Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- SLOWLY PIVOTING TO CUTS, UNLIKELY IN MARCH - MNI FED WATCH

- ECB NEEDS MORE CONFIDENCE INFLATION IS HEADED TO 2%, LANE SAYS - BBG

- CHINA TO ENHANCE FISCAL SUPPORT VIA CGB ISSUE - MNI BRIEF

- CAIXIN JAN MANUFACTURING PMI RERMAINS FLAT FROM DEC - MNI BRIEF

- JAPAN Q4 GDP TO RISE 0.3% Q/Q; 1.4% ANNUALISED - MNI BRIEF

- JAPAN UNION SEEKS AT LEAST 6% PAY RISE TO PUSH BOJ POLICY - BBG

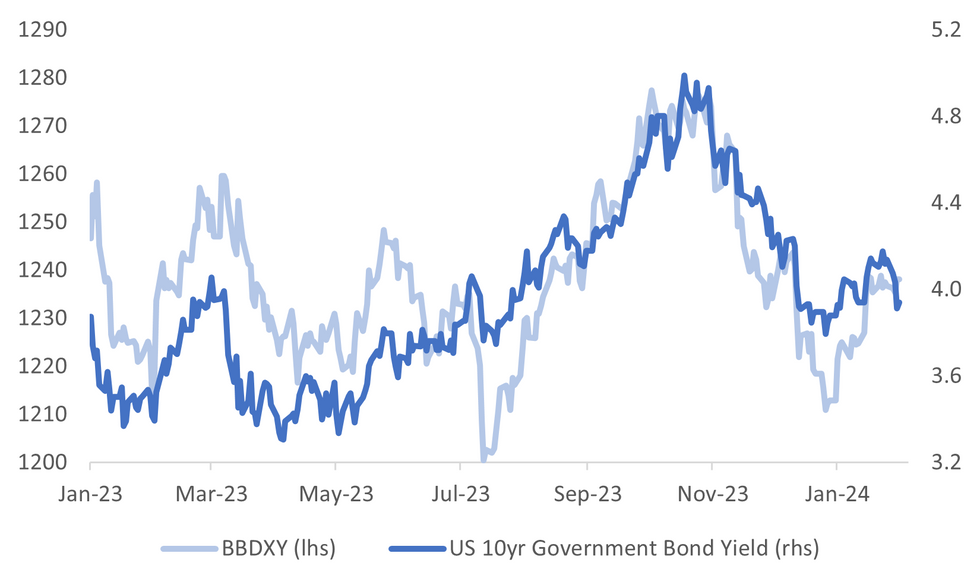

Fig. 1: US BBDXY Index & US 10yr Nominal Tsy Yield

Source: MNI - Market News/Bloomberg

U.K.

FISCAL (BBC): Jeremy Hunt has said there is likely to be less scope for tax cuts in the March. Budget than there was last autumn. The chancellor told the BBC he wanted to "lighten the tax burden" to help grow the economy. But he said this had to be done in a "responsible" way.

POLITICS (BBC): A deal between the UK government and the Democratic Unionist Party (DUP) will reduce checks and paperwork on goods moving from Great Britain to Northern Ireland. The changes apply to GB goods which are staying in Northern Ireland and will mean no routine checks on those goods.

EUROPE

ECB (BBG): European Central Bank officials need more evidence that inflation is returning to their target before they decide it’s safe to begin loosening monetary policy, according to Chief Economist Philip Lane.

FISCAL (MNI BRIEF): The European Parliament aims to finalise Trilogue talks with the European Union’s Belgian presidency and the European Commission on proposed reforms to the bloc’s fiscal rules by Feb 9, but parliamentarians and other sources said the timetable would be tight.

GERMANY (DEUTSCHE WELL): Starting on February 1, 45 companies in Germany are test-driving a 4-day workweek.

GERMANY (DEUTSCHE WELL): In the year's first Bundestag general debate, German Chancellor Olaf Scholz spared with the conservative opposition, but both sides of the political spectrum agreed on denouncing the far-right AfD.

RUSSIA (BBC): Kremlin challenger Boris Nadezhdin says he has collected enough signatures to stand as a candidate in Russia's upcoming presidential election. The former MP has become known for his relatively outspoken criticism of Mr Putin and of Russia's full-scale invasion of Ukraine.

UKRAINE (DEUTSCHE WELL): Hungary is delaying an agreement on long-term EU aid for Ukraine. EU leaders gathering in Brussels on Thursday will press Budapest to unblock the funds. Deutsche Welle

U.S.

FED (MNI FED WATCH): The Federal Reserve Wednesday held interest rates at a 23-year high range of 5.25%-5.5% for a fourth straight meeting and shifted its forward guidance to a more neutral tone, but Chair Jay Powell said rate cuts likely aren’t imminent.

FISCAL (BBG): Key Republican senators are exploring dropping demands for new border restrictions and backing a stand-alone emergency aid package for Ukraine, Israel and Taiwan.

FISCAL (BBG): The House passed a $78 billion business and child tax break bill that would provide a boon for US companies with large capital and domestic research expenditures and hand President Joe Biden an election-year political victory.

OTHER

MIDDLE EAST (BBG): Negotiations are advancing for an agreement to pause the Israel-Hamas war and free civilian hostages captured by Hamas, people familiar with the matter said, in a deal that those involved believe could be a crucial step toward ending the four-month conflict.

JAPAN (MNI BRIEF): Japan's economy in Q4 2023 is expected to have grown for the first time in two quarters, thanks to stronger capital investment and net exports, although private consumption was flat, economists predicted.

JAPAN (BBG): One of Japan’s biggest unions plans to push for pay gains above 6% in a bid to kickstart a virtuous wage-price cycle that would enable the Bank of Japan to raise interest rates and strengthen the yen.

ASIA (RTRS): Asia's factories delivered a largely patchy performance in January, surveys showed on Thursday, as soft Chinese demand left the region's economies on a shaky footing at the start of 2024.

NEW ZEALAND (BBG): Adult minimum wage rate will increase to NZ$23.15 an hour from April 1, Workplace Relations and Safety Minister Brooke van Velden says in emailed statement.

BRAZIL (MNI BRIEF): The Central Bank of Brazil reduced its official Selic rate by 50bps to 11.25% for the fifth consecutive time on Wednesday and indicated more cuts of the same size in the "next meetings," keeping the plural forward guidance language that effectively commits policymakers to the current pace of easing until at least the May decision.

CHINA

FISCAL (MNI BRIEF): China will strengthen fiscal efforts to boost investment and consumption to support economic recovery, officials of Ministry of Finance told reporters on Thursday in a briefing.

MANUFACTURING (MNI BRIEF): China's Caixin manufacturing PMI registered 50.8 in January, flat from December, staying in the expansionary zone above the breakeven 50 mark for the third month, with pro-growth policies taking effect, the financial publisher said Thursday.

ECONOMY (21st Century Herald): The government should use investment to boost the economy after January’s PMI reading of 49.2 showed domestic demand remained insufficient, according to Zhang Liqun, a special analyst at the China Federation of Logistics and Purchasing. Going forwards, the PMI will remain moderate as domestic demand recovers, but the Spring Festival and uneven trade patterns will cause fluctuations, according to Zhou Maohua, macro researcher at China Everbright Bank.

PRICES (21st Century Herald): Authorities are carefully monitoring price fluctuations during the Spring Festival season and taking action to avoid risks that may affect the market order, according to Pu Chun, deputy director of the State Administration for Market Regulation.

US/CHINA (MNI BRIEF): U.S. firms in China have increased profit expectations and lowered risk assessment for U.S. China relations for 2024, according to a report by the American Chamber of Commerce on Thursday.

PROPERTY PRICES (RTRS): China's new home prices rose in January at the fastest monthly pace in nearly 2-1/2 years, according to a survey released on Thursday, following a slew of government support measures and expectations of further relaxation in homebuying policies.

CHINA MARKETS

MNI: PBOC Drains Net CNY423 Bln Via OMO Thurs; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY43 billion via 7-day reverse repo on Thursday, with the rates unchanged at 1.80%. The reverse repo operation has led to a net drain of CNY423 billion reverse repos after offsetting CNY466 billion maturity today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8000% at 09:26 am local time from the close of 1.8706% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 47 on Wednesday, compared with the close of 52 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1049 on Thursday, compared with 7.1039 set on Wednesday. The fixing was estimated at 7.1787 by Bloomberg survey today.

MARKET DATA

AUSTRALIA JAN. CORELOGIC HOUSE PRICE INDEX RISES 0.4% M/M; PRIOR +0.4% M/M

AUSTRALIA JUDO BANK JAN. MANUFACTURING PMI 50.1; PRIOR 47.6; PRELIM 50.3

AUSTRALIA 4Q EXPORT PRICES RISE 5.6% Q/Q; EST. +3.5%; PRIOR -3.1%

AUSTRALIA 4Q IMPORT PRICES RISE 1.1% Q/Q; EST. +0.6%; PRIOR +0.8%

AUSTRALIA 4Q NAB BUSINESS CONFIDENCE FALLS TO -6; PRIOR -1

AUSTRALIA DEC. BUILDING APPROVALS FALL 9.5% M/M; EST. +0.5%; PRIOR +0.3%

AUSTRALIA DEC. PRIVATE-SECTOR HOME APPROVALS FALL 0.5% M/M; PRIOR -4.3%

NZ JAN. CORELOGIC HOUSE PRICES FALL 2.7% Y/Y; PRIOR -3.3% Y/Y

CHINA JAN. CAIXIN MANUFACTURING PMI 50.8; EST. 50.8; PRIOR 50.8

SOUTH KOREA JAN. TRADE SURPLUS NARROWS TO $300M; EST. +$1.000B; PRIOR $4457M

SOUTH KOREA JAN. EXPORTS RISE 18% Y/Y; EST. +17.6%; PRIOR +5.0% Y/Y

SOUTH KOREA JAN. IMPORTS FALL 7.8% Y/Y; EST. -8.1%; PRIOR -10.8% Y/Y

SOUTH KOREA JAN. S&P GLOBAL MFG PMI 51.2; PRIOR 49.9

MARKETS

US TSYS: US Yields Recoup Some Of Wednesday's Losses

TYH4 is trading at 112-12+, + 02 from NY closing levels.

Not too much to speak about for Tsys today, we have remained rangebound all day, with a slight flattening of the curve occurring, cash yields are up 1-4.5bps.

- Slightly better selling in the front end of the curve in Asia trading as the 2Y yield is 4.5bps higher at 4.252%, while the 10Y yield is 2.6bps higher at 3.937%.

- Firms are pushing back their forecast for Fed cuts. Goldman Sachs has pushed back its forecast for the 1st Fed cut to May from March. It still expects 5cuts this year (BBG), with Abrdn sees fed cutting rates three times this year (BBG). This may be lending support to today's moves.

- TYH4 is still trading within initial resistance levels of 112-26+ from the highs of Jan 12th, while first support remains back at 110-26 from Jan 19th.

- Data Tonight: Weekly Claims, Flash PMIs, ISMs, followed by Non-Farm Payrolls on Friday

JGBS: Futures Richer & At Tokyo Session Highs After 10Y Supply

JGB futures are sharply higher, +30 compared to settlement levels, after dealing in a relatively narrow range in the Tokyo morning session. The catalyst for the move higher was a solid 10-year JGB auction. The low price matched wider expectations, the tail shortened, and the cover ratio improved to 3.648x from 2.904x at January’s auction. It is worth noting that the cover ratio has improved for two straight months after December’s cover was the lowest seen at a 10-year auction since 2021.

- Afternoon strength in JGB futures came despite a paring of yesterday’s post-FOMC gains in US tsys in today’s Asia-Pac session. US tsys are currently dealing 1-5bps cheaper across benchmarks. Market commentators have started to push back their forecast for Fed cuts.

- International Investment Flows and PMI Manufacturing data failed to be market-moving.

- Post-auction dealings have shown a change of fortune for cash JGBs. After cheapening in the morning session, JGBs are now 1-3bps richer across benchmarks, with the 10-year leading. The benchmark 10-year yield is 2.5bps lower at 0.707% versus the morning high of 0.747%.

- The swaps curve is dealing slightly richer beyond the 2-year. Swap spreads are wider.

- Tomorrow, the local calendar sees Monetary Base data, along with BoJ Rinban Operations covering 1-10-year JGBs.

AUSSIE BONDS: Little Changed & Near Cheaps, PPI Data & May-34 Supply Tomorrow

ACGBs (YM -1.0 & XM +0.5) sit little changed and near Sydney session cheaps as US tsys pare yesterday’s post-FOMC rally in today’s Asia-Pac session. Cash US tsys are dealing 1-4bps cheaper, with a flattening bias.

- Market commentators have started to push back their forecast for Fed cuts. Fed Chair Powell yesterday said policymakers were unlikely to pivot to rate cuts in March. Goldman Sachs has pushed back its forecast for the 1st Fed cut to May from March. They still expect 5 cuts this year (BBG). Aberdeen sees the Fed cutting rates three times this year (BBG). This may be lending support to today's US tsy moves.

- Today’s local data drop of House Prices, PMI, Terms of Trade, NAB Business Confidence and Building Approvals failed to be market-moving.

- Cash ACGBs are 1-2bps richer, with the AU-US 10-year yield differential 6bps higher at +6bps.

- Swap rates are flat to 2bps lower, with the 3s10s curve flatter.

- The bills strip has twist-flattened, with pricing -1 to +2.

- RBA-dated OIS pricing is 1-2bps softer across meetings. A cumulative 61bps of easing is priced by year-end.

- Tomorrow, the local calendar sees PPI and Home Loans data.

- Tomorrow, the AOFM plans to sell A$800mn of 3.75% 21 May 2034 bond.

NZGBS: Strength Given Up As US Tsys Post-FOMC Rally Is Pared

NZGBs closed 3-4bps richer but well off the session’s best levels. There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined CoreLogic residential property prices. However, weekly supply saw lacklustre demand metrics, with cover ratios ranging from 1.32x to 1.88x. That likely contributed to the through-the-session cheapening.

- That said, the key driver of the move away from the session’s best levels was likely to have been today’s partial give-back of yesterday’s post-FOMC gains in US tsys. They are currently dealing 2-4bps cheaper across benchmarks in today’s Asia-Pac session.

- Firms are pushing back their forecast for Fed cuts. Goldman Sachs has pushed back its forecast for the 1st Fed cut to May from March. They still expect 5 cuts this year (BBG). Aberdeen sees the Fed cutting rates three times this year (BBG). This may be lending support to today's moves.

- Swap rates closed 1-3bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed flat to 4bps softer across meetings, with Oct-Nov leading. A cumulative 94bps of easing is priced by year-end.

- Tomorrow, the local calendar will see ANZ Consumer Confidence and Building Permits data.

FOREX: USD Up From Earlier Lows, A$ Underperforms

JPY and NZD are modestly higher against the USD, but the rest of the G10 block has struggled as Thursday session has unfolded so far. The BBDXY got close to 1235.7 in earlier trade, but we now sit back near 1237, down only slightly for the session.

- Cross asset focus has been on some modest recover in US yields post Wednesday's slump. Some sell-side names have shifted out their expectation for when the Fed starts cutting. The front end has led the moves, the 2yr up nearly 4bps to 4.24%.

- This has likely kept USD/JPY dips supported to a degree. For this pair, we saw lows of 146.48, but we sit back near 146.75 now. Earlier highs were at 147.08.

- NZD has firmed back to 0.6125, but remains within recent ranges (highs for the session at 0.6141). Some support likely evident from the better US equity futures tone, with Nasdaq futures up close to 0.45%.

- The same can't be said for AUD, last near session lows in the 0.6555/60 region. Earlier highs came close to 0.6580. This underperformance may reflect market pricing around potential RBA cuts in Q2 of this year post yesterday's Q4 CPI update. Metals prices are mixed, with iron ore slightly higher, while copper is down.

- The AUD/NZD cross is back close to 1.0700, near Jan lows.

- EUR/USD has spent most of the session fairly close to 1.0800.

- Looking ahead, there is US Q4 productivity/ULC, jobless claims, January manufacturing PMI/ISM as well as European PMIs and euro area January CPI. The Bank of England meets and is expected to leave rates unchanged. ECB’s Lagarde and Lane make appearances.

CHINA EQUITIES: Equities Rebound, After Vice FinMin Pledges Support For Economy

Hong Kong and Mainland China Equities are higher today, erasing early morning moves after Comments from the Vice Finance Minister around continuing to develop the chip and tech sectors has likely aided sentiment in this space. The minister also stated that broader fiscal policy will continue to aid the domestic demand recovery. The CSI 300 rebounding to +0.75%, Hang Seng up 1.35%, while the tech Index is up 3.20%

- Hong Kong, is being led higher by the tech index, trading 3.20% higher so far, as they brush of poor earnings from some of the Big US Tech stocks this week. The HSTECH sub index may also be seeing some support around the 3000 level, which has marked recent lows. Elsewhere the property index is trading 0.75% higher, after being down 1.1% at one point after new home sales from the nation’s largest developers tumbled and “underwater mortgage” levels in Hong Kong surged to a two-decade high.

- China had PMI data out earlier, holding steady at 50.8, markets initially didn't react positively to the PMI data, with all major benchmarks trading lower on the day, however once the Vice Finance Minister spoke markets keeping changed directions, CSI 300 now up 0.75%, ChiNext up 1.90%.

ASIA EQUITIES: Asia Equities Mostly Lower, Higher PMIs Help Some Markets

Asia equities are mostly lower today, largely on the back of the FOMC rate decision and Powell's comments around not cutting in March. While regional PMI prints have mostly been to the upside for Jan, helping some local markets.

- Japan equity indices are lower across the board today, the biggest news coming out is from Aozora Bank, as their shares plunged 21.5% on the back of losses in their US commercial property exposure, this coming on the back of NY Community Bancorp slashing it's dividend and stockpile reserves, due to bad loan exposure to US property, causing the stock to fall 38%. Currently the Topix is 0.75% lower, while the Nikkei trades 0.90% lower

- South Korea equities indices are higher today as PMI data showed a return to growth 51.2 up from 49.9 in Dec, while headlines out earlier from the Finance Minister around resolving the "Korea Discount" in stock markets are helping push the Kospi higher, currently up 1.50%

- Taiwan PMI out earlier improved from last month at 48.8 vs 47.1, the Taiex is currently trading flat.

- Australia equities have ended their winning run by giving all gains from yesterday back, after Powell dampened hope of a US rate cut in march, the ASX200 is trading lower by 1.20%, elsewhere in Aus the 3Y hit 3.50% for the first time since June, while a rate cut is fully priced in for June.

- Elsewhere in SEA, PMI data has been released showing Indonesia the standout in the region coming in at 52.9 vs 52.2, equities higher by 0.70%, elsewhere Thailand's PMI data improved from last month, but still showing signs production is contracting 46.7 vs 45.1, equities lower by 0.40%, while Philippines PMI fell to 50.9 vs 51.50 last month with equities lower by 0.65%

OIL: Crude Up Moderately Following Wednesday’s Sharp Fall

Oil prices are off Wednesday’s lows during APAC trading today. Continued geopolitical uncertainties with better risk sentiment have supported crude. WTI is up 0.7% to $76.38/bbl but off the intraday high of $76.50 and Brent is 0.7% higher at $81.08 after reaching a high of $81.20. A slightly lower US dollar has also provided some support.

- The US said that is shot down Iranian drones and a Houthi missile in the Gulf of Aden off Yemen’s coast. Threats to shipping in the area are yet to abate. Also, an expected US response to the killing of 3 soldiers is keeping markets alert. Iran has denied supplying the weapons and has warned against retaliating.

- Total US production rose 5.7% in the latest week, rebounding from weather-impacted closures. But strong US output over recent months has been one of the factors keeping a lid on oil prices.

- Bloomberg is reporting that the problems in the Red Sea are pushing European diesel prices higher due to the longer routes to avoid the area. Europe has found other sources of refined products since it banned Russian diesel following its invasion of Ukraine.

- Later there is US Q4 productivity/ULC, jobless claims, January manufacturing PMI/ISM as well as European PMIs and euro area January CPI. The Bank of England meets and is expected to leave rates unchanged. ECB’s Lagarde and Lane make appearances.

GOLD: Slightly Stronger But Still Below Yesterday’s ADP Employment-Induced High

Gold is slightly higher in the Asia-Pac session, after closing 0.1% higher at $2039.52 on Wednesday following the FOMC Policy Decision.

- The bullion market experienced considerable volatility during the session, marked by a peak of $2055.92. This surge in gold occurred as the USD dollar weakened and US Treasury yields declined due to disappointing US economic data. ADP Employment showed a change of 107k vs. 135k est (prior down revised to 158k from 164k), ahead of Friday’s Non-Farm Payrolls for January.

- However, later in the session, there was an intraday resurgence in the USD and yields as Fed Chair Powell expressed reservations about the possibility of a Fed rate cut in March.

- The market is now assigns around a 35% chance to a 25bp rate cut in March. This compares to the near 70% chance seen a couple of weeks ago.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 01/02/2024 | 0815/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 01/02/2024 | 0830/0930 | *** |  | SE | Riksbank Interest Rate Decison |

| 01/02/2024 | 0845/0945 | ** |  | IT | S&P Global Manufacturing PMI (f) |

| 01/02/2024 | 0850/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 01/02/2024 | 0855/0955 | ** |  | DE | IHS Markit Manufacturing PMI (f) |

| 01/02/2024 | 0900/1000 | ** |  | EU | IHS Markit Manufacturing PMI (f) |

| 01/02/2024 | 0930/0930 | ** |  | UK | S&P Global Manufacturing PMI (Final) |

| 01/02/2024 | 1000/1100 | *** | | EU | HICP (p) |

| 01/02/2024 | 1000/1100 | ** | | EU | Unemployment |

| 01/02/2024 | 1000/1100 | *** | | IT | HICP (p) |

| 01/02/2024 | 1130/1230 | | EU | ECB's Lane remarks at EIEF | |

| 01/02/2024 | 1200/1200 | *** | | UK | Bank Of England Interest Rate |

| 01/02/2024 | 1200/1200 | *** | | UK | Bank Of England Interest Rate |

| 01/02/2024 | 1230/1230 | | UK | BoE Press Conference | |

| 01/02/2024 | - | *** |  | US | Domestic-Made Vehicle Sales |

| 01/02/2024 | 1330/0830 | *** | | US | Jobless Claims |

| 01/02/2024 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 01/02/2024 | 1330/0830 | ** | | US | Preliminary Non-Farm Productivity |

| 01/02/2024 | 1400/1400 | | UK | DMP Data | |

| 01/02/2024 | 1445/0945 | *** | | US | IHS Markit Manufacturing Index (final) |

| 01/02/2024 | 1500/1000 | *** | | US | ISM Manufacturing Index |

| 01/02/2024 | 1500/1000 | * | | US | Construction Spending |

| 01/02/2024 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 01/02/2024 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 01/02/2024 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 01/02/2024 | 1630/1130 |  | CA | BOC Governor Macklem testifies at House finance committee. |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.