Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

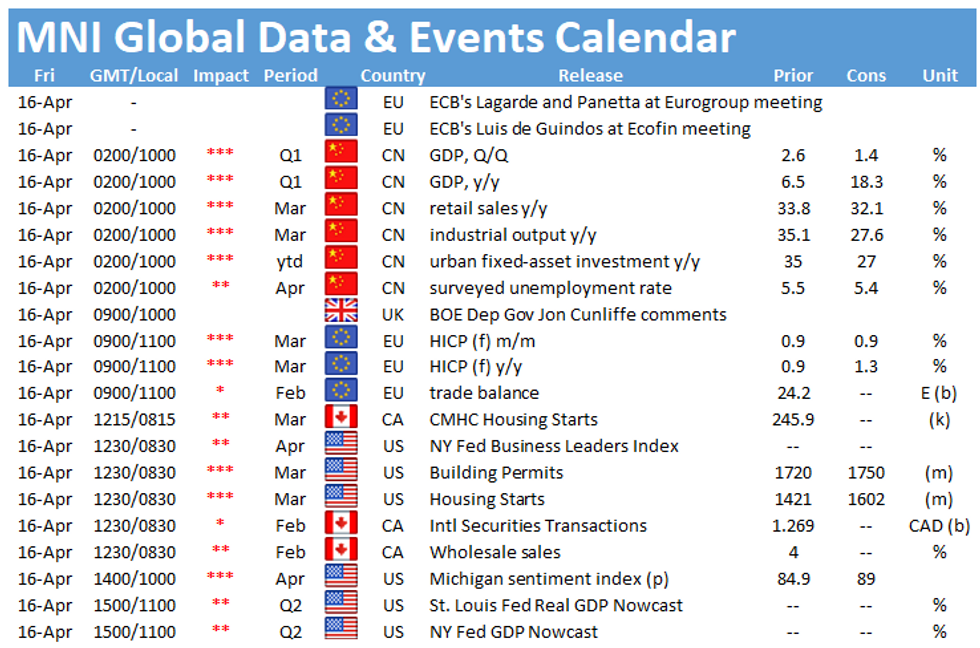

Friday sees a quiet schedule in terms of data releases with Europe's highlights including EZ final inflation and the EZ trade balance, both released at 1000BST. In the US, the main data event is the release of the preliminary Michigan sentiment index at 1500BST.

EZ final inflation seen at flash estimate

Final EZ inflation is forecast to register in line with the flash results showing an uptick to 1.3% for the annual CPI. This marks the third consecutive positive reading and the highest level since January 2020 (+1.4%). March's increase was mainly driven by a sharp rebound of energy inflation, up 4.3% after falling by 1.7%, which is unsurprising given the steep decline of oil prices a year earlier. Headline inflation is likely to increase in the coming months due to fluctuations in oil prices in 2020. The ECB sees inflation gradually rising over the medium-term once the impact of the pandemic fades.

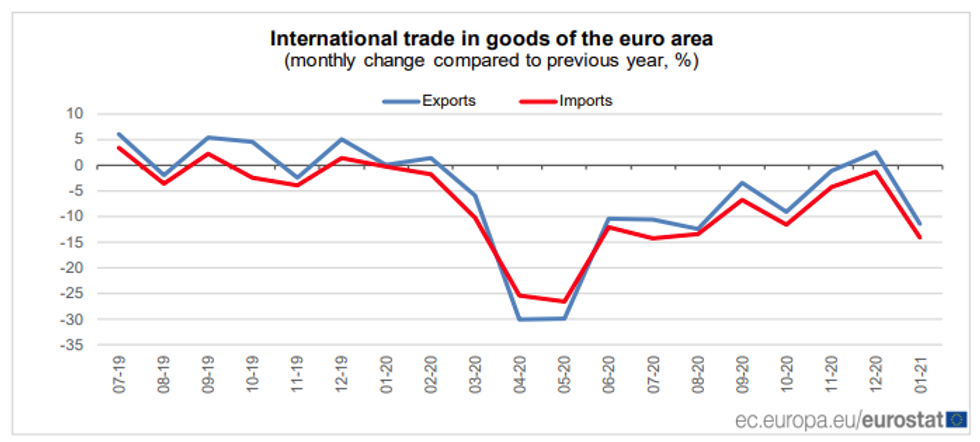

EZ trade surplus forecast to shrink

The EZ trade surplus is expected to narrow to EUR 22.0bn in February, after declining to EUR 24.2bn in the previous month. This would mark the lowest reading since August and the second consecutive decrease. January saw monthly exports drop by 2.8%, while imports fell by 1.3%. On an annual basis, exports were down 11.4% and imports fell by 14.1%.

Survey evidence including the composite PMI suggest an increase in new export business in the eurozone, however this rise is driven by the manufacturing sector. Already available state level data showed an increase of both German exports and imports, whereby imports rose by more than exports, leading to a smaller trade surplus. Meanwhile, the French trade deficit widened in February, with exports falling by more than imports.

Michigan consumer sentiment expected to rise

Markets look for the preliminary Michigan sentiment index to rise further in April to 89.0, up from 84.9 seen in March. The index increased to the highest level in a year due to the new round of relief checks and better than expected progress of the vaccination program. The successful vaccination progress is likely to fuel consumer confidence further in the coming months. Moreover, the labour market is gaining momentum. The latest payroll data showed an increase in jobs growth in March. Moreover, the unemployment rate eased further to 6.0%, which is the lowest level in a year.

The main events to look out for include speeches by BOE's Jon Cunliffe and Dallas Fed's Rob Kaplan.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.