Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

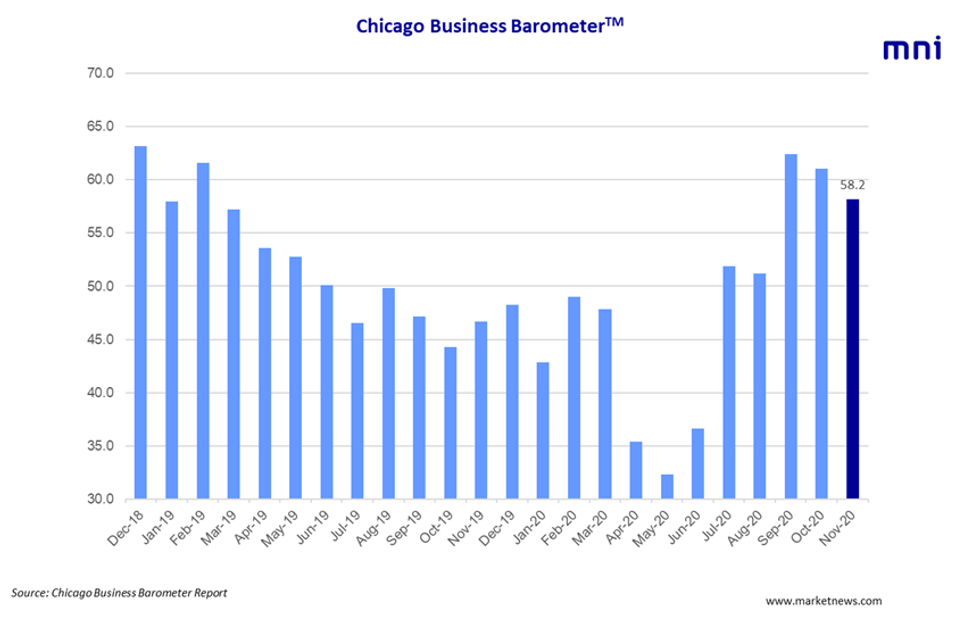

The Chicago Business Barometer declined again in November, falling short of market expectations looking for a softer decline. The headline index slipped to 58.2 and now stands at the lowest level since August although it remains in expansion.

Among the main five indicators, New Orders and Production posted the only declines, while Supplier Deliveries saw the largest gain.

Demand cooled in November with New Orders dropping by 5.0 points to 60.0, its lowest level since August. New Orders fell for the first time since May. Production dipped to 60.8, down from October's 62.1. Some companies reported an uptick in demand, although order levels remain below pre-crisis levels. Others noted stagnant demand and adjusted production due to Covid-19.

The Backlog of work edged up marginally by 0.9 points to 51.4 in November, marking a third consecutive reading above the 50-mark. Meanwhile, Inventories eased further in November, slipping 2.0 points to 45.7, hitting a three-month low.

EMPLOYMENT

The demand for labour edged up 0.8 points to 44.0 following October's drop to 43.2. Nevertheless, employment remains in contraction since July 2019.

Supplier Deliveries jumped to 70.3 in November, up from 65.3 recorded in October. The index rose to the highest level since May as firms saw delivery delays. Prices at the factory gate surged 9.8 points to 74.4 in November, hitting the highest level in over two years.

This month's special question asked how employee productivity had been during the crisis period. The majority, at 55.4%, reported no change in productivity during the current crisis, while 32.1% saw productivity gain between 1-10%. The second special question asked: "Does the outcome of the general election have any effect on your forecast?" The majority, at 73.2%, noted that the election results do not influence their forecasts. On the other hand, 12.5% see forecasts increase, while 14.3% reported a decrease.

This month's survey ran from November 2 to 16.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.