Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

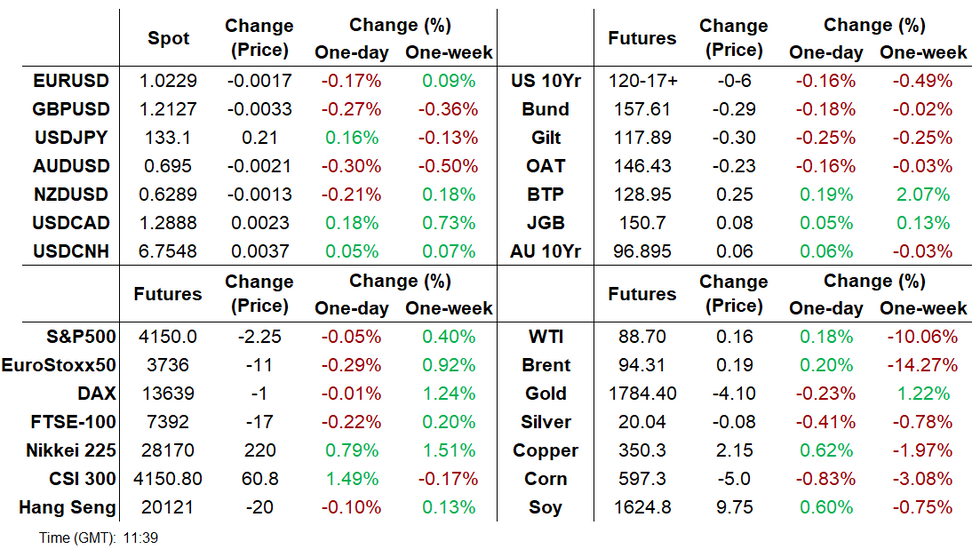

- Equities are flat with the USD a little firmer ahead of July's US nonfarm payrolls report

- Analysts see a slowdown in job growth in July: MNI dealer median +270k vs +372k in June

- Treasuries have cheapened slightly, shrugging off the latest China-US escalations overnight

US TSYS: Fading Latest US-China Escalation Ahead Of Payrolls

- Cash Tsys trade modestly cheaper across the curve this morning ahead of payrolls as they consolidate yesterday’s rally after particularly large swings this week (2YY range of 2.815%-3.198%). There has been little obvious haven demand from China cutting ties to the US in retaliation to Pelosi’s Taiwan visit, increasing the risk of miscalculation in the Taiwan Strait and South China Sea with military and maritime lines cut.

- FOMC speakers continue to push back on yield curve indicators of recession - most recently Mester yesterday - but 2s10s are back near yesterday’s intraday fresh post-2000 lows, currently at -36bps.

- 2YY +1.6bps at 3.059%, 5YY +0.7bps at 2.799%, 10YY +0.7bps at 2.695% and 30YY +0.7bps at 2.973%.

- TYU2 trades 6 ticks lower at 120-17+ on soft volumes, towards the middle of the week’s range. Short-term technical trend conditions are bullish whilst above key support at the 50-day EMA of 119-05, whilst resistance is seen at 122-02 (Aug 2 high).

- Data: Payrolls at 0830ET clearly dominates the docket. See MNI’s full preview here: https://marketnews.com/mni-payrolls-preview-just-how-much-slower

- Fedspeak: Barkin (’24 voter) at 0800ET with Q&A.

- No issuance.

STIR FUTURES: Range Bound Ahead of Payrolls

- Fed Funds implied hikes for Sept sit at 60.5bps, the middle of the wide post-July FOMC range of 55-65bps.

- Beyond Sept, hikes sit towards the higher end of the range with a cumulative 108bps priced to year-end or 113bps to a current peak seen in Feb'23 at 3.46% before 50bp of cuts to Dec'23, having seen only a small boost after Mester ('22) said she sees rates peaking a little over 4% next year.

- Prior to payrolls, Barkin ('24) speaks to the Lexington Chamber of Commerce with Q&A at 0800ET. Remarks from two days ago included recession fears look inconsistent given jobs growth but a recession could happen, whilst expecting inflation to not ease immediately or predictably.

FOMC-dated Fed Funds implied rate at specific meetings plus Dec22-23 curve (green)Source: Bloomberg

FOMC-dated Fed Funds implied rate at specific meetings plus Dec22-23 curve (green)Source: Bloomberg

EGB/Gilt - Positioning ahead of NFP

- EGBs and Bund are offered, on likely positioning ahead of the US NFP, although Italian BTP outperforms in early trade, pushing the BTP/Bund spread 1.8bps tighter so far in early trade.

- Greece is still in the lead and sits 3.9bps tighter against the German 10yr.

- Bund is drifting lower as the US starts to come in and has tested small initial support noted at 157.57, printed 157.58 low so far.

- Gilt/Bund spread was initially wider, after it broke through the April high yesterday, that was 106.10.

- Next psychological level is at 110.00bps, but better is seen towards 112.00bps.

- The spread is now widest since 25th March, but is flat at the time of typing.

- Focus turns to the US NFP release, speakers include BoE Pill and Fed Barkin.

- Sep Bund futures (RX) down 27 ticks at 157.63 (L: 157.58 / H: 158.21).

- Germany: The 2-Yr yield is up 1.7bps at 0.36%, 5-Yr is up 3.3bps at 0.577%, 10-Yr is up 2.7bps at 0.83%, and 30-Yr is up 1.2bps at 1.051%.

- Sep Gilt futures (G) down 28 ticks at 117.91 (L: 117.76 / H: 118.14).

- UK: The 2-Yr yield is down 1.1bps at 1.843%, 5-Yr is up 0.2bps at 1.724%, 10-Yr is up 2.2bps at 1.911%, and 30-Yr is up 1.1bps at 2.298%.

- Sep BTP futures (IK) up 22 ticks at 128.92 (L: 128.51 / H: 129.07)

- Sep OAT futures (OA) down 24 ticks at 146.42 (L: 146.37 / H: 146.86)

- Italian BTP spread down 3bps at 210.3bps

- Spanish bond spread down 0.5bps at 109.3bps

- Portuguese PGB spread down 0.8bps at 101.3bps

- Greek bond spread down 2.5bps at 213.9bps

US NONFARM PAYROLLS (MNI PREVIEW)

Consensus sees nonfarm payrolls growth moderating in July in a resumption of a downward trend after four remarkably steady months as the gap on pre-pandemic employment levels is almost completely shut. Particular focus is likely on the strength of jobs growth plus any differences between establishment and household surveys, with FOMC speakers putting weight on labour market strength as evidence against the economy already being in recession.

PREVIEW: Primary Dealer NFP Estimates

| Primary Dealer | Estimate | Primary Dealer | Estimate |

|---|---|---|---|

| Amherst Pierpoint | +325K | RBC | +320K |

| Citi | +300K | Credit Suisse | +300K |

| Morgan Stanley | +300K | TD Securities | +300K |

| Scotiabank | +290K | BNP Paribas | +280K |

| Bank of America | +275K | Barclays | +275K |

| Daiwa | +275K | NatWest | +270K |

| Jefferies | +260K | Deutsche Bank | +250K |

| HSBC | +250K | Nomura | +240K |

| Wells Fargo | +240K | Goldman Sachs | +225K |

| Societe Generale | +225K | J.P.Morgan | +200K |

| Mizuho | +200K | BMO | +150K |

| UBS | +150K | ||

| Dealer Median | +270K | BBG Whisper | +226K |

EUROPE ISSUANCE UPDATE

Belgium ORI auction results:

- E201mln of the 1.25% Apr-33 Green OLO. Avg yield 1.381% (bid-to-cover 3.88x).

- E212mln of the 2.25% Jun-57 OLO. Avg yield 2.045% (bid-to-cover 1.19x).

BOND / RATE OPTIONS SUMMARY

Europe:

- DUU2 109.90/109.70/109.50p fly, was bought for 2.5 in 3k

US:

- FVV2 111.75/111.00 ps sold at 9.5 in 7.5k

FOREX: USD is in the green ahead of the NFP

- The Dollar trades in the green ahead of the US data, some of the move lower in Equities, has underpinned the USD.

- Desks are also likely positioning, but low turnovers, suggest that most market participants are on the sideline.

- After being mostly in the green, but still short of pre BoE levels, the GBP is mostly back in the red.

- At session low against the USD and the EUR, and after leading vs the Yen, it continues to unwind.

- Support in Cable moves up to 1.2101 initially.

- Vs the EUR, would need the latter to drift back towards 0.8359, for pre BoE level.

- Looking ahead, US NFP's range is 50k to 325k.

- Median is 250k, whisper is 226k.

- The 10 top ranked Bloomberg Economists surveyed, have a range of 180k to 280k.

FX OPTION EXPIRY

Of note:

EURUSD 2bn at 1.0200

USDCAD 1.03bn at 1.2900

USDJPY 2.05bn at 134.00- EURUSD: 1.0100 (379mln), 1.0175 (205mln), 1.0195 (318mln), 1.0200 (2bn), 1.0300 (1.24bn).

- EURGBP: 0.8350 (1.48bn), 0.8450 (750mln)

- USDJY: 133.25 (410mln), 133.30 (286mln), 133.75 (284mln), 134.00 (2.05bn), 135.00 (1.09bn).

- GBPUSD: 1.2100 (590mln)

- USDCAD: 1.2800 (1.46bn), 1.2900 (1.03bn)

- AUDUSD: 0.6900 (464mln), 0.6950 (498mln)

- AUDNZD; 1.0950 (800mln)

PRICE SIGNAL SUMMARY: Gold Approaches A Key 5-Month Trendline Resistance

- In the equity space, current bullish conditions in S&P E-Minis remains intact. Fresh highs this week reinforces the current trend direction and this signals scope for a climb towards 4204.75 next, May 31 high and the next key resistance. Initial key support is 3991.98, the 50-day EMA. EUROSTOXX 50 futures trend conditions remain bullish and yesterday’s high print reinforces this theme. The contract has breached the 76.4% retracement of the Jun 6 - Jul 5 downleg, at 3722.40. Scope is seen for gains towards 3840.00, the Jun 6 high. Initial firm support to watch is 3592.30, the 50-day EMA.

- In FX, the EURUSD short-term outlook is bullish and the pair remains above support at 1.0097, the Jul 27 low. A resumption of gains would signal scope for an extension higher within the bull channel - the top intersects at 1.0379. Weakness below 1.0097 would alter the picture. A bullish short-term theme in GBPUSD remains intact. Price has recently traded above the 50-day EMA. This reinforces current conditions with the next objective at 1.2332, the Jun 27 high. Potential is also seen for a climb towards 1.2406, the Jun 16 high and a key resistance. Initial firm support to watch lies at 1.2063, the Jul 29 low. USDJPY remains above support at 130.41, Tuesday’s low. Gains are - for now - considered corrective. A resumption of weakness would open 130.00. Initial resistance is at 135.09, the 20-day EMA.

- On the commodity front, Gold maintains a firmer tone. The yellow metal has breached the 50-day EMA and attention is on trendline resistance at $1802.1. A breach of the trendline would represent an important technical break and highlight a stronger reversal of the 5-month downtrend. A break would open $1825.1, the Jun 30 high. Initial firm support lies at $1754.4 the Aug 3 low. In the Oil space, WTI futures remain vulnerable and yesterday’s extension lower reinforces current bearish conditions. Price has breached support at $88.23, Jul 14 low and a key support. This opens $91.22, Jul 14 low.

- In the FI space, a short-term bull cycle in Bund futures remains intact. Scope is seen for a climb to 159.79 next, the Apr 4 high (cont). Initial firm support is 154.77, the 20-day EMA. The trend condition in Gilts remain bullish and pullbacks are considered corrective. A resumption of gains would open 120.00. Support is at 116.93 20-day EMA.

EQUITIES AND COMMODITIES

Equities:

- Asia: Japan's NIKKEI closed up 243.67 pts or +0.87% at 28175.87 and the TOPIX ended 16.44 pts higher or +0.85% at 1947.17. China's SHANGHAI closed up 37.988 pts or +1.19% at 3227.027 and the HANG SENG ended 27.9 pts higher or +0.14% at 20201.94.

- Europe: German Dax down 12.27 pts or -0.09% at 13639.28, FTSE 100 down 10.7 pts or -0.14% at 7434.84, CAC 40 down 34.57 pts or -0.53% at 6481.1 and Euro Stoxx 50 down 12.97 pts or -0.35% at 3739.

- US: Dow Jones mini up 30 pts or +0.09% at 32711, S&P 500 mini down 1.75 pts or -0.04% at 4150.5, NASDAQ mini down 21.5 pts or -0.16% at 13305.5.

Commodities:

- WTI Crude down $0.09 or -0.1% at $88.46

- Natural Gas down $0.1 or -1.21% at $8.059

- Gold spot down $7.11 or -0.4% at $1786.4

- Copper up $1.4 or +0.4% at $349.8

- Silver down $0.15 or -0.76% at $20.0722

- Platinum up $7.52 or +0.81% at $939.99

| Date | GMT/Local | Impact | Flag | Country | Event |

| 05/08/2022 | 1115/1215 |  | UK | BOE Pill Monetary Policy Report National Agency Briefing | |

| 05/08/2022 | 1200/0800 |  | US | Richmond Fed's Tom Barkin | |

| 05/08/2022 | 1230/0830 | *** |  | CA | Labour Force Survey |

| 05/08/2022 | 1230/0830 | *** | | US | Employment Report |

| 05/08/2022 | 1400/1000 | * | | CA | Ivey PMI |

| 05/08/2022 | 1900/1500 | * | | US | Consumer Credit |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok