Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI US OPEN: Concerns Over Delta Variant Mount

HIGHLIGHTS:

- European govies trade mixed while the dollar is broadly bid alongside equity gains

- Covid restrictions continue to tighten in several countries as the delta variant surges

- The inaugural NextGenerationEU bond will be launched today

Source: MNI, Bloomberg

NEWS

GERMANY (FT): German finance minister Olaf Scholz has dismissed calls for reform of German and EU fiscal rules, saying they provide enough flexibility to overcome crises such as the pandemic. But in an interview with the Financial Times, Scholz, who is also the Social Democrats' candidate for chancellor in September's federal election, said Germany must continue its big-spending plans next year to avoid a hard economic landing. "We fared better economically than anyone would have expected in the midst of the crisis because we pursued an expansionary fiscal strategy," he told the FT. "We mustn't abruptly stop the measures we took to ensure the economic recovery."

FRANCE (FT): The Delta variant of Covid-19, which was first detected in India and has swept across the UK, now accounts for around 20 per cent of new cases in France, the country's health minister Olivier Veran said on Tuesday. The proportion has doubled from 10 per cent over the past week. The overall number of Covid-19 cases is continuing to fall however, with only 509 new infections reported on Monday.

UK (GUARDIAN): Ministers are facing demands to re-examine 85 oversight jobs across Whitehall amid questions over Conservative government appointments to the health department. Concerns were raised after it emerged that Matt Hancock had appointed Gina Coladangelo, whom he was pictured kissing in his office in May, as a non-executive director at the Department of Health and Social Care (DHSC) last year. She was paid £15,000 for 15 days' work a year in a role that included scrutinising his performance as a minister.

SOUTH AFRICA (BLOOMBERG): Jacob Zuma, who's been repeatedly implicated in aiding and abetting the plunder of state funds during the nine years he led South Africa, was sentenced to 15 months in jail for defying a court order to testify at a graft inquiry. The Constitutional Court ruled in January that Zuma had to respond to questions from a judicial commission headed by Deputy Chief Justice Raymond Zondo. But the 79-year-old former intelligence operative accused the court and Zondo of bias, walked out of one scheduled panel hearing in November and boycotted another in February. The panel responded by filing contempt charges against him. "This sends an unequivocal message in this our constitutional dispensation, the rule of law and the administration of justice prevails," acting Chief Justice Sisi Khampepe said in a ruling in Johannesburg on Tuesday.

DATA

FRANCE DATA: Consumer Sentiment At 15-Mo High

FRANCE JUN CONSUMER CONF IND 102; MAY 98r

Consumer confidence rose 4pt to 102 in Jun, beating expectations (100), hitting the highest level since Mar 2020.

Jun's uptick was broad-based, but most notably the fear of unemployment eased by 19pt, showing the lowest level since Mar 2020.

While savings intentions eased to a 6-month low, the intentions to make major purchases gained 10pt and rose to the highest reading since Feb 2018.

However, consumer's expected savings capacity hit a new record high, up 2pt in June.

Household's assessment of their future financial situation and the general economic conditions in the next year increased significantly by 6pt and 8pt, respectively.

Restrictions continue to be eased in France and vaccinations are progressing which provides a boost to household confidence.

SPAIN DATA: JUN FINAL CPI UNREVISED FROM FLASH

SPAIN JUN FINAL CPI UNREVISED FROM FLASH

GERMANY DATA: SAXONY JUN FOOD PRICES -0.2% M/M

SAXONY JUN FOOD PRICES -0.2% M/M

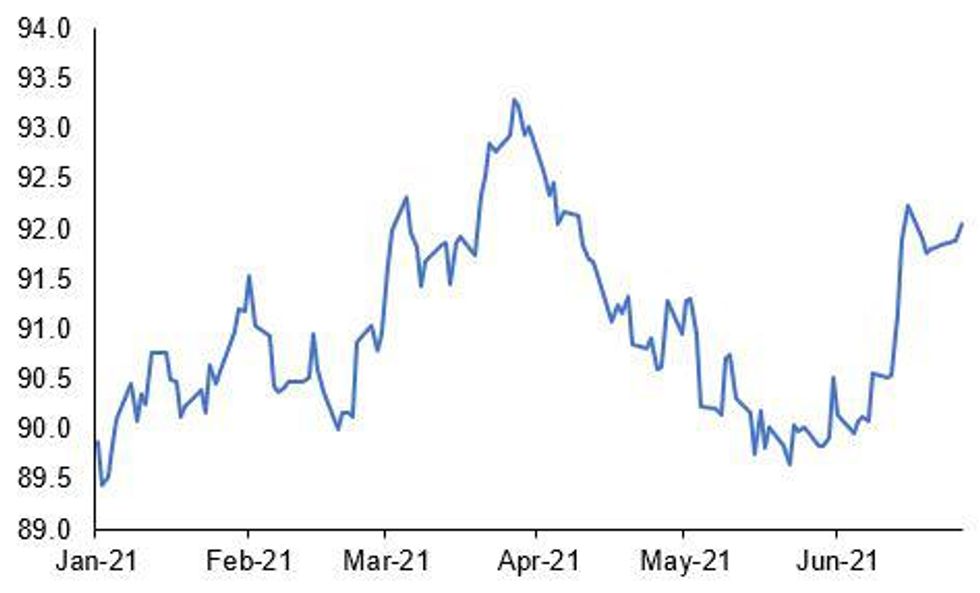

EUROZONE DATA: ESI Eased in January

Economic Sentiment Indicator (ESI): 91.5; Prev (Dec): 92.4

Consumer: -15.5 (Dec: -13.8); Industry: -5.9 (Dec: -6.8); Services: -17.8 (Dec: -17.1); Retail: -18.9 (Dec: -12.9); Construction: -7.7 (Dec: -8.0)

- The EZ ESI slipped 0.9pt to 91.5 in Jan, however coming in stronger than markets expected (BBG: 89.4).

- The index still remains below Feb's pre-crisis level.

- Among the largest EZ economies, the ESI saw the largest falls in France (-2.6pt to 90.4) and Germany (-2.3pt to 92.8), while it improved in Spain (+2.4pt to 93.9), the Netherlands (+0.6pt to 94.8) and Italy (+0.4pt to 90.2).

- Industrial sentiment improved further in Jan, rising to -5.9 and showing the second consecutive gain.

- The construction sector saw an uptick in sentiment as well to -7.7, marking the highest level since Mar.

- On the other hand, service and retail trade sentiment deteriorated further to -17.8 and -18.9, respectively.

- Service confidence saw the lowest level since July, while retail trade sentiment dropped to seven month low.

- Consumer confidence remains well below the pre-crisis level with the index declining to -15.5 in Jan, down from -13.8 seen in Dec.

- The employment expectations index eased 1.6pt to 88.8 in Jan, following Dec's uptick to 90.4.

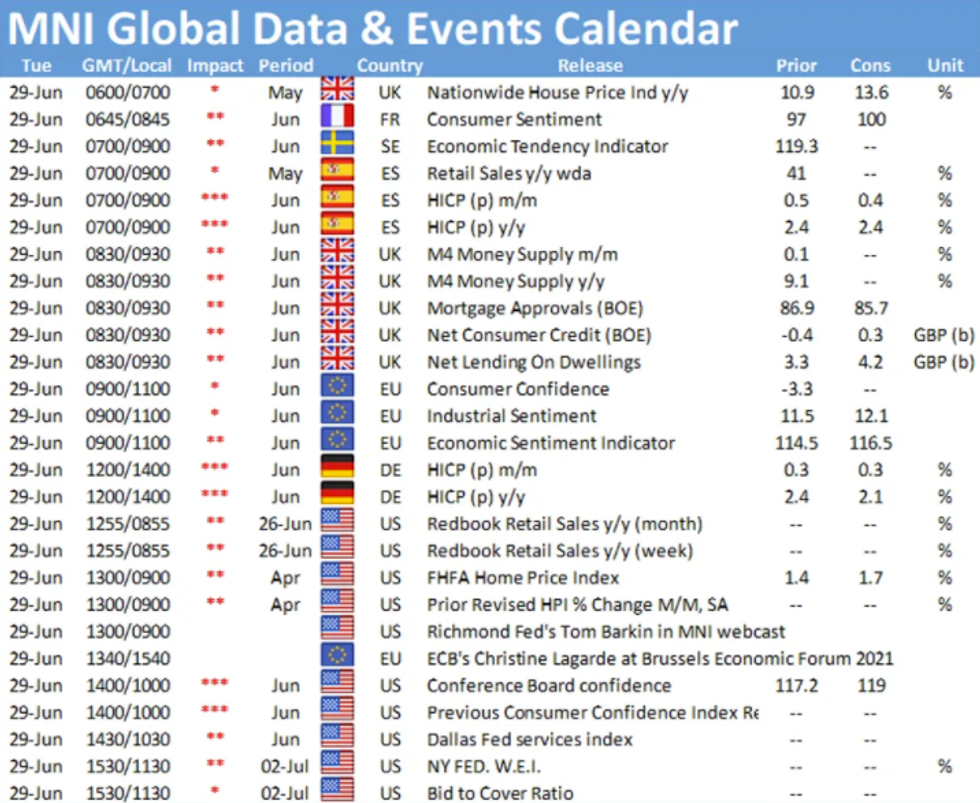

FIXED INCOME: NGEU syndication the highlight

- The main event for Eurozone bonds this morning will be the inaugural launch of the NextGenerationEU bond, with a 10-year bond due to be sold via syndication. We look for a transaction size of E10-12bln.

- There are a number of ECB speakers today (de Cos, Lane, Panetta, Holzmann) with Lane's opening remarks at the ECB Conference on Forecasting Techniques likely the highlight (due at 12:00BST).

- The European data calendar is rather light this morning with final inflation prints and trade data the highlights. However US data will be closely watched ahead of tomorrow's FOMC decision. PPI is the highlight but retail sales and industrial production are both also significant.

- In terms of other supply this morning, Germany looks to sell Schatz for E5bln, Finland 7/10-year RFGBs for E1.5bln while Spain and the ESM both look to sell bills.

- Bund futures are up 0.02 today at 172.66 with 10y Bund yields down -0.4bp at -0.256% and Schatz yields unch at -0.678%.

- BTP futures are down -0.03 today at 151.94 with 10y yields down -0.3bp at 0.776% and 2y yields down -0.4bp at -0.396%.

FOREX: USD Is Favoured

The story so far during the morning European session, has been the better bid in the USD.

- The currency extended higher across the board and is up across G10s and EM, and that's despite risk still tilted to the upside, with Mini S&P hovering near all time high.

- Worst performers against the Greenbacks are the Kiwi, the Aussie and the NOK, all down above half a percent at the time of typing.

- AUD is weighted by further lockdown, with Perth joining Sydney and Darwin.

- USDNOK is up 0.52% and now eye the 22/06 high at 8.6151.

- In terms of Month End flow, this has so far been limited, with very little reported from desks.

- Citi's prelim month-end model for June indicates slight USD sales.

- And Barcap, preliminary run of month-end rebalancing model points to moderate USD selling against all majors.

- Looking ahead, more speakers are scheduled but unlikely to hear anything new, since we have heard from them previously.

- Today includes, Fed Barkin (At MNI Event), and ECB Lagarde, Villeroy, Weidmann, BoE Hauser.

- Attention though, is already turning to the US NFP Friday.

EQUITIES: European and US stocks a bit higher

- Japan's NIKKEI down 235.41 pts or -0.81% at 28812.61 and the TOPIX down 16.19 pts or -0.82% at 1949.48

- China's SHANGHAI closed down 33.194 pts or -0.92% at 3573.178 and the HANG SENG ended 274.2 pts lower or -0.94% at 28994.1

- German Dax up 79.75 pts or +0.51% at 15637.48, FTSE 100 up 6.78 pts or +0.1% at 7082.55, CAC 40 up 13.46 pts or +0.21% at 6573.96 and Euro Stoxx 50 up 10.32 pts or +0.25% at 4101.43.

- Dow Jones mini up 11 pts or +0.03% at 34173, S&P 500 mini down 4 pts or -0.09% at 4277.25, NASDAQ mini down 30.75 pts or -0.21% at 14480.5.

COMMODITIES: Generally lower

- WTI Crude down $0.36 or -0.49% at $72.54

- Natural Gas up $0 or +0.11% at $3.598

- Gold spot down $8.28 or -0.47% at $1770.2

- Copper down $5.6 or -1.31% at $422.25

- Silver down $0.16 or -0.63% at $25.9476

- Platinum down $15.96 or -1.46% at $1079.66

LOOK AHEAD

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.