Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (Washington)

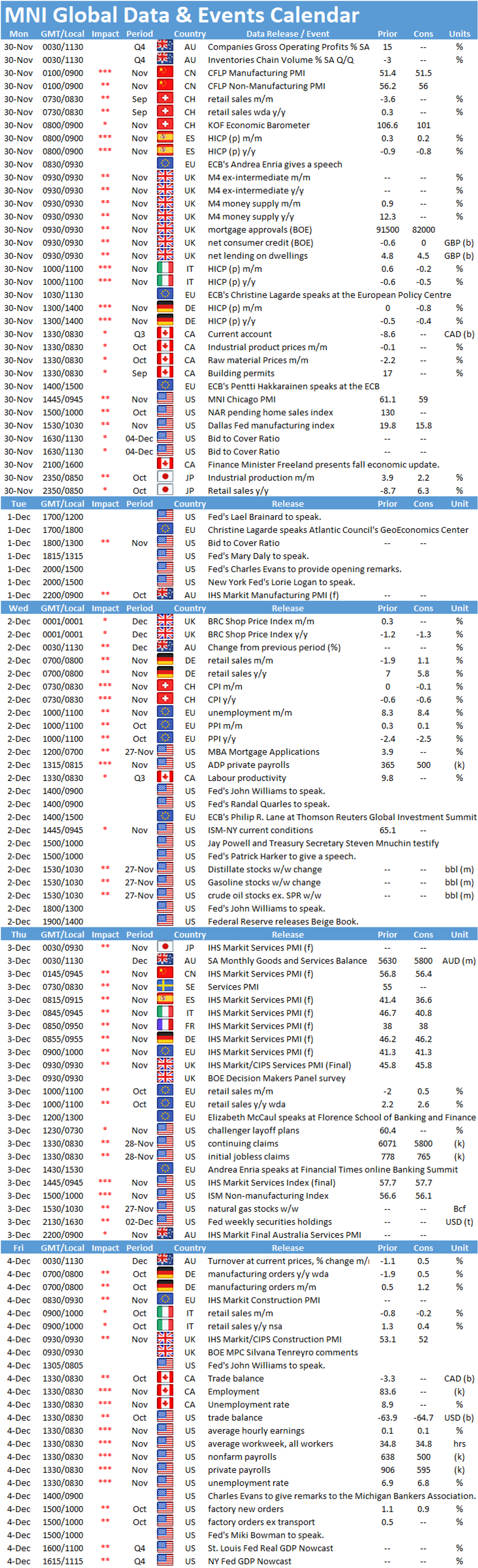

Key Things to Watch:

- Monday, November 30 – German and Italian Inflation

- Italy's flash inflation is expected to tick up to -0.5% in November after -0.6% in the previous month. The national print came in at -0.3% in October, up from -0.6% seen in September. The difference between the HICP and the CPI mainly stems from effects of the end of summer sales which are not taken into account by the CPI. The flash composite PMI for the Eurozone noted a decline in service prices due to discounting which is in line with the negative inflation reading for Italy in November.

- In November, markets are looking for annual German inflation to register in line with the October reading, when it recorded a third successive negative reading, declining by 0.5% after falling 0.4% in September. Prices are being pulled down by the temporary VAT reduction introduced in July and by lower energy costs. Excluding energy, HICP increased 0.6% in October. The flash composite PMI for Germany showed an increase in prices charged for goods and services in November, suggesting an upward risk for inflation.

- Thursday, December 3 – U.S. Weekly Jobless Claims

- Initial jobless claims filed through November 28 should dip to 765,000 after climbing to 778,000 in the week ending November 21.

- Claims for benefits under the Pandemic Unemployment Assistance (PUA) and Pandemic Emergency Unemployment Compensation (PEUC) continue to rise. Analysts say this indicates many job losses have become longer in duration and unemployed workers are exhausting regular state benefits.

- Friday, December 4 – U.S. Nonfarm Payrolls

- The U.S. economy likely added 500,000 jobs in November, according to Bloomberg, a sign that payrolls growth is continuing to slow from the outsized gains of the springtime and summer.

- Surging Covid-19 infections across the country and renewed shutdowns of bars and restaurants in late October and early November should put downward pressure on service-sector job growth.

MNI Washington Bureau | +1 202-371-2121 | brooke.migdon@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok