Highlights:

- Treasuries hold tight range as all focus turns to inflation print, and FOMC decision

- Dot plot in focus, with median dot seen trimming a rate cut for this year

- USD vols bid to YTD highs as markets contemplate triple whammy of US risk events

- Treasuries are holding mildly higher, inside narrow overnight ranges ahead of this morning's May CPI inflation data at 0830ET followed by this afternoon's FOMC rate announcement at 1400ET and Chairman Powell's press conference at 1430ET.

- Headline CPI is expected to pull back fairly sharply to 0.1% (median; 0.12% average unrounded) vs 0.31% in April, owing largely to a drop in energy/gasoline prices on a seasonally-adjusted basis.

- The Fed is expected to keep rates steady today, market focus on what they may signal for potential easing later this year. The new Dot Plot is likely to show a shift in the Fed funds median to 2 cuts in 2024, versus 3 in the prior two editions, alongside a nudge higher in the inflation forecasts.

- Sep'24 10Y Treasury futures are currently trading +0.5 at 109-18. Initial technical resistance at 109-27 (50% of of the June 7-10 sell-off) followed by 110-21 (June 7 high).

- Cash yields are running mildly lower: 5s -.0054 at 4.4129, 10s -.0059 at 4.3981%, 30s -.0048 at 4.5318%, while curves remain mixed: 2s10s -0.787 at -43.999, 5s30s +0.061 at 11.708.

- Following today's data/event risk, focus turns to May PPI and weekly claims Thursday morning.

STIR: OI Points To Mix Of Long Setting & Short Cover In SOFR Futures On Wednesday

The combination of yesterday’s rally in SOFR futures and preliminary OI data points to net short cover dominating in the whites and greens (in net pack OI terms), while long setting was the more prominent factor in the reds and blues.

- The long end rally was driven by political unrest in Europe and strong demand at the latest 10-Year Tsy auction, which provided spill over support for the short end.

- SOFR options flow saw a mix of dovish and hawkish Fed plays on the day.

- ~37bp of ’24 cuts are priced into FOMC-dated OIS, little changed vs. this time yesterday.

- ~22bp of cuts are priced through the November FOMC, also little changed vs. this time yesterday.

- CPI data and the latest FOMC decision headline the macro calendar today.

| 11-Jun-24 | 10-Jun-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRH4 | 905,911 | 903,652 | +2,259 | Whites | -30,619 |

| SFRM4 | 1,335,747 | 1,349,422 | -13,675 | Reds | +7,357 |

| SFRU4 | 1,202,154 | 1,209,723 | -7,569 | Greens | -13,146 |

| SFRZ4 | 1,095,207 | 1,106,841 | -11,634 | Blues | +3,915 |

| SFRH5 | 808,902 | 802,598 | +6,304 | ||

| SFRM5 | 767,663 | 781,957 | -14,294 | ||

| SFRU5 | 735,108 | 737,219 | -2,111 | ||

| SFRZ5 | 816,259 | 798,801 | +17,458 | ||

| SFRH6 | 564,325 | 559,814 | +4,511 | ||

| SFRM6 | 496,670 | 507,138 | -10,468 | ||

| SFRU6 | 427,151 | 421,970 | +5,181 | ||

| SFRZ6 | 364,773 | 377,143 | -12,370 | ||

| SFRH7 | 254,862 | 256,290 | -1,428 | ||

| SFRM7 | 201,942 | 195,567 | +6,375 | ||

| SFRU7 | 161,765 | 160,875 | +890 | ||

| SFRZ7 | 158,099 | 160,021 | -1,922 |

MNI Livestreamed Connect with ECB Luis de Guindos Today

You are invited to listen to a livestreamed MNI Connect event with Luis de Guindos, Vice-President of the European Central Bank on June 12.

Please sign up to listen to the opening remarks and Q+A in real-time.

- Speaker: Luis de Guindos, Vice-President of the European Central Bank

- Topic of discussion: 'Euro Area Growth and Inflation Outlook'

- Date: Wednesday 12 June, 2pm-3.30pm London time

- This event is on the record and will run as a Zoom Webinar

To register please go to: MNI Webcast Registration

FRANCE: Macron Refutes Rumour Of Resignation

French President Emmanuel Macron, now answering questions from journalists at his first election press conference, strongly refutes the prospect of his resignation as president should his bloc perform poorly. Rumours had circulated in recent days (and believed to have been accelerated by Russian outlets). Macron says, "I am going to wring the neck of this duck which never existed” , stating that he committed to a full five year term in the 2022 presidential election.

- Macron claims that a win for the far-right Rassembelement National (National Rally, RN) in the upcoming legislative elections would mean France leaving NATO and an ambiguous stance from Paris towards Russia and its invasion of Ukraine.

- Says that many of those who voted for the far-right do not“agree with the ideas of the National Rally,” and that“They simply expressed anger ,” Macron says that the 'signal was recieved'. Goes on to say the National Rally is "a project which will not respond to the insecurity you are experiencing," and that they do not have the answer.

- Macron says he will not debate against RN parliament leader Marine Le Pen, and that he will also not actively campaign in the elections. Says he did not do so in the 2017 or 2022 legislative elections, and will leave it to PM Gabriel Attal.

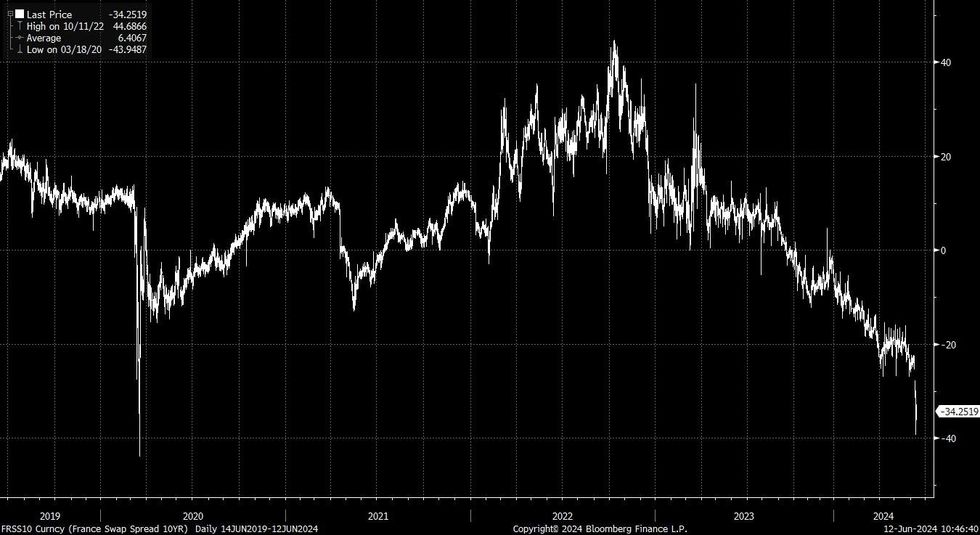

OAT: 10-Year Swap Spreads Off Yesterday’s Cycle Tights, Parallels With ’17 Move Noted

Political uncertainty has also showed up in OAT swap spreads in recent days, with the move off yesterday’s fresh cycle tights coming alongside a move off fresh cycle wides in OAT/Bunds.

- The 10-Year swap spread tightened to levels not seen since ’17 on Tuesday, but last shows the best part of 10bp off’17 tights (and 5bp off yesterday’s tightest levels).

- The ’17 tights correspond with the time that Frexit worry and RN popularity peaked in the ‘17 election cycle, drawing some obvious comparisons when it comes to the recent move.

- Local matters have taken over from the broader EGB-/ECB-driven spread tightening.

French 10-Year Swap Spread (bp)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

EUROPE ISSUANCE UPDATE:

UK auction results

* That is the first auction of that linker. It was a very well received auction with a bid-to-cover of 3.88x which is the highest at a linker auction since at least 2017 (possibly further).

* There was an upward move in the 0.625% Mar-45 linker price, but only reversing the concession seen at the end of the auction window.

* No notable impact on wider conventional gilts or gilt futures.

* GBP900mln of the 0.625% Mar-45 linker. Avg yield 1.304% (bid-to-cover 3.88x).

Germany auction results

* E4bln (E3.33bln allotted) of the 2.20% Feb-34 Bund. Avg yield 2.6% (bid-to-offer 1.70x; bid-to-cover 2.05x).

USD Index Remains Firm Ahead of Triple Whammy of US Risk

- The US CPI release and the Fed decision should keep markets busy for the duration Wednesday. USD vols are well bid headed into the event risk, with EUR/USD overnight vols topping 14 points for the first time in 2024 as contracts capture both US CPI and PPI prints, as well as tonight's press conference with Powell.

- The JPY is the poorest performer in G10, USD/JPY remains well within reach of yesterday's 157.40 highs, but resistance is seen firmer into 157.71, the late May cycle highs. The underlying bull trend remains intact with prices comfortably above the 50-dma at 155.34 ahead of this week's BoJ decision - due Friday.

- The greenback is mid-range, but still holds the bulk of the post-NFP rally. Gains off the pre-NFP low remain at ~1.2% and firm CPI and/or hawkish Powell appearance could tip the USD Index north of 105.459 to mark new multi-week highs and retrace more of the downleg posted off the mid-April highs. 105.553 the next key resistance to watch.

- NOK is the furtive outperformer, but gains are mild. NOK/SEK has recovered just off the June multi-month lows posted yesterday at 0.9769, but remains bearish below 0.9870.

- Outside of the Fed decision and US data, ECB's de Guindos attends an MNI Connect event at 1400BST/0900ET, while ECB's Nagel appears just ahead of the US close.

Markets Eye Key Levels on Any USD Break Higher

- EUR/USD clearly in focus given the run-up in implied vols to YTD highs (overnight contract cleared 14 points for the first time since December), with yesterday's lows of 1.0720 well within range on any USD rally. Clearance here opens key support at 1.0601 - the Apr 16 low - in the medium-term. Options markets currently price a 14% probability of the pair below here as of July 1st, relative to the 7.5% pricing seen before Macron called for snap elections this weekend.

- The USD Index net position reached a new multi-month high in last week's CFTC update, with the net position rising to just shy of 5k contracts and nearing the longest levels of the year. This fully reverses the brief dip to a net short USD position in early April and coincides with the re-tightening of Fed pricing over the past six weeks and the building expectation for the Fed's dot plot to today confirm a shift in the median dot to 2 rate cuts for '24.

- The greenback is mid-range on the day, but still holds the bulk of the post-NFP rally. Gains off the pre-NFP low remain at ~1.2% and a firm CPI and/or hawkish Powell appearance could tip the USD Index north of 105.459 to mark new multi-week highs and retrace more of the downleg posted off the mid-April highs. 105.553 the next key resistance to watch.

USD Vols Bid to YTD Highs on Triple US Event Risk

- No surprise to see a run-up in overnight USD vols ahead of the FOMC decision later today, with markets getting an extra boost by capturing today's CPI print and Thursday's PPI. This puts overnight USD vols at YTD highs against the EUR, and close to the year's best levels against the AUD, GBP and NZD, in anticipation of a busy 24 hours for markets. See vol premiums below

- Broader options market activity remains well supported, with yesterday's session seeing volumes north of $120bln notional for the first time since the start of May. EUR hedges have been largely responsible for the uptick in activity, and particularly EUR/GBP as the cross broke below key technical support to print the lowest levels since mid-2022. Notional across EUR/GBP vanilla options is already closing in on $10bln this week alone - well ahead of average for the usual activity in the cross.

- EUR/USD overnight vols topped 14 points this morning for the first time since December last year, implying a near 65 pip swing in the pair into the Thursday NY cut - well over double the average break-even using YTD background vols.

Expiries for Jun12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0665-75(E618mln), $1.0725-45(E762mln), $1.0790-10($2.7bln)

- USD/JPY: Y155.25-30($1.3bln), Y156.00($1.3bln), Y157.00($712mln),

- GBP/USD: $1.2795-05(Gbp2.1bln)

- AUD/USD: $0.6615-30(A$3.4bln)

- NZD/USD: $0.6100(N$991mln), $0.6200(N$1.5bln)

- USD/CNY: Cny7.2500($808mln)

GERMAN DATA: Rather Encouraging CPI Details Despite Services Acceleration

German final April HICP was unrevised from the flash readings at +2.8% Y/Y (+2.4% Apr) and +0.2% M/M (+0.6% Apr). The final reading of CPI was also unrevised at +2.4% Y/Y (+2.2% Apr) and +0.1% M/M (+0.5% Mar). Core CPI printed at +3.0% Y/Y (+3.0% Mar), the lowest since March 2022.

- The final major CPI components confirmed the flash estimates: goods prices printed at +1.0% Y/Y (+1.2% Apr), services at 3.9% (+3.4% Apr). The acceleration in services inflation appears to be fully driven by the transport category on the back of the base effect on a subsidized public transport ticket ('Deutschlandticket').

- Specifically, transport came in at 2.6% (vs 0.9% Apr) - this means it added broadly about 0.38pp to the headline figure (0.13pp Apr) and 0.84pp to services (0.29 Apr) - which is even more than MNI initially estimated, and which shows that services inflation would have been broadly stable barring that base effect. The Deutschlandticket had been weighing on inflation over the past year due to base effects.

- Stability was also apparent when looking at the other services subcategories: healthcare (2.7% Y/Y May vs 2.9% Apr), recreation and culture (1.8% vs 1.8%), insurance (13.0% vs 13.1%), and restaurants and accommodation (6.3% vs 6.4%) all showed little change in their respective yearly rates.

- On the headline front, energy remained in deflationary territory but ticked up further slightly vs April at -1.1% Y/Y (-1.2% Apr). Looking at the subcategories that weren't available in the flash reading, household energy prices came in at -3.3% Y/Y (-3.2% Apr), and petrol at +2.2% (+2.0%).

- Food prices, which were one of the main inflation upside drivers through 2023 but had cooled towards the end of the year, printed similar to April, at +0.6% Y/Y (0.5%).

MNI UK Labour Market Insight: June 2024 Release

- The key private sector regular AWE came in line with the median of the analyst previews that we read at 5.83%Y/Y while total regular AWE was 5.97%Y/Y in the 3-months to April (in line with a number of analyst forecasts but the median from the surveys we read and the Bloomberg consensus were both 0.1ppt higher).

- Digging into the wage numbers, there are no large impacts from the National Living Wage increase but there appear to be sticky wages in finance and manufacturing in particular.

- We look at the potential implications for next week's inflation data from this week's labour market release.

- We also summarise more than a dozen sell-side reviews of both the labour market and UK GDP releases.

For the full PDF see:

UK_Labour_Review_2024_06_Release.pdf

GERMAN DATA: Rather Encouraging CPI Details Despite Services Acceleration

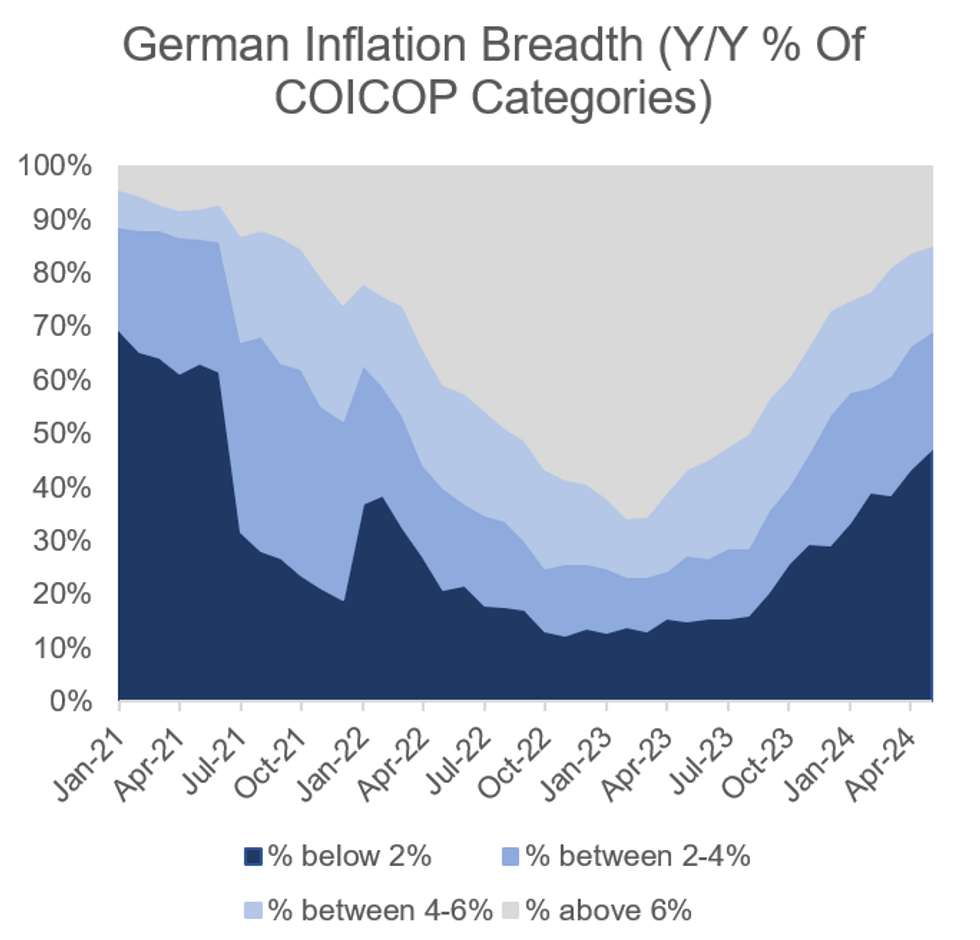

- MNI's inflation breadth tracker (see chart below) shows disinflation further progressing in May, with the percentage of categories printing at or above 6% falling to 14.8% from 16.2% in April, and the percentage of categories printing below 2% Y/Y increasing to 47.2% vs 43.5% in April.

- ECB leadership flagged that services inflation continues to be a "weak spot" within the overall inflation dynamics, so it is subject to heightened scrutiny - and its future development will be crucial for the ECB rate path going ahead.

MNI, Destatis

MNI, Destatis

E-Mini S&P Remains Above Bull Trigger, Targets 5400 Next

- The trend condition in Eurostoxx 50 futures is bullish and this week’s pullback is considered corrective. A resumption of gains would refocus attention on key resistance and the bull trigger at 5110.00, the May 16 high. Clearance of this level would confirm a resumption of the uptrend. On the downside, support at 4947.00, the Jun 4 low, has been pierced. A clear break of it would be bearish and instead expose 4894.90, a Fibonacci retracement.

- The uptrend in S&P E-Minis remains intact and the contract is trading higher today. Price has recently cleared 5368.25, the May 23 high and bull trigger. The move confirmed a resumption of the uptrend. A continuation higher would signal scope for a climb towards the 5400.00 handle next. On the downside, key short-term support has been defined at 5205.50, the May 31 low. Clearance of this level is required to signal a short-term reversal.

WTI Futures Pierce 50-Day EMA, Gains Still Considered Corrective

- WTI futures have traded higher this week. For now, short-term gains are considered corrective and the trend direction remains bearish. However, resistance at $78.36, the 50-day EMA, has been pierced. A clear break of this average would expose the key short-term resistance at $80.62, the May 1 high, where a break is required to cancel a bear theme. On the downside, a resumption of weakness would open $71.33, the Feb 5 low.

- A sharp sell-off in Gold last Friday reinforces a short-term bearish theme. The yellow metal has cleared support around the 50-day EMA, at 2313.6. The break confirms a resumption of the reversal that started May 20 and signals scope for a deeper correction near-term. This has opened $2277.4, the May 3 low. Clearance of this price point would strengthen a bearish theme. Initial firm resistance to watch is $2387.8, the Jun 7 high.

| Date | GMT/Local | Impact | Country | Event |

| 12/06/2024 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 12/06/2024 | - | Sky News- Election Leaders Event | ||

| 12/06/2024 | 1230/0830 | *** | CPI | |

| 12/06/2024 | 1230/0830 | * | Intl Investment Position | |

| 12/06/2024 | 1300/1500 | ECB's De Guindos at MNI Connect Event | ||

| 12/06/2024 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 12/06/2024 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/06/2024 | 1800/1400 | ** | Treasury Budget | |

| 12/06/2024 | 1800/1400 | *** | FOMC Statement | |

| 12/06/2024 | 1915/1515 | BOC Governor Macklem speaks at panel in Montreal. | ||

| 13/06/2024 | 0130/1130 | *** | Labor Force Survey | |

| 13/06/2024 | 0700/0900 | *** | HICP (f) | |

| 13/06/2024 | 0900/1100 | ** | Industrial Production | |

| 13/06/2024 | - | *** | Money Supply | |

| 13/06/2024 | - | *** | New Loans | |

| 13/06/2024 | - | *** | Social Financing | |

| 13/06/2024 | 1230/0830 | *** | Jobless Claims | |

| 13/06/2024 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 13/06/2024 | 1230/0830 | *** | PPI | |

| 13/06/2024 | 1230/0830 | * | Household debt-to-income | |

| 13/06/2024 | 1335/0935 | BOC Deputy Kozicki speaks on balance sheet policies. | ||

| 13/06/2024 | 1430/1030 | ** | Natural Gas Stocks | |

| 13/06/2024 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 13/06/2024 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 13/06/2024 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 14/06/2024 | 0200/1100 | *** | BOJ Policy Rate Announcement | |

| 14/06/2024 | 0430/1330 | ** | Industrial Production | |

| 14/06/2024 | 0600/0800 | *** | Inflation Report | |

| 14/06/2024 | 0645/0845 | *** | HICP (f) | |

| 14/06/2024 | 0830/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 14/06/2024 | 0900/1100 | * | Trade Balance | |

| 14/06/2024 | 0900/1100 | ECB's Lane participates at Dubrovnik Economic Conference | ||

| 14/06/2024 | 0900/1100 | ECB's De Guindos at Carlos V European Prize Ceremony | ||

| 14/06/2024 | 1230/0830 | ** | Import/Export Price Index | |

| 14/06/2024 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 14/06/2024 | 1230/0830 | ** | Wholesale Trade | |

| 14/06/2024 | 1330/1530 | ECB's Schnabel in European Fiscal Board Meeting | ||

| 14/06/2024 | 1400/1000 | ** | U. Mich. Survey of Consumers | |

| 14/06/2024 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/06/2024 | 1730/1930 | ECB's Lagarde Speech at Dubrovnik Economic Conference | ||

| 14/06/2024 | 1800/1400 | Chicago Fed's Austan Goolsbee |