Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI Eurozone Inflation Insight - January 2024

MNI Eurozone Inflation Insight - January 2024

EXECUTIVE SUMMARY

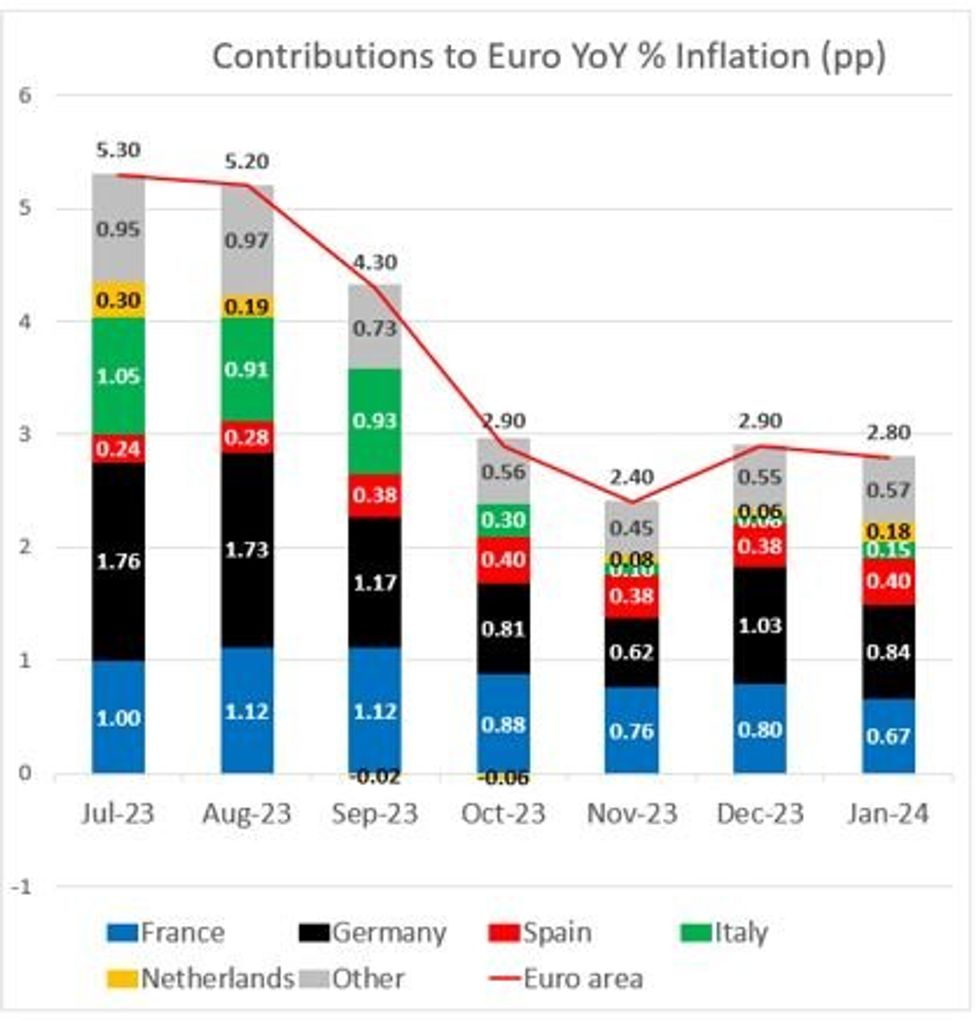

Core Goods Disinflate Further, But Services Progress Stalls

Eurozone flash January HICP decelerated as expected versus December’s largely base-induced uptick, but printed slightly above the 2.7% Y/Y consensus at an unrounded 2.752% (vs 2.929% prior). Core inflation was an unrounded 3.275% Y/Y (vs 3.426% prior) – slightly above expectations of 3.2% but the 6th consecutive fall.

- The main core categories mirrored December’s results, with services at 4.0% Y/Y for the 3rd month in a row (and -0.1% M/M NSA) while non-energy industrial goods disinflated further at 2.0% Y/Y (vs 2.5% prior).

- Analysts were slightly surprised by the stickiness in services inflation, though there was some debate as to its significance. Some identified one-off factors including the increase in German restaurant VAT as the reason for sustained strength, but others cautioned that it appears services inflation overall is stabilising at a relatively high rate.

- Medium-term market-implied ECB rate cut expectations ended up slightly reduced over the 3 days of Eurozone inflation releases (Jan 30, Jan 31, Feb 1), with markets currently expecting 140bps of cuts through 2024 versus 145bp at the close on Jan 29.

- Our review of January's preliminary Eurozone inflation data includes breakdowns and analysis of the national inflation prints, and some sell-side reactions.

FOR FULL PDF ANALYSIS:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok