Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Equity rally hits pause, but no dip yet

- Germany sees first positive yield at 30y operation since June

- JPY crosses reverse, first down day in six for EUR/JPY

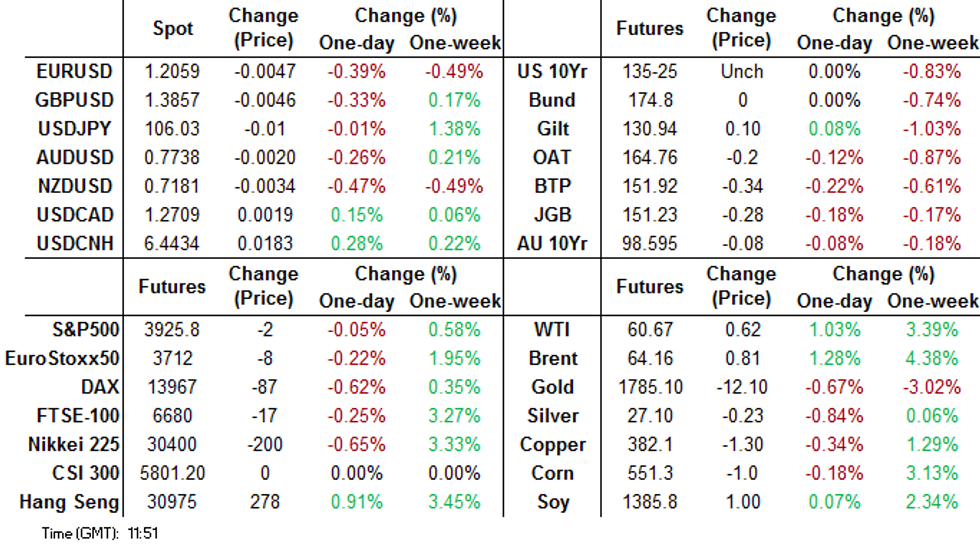

US TSYS SUMMARY: Data Eyed Ahead Of 20Y Supply And FOMC Minutes

Tsys have bounced from overnight lows with the curve flattening substantially from Tuesday's steepest levels.

- Mar 10-Yr futures (TY) steady at at 135-25 (L: 135-17 / H: 135-28.5)

- The 2-Yr yield is down 0.4bps at 0.115%, 5-Yr is down 1.3bps at 0.5609%, 10-Yr is down 2.2bps at 1.2922%, and 30-Yr is down 2.5bps at 2.0673%.

- Safe havens are broadly in favor, with the dollar hitting best levels in more than a week, and stock futures a little lower.

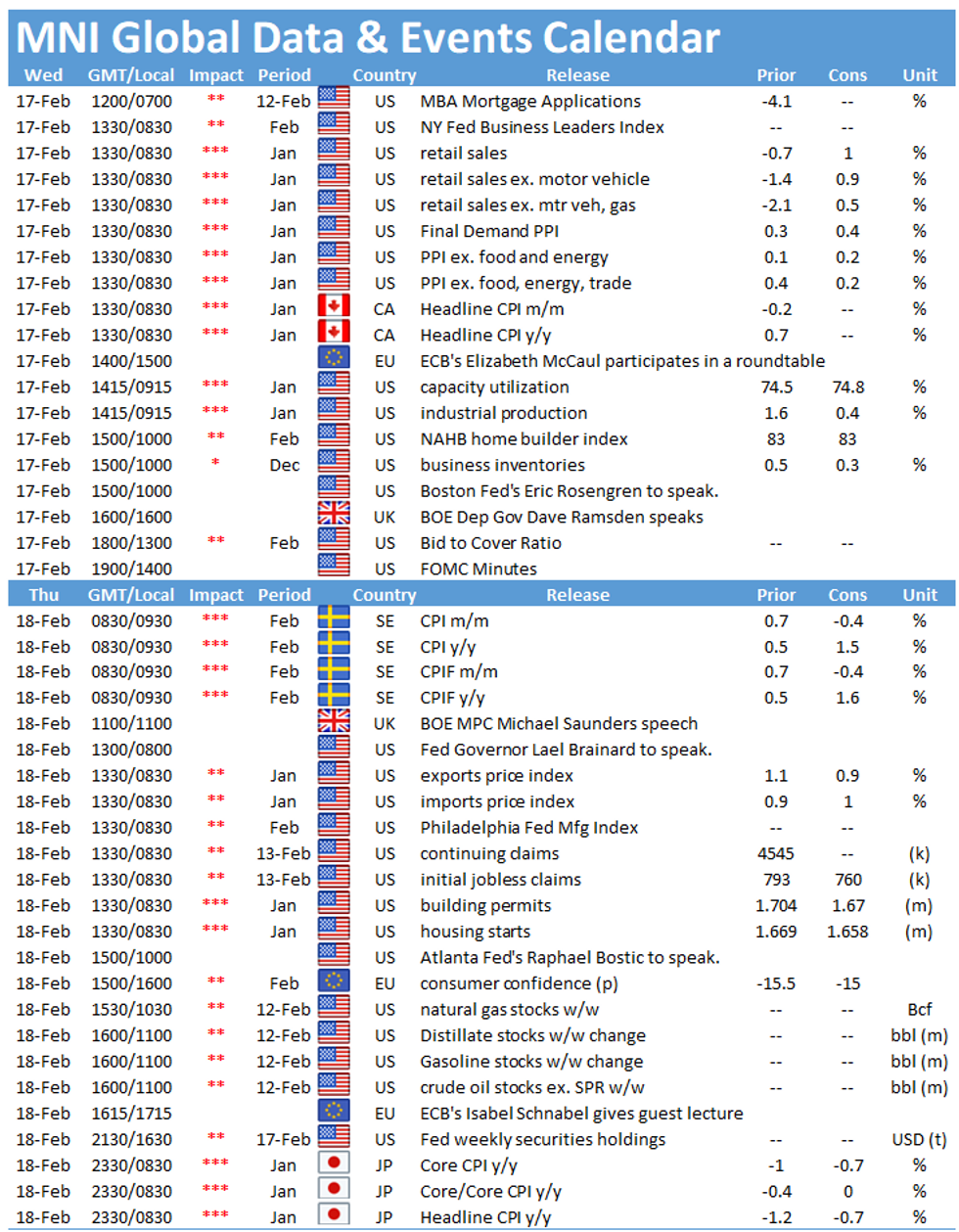

- A relatively busy data schedule today: 0830ET sees Jan advance retail sales and PPI data. Then at 0915ET, Jan industrial production, and at 1000ET, Dec business inventories.

- In Fed speakers, Richmond's Barkin is up at 0900ET, with Boston Fed's Rosengren at 0915ET (today's previously scheduled event w Dallas's Kaplan was cancelled). These appearances come ahead of the Jan FOMC minutes, out at 1400ET.

- Supply is $27B 20Y Bond auction at 1300ET. PNY Fed buys ~$1.225B of 7.5-30Y TIPS.

EGB/GILT SUMMARY: Risk Off Posture Helps Core EGBs Rally

Markets have shifted to a risk-off posture this morning with core govies rallying, periphery EGBs trading weaker, equities broadly lower and the US dollar gaining ground against G10 FX.

- Gilts have rallied and outperformed European majors with longer end yields now down 3bp on the day.

- Bunds opened weaker but have firmed through the morning and now trade marginally above yesterday's close.

- BTPs have sold off and the curve has slightly bear steepened with the 2s30s spread 2bp wider.

- Mirroring a similar trend seen in the euro area, UK CPI pushed higher in January and came in above expectations (0.7% vs 0.6% survey).

- Supply this morning came from the UK (Gilt, GBP2.5bn), Germany (Bund, EUR 1.2324bn allotted), and Portugal (BTs, EUR1.25bn).

EUROPE ISSUANCE: German, UK Auctions

GERMAN AUCTION RESULTS: First positive yield for 30y operation since June

Germany Allots E1.2324bln of the 1.25% Aug-48 Bund

Average yield 0.10% (-0.07%), Buba cover 1.31x (1.95x), Bid-to-cover 1.08x (1.73x)

UK DMO sells GBP2.50bln nominal of the 0.625% Jul-35 gilt

Avg yield 0.969% (0.614%), bid-to-cover 2.55x (2.66x), tail 0.5bp (0.2bp), price 95.372 (100.154)

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXH1 176c, bought for 2 in 7.5k

RXH1 173.50p, bought for 3 in 5k

RXJ1 173.5c, bought for 30 in 12.75k

RXM1 172/169.5ps 1x2, bought for 36 in 1.5k

OEH1 135/134.75/134.50p fly sold at 3 in ~6k

UK:

LZ1 100/99.87/99.75p fly 1x3x2 vs LM1 100/99.87/99.75p fly 1x3x2, bought the Dec for -1 (receive) in 30k

3LM1 99.62/50/37/25p condor, sold at 4 in 3k

3LM1 99.25/99.00ps vs 99.75c, bought ps for 0.25 in 4.8k

FOREX: First Down Day in Six For EUR/JPY

The pullback from Tuesday's EUR/USD high has extended early Wednesday, with prices slipping comfortably through the 1.21 handle to set sights on the Feb 9 low at 1.2047. A break below here would be a bearish development, and increase focus on Tuesday's candle pattern which resembles a bearish shooting star.

The greenback is among the strongest in G10 so far today, with equities circling the week's lows and consolidating yesterday's (slightly) negative close for the S&P 500. This has buoyed JPY so far Wednesday, which is clawing back recent losses against a number of currencies, most notably EUR.

The front-end of the DM implied vol curve has seen some support, with the equity pullback helping arrest recent declines. 1m AUD/USD implied vols look to have bottomed after printing post-COVID lows earlier this week of just 8.97 points.

Focus for the rest of the sessions switches to data, with US retail sales, PPI and industrial production due. CPI numbers for January from Canada also cross. Central bank speakers include Fed's Barkin & Rosengren, BoE's Ramsden and the FOMC minutes.

OPTIONS: Expiries for Feb17 NY cut 1000ET (Source DTCC)

EUR/USD: $1.2000-10(E880mln), $1.2035-40(E611mln), $1.2075(E544mln), $1.2100-05(E654mln), $1.2120-40(E2.4bln-EUR puts), $1.2150-55(E527mln), $1.2170(E699mln)

USD/JPY: Y105.35-50($735mln)

EUR/GBP: Gbp0.8700(E781mln-EUR puts), Gbp0.8750(E501mln-EUR puts)

EUR/CHF: Chf1.0725(E445mln), Chf1.0775(E430mln)

USD/NOK: Nok8.40($610mln-USD puts), Nok8.50($300mln-USD puts), Nok8.80($560mln-USD puts)

AUD/USD: $0.7615-25(A$2.1bln), $0.7750(A$759mln), $0.7850-55(A$564mln)

AUD/JPY: Y80.00(A$636mln), Y81.75-85(A$697mln)

USD/CAD: C$1.2650($475mln)

TECHS: Price Signal Summary - Shooting Star Candle In EURUSD

- Equity indices outlook is unchanged and bullish, E-mini S&P futures target the psychological 4000.00 handle.

- An initial objective is at 3988.40, 2.236 projection of the Sep 24 - Oct 12 - Oct 30 price swing last year.

- In the FX space, EURUSD is softer this morning. Yesterday's candle pattern - a shooting star formation is a concern for bulls. Support to watch lies at 1.2020, the Feb 8 low. The key support to watch in the USD Index is 90.05, Jan 21 low. This level remains intact and is still a key pivot point. A break would negate the recent reversal pattern - an inverted head and shoulders. USDJPY key resistance at 105.77, Feb 5 high has been cleared and the uptrend from Feb 10 has resumed. The focus is on 106.26 next, 1.50 projection of Jan 6 / 11 / 21 price swing EURGBP outlook remains bearish and has traded below 0.8700. Scope is seen for weakness towards 0.8671, Apr 30 low, 2020.

- On the commodity front, Gold has probed support at $1785.0, Feb 4 low. A clear break would confirm a resumption of the downtrend that started Jan 6 and open $1764.8, Nov 30 low. Oil contracts remain firm. Brent (J1) targets $64.58, Jan 22 high, 2020 (cont). WTI (H1) bulls eye $61.11, 1.500 projection of Apr - Aug rally from the Nov 2 low

- In the FI space, Bunds (H1) have found support today but the trend remains down and gains are considered corrective. Resistance is seen at 175.45, Dec 16 high. Gilts (H1) remain in a downtrend and gains are also considered corrective. Resistance is seen at 131.49, Feb 16 high. Initial resistance in Treasuries is seen at 136-01, Jan 12 low. The trend remains down.

EQUITIES: Stocks Hit Speed Bump, But Little Sign of Any Material Dip

Stocks across Europe are in minor negative territory early Wednesday, following on from the pullback in US futures overnight. The downside is mild, with losses contained to 0.2-0.6% for continental bourses while US futures are circling at and around yesterday's lowest levels.

Consumer discretionary and tech names are leading losses on the continent, while energy and materials firms are spared from the bulk of the losses.

- Equity indices remain bullish despite Tuesday's pullback, E-mini S&P futures have edged higher and are moving towards the psychological 4000.00 handle. An initial objective is at 3988.40, 2.236 projection of the Sep 24 - Oct 12 - Oct 30 price swing last year.

COMMODITIES: Oil Curve Firms Further, Dec-23 Futures Top $50/bbl

The crude futures curve firmed further Wednesday, with the all contracts out to Dec-2023 now north of $50/bbl for the first time since early 2020.

- The move higher in both WTI and Brent crude futures Wednesday comes despite the stall in equity momentum, with focus remaining on the inclement weather conditions in southern US states. Rolling blackouts are persisting across Texas, with areas of the state seen being effected for several more days due to production shutdowns, soaring energy demand and scarce supply.

- Near-term resistance for WTI crude futures crosses at $60.95 for the front-month contract and $61.11 further out.

- Silver remains vulnerable following the sharp sell-off on Feb 2. Recent gains are considered a correction and a resumption of weakness is seen likely near-term. A move lower would refocus attention on $25.905, the Feb 4 low and clearance of this support would set the scene for a deeper pullback.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.