Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Post-CPI moves extend, with Greenback firmer and short-end rates squeezed

- European gas prices surge as Lukashenko threatens to shutter pipeline

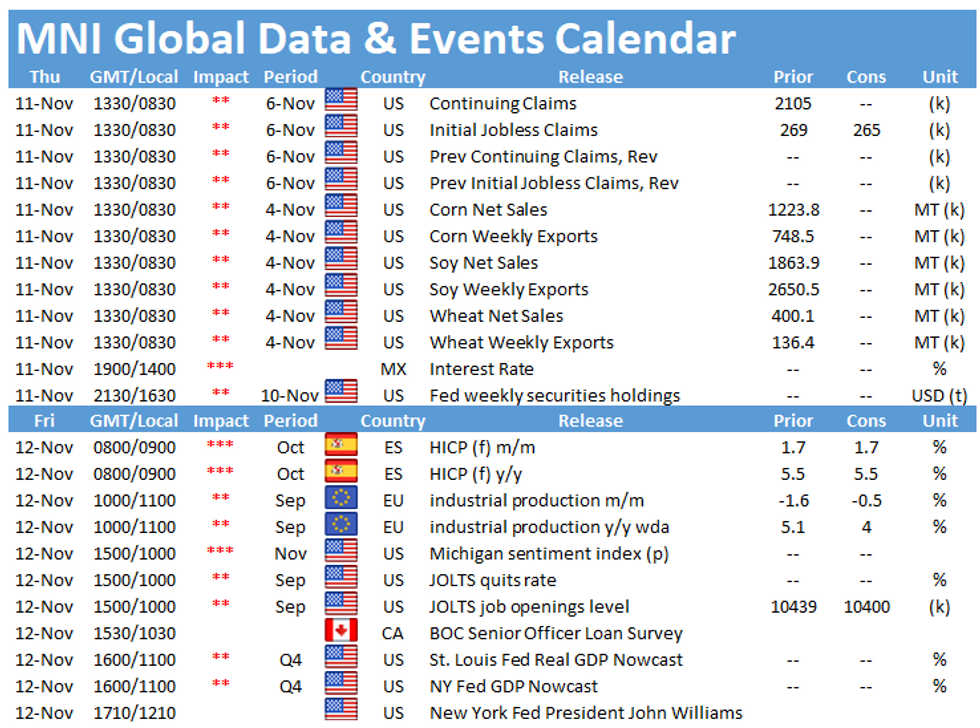

- Veteran's Day holiday should keep price action thin

US TSYS SUMMARY: Short-End Futures Weaken Further Post-CPI

Treasury futures weakened a little overnight Thursday, with the short-end seeing notable weakness as reverberations from Wednesday's high CPI print continue to reverberate.

- Dec 10-Yr futures (TY) down 1/32 at 130-22.5 (L: 130-15 / H: 130-26); not terrible volumes (~240k) considering that with the Veterans Day Holiday being observed, there is no cash Tsy trading and the CME floor is closed.

- However, equity markets are open as usual (futures rising, led by the Nasdaq).

- The ED strip through 2023 touched fresh cycle lows briefly before bouncing. 2Y futures off slightly; Ultras a little higher, bouncing a bit following the terrible 30Y auction Weds.

- No data, speakers, or supply due to the holiday.

- MNI's US Fixed Income coverage will end at 1230ET, shortly after the European cash close, picking up again during the Asia-Pacific session (around 1800ET).

EGB/GILT SUMMARY: Short-end Rates Continue Post-CPI Squeeze

- Market focus remains on rate expectations, with much of the action seen across the Euribor strip, with yesterday's multi-decade high US CPI still the catalyst behind gyrations in the fixed income market. The strip has traded lower by as much as 7 ticks this morning,

- Bund futures are recovering off the morning's lows of 170.21, prompting a minor drift in the 10yr yield, retreating to -0.255%. The curve has steepened slightly, with 2y yields off as much as 2bps.

- Gilt futures are extending the bounce off the 50-dma at 125.90, but remain well off the Wednesday highs of 127.10.

- Treasury cash markets are closed for the duration of the Thursday session, which may see volumes and liquidity dry up beyond the NY crossover. As a result, there's little data due, but CB speak keeps up, with BOE's Mann, ECB's Lane, Schnabel and de Cos on the docket.

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXF2 171.5/173/174.5c fly, bought for 30.5 in 1k

RXZ1 169.5/168.5ps, bought for 19 in 2.15k

OEZ1 135.50/135.75cs, bought for 2.5 in 2k

FOREX: Greenback Holds Post-CPI Strength

- The greenback remains the firmest currency in G10 Thursday, extending the strength built on the back of the surge in inflation evident in Wednesday's CPI. This puts EUR/USD at a fresh 2021 low and the lowest levels since July 2020, opening losses toward 1.1423, the Jul 21 2020 low as well as the 1.1375 1.382 projection, drawn from the Jan 6 - Mar 31 - May 25 price swing.

- Growth proxies and high beta currencies are following suit, with NZD, AUD and CAD among the session's worst performers, reinforcing the market's renewed concern that hot inflation will force the Fed to bring forward possible rate hikes or accelerate the pace of the asset purchase taper. NZD/USD plumbs a fresh November low at 0.7013, breaking below the 100-dma at 0.7027 in the process.

- Volume and market activity will likely drop off as the session continues, with the Veteran's Day holiday keeping fixed income markets closed for the duration. As a result, there are no key data releases Thursday, however a number of ECB speakers are due - with ECB's Lane, Schnabel and de Cos all on the docket.

FX OPTIONS: Expiries for Nov11 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550-70(E1.6bln), $1.1580(E566mln), $1.1650(E605mln)

- USD/JPY: Y113.00-20($1.8bln), Y113.25-45($1.5bln), Y113.50-60($1.7bln), Y113.70($1.5bln)

- AUD/USD: $0.7330-40(A$845mln)

Price Signal Summary - USD Resumes Its Uptrend

- In the equity space, the uptrend in the S&P E-minis remains intact and this week's pullback is still considered a correction. The focus is on 4717.00 next, 1.50 projection of the Jul 19 - Aug 16 - Aug 19 price swing. Initial support to watch is 4585.38, the 20-day EMA. EUROSTOXX 50 futures are consolidating below recent highs and this week's activity still appears to be a bull flag. The trend needle points north and the focus is on 4371.00, 1.236 projection of Jul 19-Sep 6-Oct 6 2020 swing (cont).

- In FX, a sharp sell-off in EURUSD yesterday has confirmed a resumption of the downtrend and conditions remain bearish within the bear channel drawn off the Jun 1 high. The focus is on 1.1423, Jul 21 2020 low. GBPUSD remains vulnerable following a doji candle pattern Tuesday and yesterday's sharp sell-off. The break of 1.3412, Sep 29 low, opens 1.3354, Dec 23, 2020 low. Yesterday's candle pattern in USDJPY appears to be a bullish engulfing reversal. If correct, this pattern signals scope for a climb towards key resistance at 114.70, Oct 20 high. Key support has been defined at 112.73, Nov 9 low.

- On the commodity front, Gold rallied sharply higher yesterday and remains firm. The focus is on $1877.7 next, Jun 14 high ahead of the $1900.00 handle. WTI gains stalled yesterday and the key resistance of $85.41, Oct 25 high, remains intact. A break would confirm a resumption of the uptrend. On the downside, key short-term support has been defined at $78.25, Nov 4 low.

- In the FI space, Bund futures maintain a bullish short-term tone despite yesterday's move lower. The recent break of 169.83, Oct 27 high and clearance of the 50-day EMA, opens 171.95, 61.8% of the Aug - Nov sell-off. Gilts also maintain a firmer tone. The focus is on a climb towards 127.69 next, Sep 21 high. The recent pullback is considered corrective.

EQUITIES: Futures Recover Off Bottom Ahead of Holiday-Thinned Trade

- US stock futures trade solidly ahead of the NY crossover, with the e-mini S&P adding 15 points on the session and over 30 points off the lows printed late yesterday. The improvement for stocks comes alongside further gains for European markets, helping to boost Germany's DAX to fresh alltime highs.

- Europe's materials and industrials sectors are top of the pile, with energy and real estate names lagging.

- Cash equities remain open throughout the Thursday session, however broad closures across fixed income exchanges could drain volumes as newsflow dims for the Veteran's Day holiday.

COMMODITIES: European Gas Prices Buoyed By Lukashenko Threats

- Oil futures are under pressure in early Thursday trade, with WTI and Brent off 0.5 to 0.75% ahead of the NY crossover. Post-CPI losses for energy have continued, with a firming greenback adding additional pressure.

- More notable activity was present in European energy markets, with prices supported by threats from Belarus' Lukashenko, who warned that gas supply pipelines linking Russia to Europe could be shuttered in response to Europe's warnings that borders into the European Union could be closed to migrants.

- Contrasting with US energy markets, precious metals are advancing as gold's status as an inflation hedge comes back into view following yesterday's multi-decade high in CPI.

- The move higher resulted in a clear break of resistance at $1834.0, Sep 3 high. The breach of this hurdle reinforces current bullish conditions and paves the way for further upside. Note too that the yellow metal has also breached $1863.3, 76.4% of the Jun -Aug sell-off. The focus is on $1877.7 next, Jun 14 high.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok