Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Treasury yields rebounding alongside equities

- Recovery trade most evident in energy, financials

- USD Index lower for first session in five

US TSYS SUMMARY: Yield Rebound Continues Ahead Of 20Y Supply

The rebound in Tsy yields from Tuesday's mid-morning lows continues, alongside a rebound in equities.

- Price action (and actionable headlines) proved limited in the Asia-Pac session, with weakness concentrated in about 2 hours of early London trade as stocks picked up the pace.

- Curve is bear steepening: the 2-Yr yield is up 0.2bps at 0.2017%, 5-Yr is up 1bps at 0.6945%, 10-Yr is up 1.8bps at 1.24%, and 30-Yr is up 3.2bps at 1.9087%.

- Sep 10-Yr futures (TY) down 6.5/32 at 134-15 (L: 134-10.5 / H: 134-26.5). Good volumes once again: ~485k traded (as of 0630ET).

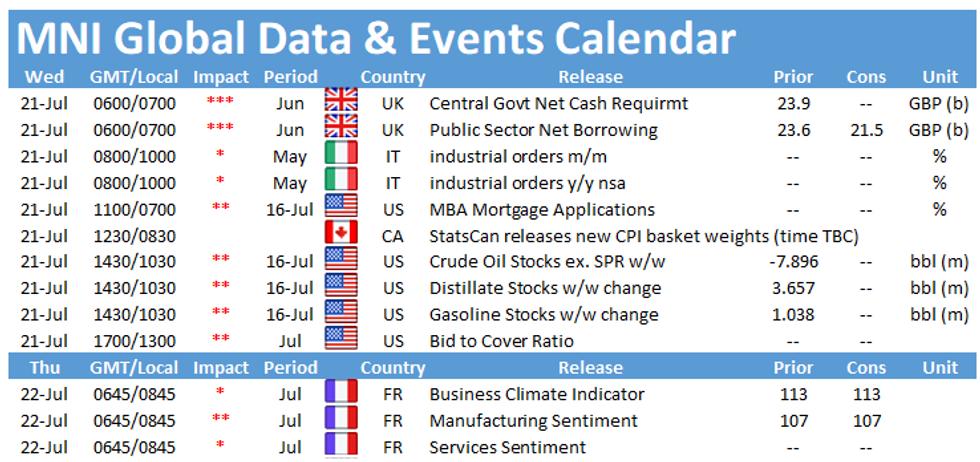

- Supply in focus with $24B 20Y Bond re-open at 1300ET (also $30B 119-day bills at 1130ET). NY Fed buys ~$8.425B of 2.25-4.5Y Tsys.

- A bare data slate (weekly MBA mortgage apps at 0700ET) and of course no Fed speakers.

- Note, Senate set to take a procedural vote on whether to proceed with debate on bipartisan infra bill at 1430ET - but this is set to fail, with both sides still wrangling over text.

- A couple of overnight D.C. items worth noting: a broad WSJ survey piece noting that Powell's re-appointment as Fed Chair was likely but not certain. Also Senate Min Leader McConnell told Punchbowl News that he thinks no Republicans will be willing to vote to raise the debt limit (so Dems might have to go it alone, perhaps attached to a reconciliation bill).

EGB/GILT SUMMARY: Curve Steepening As Equity Recovery Builds

European government bonds trade a touch weaker this morning while equities gains continue to build following losses earlier in the week

- The gilt curve has steepened on the back of the short end firming and longer end trading weaker. The 2s30s spread is now 2bp wider on the day.

- It is a similar story for bunds where the curve is 2bp steeper.

- OATs are broadly weaker with longer end yields up 1-2bp.

- BTPs trade in line with OATs. The curve is very marginally steeper.

- The FT reports that the UK government will unveil new demands today to remove border checks in Northern Ireland which is likely to pave the way to another significant clash with Brussels.

- Supply this morning came from Germany (Bund, EUR1.23bn allotted) and Portugal (BT, EUR1.00bn).

- There were no tier one data releases this morning.

EUROPE ISSUANCE UPDATE:

Germany allots E1.23bln 1.25% Aug-48 Bund, Avg yield 0.03% (Prev. 0.22%), Bid-to-cover 1.11x (Prev. 1.08x), Buba cover 1.35x (Prev. 1.26x)

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXU1 176.5/178cs sold at 43 down to 41 in 7,318

DUU1 112.20/112.10ps 1x2 bought for average 1.25 in 4

UK:

0LZ1 99.50/99.62cs 1x2, bought for 1 in 2k

FOREX: JPY Hampered by Continued Bounce in Stocks

- Reflecting the continued bounce in equities, JPY is Wednesday's poorest performer so far, with USD/JPY edging comfortably back above the Y110.00 ahead of the NY crossover.

- The surge in the e-mini S&P puts the index through the week's best levels, with the contract now inside 50 points of the alltime highs posted on July 14th. The energy and financials sectors (the poorest performers at the beginning of the week) are driving the recovery in Europe, with US indices likely to follow suit.

- This has put a temporary end to the recent USD strength, with the USD Index in minor negative territory at pixel time. A negative close for the index today would be the first in five sessions. EUR/USD's rejection of any test on key support at 1.1704 is largely responsible, but the pair needs to make progress through the Tuesday high of 1.1803 before the outlook begins to look more positive.

- Once again, there's relatively little data or central bank speak to digest across G10, keeping focus on the ECB rate decision due tomorrow and the continued roll out of US earnings. Highlights today include Johnson & Johnson, Coca-Cola and Verizon Communications.

FX OPTIONS: Expiries for Jul21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700(E1.3bln), $1.1835-50(E1.1bln), $1.1900(E1.1bln)

- USD/JPY: Y110.00-15($947mln), Y110.50($820mln)

- AUD/USD: $0.7400(A$857mln)

Price Signal Summary -S&P E-Minis Find Support At The 50-Day EMA

- In the equity space, conditions have improved for bulls, for now at least. S&P E-minis started the week on a bearish note but found support at Monday's low. The contact has tested the 50-day EMA at 4239.07 and the average has so far also provided support. A key pivot level has been defined at 4224.00, Monday's low. EUROSTOXX 50 futures are extending the recovery from Monday's low of 3895.00, low Jul 19 and marks a pivotal short-term support. Gains are considered corrective, 4039.00 marks initial resistance, the 20-day EMA.

- In FX, the USD outlook remains bullish. EURUSD maintains the bearish sequence of lower lows and lower highs. The focus is on 1.1704, Mar 31 low and key support. GBPUSD took out key support at 1.3669, Apr 12 low as well as the 200-dma at 1.3700. The breach of 1.3669 reinforces bearish conditions and paves the way for an extension of the bear cycle towards 1.3520 next, Jan 18 low. USDJPY is trading above Monday's low but remains vulnerable. This week's low print of 109.07 confirms a resumption of the downtrend paving the way for an extension lower. The focus is on 108.47, 76.4% of the Apr 23 - Jul 2 rally. Resistance is at 110.34, Jul 16 high.

- On the commodity front, Gold maintains a bullish tone and the recent pullback is considered corrective. Price needs to clear last week's high print to confirm a resumption of the recent upleg. Key short-term support is at $1791.7, Jul 12 low. Brent futures gains are considered corrective. The focus is on $67.43, a Fibonacci retracement. Initial resistance is at $70.54, 50.0% of Monday's range. WTI (U1) sights are on $64.60, 76.4% of the May 21 - Jul 6 rally.

- Within FI, Bund futures remain firm following this week's break of 174.77, Jul 8 high. Sights are on 176.30, 76.4% retracement of the Dec '20 - May sell-off (cont). Gilts remain in a bullish condition despite the current pullback. The break of 129.92, Jul 8 high confirms a resumption of the uptrend and opens 130.72 2.236 projection of the May 13 - 26 - Jun 3 price swing.

EQUITIES: Stocks Extend the Bounce, with EuroStoxx50 Testing Friday Close

- Equity markets are firmer for a second session, with European indices uniformly positive. Spain's IBEX-35 is leading with gains of over 2%, but the UK's FTSE-100 and Italy's FTSE-MIB are also sharply higher.

- Energy and financials are the sectors driving the rally across Europe - both of which were the poorest performing sectors earlier in the week. Steepening of government bond yield curves and a stabilisation of the oil price are largely responsible, keeping both these market metrics in focus headed into the NY crossover.

- US futures are firm and indicate a positive open on Wall Street later today. The e-mini S&P has added over 100 points from the Monday low to trade inside 50 points of the alltime highs posted July 14th.

- Focus remains on US earnings, with Johnson & Johnson, Verizon Communications and Coca-Cola among the headline reports Wednesday.

COMMODITIES: Solid Stock Bounce Underpins Modest Oil Recovery

- WTI and Brent crude futures are trading higher, with both benchmarks up over 1% apiece. This puts WTI back above the $68/bbl level, but still well shy of the week's highs at $71.67/bbl. The front-end of the futures curve has steepened out to end-2023.

- Firmer stock markets globally have helped stem losses from earlier in the week, keeping the tech picture broadly unchanged for now. The sharp sell-off defines a short-term trend top and signals scope for a deeper corrective pullback. The focus is on $64.60, a Fibonacci retracement where a break would open $63.10, the May 24 low.

- Today's DoE crude oil reserves data is the next focus, with markets expecting a draw of near 4mln bbls for the week ending July 16th.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok