Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Markets retain post-payrolls bid as copper, equities hit new cycle highs

- Sterling surges as next phase of reopening looks to be confirmed

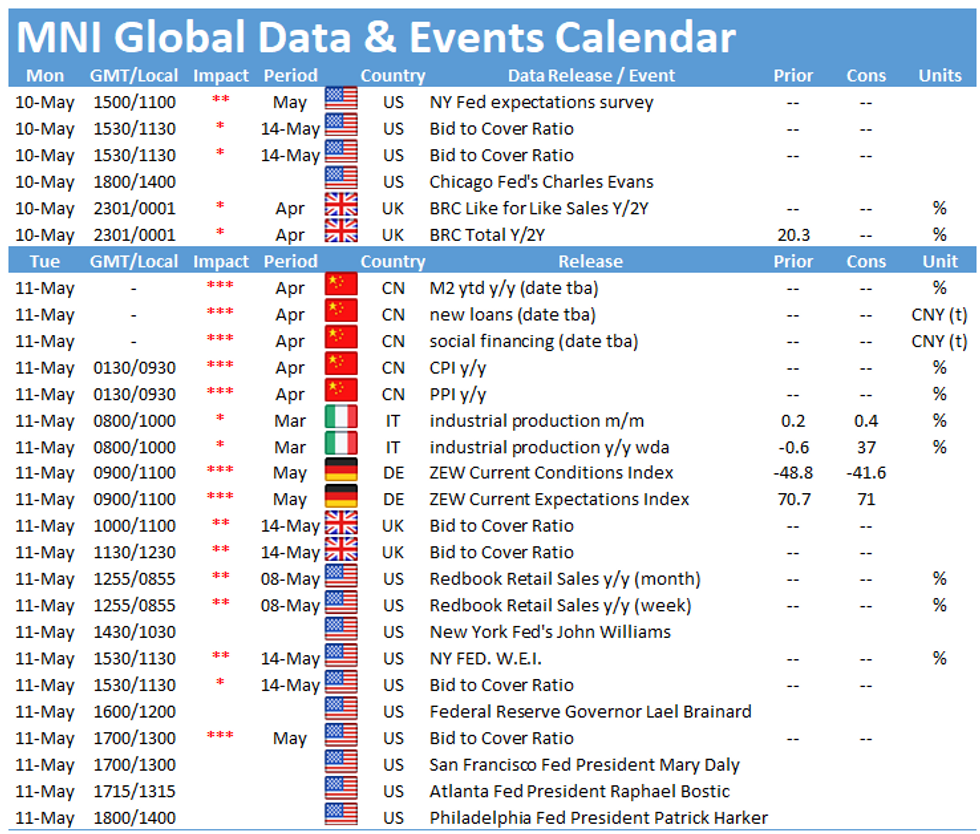

- No data due, but markets await comments from Fed's Evans

US TSYS SUMMARY: Steepening Continues Post-Payrolls

Tsys have bounced in European morning trade Monday, following modest losses in the Asia-Pac session. The reversal kept Friday's lows in TY1 intact.

- While Tsy futures have largely roundtripped since pre-payrolls, notably, steepening remains intact and has in fact resumed early Monday (e.g. 5s30s up ~9bps since the data). The 2-Yr yield is down 0.4bps at 0.1409%, 5-Yr is down 0.7bps at 0.7676%, 10-Yr is up 0.4bps at 1.5807%, and 30-Yr is up 1.2bps at 2.2885%.

- Jun 10-Yr futures (TY) up 0.5/32 at 132-24.5 (L: 132-18.5 / H: 132-25.5)

- Little newsflow overnight, with attention on soaring metals prices (iron ore +10%, copper new all-time highs) and a cyberattack knocking out the US's largest oil products pipeline.

- Chicago Fed's Evans is the lone scheduled Fed speaker today, appearing at 1400ET. Over the weekend, Minn Pres Kashkari noted that Friday's payrolls showed the domestic labor market remains in a "deep hole".

- Pres Biden delivers remarks on the economy at 1315ET.

- No data today, and only supply is $111B of 13-/26-week bill auction at 1130ET. NY Fed buys ~$3.625B of Tsy 7Y-20Y.

EGB/GILT SUMMARY - Perceived Reduction In Scottish Referendum Risk Boosts GB Sentiment

It has been a mixed start to the week with gilts selling off and EGBs initially trading weaker before reclaiming early losses.

- The failure of the SNP to secure a parliamentary majority in the Scottish elections has been perceived as lowering the probability of a fresh independence referendum, and in turn has underpinned the gilt sell off and cable rally.

- Gilt yields are 1-2bp higher on the day with the curve bear steepening.

- Bunds opened weaker but have gradually paired losses to trade flat on the day.

- OATs have followed a similar course while trading above the Friday close.

- BTPs have firmed with yields 1bp lower.

- Supply this morning came from Germany (Bubills, EUR3.901bn allotted) and Finland (RFTBs, EUR1.962bn)

EUROPE OPTION FLOW SUMMARY

Eurozone:

OEM1 134.5/134.25/134.00p fly, bought for 2.5 in 1k

US:

TYN1 133c, sold at 19 in 5k

FOREX: All about the Pound

FX have mostly stayed range bound, but most of the action has been in GBP.

- Better buying continuation in GBP as Europe. joined the session.

- Overnight desk reported shorts bailing as we broke through the important 1.4000.

- Similar price action during the EU session with Cable making an attempt at 1.4100 (printed 1.4097 high).

- Contributing factors, UK politics saw the Tories make further inroads into traditional Labour strongholds.

- SNP failed by just 1 seat to get an outright majority. BUT, the party is expected to team up with pro-independence Greens to launch another bid for a referendum, but unlikely to be anytime soon.

- Boris also confirmed that the next stage of re-opening will go as planned on the 17th, and he will hold a presser later today.

- The Pound is bid across the board and versus all majors.

- While a more mixed session for the USD, as noted down 0.75% against GBP, but trade marginally in positive territory vs JPY, SEK and EUR.

- Looking at the rest of the day, US fed Evans Voter, leaning Dove), will be discussing Economic outlook at a virtual event.

FX OPTIONS: Expiries for May10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2000(E685mln), $1.2040(E683mln)

- USD/JPY: Y109.00-05($587mln), Y110.00($740mln)

- GBP/USD: $1.3800(Gbp678mln)

- EUR/GBP: Gbp0.8760-80(E670mln)

- AUD/USD: $0.7900(A$639mln)

Price Signal Summary - USD Remains Soft

- In the equity space, S&P E-minis have traded to fresh cycle highs and maintain a clear bullish tine. The focus is on 4239.26, 1.764 projection of the Feb 1 - Feb 16 - Mar 4 price swing and the 4300.00 handle. EUROSTOXX 50 futures have cleared the psychological hurdle of 4000.00. The trend remains up and the focus is on 4099.00 1.00 projection of the Mar - Jul - Oct 2020 price swing.

- In FX, EURUSD maintains a firmer tone following Friday's gains and the break of 1.2150, Apr 29 high. The focus is on 1.2184, Feb 26 high and 1.2243, Feb 25 high. GBPUSD is firm today and extending Friday's rally. A number of immediate resistance levels have been cleared. The focus is on 1.4103, 76.4% retracement of the Feb 24 - Apr 12 downleg. USDJPY short-term support has been defined at Friday's low of 108.34. A bullish theme remains intact while this level holds and attention is on 109.70, May 3 high. A break of support would highlight a move below the trendline drawn off the Jan 6 low and risk a deeper pullback.

- On the commodity front, the Gold outlook is bullish and the uptrend has resumed. This has opened $1851.5, 61.8% retracement of the Jan 6 - Mar 8 sell-off. Oil is off recent highs but the uptrend remains intact. The {7I} Brent (N1) focus is on the psychological $70.00 level and $71.75, Jan 8 2020 high (cont). WTI bulls are eyeing the key resistance at $67.29, Mar 8 high.

- In the FI space, Bunds (M1) have recently breached 170.05, 76.4% of the Feb 25 - Mar 25 rally. This opens 169.24, Feb 25 low and the bear trigger. Near-term risk in Gilts is still skewed to the downside. The next support and intraday bear trigger is at 127.32, Apr 1 low.

EQUITIES: Natural Resources Stocks Lead Gains

- Asian stocks closed higher, with Japan's NIKKEI up 160.52 pts or +0.55% at 29518.34 and the TOPIX up 19.22 pts or +0.99% at 1952.27. China's SHANGHAI closed up 9.117 pts or +0.27% at 3427.991 and the HANG SENG ended 14.99 pts lower or -0.05% at 28595.66.

- European equities are mixed, with the German Dax down 36.46 pts or -0.24% at 15393.67, FTSE 100 up 12.11 pts or +0.17% at 7136.32, CAC 40 down 7.78 pts or -0.12% at 6372.73 and Euro Stoxx 50 down 15.88 pts or -0.39% at 4025.84.

- U.S. futures are mixed too, with the Dow Jones mini up 66 pts or +0.19% at 34752, S&P 500 mini down 0.75 pts or -0.02% at 4224.5, NASDAQ mini down 51 pts or -0.37% at 13658.75.

COMMODITIES: Industrial Metals Rally Continues

- WTI Crude up $0.52 or +0.8% at $65.35

- Natural Gas down $0.02 or -0.68% at $2.936

- Gold spot up $5.08 or +0.28% at $1834.71

- Copper up $11.3 or +2.38% at $486.35

- Silver up $0.24 or +0.88% at $27.6643

- Platinum up $9.76 or +0.78% at $1261.32

MNI London Bureau | +44 203-865-3809 | edward.hardy@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok