CNY2 billion via 7-day reverse repo on Wednesday, with the rates unchanged at 1.80%. The operation has led to no change to the liquidity after offsetting the CNY2 billion maturity today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8253% at 10:21 am local time from the close of 1.8470% on Tuesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 45 on Tuesday, compared with the close of 55 on Monday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1077 on Wednesday, compared with 7.1069 set on Tuesday. The fixing was estimated at 7.2372 by Bloomberg survey today.

MARKET DATA

JAPAN APRIL TRADE BALANCE -462.5B YEN; EST. -297.0B YEN; PRIOR +387.0B YEN

JAPAN APRIL EXPORTS RISE 8.3% Y/Y; EST. 11.0%; PRIOR +7.3%

JAPAN APRIL IMPORTS RISE 8.3% Y/Y; EST. 8.9%; PRIOR -5.1%

JAPAN APRIL ADJUSTED TRADE DEFICIT 560.76BLN YEN; PRIOR -681.9B YEN

JAPAN MARCH CORE MACHINERY ORDERS +2.9% M/M; EST. -2.0%; PRIOR +7.7%

JAPAN MARCH CORE MACHINERY ORDERS +2.7% Y/Y; EST. +1.4%; PRIOR -1.8%

SOUTH KOREA JUNE MANUFACTURING CONFIDENCE RISES TO 76; PRIOR 74

SOUTH KOREA JUNE NON-MANUFACTURING CONFIDENCE RISES TO 72; PRIOR 71

SOUTH KOREA APRIL PRODUCER PRICES RISE 1.8% Y/Y; PRIOR +1.5%

MARKETS

US TSYS: Treasury Futures Edge Lower, Ahead Of FOMC Mins Later

- Treasury futures have ticked lower in the second half of the trading session, the 10Y contract is (- 02) at 109-05+, while the 2Y contract is ( - 00.375) at 101-21+.

- Volumes: TU 35k, FV 42.5k, TY 50k

- Tsys flows: Large SOFR futures strip block, totaling 1.7mm DV01, looks to be a buyer.

- The treasury curve is little changed today, yields are about 1bps higher, the 2Y yield +0.8bp at 4.839%, 10Y +0.8 at 4.420%

- Regionally: ACBGs yields are 1-2bps higher curve has bear-flattened, NZGBs yields are 3-7bps higher, curve bear-flattened post a hawkish RBNZ, while JGBs are 0.5bps to 6bps higher, with the 10y now trading at 0.99%

- Earlier, the Fed's Bostic, Collins & Mester have been involved in a moderated discussion, with the key points from each; Bostic stated that the economy is incredibly resilient and that it will take longer for interest rates to influence decisions, Mester believes economic growth will be above trend this year, inflation will take longer to decrease, and current policy is well-positioned but needs monitoring while Collins emphasized the importance of patience in policy adjustments, noting that it will take longer to see progress and that a methodical, holistic approach is needed.

- Rate cut projections hold steady vs. late Monday: June 2024 at -5% w/ cumulative rate cut -1.2bp at 5.318%, July'24 at -20% w/ cumulative at -6.3bp at 5.267%, Sep'24 cumulative -19.9bp, Nov'24 cumulative -27.6bp, Dec'24 -43.7bp.

- Looking ahead: May 1 FOMC Minutes, Existing Home Sales and US Tsy 20Y Bond Sale.

JGBS: Bear-Steepener After A Poor 40Y Auction, FOMC Minutes Later Today

JGB futures are weaker and at session lows, -4 compared to the settlement levels, in afternoon trading.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Trade Balance and Machine Orders data.

- Cash US tsys are slightly cheaper in today’s Asia-Pac session ahead of the release of the May Meeting FOMC Minutes later today.

- The cash JGB curve has bear-steepened following today’s lacklustre 40-year auction, with yields flat to 4bps higher. The benchmark 10-year yield is 1.5bp higher at 0.995%, a new cycle high.

- The 40-year yield zone is 2.0bps in post-auction trading and approximately 4bps higher on the day.

- The swaps curve has bear-steepened, with rates flat to 4bps higher.

- Tomorrow, the local calendar sees Weekly International Investment Flow, Jibun Bank PMIs and Machine Tool Orders data alongside BoJ Rinban Operations covering 1-10-year JGBs.

AUSSIE BONDS: Slightly Richer, Narrow Ranges Ahead Of FOMC Minutes

ACGBs (YM flat & XM +1.0) are slightly stronger after dealing in narrow ranges in today’s Asia-Pac session. With the local calendar empty, local participants have been content to sit on the sidelines ahead of the release of the May FOMC Minutes later today.

- Cash US tsys are little changed in today’s Asia-Pac session after yesterday’s modest gains.

- Cash ACGBs are flat to 1bp richer, with the AU-US 10-year yield differential 2bps higher at -17bps.

- ACGBs have significantly outperformed their NZ counterparts, with the AU-NZ 10-year yield differential 7bps more negative, after the RBNZ delivered its policy decision. NZGBs closed 4-7bps cheaper. The 0.2pp overshoot of the RBNZ’s Q1 CPI forecast seemed to drive a hawkish shift. Rates may now need to stay restrictive for “longer than anticipated”. The RBNZ’s upward revision to its OCR path and the discussion of another hike reflect this. It said “rate cuts continue to be delayed”.

- Swap rates are flat.

- The bills strip is flat to -2.

- RBA-dated OIS pricing is flat to 1bps firmer across meetings. A cumulative 9bps of easing is priced by year-end.

- The local calendar will see Judo Bank Preliminary PMIs and Consumer Inflation Expectations data tomorrow.

NZGBS: Closed Sharply Cheaper After The RBNZ Pushes Out Rate Cut Expectations

NZGBs closed 4-7bps cheaper following the RBNZ’s decision to leave the OCR at 5.50%. The 0.2pp overshoot of the RBNZ’s Q1 CPI forecast seems to have driven a hawkish shift. Rates may now need to stay restrictive for “longer than anticipated”. The RBNZ’s upward revision to its OCR path and the discussion of another hike reflect this. It said “rate cuts continue to be delayed”.

- The NZ OCR is now not expected to be materially below 5.5% until H2 2025. The decision to leave rates at 5.5% was unanimous.

- (Dow Jones) The RBNZ signalled that interest rates might need to remain restrictive for longer than expected due to stubborn inflation, delivering a hawkish shock to money markets. (See link)

- Swap rates closed 5-9bps, with the 2s10s flatter.

- RBNZ dated OIS pricing closed 5-11bps firmer for meetings beyond July. A cumulative 33bps of easing is priced by year-end versus 43bps before today’s decision.

- Tomorrow, the local calendar will see Retail Sales Ex Inflation data along with RBNZ Governor Orr's appearance in front of the Parliamentary Finance & Expenditure Select Committee.

- Tomorrow, the NZ Treasury plans to sell NZ$250mn of the 3% Apr-29 bond, NZ$175mn of the 2% May-32 bond and NZ$75mn of the 1.75% May-41 bond.

FOREX: USD Index Steady, NZD Surges On Hawkish RBNZ Hold Before Trimming Gains

The BBDXY is little changed in the first part of Wednesday dealings, last around 1247.55. This has masked noticeable outperformance from the NZD, post a hawkish hold from the RBNZ.

- The RBNZ revised the OCR track higher, along with the inflation outlook. We have seen a sharp rise in NZGB yields as a result (5-8bps, led by the front end).

- NZD/USD got to highs of 0.6152 but we sit back around 0.6120/25 in recent dealings, still +0.50% firmer for the session. RBNZ Chief Economist Conway pushed back against market pricing of a Dec hike at the press conference. Still, Governor Orr noted raising rates at this meeting was a real consideration.

- Upside focus for NZD is likely to rest at 0.6200/20 (round number, March 8 High). Note the 200-day EMA is back near 0.6075.

- AUD/USD has been relatively steady, dragged higher by NZD but now back to flat at 0.6665. The AUD/NZD cross got to lows of 1.0861 (close to the 100-day EMA at 1.0857), but we sit slightly higher now, around 1.0880/85.

- Trends have been relatively quiet elsewhere. USD/JPY has drifted higher but remains within Wednesday ranges. We were last 156.30/35.

- In the cross asset space, US trends have been very steady in terms of equity futures and yields.

- Looking ahead, Wednesday’s calendar is highlighted by UK inflation data and the FOMC minutes of the May meeting.

ASIA PAC EQUITIES: Equities Mixed Ahead of Nvidia Earnings And FOMC Minutes

Asia markets have traded mixed today, while ranges have been tight. Stocks in Japan are lower as yields tick higher, yen ticked lower and some investors await Nvidia's earnings, while elsewhere in the region markets are higher with Taiwan's chip related stocks in particular TSMC performing the best. Today, we had Fed official speaking earlier this morning where they reiterated their higher for longer message, the RBNZ left rates unchanged which was widely expected, however they were more hawkish than the markets were expecting. Later today we have the BI rate decision who are also expected to keep rates on hold and the FOMC minutes will be a focus later tonight.

- Japanese equities have opened slightly lower today, and have remained rangebound since as investors await results from Nvidia and the minutes from the FOMC meeting. Earlier, Trade balance data show the deficit has increased to -¥462.5b from a revised ¥387.0b, exports increased to 8.3% from 7.3% in March, while imports increased to 8.3% from a revised -5.1% in March, core machine orders beat estimates coming in at 2.9% m/m vs -2.0% m/m. The Topix is down 0.57%, while the Nikkei 225 is faring slightly worse due to the higher concentration of tech stocks, down 0.69%.

- South Korean equities are off earlier highs and now trade unchanged for the day. Earlier, PPI was 1.8% y/y in Apr, up from a revised 1.5% y/y in March, while both business surveys increased with manufacturing rising to 76 from 74, and non-manufacturing rising to 72 from 71.

- Taiwan equities are are the top performing in the region today, led higher by TSMC in a sign markets may be expecting positive results out from Nvidia. Later today we have the unemployment rate due out which is expected to be unchanged at 3.40%. The Taiex is up 1.35%.

- Australian equities are little changed today and off earlier highs Australian related chicken stocks have fallen after the agriculture department said they are investigating an incident of bird flu. Gains in Financials & materials are being offset by losses in Consumer discretionary and Communications, with the ASX200 now unchanged.

- Elsewhere in SEA, New Zealand equities closed up 0.20%, however off about 0.40% post the hawkish RBNZ, Indonesian equities are up 0.68% ahead of BI later today,Indian equities are up 0.15% and Philippines equities are down 0.47%

ASIA STOCKS: HK & China Equities Off Earlier Highs, Short Positions Increase

Hong Kong & Chinese equities are mixed today, and off earlier highs, there has been very little in the way of domestic drivers today with no economic data out for either region. Short positions have increased against iShares China Large-Cap Fund & iShares MSCI China ETF, while short positions against iShares MSCI EM Ex-China fund fell to near zero, in a sign investors may think the recent equity rally has come to an end.

- Hong Kong equities are mostly higher today with property leading the way, the Mainland Property Index is up 1.93%, while the Hang Seng Property Index is up just 0.55%, the HSTech Index is up 0.75% after being down over 3% on Tuesday while the HSI is up 0.19%. In China onshore markets, equities are little changed after initial opening in the red the CSI300 is up 0.06% while the small-cap indices CSI1000 is down 0.32% & CSI2000 is unchanged, the growth focused ChiNext is up 0.15%

- (MNI) China Lacking Meaningful Opening - Britcham (See link)

- Looking ahead, quiet week for China on the data front.

OIL: Crude Continues Slide, Waiting For EIA Data

Oil prices have continued falling during today’s APAC trading after a 1.4% drop on Tuesday driven by a reported US crude stock build. Brent is down 0.7% to $82.31/bbl after a low of $82.15, and WTI -0.8% to $78.05 with a couple of brief breaks below $78. The USD index is little changed.

- Bloomberg reported that oil rose 2.5mn barrels and gasoline 2.1mn but there was a distillate drawdown of 300k, according to people familiar with the API data. The official EIA numbers are released later today but the market’s focus is on the June 1 OPEC+ meeting.

- OPEC has cut output by around 2mbd and while an extension into H2 is widely expected the details, such as how much and how long, remain unclear.

- Later the Fed’s Goolsbee appears and the May FOMC meeting minutes are published. There are US existing home sales and UK April CPI/PPI print. The BoE’s Breeden speaks.

GOLD: Consolidating Ahead Of FOMC Minutes

Gold is 0.3% weaker in the Asia-Pac session, after closing 0.2% lower at $2421.05 on Tuesday. With the release of the May FOMC Minutes later today, Tuesday’s price action represented a consolidation after the yellow metal hit a fresh all-time high on Monday.

- The US Short-Term Interest Rate market has this week reduced the odds that the Federal Reserve will deliver two rate cuts this year, even as some US policymakers deliver cautiously optimistic views on the path forward for borrowing costs. Higher rates are negative for gold, as it doesn’t pay interest.

- According to MNI’s technicals team, yesterday’s initial gains resulted in a print above resistance at $2431.5, the Apr 12 high and bull trigger. The break confirmed a resumption of the primary uptrend and paved the way for a climb towards 2452.5 next, a Fibonacci projection.

- On the downside, the 50-day EMA, at $2288.7, represents a key support. A clear break of it would be bearish.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 22/05/2024 | 0600/0700 | *** |  | UK | Consumer inflation report |

| 22/05/2024 | 0600/0700 | *** | | UK | Producer Prices |

| 22/05/2024 | 0600/0700 | *** | | UK | Public Sector Finances |

| 22/05/2024 | 0600/0800 | ** |  | SE | Unemployment |

| 22/05/2024 | 0805/1005 |  | EU | ECB's Lagarde at ESMA event on effectiveness of capital markets | |

| 22/05/2024 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 22/05/2024 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 22/05/2024 | 1245/1345 | | UK | BOE's Breeden Panellist on macroprudential policies | |

| 22/05/2024 | 1400/1000 | *** | | US | NAR existing home sales |

| 22/05/2024 | 1400/1000 | * | | US | Services Revenues |

| 22/05/2024 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 22/05/2024 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 22/05/2024 | 1800/1400 | *** | | US | FOMC Minutes |

| 23/05/2024 | 2300/0900 | *** |  | AU | Judo Bank Flash Australia PMI |