Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

- Treasury curve sits bull flatter, withdrawing from YTD steeps

- USD/JPY falters again on approach to Y150.00

- Fed's Harker, Mester round off FOMC appearances ahead of media blackout

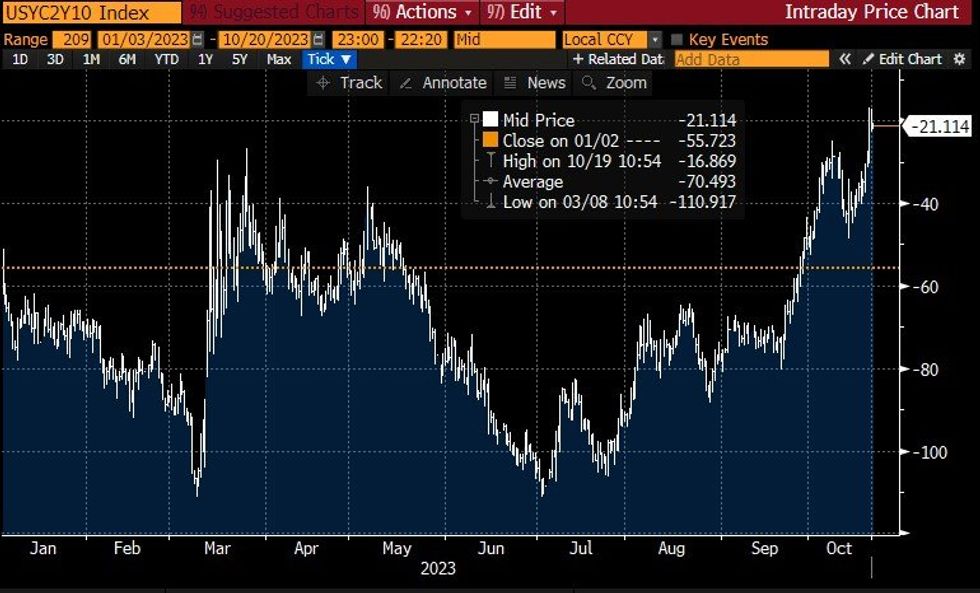

US TSYS: Bull Flatter To Pullback Off YTD Steeps

- Treasuries have seen some intraday cheapening impetus but still trade bull flatter on the day, with cash benchmarks 0.5bp to 4.5bp richer. It does however only partly reverse yesterday’s large twist steepening driven by Chair Powell’s remarks.

- They are off overnight highs across the curve, although potential catalysts for the net bid includes soft UK data, Asia-Pac liquidity provisions, the potential for some pre-weekend Israel-Hamas related hedging and Asia-Pac reaction to outright long end yield levels.

- 2s10s sit at -21bp (-4.5bp), off yesterday’s fresh ytd highs of -16.5bps.

- TYZ3 trades at 105-23 (+9), within overnight ranges and also yesterday’s ranges seen with Powell-induced volatility having touched 105-30+ with the text before a low of 105-10+ in the Q&A. The latter marks new support after which lies 104-27+ (2.0% 10-dma envelope). Volumes are robust at 370k.

- Fedspeak headlines the docket with ’23 voters Harker (0900ET) and Mester (1215ET).

- No data or issuance ahead, whilst today’s earnings schedule is relatively light compared to past days in terms of S&P market share.

Source: Bloomberg

Source: Bloomberg

STIR SUMMARY: Fed Rate Path Consolidates Powell Pullback, ’23 Voters Ahead

- Fed Funds implied rates consolidate yesterday’s decline accelerated by Chair Powell’s remarks at the Economic Club of NY, sitting marginally lower for Nov and Dec meetings and slightly higher later into 2024.

- It sees just 0.5bp of tightening for the Nov FOMC, building to a cumulative 9.5bp of hikes to a terminal 5.43% in January, followed by 70bp of cuts to end-2024.

- Today’s docket is limited to ’23 voters, with Harker (0900ET) and Mester (1215ET) both on the economic outlook including prepared remarks.

- Harker has spoken a number of times, most recently late yesterday: at a point where we can hold rates where they are but won’t hesitate to support more hikes if needed. Not going to react to normal variability in M/M data, data point to steady if slow disinflation. I tend to be on low end of the dot plot.

- It’s Mester’s first appearance since US CPI, having said on Oct 6 that interest rates are at or very near peak with further tightening depending on incoming data and that the jobs report continues to show strong job market.

CANADA: Monthly Inflation Watch - CPI Sticky Amid Recession Fears

- BOC's Sept rate decision said focus would be on: evolution of excess demand, inflation expectations, wage growth, corporate pricing power.

- Since then, excess demand has come down; the last reading of GDP was flat, although clouded by industry disruptions. A third of businesses and over half of consumers expect a recession.

- Inflation expectations remain elevated; the Q3 business survey revealed a third of firms expect it to take longer than three years to reach the inflation target.

- Firms are revising down their hiring plans, but wage growth remains high. Sept jobs report +5% wage gains and July payroll average weekly earnings +4.3%.

- Corporate pricing power still abnormal, 23% of firms plan to make larger than normal price increases.

- Oil prices down compared to Sept but remain tight from OPEC cuts with further risk of high prices from Israel/Gaza conflict.

- Broad-based slowdown in last CPI report as both headline and core eased. Inflation still far above the bank’s target rate at 3.8% YOY.

US TSYS: OI Points To Significant Long Building In SOFR Whites & Reds Post-Powell

The combination of preliminary open interest data and yesterday’s twist steepening of the SOFR strip point to the following positioning swings on Thursday:

- Whites & Reds: Notable apparent long setting through both packs. Fed Chair Powell’s dovish leaning rhetoric re: the Fed’s dual mandate was the most obvious trigger for that swing.

- Greens: Seemingly dominated by short setting.

- Blues: Long cover seemed to dominate.

- For the greens and the blues, the twist steepening of the Tsy curve generally managed to more than offset the post-Powell impulse when it came to net price action on the day.

| 19-Oct-23 | 18-Oct-23 | Daily OI Change | Daily OI Change In Packs | ||

| SFRU3 | 933,053 | 929,995 | +3,058 | Whites | +111,451 |

| SFRZ3 | 1,509,356 | 1,455,217 | +54,139 | Reds | +75,959 |

| SFRH4 | 1,005,618 | 976,467 | +29,151 | Greens | +34,136 |

| SFRM4 | 968,100 | 942,997 | +25,103 | Blues | -32,415 |

| SFRU4 | 831,653 | 792,181 | +39,472 | ||

| SFRZ4 | 996,438 | 991,572 | +4,866 | ||

| SFRH5 | 531,170 | 512,405 | +18,765 | ||

| SFRM5 | 586,312 | 573,456 | +12,856 | ||

| SFRU5 | 518,776 | 501,827 | +16,949 | ||

| SFRZ5 | 537,656 | 533,089 | +4,567 | ||

| SFRH6 | 339,971 | 331,104 | +8,867 | ||

| SFRM6 | 301,591 | 297,838 | +3,753 | ||

| SFRU6 | 245,899 | 244,745 | +1,154 | ||

| SFRZ6 | 195,612 | 225,622 | -30,010 | ||

| SFRH7 | 136,939 | 139,780 | -2,841 | ||

| SFRM7 | 133,785 | 134,503 | -718 |

STIR: OI Points To Significant Long Building In SOFR Whites & Reds Post-Powell

The combination of preliminary open interest data and yesterday’s twist steepening of the SOFR strip point to the following positioning swings on Thursday:

- Whites & Reds: Notable apparent long setting through both packs. Fed Chair Powell’s dovish leaning rhetoric re: the Fed’s dual mandate was the most obvious trigger for that swing.

- Greens: Seemingly dominated by short setting.

- Blues: Long cover seemed to dominate.

- For the greens and the blues, the twist steepening of the Tsy curve generally managed to more than offset the post-Powell impulse when it came to net price action on the day.

| 19-Oct-23 | 18-Oct-23 | Daily OI Change | Daily OI Change In Packs | ||

| SFRU3 | 933,053 | 929,995 | +3,058 | Whites | +111,451 |

| SFRZ3 | 1,509,356 | 1,455,217 | +54,139 | Reds | +75,959 |

| SFRH4 | 1,005,618 | 976,467 | +29,151 | Greens | +34,136 |

| SFRM4 | 968,100 | 942,997 | +25,103 | Blues | -32,415 |

| SFRU4 | 831,653 | 792,181 | +39,472 | ||

| SFRZ4 | 996,438 | 991,572 | +4,866 | ||

| SFRH5 | 531,170 | 512,405 | +18,765 | ||

| SFRM5 | 586,312 | 573,456 | +12,856 | ||

| SFRU5 | 518,776 | 501,827 | +16,949 | ||

| SFRZ5 | 537,656 | 533,089 | +4,567 | ||

| SFRH6 | 339,971 | 331,104 | +8,867 | ||

| SFRM6 | 301,591 | 297,838 | +3,753 | ||

| SFRU6 | 245,899 | 244,745 | +1,154 | ||

| SFRZ6 | 195,612 | 225,622 | -30,010 | ||

| SFRH7 | 136,939 | 139,780 | -2,841 | ||

| SFRM7 | 133,785 | 134,503 | -718 |

RATINGS: Friday's Sovereign Rating Slate

Potential sovereign credit rating reviews of note scheduled for after hours on Friday include:

- Fitch on Slovenia (current rating: A; Outlook Stable)

- Moody’s on France (current rating: Aa2; Outlook Stable), Ireland (current rating: Aa3; Outlook Stable) & the United Kingdom (current rating: Aa3; Outlook Negative)

- S&P on Greece (current rating: BB+; Outlook Positive), Italy (current rating: BBB; Outlook Stable), the Netherlands (current rating: AAA; Outlook Stable) & the United Kingdom (current rating: AA; Outlook Stable)

FOREX: USD/JPY Falters Again on Approach to Y150

- UK retail sales data came in soft relative to expectations, with headline Y/Y at -1.0% vs. Exp. -0.2%, helping GBP ease further off overnight highs and retain a bearish theme in the short-term. Thursday's lows provide initial support at 1.2090, and slippage through here would open the lowest levels since early October and the bear trigger of 1.2037.

- Elsewhere, USD/JPY made further progress toward Y150, printing a high at Y149.99 before aggressively retreating to touch daily lows of 149.69. The pullback proved short-lived as spot swiftly recovered to trade back above Y149.95 after a few minutes.

- The price action not driven by headline flow, more likely standing offers at the handle as markets remain cautious about potential Japanese intervention in the pair. The accompanying volume surge in JPY futures on the move (around 7,500 contracts changed hands inside 60 seconds, cash equivalent of approx $630mln) was considerably smaller relative to the move on Oct 3rd, which saw over twice the volume over the same period of time.

- CAD and USD trade toward the top-end of the G10 table early Friday, with AUD and NZD among the weakest. This reinforces the low growth, high inflation theme pervading across markets, as steepening global curves and the higher oil prices reinforce expectations of economic weakness ahead.

- Focus during US hours turns to Canadian retail sales and appearances from Fed's Harker and Mester - who make the last appearances for the FOMC before the Fed's media blackout period.

FX OPTIONS: Expiries for Oct20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0475-85(E1.2bln), $1.0550(E1.3bln), $1.0575-85(E744mln), $1.0600(E1.4bln), $1.0625(E2.0bln), $1.0640-55(E1.8bln)

- USD/JPY: Y148.85-05($1.0bln), Y149.00-05($976mln), Y150.00($857mln), Y150.50($720mln)

- USD/CAD: C$1.3555($798mln), C$1.3600($1.6bln), C$1.3715-25($576mln)

- USD/CNY: Cny7.2500($1.3bln), Cny7.3000-15($910mln)

GILTS: Futures Reverse Early Gains, Curve Twist Steepens

Gilt futures continue to fade from best levels of the day to last trade -10.

- Bears remain focused on yesterday’s low, which protects the ‘22/LDI meltdown low from a technical standpoint.

- The early bid stemming from the latest domestic public finance data and softer than expected retail sales prints has faded, leaving cash yields 3bp lower to 4bp higher as the curve twist steepens.

- 2s10s have printed at the least inverted level seen since June.

- There was also a global feel to the early bid in futures, given the rally elsewhere (pre-weekend Israel-Hamas hedging, a weaker start for equities and Asia-Pac liquidity provisions highlighted), while participants have also had to assess the degree of justified spill over from Fed Chair Powell’s Thursday comments.

- Also note that BoE Governor Bailey’s early morning comments failed to meaningfully move the needle, although the fact that he noted that September’s CPI data failed to provide any meaningful surprises may have facilitated some modest dovish repricing in the front end.

- SONIA futures last show flat to +6.0 through the blues, with the reds outperforming.

- BoE-dated OIS contracts are 1.5-4.5bp softer on the day as that strip flattens.

EQUITIES: Move Lower in Eurostoxx 50 Futures This Week Reinforces Bearish Conditions

- A bearish theme in Eurostoxx 50 futures remains in play and this week’s move lower reinforces bearish conditions. The contract has traded through support at 4082.00, the Oct 4 low and a bear trigger. This confirms a resumption of the downtrend and maintains the bearish price sequence of lower lows and lower highs. The focus is on 4055.40, a Fibonacci retracement. Initial resistance is at 4178.80, the 20-day EMA.

- S&P e-minis maintain a softer tone and the contract continues to trade below resistance at the 50-day EMA, at 4482.75. A clear breach of this average is required to strengthen bullish conditions and this would open 4486.12, trendline resistance drawn from the Jul 27 high. On the downside, a deeper pullback would open 4235.50, the Oct 4 low and bear trigger. A break of this support would confirm a resumption of the downtrend.

COMMODITIES: WTI Futures Remain Firm After Trading Higher Thursday

- WTI futures traded higher yesterday and the contract remains firm. The latest recovery has highlighted a key support at $80.20, the Oct 6 low. The medium-term trend condition remains bullish and an extension higher would expose the bull trigger at $92.48, the Sep 28 high. Clearance of this hurdle would confirm a resumption of the uptrend. For bears, a move through $80.20, would instead highlight a short-term top.

- Gold has traded higher this week, extending the reversal from $1810.5, the Oct 6 low. The yellow metal has breached key resistance at $1953.0, the Sep 1 high. The clear break of this level further strengthens a bullish theme and opens $1987.5, the Jul 20 high. Initial firm pivot support lies at $1904.7, the 50-day EMA. Clearance of this level is required to signal a short-term top and a potential reversal.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/10/2023 | 1230/0830 | ** |  | CA | Retail Trade |

| 20/10/2023 | 1300/0900 |  | US | Philadelphia Fed's Pat Harker | |

| 20/10/2023 | 1615/1215 | | US | Cleveland Fed's Loretta Mester | |

| 20/10/2023 | 1930/1530 | ** | | US | Treasury Budget |

| 20/10/2023 | 2000/1600 | | US | Fed Financial Stability Report | |

| 23/10/2023 | 1400/1600 | ** |  | EU | Consumer Confidence Indicator (p) |

| 24/10/2023 | 2200/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok