Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

south africa

Executive Summary:

- Key Rate expected to remain unchanged at 3.5% (chance of split MPC vote).

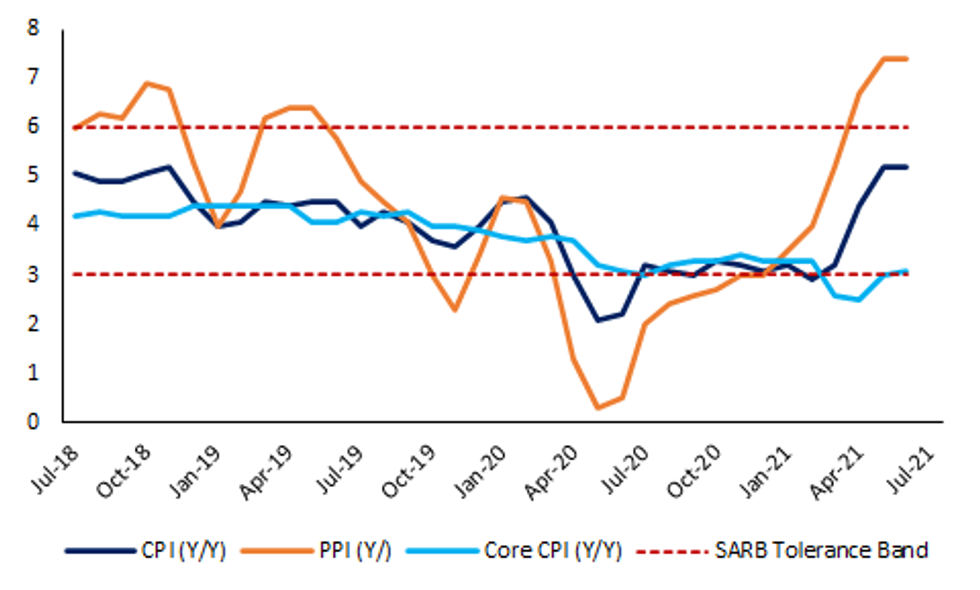

- Although headline CPI (5.2%) & PPI (7.4%) moved close to or above the SARB's upper tolerance band in May, Core CPI remained persistently low (3.1%).

- While Kganyago may pay lip service to unrest-induced supply-side risks, he has consistently reiterated his willingness to keep policy accommodative by looking through near-term transitory factors to focus on the medium-term disinflationary trajectory.

- Although the SARB's end-2021 CPI forecast may rise to ~4.6% y/y and 2022/23 to 4.7% & 4.8%, pricing behaviour remains relatively balanced over the medium-term.

- Risks from recent socio-political unrest may see SARB guidance err on the neutral/dovish side to avoid damaging the domestic economic recovery and spooking markets amid fragile investor sentiment.

- High unemployment and the muted aggregate demand impulse should also temper hawkish impetus from the SARB, keeping our base case scenario of rates unchanged to 1Q22 intact in the absence of further upside surprises in CPI.

Full Preview Here:

The SARB is expected to keep its key rate on hold at 3.5% this week, with inflation still relatively well contained within the bank's 3-6% range. While supply-side risks from socio-economic unrest may have sparked concerns of expedited policy normalisation, we expect Governor Kganyago to retain his focus on medium-term disinflationary factors and await further confirmation in the data before denting SA's recovery potential by reactively hiking policy rates.

MNI London Bureau | +44 020-3983-7894 | murray.nichol@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok