Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

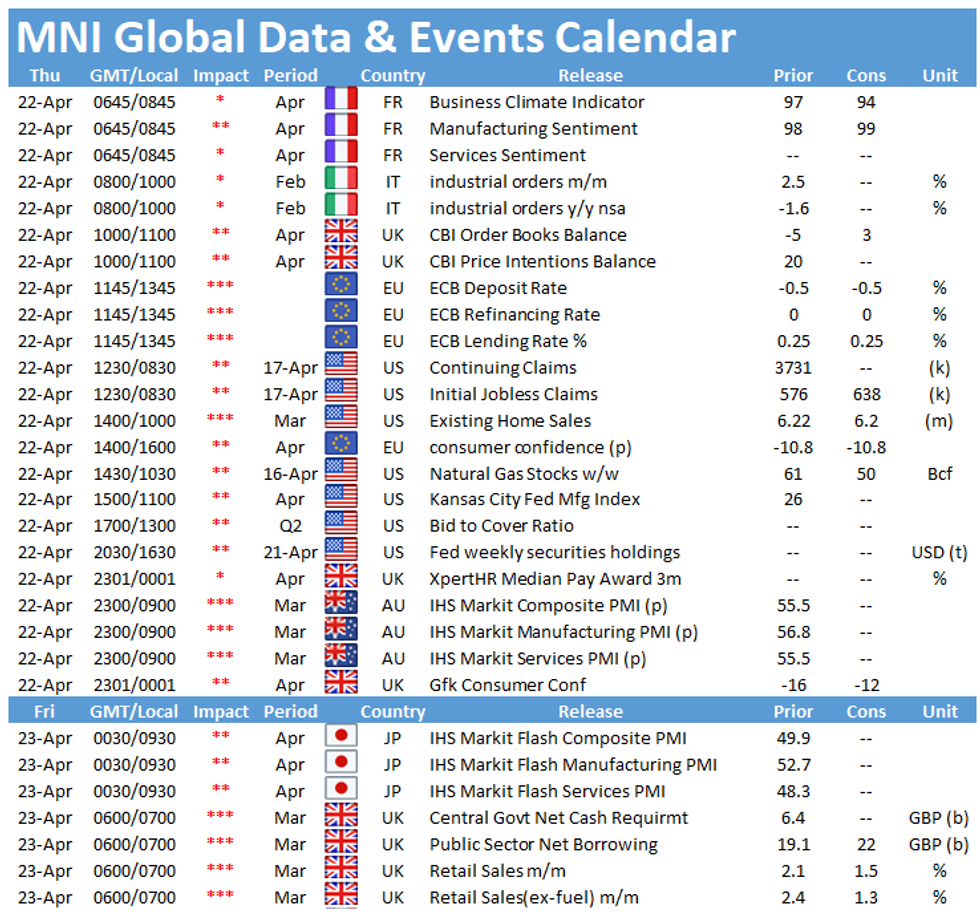

The main data events in Europe on Thursday include the publication of the French business climate indicator at 0715BST and the EZ flash consumer confidence at 1500BST. The ECB's policy rate decision will be be the main item of the day at 1245BST. In the US, the release of initial jobless claims is the highlight of the day at 1330BST.

French business climate expected to decline

The French business climate indicator is forecast to fall to 94 in April, as restrictions got tightened due to a rise in infection rates. The index gained 7pt in March and rose to 97, showing the highest level since start of the crisis. However, Insee noted that the majority of responses were collected before the announcement of tighter restrictions.

Especially the service and retail trade sector saw a sharp uptick in sentiment in March. Confidence in these sectors is still dependent on the development of the pandemic, hence both indices are likely to ease in April. Business climate in the manufacturing sector remained unchanged in March at 98, which is just slightly below the long-term average (100). In April markets are looking for a small 1-point uptick to 99, which would be the highest level since February 2020.

ECB's policy setting seen unchanged

The European Central Bank's Governing Council meets Thursday and although no changed are expected in the key policy setting, the commentary from the post-meet press conference will be closely watched.

Much attention will be on how President Christine Lagarde deals with questions on how the ECB judges current 'financing conditions' and whether they further expand on how they judge conditions. Attention will also focus on how Lagarde deals with the questions regarding the 'significant' increase in bond buys since the last meeting. which many have judged as anything but.

EZ consumer confidence forecast to remain unchanged

Consumer confidence is expected to remain unchanged in April at March's level of -10.8. Consumer sentiment improved in March, showing the second consecutive gain and the highest level since February 2020. March's survey noted that consumers assess the future economic conditions and their own future financial situation better, while their opinion regarding the past financial situation did not recover yet from the covid-induced slide. This pattern is likely to persist in April. On the one hand, the vaccination program fuels hope for an easing of restrictions in the near-term, but infection rates remain high and the progress of vaccinations is slow.

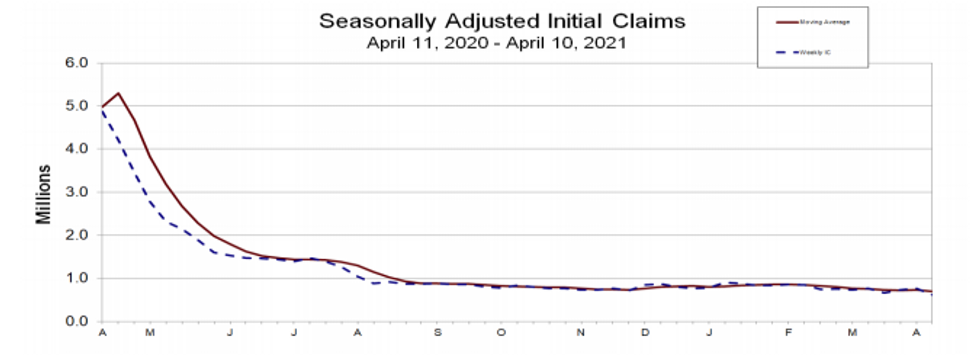

US jobless claims expected to tick up

U.S. jobless claims filed through April 17 are set to have risen to 638,000 from 576,000 through April 10, according to the Bloomberg consensus. Continuing claims filed through April 10 are expected to fall to 3.64 million from 3.731 million through April 3.

The latest payroll report showed an improvement of the labour market with employment increasing, wile the unemployment rate declined. Moreover, survey evidence suggests a continued improvement. The preliminary Michigan sentiment index reported strong job gains due to the record stimulus spending and half of the respondents expect the jobless rate to decline.

Source: U.S. Department of Labor

There are no speeches scheduled on Thursday besides the press conference following the ECB's interest rate decision.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.