Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

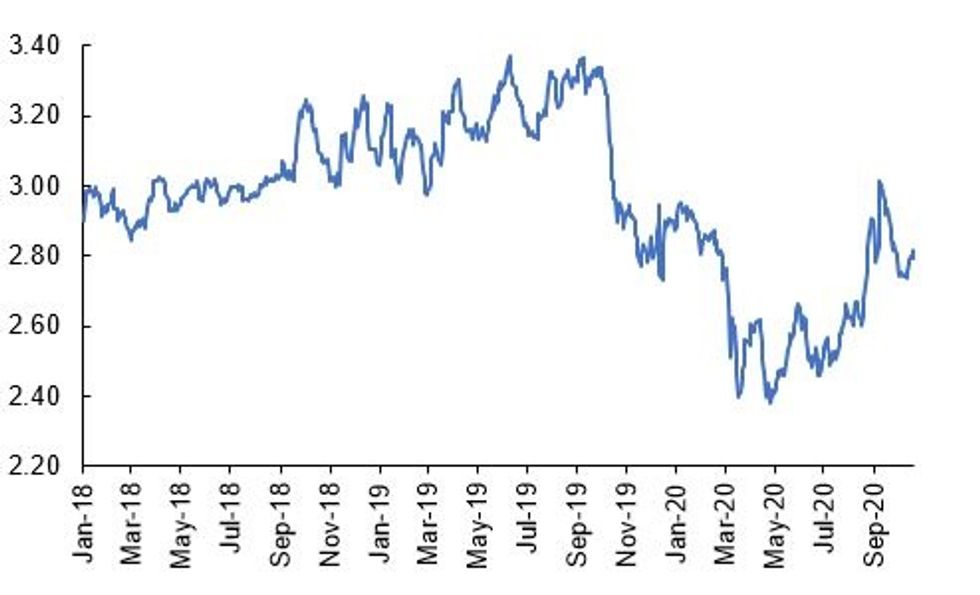

Fig 1. UK 5-Year Breakeven Rate, %

Source: MNI/Bloomberg

US TSYS SUMMARY: Stimulus Talks Head Into Overtime

Treasuries are off session lows but the direction of travel remains lower, with stimulus optimism pushing yields higher and the USD lower (DXY touching lowest levels in 6 weeks).

- Yields across the curve hitting fresh post-June highs, with bear steepening in play again. The 2-Yr yield is up 0.6bps at 0.1492%, 5-Yr is up 1.9bps at 0.3538%, 10-Yr is up 2.5bps at 0.8108%, and 30-Yr is up 2.9bps at 1.6202%. Dec 10-Yr futures (TY) down 4.5/32 at 138-18 (L: 138-13 / H: 138-24.5)

- Focus remains firmly on Washington today, as we move past House Speaker Pelosi's previously stated Tuesday deadline for a COVID stimulus deal - she and Tsy Sec Mnuchin due to speak today to reconcile outstanding differences in the deal. Pelosi's new 'deadline' is this weekend to get a bill passed by the end of next week (ie ahead of the election); Senate passage remains very much in question though.

- As with earlier in the week, the calendar is mainly about Fed speakers and not (thin) data. Cleveland's Mester speaks at 1000ET, Minn's Kashkari / Dallas' Kaplan at 1200ET, Richmond's Barkin / VC Quarles at 1300ET, and StL's Bullard at 1645ET. The latest Beige Book is released at 1400ET.

- We get 20-Yr re-open auction for $22B at 1300ET (preceded at 1130ET by 105-/154-day bill sales totalling $55B). NY Fed buys ~$1.225B of 7.5-30-Yr TIPS.

BOND SUMMARY: EGB/GILT Trade Weaker

European govies have traded weaker today alongside G10 gains against USD and fresh downside for stocks.

- Gilts have traded lower with the long-end underperforming. The 2s30s spread is 3bp wider.

- Bunds sold off early into session but have clawed back through the morning and now trade in line with yesterday's close.

- French OATs are similarly unch on the day. Last yields: 2-year -0.7093%, 5-year -0.6825%, 10-year -0.5670%, 30-year 0.3506%.

- The BTP curve has bear steepened with long-end yields inching up 3bp.

- UK CPI for September narrowing missed expectations (0.5% Y/Y vs 0.6% survey), while the public sector net borrowing requirement came in at GBP35.4bn for September, above the EUR32.4bn consensus.

- Greece is placing a Feb-35 bond through syndication today. Books were last seen above EUR14bn.

- The BoE's Ramsden will be speaking at 1310BST with Philip Lane and Luis de Guindos from the ECB will be speaking at 1455 and 1700, respectively.

- The FT reports that the UK government has abandoned spending plans which would covered the remainder of the parliament and will instead opt for a one-year review given the difficulties presented by the Covid crisis.

OPTIONS

SHORT STERLING OPTIONS: All upside structure this morning

Gist so far this morning in Sterling, has been dominated by upside structures

- 0LF1 with 0LG! 100.12/100.37c strip, bought for 6.5 in 5k

SHORT STERLING OPTIONS: Adding in bullish trade

- LH1 100.00/100.12cs 1x2 trades again for 1 in 1.5k (3k total bought).

- LG1 100.25c, bought again for 0.75 in 2k (27.5k total)

SHORT STERLING OPTIONS: 1x2 cs

LH1 100.00/100.12cs 1x2, bought for 1 in 1.5k

SHORT STERLING OPTIONS: More upside via option

LM1 100.12/100.37cs 1x1.5, bought for 3.5 in 10k (ref: 100.025)

SHORT STERLING OPTIONS: Red/Green steepener

Sterling strip Red/Green steepener

- L Z1/Z2 bought for 7 in 4k

EGB OPTIONS: Bund upside

RXX0 176.0/176.5/177 c ladder, bought for 6 in 1.2k

TECHS

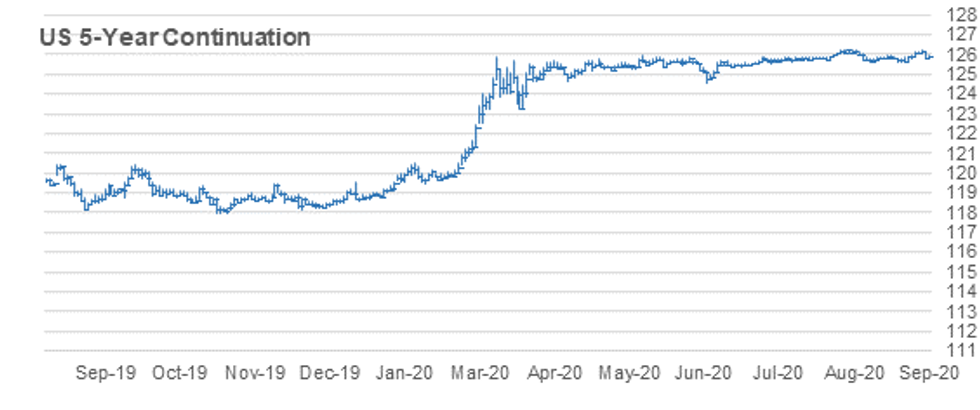

US 5YR FUTURE TECHS: (Z0) Trades Through Key Support

- RES 4: 125-316 High Oct 5

- RES 3: 125-30+ 61.8% retracement of the Sep 30 - Oct 7 sell-off

- RES 2: 125-31 High Oct 15

- RES 1: 125-26 High Oct 19

- PRICE: 125-21+ @ 11:33 BST Oct 21

- SUP 1: 125-19 Intraday low

- SUP 2: 125-18 Low Aug 28 (cont)

- SUP 3: 125-16+ 1.00 proj of Aug 4 - 13 sell-off from Sep 3 high

- SUP 4: 125-112 Low Jun 10 (cont)

5yr futures maintain a softer tone. The recent sell-off from 125-31, Oct 15 high has extended lower today resulting in a break of key support at 125-202,Oct 7 low. The break confirms a resumption of the downtrend that has been in place since early August. This paves the way for weakness towards 125-16+ next, a Fibonacci projection. Key short-term resistance is at 125-31.

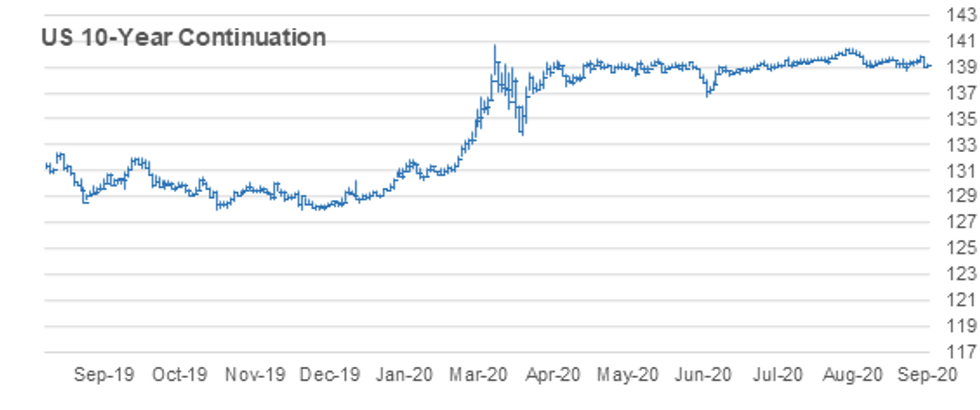

US 10YR FUTURE TECHS: (Z0) Key Support Cleared

- RES 4: 139-25 High Oct 2

- RES 3: 139-17 76.4% retracement of the Sep 29 - Oct 7 sell-off

- RES 2: 139-14 High Oct 15

- RES 1: 139-01+ High Oct 20

- PRICE: 138-19+ @ 11:44 BST Oct 21

- SUP 1: 138-13+ Intraday low

- SUP 2: 138-12 61.8% retracement of the Jun - Aug rally (cont)

- SUP 3: 138-04+ 1.00 proj of Aug 4 - 28 decline from Sep 3 high

- SUP 4: 137-29 76.4% retracement of the Jun - Aug rally (cont)

Treasuries remain weaker following the strong reversal off 139-14, Oct 15 high. Earlier, futures traded sharply lower resulting in a break of the key support at 138-18+, Aug 28 low and the bear trigger. The move lower confirms a resumption of the reversal that occurred on Aug 4. This has opened 138-04+, a Fibonacci projection. Firm resistance is at 139-14, Oct 15 high with initial resistance at 139-01+.

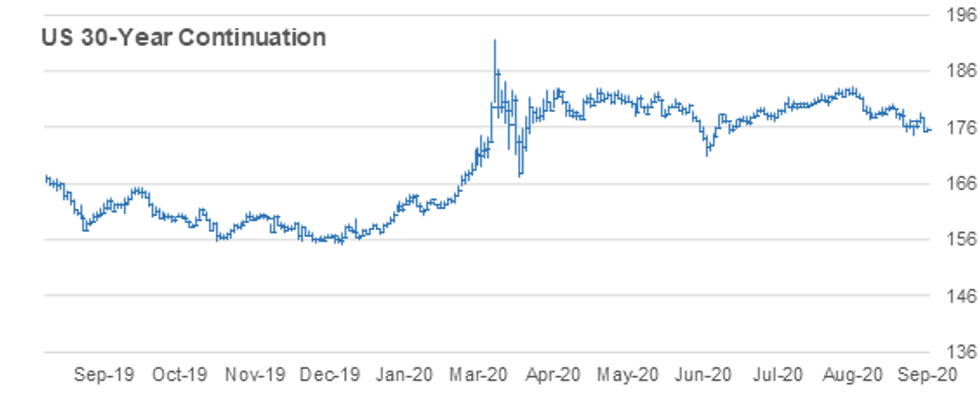

US 30YR FUTURE TECHS: (Z0) Bearish Trend Resumes

- RES 4: 177-00 High Oct 2

- RES 3: 176-10 High Oct 15

- RES 2: 175-18 Trendline resistance drawn off the Aug 6 high

- RES 1: 174-14 High Oct 20

- PRICE: 173-07 @ 11:52 BST Oct 21

- SUP 1: 172-17 Low Jun 5 (cont) and intraday low

- SUP 2: 172-13 0.764 proj of Aug 6 - 28 downleg from Sep 3 high

- SUP 3: 172-00 Round number support

- SUP 4: 170-19 1.00 proj of Aug 6 - 28 downleg from Sep 3 high

30yr futures remain bearish having started the week on a softer note. Price has traded below key support at 173-10 Oct 7 low. The break negates recent bullish developments and instead confirms a resumption of the downtrend that has been in place since the Aug 6 reversal. This opens 172-17 (tested today), Jun 5 low (cont) and 172-13, a Fibonacci projection. Key resistance has been defined at 176-10, Oct 15 high.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.