Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- GBP bull binge sees GBP/USD hit new multi-year highs

- Equities buoyed by late US bounce

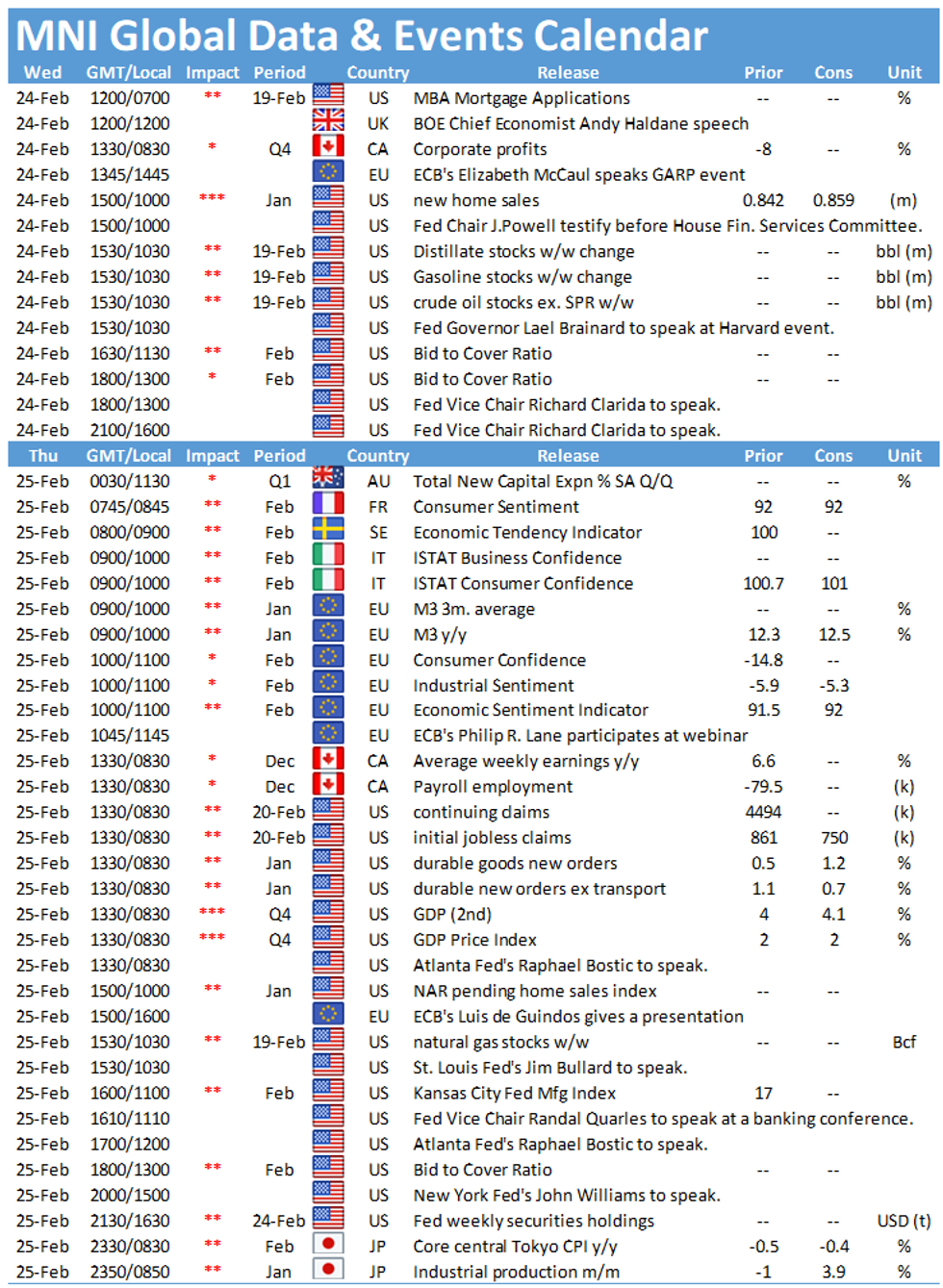

- No data due, Fed speakers again in focus

US TSYS SUMMARY: Long End Continues To Weaken, Fed Speakers Eyed

Tsys have been heading lower (within Tuesday's ranges) in the European morning as equities have bounced. A trio of Fed heavy hitters highlight Wednesday's calendar, with 2Y FRN and 5Y supply for good measure.

- Mar 10-Yr futures (TY) down 1/32 at 135-12.5 (L: 135-11.5 / H: 135-23). The long-end continues to get hit hard: the 2-Yr yield is up 0.4bps at 0.1152%, 5-Yr is up 1bps at 0.5762%, 10-Yr is up 2.7bps at 1.3688%, and 30-Yr is up 4.7bps at 2.2272% (highest since Jan 2020).

- Equities have proven resilient, bouncing Tuesday of course but also from lows overnight Wednesday. Dollar a little softer.

- Judging from Fed Chair Powell's Senate appearance Tuesday which basically hit all of the same notes he'd repeated previously, there's unlikely to be much to move the market in Wednesday's House testimony - but still bears watching (starts 1000ET, same prepared text as yesterday).

- More impactful perhaps will be Gov Brainard at 1030ET, and/or Vice Chair Clarida at 1300ET (then later at 1600ET).

- Today's data consists of Jan New Home Sales at 1000ET.

- In supply, 1130ET sees auctions of $30B 119-day bill and $26B 2Y FRN; at 1300ET, $61B 5Y Note. NY Fed buys $3.625B of 7-20Y Tsys.

EGBs/GILT SUMMARY: Broadly Weaker

European sovereign bonds have broadly traded weaker this morning alongside gains for equities.

- The gilt curve continues to bear steepen with the 2s30s spread 4bp wider.

- Bunds started the session on a strong footing, but gave up the early gains to now trade close to unchanged on the day. Last yields: 2-year -0.6905%, 5-year -0.6216%, 10-year -0.3181%, 30-year 0.1924.

- OATs have traded a touch weaker with the longer end underperforming.

- BTPs have underperformed core EGBs on the day. Cash yields are 1-3bp higher and the curve 2bp steeper.

- Supply this morning came from Germany (Bund, EUR3.32bn allotted), Italy (BOTs, EUR6.5bn) and Greece (Bills, EUR812.5mn).

- The final estimate of German Q4 GDP came in stronger than the original print (0.3% SA Q/Q vs 0.1%, -3.7% WDA Y/Y vs -3.9%).

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXJ1 170p, sold at 40 and 38 in 2k

IKJ1 151.00c, bought for 30 in 1.3k (underlying IKM1 is 149.17)

ERH1 100.50c, sold at 3.25 in 20k (ref 100.53)

3RK1 100.25/100.12ps vs 0RK1 100.50/100.37ps, bought the blue for 1.25 in 4.5k

UK:

LU1 99.87/100.00/100.12c fly, bought for 4.75 in 5k

3LH1 99.75/99.62ps vs 2LH1 99.87/99.75ps, sold the blue at 1 in 4.25k

US:

TYJ1 133.25p, sold at @15 in 20k

EUROZONE ISSUANCE: German Auction

Germany Allots E3.320bln of the 0% Feb-31 Bund:

Average yield -0.32% (-0.54%), Buba cover 1.55x (1.97x), Bid-to-cover 1.28x (1.63x)

FOREX: GBP Bull Binge Sees Cable Narrow Gap With 2018 High

GBP's impressive rally continued in early Asia-Pac hours, with GBP/USD running higher amid thin liquidity to touch 1.4237 - the best level since 2018. This narrows the gap considerably with the multi-year highs of 1.4377 - a considerable level for the pair. Contrasting the recent bull run, RSI measures are flashing the pair as technically overbought, which could suggest progress may slow from here.

At the other end of the scale, JPY is on the backfoot, reflecting the impressive recovery in US equity markets ahead of the Tuesday close. USD/JPY trades within 40 pips of the 2021 highs, but EUR/JPY's run has been more notable, with the cross extending gains to the best levels since late 2018.

There are few tier one data releases due Wednesday, leaving focus on the central bank speaker slate - BoE's Bailey, Haldane, Broadbent, Vlieghe and Haskel all speak as well as Fed's Powell (second part of his semi-annual testimony), Clarida and Brainard.

OPTIONS: Expiries for Feb24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2000-05(E627mln), $1.2035-50(E768mln), $1.2090-1.2100(E1.2bln), $1.2130-35(E1.1bln-EUR puts), $1.2150-60(E1.6bln), $1.2170-90(E2.0bln-EUR puts), $1.2200-10(E728mln)

- USD/JPY: Y103.70-80($1.6bln), Y103.95-15($1.2bln), Y105.00(E1.7bln-USD puts), Y105.65-80($3.4bln), Y105.95-15($1.3bln), Y106.70-75($580mln), Y107.00-05($1.0bln)

- EUR/GBP: Gbp0.8650(E534mln), Gbp.0.8700-20(E614mln)

- AUD/USD: $0.7700-15(A$1.2bln), $0.7800(A$1.4bln), $0.7850(A$529mln), $0.7865-75(A$1.8bln), $0.7910(A$1.2bln), $0.7950(A$604mln)

- USD/CAD: C$1.2690-1.2700($1.3bln)

- USD/CNY: Cny6.50($784mln-USD puts)

- USD/MXN: Mxn20.50($714mln), Mxn20.64-65($556mln)

EQUITIES: Late Recovery in US Stocks Boosting Core Europe

Despite a shaky session Tuesday, US equities rallied into the close which has fed into a positive start for stocks across the continent. German firms are outperforming, with the DAX higher by 0.8% while the UK's FTSE-100 lags under domestic currency strength, slipping into negative territory by 0.1%.

Across Europe, the materials sector is trading well, led higher by persistent strength in commodities markets. The only two sectors in the red so far Wednesday are communication services and consumer staples.

US equity futures continue to find support ahead of the 50-dma at 3795.35. A break below here would be a bearish sign, but markets remain well within reach of all time highs at 3959.25 should resistance at 3900.23 give way (the 61.8% Fib of the pullback from Feb highs).

COMMODITIES: Oil, Industrial Metals Stable At New Highs

Both WTI and Brent crude futures are sitting slightly higher ahead of the NYMEX open, bouncing slightly off the late Tuesday lows. Markets watch today's DoE inventories release with forecasts eyeing a draw of close to 7mln barrels in the most recent week's data. The expectations are despite the API release yesterday showing an unexpected build in stocks of just over 1mln bbls.

Copper futures continue to print higher highs, with the metal touching a new cycle high of $423.65 in early Asia-Pac trade before consolidating.

General USD weakness has helped early Wednesday, but the greenback is largely rangebound. There are no key data releases to watch Wednesday, but the second half of Powell's semi-annual testimony could be worth watching.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.