Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

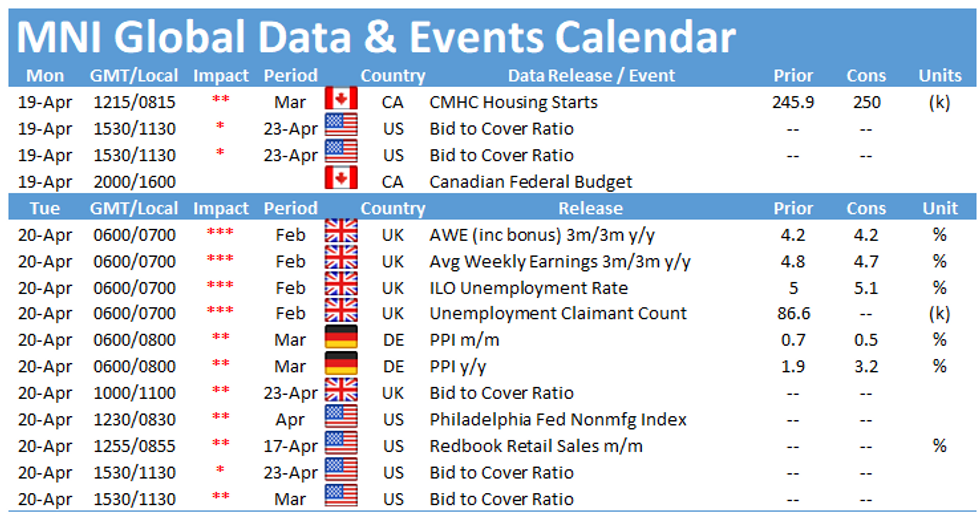

HIGHLIGHTS:

- USD dives as EUR/USD rips to new six-week highs

- Stocks hover below last week's record highs

- Data, speaker schedule quiet as FOMC enter media blackout

US TSYS SUMMARY: Underlying Risk Factors Remain

US FI markets moderately firmer at the moment, Tsys scaling back from late overnight highs to near middle of range (10YY 1.5711% last vs.1.5500%), equities moving lower as well (ESM1 -11.0). Modest volumes: TYM under 290k at the moment.

- Modest unwind does not appear headline driven at the moment as underlying global risk factors continue: US/Russia tensions tied to Ukraine border troop build not to mention calls for mass protests over Kremlin opposition leader Navalny's health while incarcerated, J&J vaccine news.

- Very quiet start to week for scheduled data after Fed entered media blackout regarding monetary policy through Apr-29, no significant data Mon-Tue. Bill auctions ($57B 13W, $54B 26W) and NY Fed Buy-back (Tsy 2.25Y-4.5Y, appr $8.825B) on tap.

- Rate-locks in the mix ahead continued corporate supply as banks continue to exit latest earnings cycle, Citi expected this week.

- The 2-Yr yield is down 0.4bps at 0.1572%, 5-Yr is down 0.8bps at 0.8227%, 10-Yr is down 0.9bps at 1.5711%, and 30-Yr is down 0.9bps at 2.2558%.

EGB/GILT SUMMARY: Giving Up Early Gains

European sovereign bonds started the week a strong footing with EGBs subsequently selling off towards midday.

- Gilts yields are broadly 1bp lower with the curve marginally flatter on the day.

- Bunds had opened stronger but sold off from around 1130GMT following a headline that the CDU chairman will speak about the chancellor candidacy at 1300 today.

- OATs have followed bunds lower and now trade close to unch on the day.

- BTPs similarly trade close to flat.

- Supply this morning came from Germany (Bubills, EUR4.92bn allotted), Netherlands (DTCs, EUR2.95bn) and Slovakia (SLOVGBs, EUR458.4mn).

- UK PM Boris Johnson decided to cancel a planned trip to India as a result of surging Covid infections in that country.

- Focus this week will be on the ECB meeting on Thursday. No material change in monetary policy is expected, but communication around the weekly PEPP purchases will be closely monitored.

EUROPE ISSUANCE UPDATE: New EU Mandate

EUROZONE ISSUANCE:

EU EUR Benchmark 15yr

size of EUR 4.75 billion (no-grow)

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXM1 170/169ps, bought for 25 in 4k

0RM1 100.50p, bought for 1.75 in 2.25k

3RZ1 100.12/100ps vs 100.37/100.50cs, bought the ps for 1 in 3k

UK:

LZ1 99.87/100/100.12c fly, bought for 3.25 in 4k

0LM1 99.62p, bought for 0.75 in 2k0LZ1 99.62^, bought for 22.5 in 1k

FOREX: Dollar Starts Week Poorly, EUR/USD Highest Since Early March

- The greenback underwent a short, sharp bout of selling pressure in early European hours, with EUR/USD rallying through key resistance at 1.1990 to hit the highest levels since early March and sit comfortably back above 1.20.

- There was no major headline or flow catalyst behind the greenback weakness, with a pick-up in volumes after light overnight trade likely the underlying driver. EUR buoyancy was also helped by Pfizer announcing the shipment of a further 100mln vaccine doses to the European Union in 2021, bringing the total shipment to 600mln.

- USD is the weakest, alongside CAD, while JPY, CHF and NOK are the firmest in G10.

- Tier one data is few and far between Monday, with focus on risk events later in the week - most notably the ECB rate decision on Thursday. There are no central bank speakers of note after the Fed entered their pre-decision media blackout period over the weekend.

FX OPTIONS: Expiries for Apr19 NY cut 1000ET (Source DTCC)

- USD/JPY: Y108.50($565mln-USD puts), Y108.60-64($1.2bln-USD puts), Y110.00($1.2bln)

- EUR/GBP: Gbp0.8700-10(E519mln-EUR puts)

- AUD/USD: $0.7620-40(A$705mln), $0.7720-30(A$871mln)

- USD/CAD: C$1.2485-90($735mln-USD puts), C$1.2500-10($625mln-USD puts), C$1.2615-25($600mln-USD puts), C$1.2715-25($1.1bln)

Price Signal Summary - USD Retreats

- In the equity space, bullish conditions continue to prevail. S&P E-minis are trading closer to recent highs and the focus is on 4195.50 next, 1.618 projection of the Feb 1 - Feb 16 - Mar 4 price swing.

- In the FX world, EURUSD has rallied this morning and importantly cleared 1.1990, Mar 11 high. This reinforces current bullish conditions and opens 1.2037 next, 61.8% of the Feb 25 - Mar 31 sell-off. GBPUSD is firmer too. Key resistance is at 1.3919, Apr 6 high where a break is required to signal scope for a stronger rally. EURGBP has found resistance at 0.8719, Friday's high. The support to watch is 0.8582, Apr 7 low. USDJPY has traded through 108.41, Mar 23 low and is pressuring the 50-day EMA. A break of the average would open 107.50, trendline support drawn off the Jan 6 low

- On the commodity front, Gold is firmer. The focus is on $1805.7, Feb 25 high. Brent (M1) remains firm. Scope if for a climb towards $69.50 - High Mar 15. WTI (K1) is firmer too with potential for gains towards $64.88, Mar 18 high.

- In the FI space, key support to watch in Bunds (M1) remains 170.52, Mar 18 low. A break would signal scope for an extension lower and open 170.05, 76.4% of the Feb 25 - Mar 25 rally. Support to watch in Gilts (M1) is 127.81, Apr 14 low. Initial firm resistance is 128.93, Mar 25 high.

EQUITIES: Mixed Picture, Spanish Stocks Outperform While German Stocks Retreat

- European equity markets are inconsistent early Monday, with Spanish and French indices outperforming while German, Italian stocks sit in minor negative territory.

- Across Europe's Stoxx 600, health care and real estate names are in the green, highlighting a somewhat defensive theme, while energy and consumer staples are in retreat.

- The moves follow a wholly positive Wall Street close on Friday, although US futures are rolling off recent highs early Monday, with the e-mini S&P inching off Friday's record high of 4,183.50.

- Earnings season rolls on this week, highlights include:

- MON: IBM, Coca-Cola

- TUES: Abbott Labs, J&J, Netflix, P&G

- WEDS: Verizon

- THURS: Intel, AT&T

- FRI: AmEx, Honeywell

- Full schedule with timings, EPS & Rev expectations here: https://roar-assets-auto.rbl.ms/documents/9570/MNI...

COMMODITIES: WTI, Brent Trade Heavy Despite Dollar Pullback

- Oil markets are soft, with both WTI and Brent crude futures sitting lower by 0.2-0.3% ahead of NY hours. The moves come despite greenback weakness in currency markets, underpinning the underlying weakness in commodities.

- That said, WTI and Brent crude sit inside last week's range, oscillating either side of the $63/bbl mark.

- Greenback weakness is, however, helping buoy precious metals to keep both spot gold and silver higher by 0.5% apiece in early Monday trade. Spot gold eyes the 100-dma at $1804.08 for direction, a level not topped since early January.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.